Michail_Petrov-96/iStock via Getty Images

Michail_Petrov-96/iStock via Getty Images

Cogent Biosciences, Inc. (NASDAQ:COGT) stock is soaring today after the Waltham, Massachusetts based biotech announced via a press release today that it has:

entered into a securities purchase agreement for a private investment in public equity financing that is expected to result in gross proceeds of approximately $225 million to the Company, before deducting placement agent fees and offering expenses.

This financing was led by Commodore Capital and a large investment management firm and included participation from both new and existing investors, including Fairmount Funds, Redmile Group, Janus, TCGX, Adage Capital Partners LP, Venrock Healthcare Capital Partners, Deerfield and Perceptive Advisors.

J.P. Morgan Securities LLC, Jefferies LLC and Piper Sandler & Co. acted as placement agents.

Cogent has agreed to sell 17m shares of its common stock at a price of $7.5 per share. At close of business yesterday, 13th February, the company's stock traded at ~$5.5 per share, which partly explains the surge in value today, although shares have exceeded the "PIPE" financing price in value, trading at ~$9 per share at the time of writing, up ~65% for the day.

The press release goes on to say:

Cogent intends to use the net proceeds from the proposed financing to fund research and development, activities relating to bezuclastinib and other product candidates, as well as for working capital and general corporate purposes.

The proceeds from this financing, combined with current cash, cash equivalents and marketable securities, are expected to fund Cogent into 2027 and through all clinical readouts from SUMMIT, PEAK and APEX registration-directed trials.

To secure a funding runway until 2027, especially for a biotech of Cogent's relatively small size, with <150 employees (as of the end of 2022), is clearly good news for the company, but for the raise to be oversubscribed, with a who's who of biotech investment firms participating, seems to imply the company may have further good news to share with investors soon.

Given the company is overwhelmingly focused on the development of a single asset - bezuclastinib,

"also known as CGT9486, a highly selective tyrosine kinase inhibitor designed to potently inhibit the KIT D816V mutation as well as other mutations in KIT exon 17,"

according to its Q3 2023 10Q submission / quarterly report. It is probably safe to assume that share price needle-moving news will soon be shared in relation to this asset.

Bezuclastinib is being developed to target two separate disease indications, - systemic mastocytosis ("SM"), and gastrointestinal stromal tumors ("GIST").

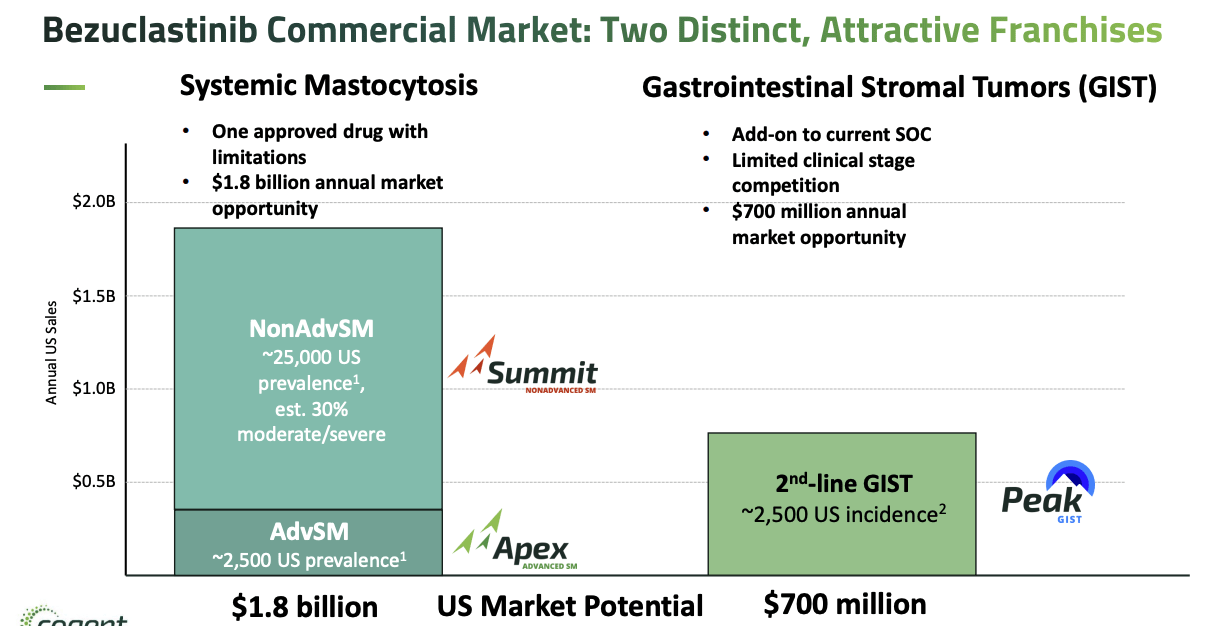

bezuclastinib target indications / markets (Cogent JP Morgan Healthcare Conference presentation)

As we can see above, in a slide taken from a presentation Cogent gave at this year's JP Morgan Healthcare conference in January, the SM market is estimated by Cogent management to be worth ~$1.8bn in total, split into two distinct indications, advanced SM, and non-advanced SM, which encompasses a patient population of ~25k patients - 10x the prevalence of advanced SM patients. Cogent believes the GIST market is worth ~$700m, based on a patient population of ~2.5k in the U.S.

According to Cogent's quarterly report:

In the vast majority of cases, KIT D816V is responsible for driving Systemic Mastocytosis ("SM"), a serious and rare disease caused by unchecked proliferation of mast cells. Exon 17 mutations are also found in patients with advanced gastrointestinal stromal tumors ("GIST"), a type of cancer with strong dependence on oncogenic KIT signaling.

Blueprint Medicines (BPMC), a $4.7bn market cap, Cambridge, Massachusetts-based commercial stage pharma, has secured approval for its drug avapritinib, marketed and sold under the brand name Ayvakit, in both the advanced and non-advanced forms of SM, in 2021, and in May this year, respectively. Like Bezuclastinib, the drug works by inhibiting KIT D816V.

In Q3 of 2023, Ayvakit brought in revenues of $54.2m, up from $39.9m in the prior quarter, doubtless thanks to its new approval in non-advanced SM, the much larger market. The company estimated that ~800 patients were using its therapy, and has suggested that it can grow that figure to ~7.5k patients, and that "blockbuster potential is highly achievable" i.e., revenues of >$1bn per annum.

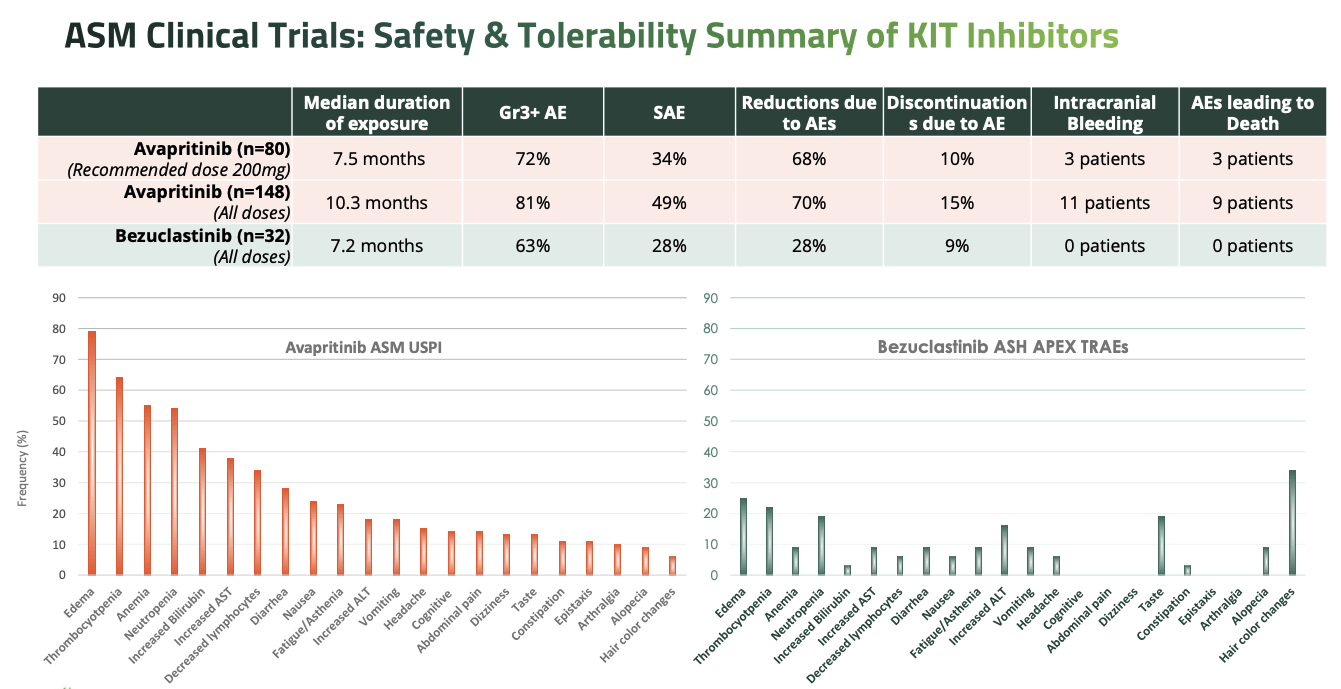

Cogent's contention however is that Bezuclastinib is a superior drug compared to avapritinib / Ayvakit, being more potent, selective and safer than Blueprint's drug. This has to some extent been suggested by preclinical studies carried out by the company, in which its drug targeted more mast cells in a shorter space of time than avapritinib, with less off-target toxicity.

Most importantly, Bezuclastinib demonstrates minimal brain penetration - Ayvakit carries a boxed warning from the Food and Drug Agency ("FDA") around cases of intracranial haemorrhage.

In SM, Cogent is trying to prove its superiority through two Phase 2 clinical studies. The first is APEX, a:

"global, open-label, multi-center, Phase 2 clinical trial in patients with AdvSM evaluating the safety, efficacy, pharmacokinetic, and pharmacodynamic profiles of bezuclastinib."

In December 2022, Cogent revealed positive data from this study, showing a 56% objective response rate ("ORR") in Tyrosine Kinase Inhibitor ("TKI") naive patients. 100% of 32 patients treated with the 100mg twice daily dose (likely ~8 of 32 patients in the study received this dose) achieved a partial response ("PR") or better, and a 75% ORR per pure pathological response ("PPR") criteria, including 86% ORR for TKI-treatment-naïve patients.

The press release also stated that "Cogent continues to actively enroll Part 2 of the APEX trial which is expected to include approximately 65 AdvSM patients and is on track to complete enrollment by the end of 2024." Additionally, as we can see below, the safety profile of Bezuclastinib was apparently superior to Ayvakit (with the caveat that the below slide is taken from a Cogent presentation, and that it is not usually a good idea to cross-compare different studies).

safety of Bezuclastinib vs Ayvakit compared (Cogent presentation)

Meanwhile, Cogent is also running the SUMMIT study, a randomized, global, multicenter, double-blind, placebo-controlled, multi-part Phase 2 clinical trial for patients in the larger indication of Non-AdvSM. The company also updated on this study in December last year, with headline data presented as follows:

- Rapid and ongoing improvement in patient symptoms, with 57% median best improvement on MC-QoL (Mastocytosis Quality of Life Questionnaire) and 78% of patients reporting ≥1 point improvement on PGIS (Patient Global Impression of Severity) by week 20

- 100% of bezuclastinib treated patients achieved at least 50% improvement across all relevant biomarker measures, including serum tryptase, KIT D816V VAF, and mast cell burden;

- Placebo patients, after cross-over to bezuclastinib, also demonstrated rapid symptomatic improvement, with 75% median best improvement on MC-QoL, and 67% of patients reporting ≥1 point improvement on PGIS

- Bezuclastinib safety and tolerability profile supports potential for chronic dosing with no related serious adverse events and no bleeding or cognitive events

Additionally, the press release states that:

Cogent completed enrollment in SUMMIT Part 1 and plans to initiate SUMMIT Part 2, a registration-directed, global, randomized placebo-controlled trial in the first half of 2024. In addition, Cogent plans to present data from the completed SUMMIT Part 1 trial (1a and 1b), including all 54 patients enrolled across Part 1a and Part 1b, in the first quarter of 2024.

Finally, Cogent is most advanced in its smallest indication of GIST, with a Phase 3 PEAK study ongoing, in which Bezuclastinib is used in combo with sunitinib, marketed and sold by Pharma giant as Sutent, and compared to Sutent alone. The study is expected to be fully enrolled by the end of this year.

Considering the below list of upcoming data catalysts, it is tempting to wonder if Cogent's sharing data at the upcoming 2024 American Academy of Allergy, Asthma and Immunology (AAAAI) annual meeting, which will start on 22nd February, constitutes a potentially major catalysts for shareholders to consider, and possibly a positive one, given Cogent's PIPE financing announced today.

The SUMMIT study is the most important for Cogent in terms of market opportunity, although it may be worth asking if a drug can be approved to treat non-advanced SM before it is approved to treat the advanced form. There is unmet need in both indications, although as Cogent states in its latest quarterly report:

Patients with AdvSM have a significantly diminished lifespan with a median survival of less than 3.5 years. For patients with Non-AdvSM, while their lifespan is not impacted by the disease, these patients suffer from a poor quality of life and new treatment options are badly needed.

Frankly, given Cogent is not apparently sharing any other data readouts in 2024, the data due this month could have a significant impact on how Cogent is valued by the market for the rest of the year, which is why I am drawing reader attention to it, although there are some other developments to consider, not least the emergence of new competitors.

For example, Blueprint Medicines has not been resting on its laurels, and has developed a next generation version of Ayvakit that it says is non-brain penetrant, handing it the same advantage over the original drug that Cogent suggests it has. Blueprint is also a cash-rich company, reporting $827m of cash in its Q3 earnings reporting.

A cross trial comparison table comparing Ayvakit, Blueprint's latest candidate elenestinib, and bezuclastinib has been shared by oncologypipeline.com, although it is hard to draw many conclusions as Blueprint's Harbor study and Cogent's SUMMIT study apparently have differing endpoints and objectives.

The reality is that Cogent experienced a difficult year in 2023, firstly due to Blueprint securing approval in the non-AdvSM market, handing Blueprint a substantial first-mover advantage in this large, potentially blockbuster market, and secondly as analysts gave Cogent's Phase 2 data the thumbs down, in December, suggesting bezuclastinib is not sufficiently differentiated to Ayvakit, let alone Blueprint's next-generation candidate.

Cogent stock was riding high at $15 per share in January last year, but one year on the share price had declined to ~$4. As such, today's lift, generated by news of the PIPE financing, was much needed, and arguably hints at an intriguing data readout set to arrive in few days' time at the AAAAI annual conference.

If we compare the market cap of Cogent - $715m at the time of writing - to that of Blueprint Medicines - $$.7bn, it seems clear that if Cogent can establish bezuclastinib as the best-in-class candidate, its valuation can still soar, and that seems to be the story the company is attempting to sell to the public.

It is certainly plausible, although potential investors should consider the downside risk - if bezuclastinib ultimately proves inferior to Ayvakit, Cogent's valuation will plummet as the company has no other clinical stage assets of note, and only the much smaller GIST market to target, and an approval in this indication can by no means be taken for granted.

As such, everything is set up intriguingly for a reckoning come the SUMMIT data reveal. I'll be remaining on the sidelines, and it is possible, even likely, that the data when it arrives is inconclusive, with the PIPE financing signifying a longer-term vote of confidence in the company rather than short-term confidence in upcoming data.

Nevertheless, the more and later stage the data, the more a judgement can be framed about Cogent Biosciences, Inc. And as far as bezuclastinib is concerned, it is increasingly becoming all or nothing for Cogent and its valuation.