MelanieMaya/iStock via Getty Images

MelanieMaya/iStock via Getty Images

I recommended a buy rating for Vita Coco Company (NASDAQ:COCO) when I wrote about it the last time, as I expected management to continue executing strongly and meeting growth targets. As it achieves them, the margin should expand accordingly. Based on my current outlook and analysis, I recommend a buy rating. The main concern regarding the stock was gross margin pressure from logistic costs, and COCO showed that it can manage it and has done an impressive job managing it. Looking ahead, while FY24 growth is going to be subdued due to one-off reasons, I expect growth to surge back to >10% levels given the strong underlying demand. Reductions in logistic costs and product innovation should also drive further margin expansion.

I reiterate my buy rating on COCO following another quarter of strong topline growth (4Q23 top line grew 15% to $106.1 million, beating consensus growth estimate of 8.5%, primarily driven by Vita Coco Coconut Water sales growth of 8% y/y). The good thing is that topline growth was entirely volume-driven as underlying consumer demand remained healthy, up 15.6%, while pricing growth was pretty much flat at -0.2%. Coupled with an improved transportation cost environment, this led to strong gross margin expansion. COCO’s gross margins were up 1300bps y/y to 37.5%, which resulted in a 17.5% decrease in COGS per unit. This led to an EBIT margin increase of ~1000 bps to 5.1%. Overall, 4Q23 EPS saw $0.11, which was above consensus estimates of $0.07.

The strong business momentum so far, as seen from the volume-led topline in 4Q23, clearly points to positive demand going into FY24. That said, I caution investors not to be too aggressive in extrapolating 4Q23 growth into FY24 as COCO is lapping several one-off items that will likely weigh on topline growth this year. Firstly, COCO is going to see a lesser contribution from its private label coconut oil business (they stopped supplying to one major customer, as noted in the 3Q23 earnings call). While this is a low-margin business, it carries a pretty high price point, so it will impact topline growth strength. Secondly, COCO is going to grow against a tough FY23 comp, given that 1H23 saw incremental promotional activity at a major club retailer. This is going to pressure relative percentage growth. Lastly, COCO is not going to see the benefit of selling coconut water concentrate (a commodity sale) this year (FY23 was an opportunistic sale). Post FY24, I believe growth should normalize back to the >10% growth range, particularly as underlying consumer demand for COCO’s products remains quite strong despite economic uncertainty and potential pressures on consumer spending.

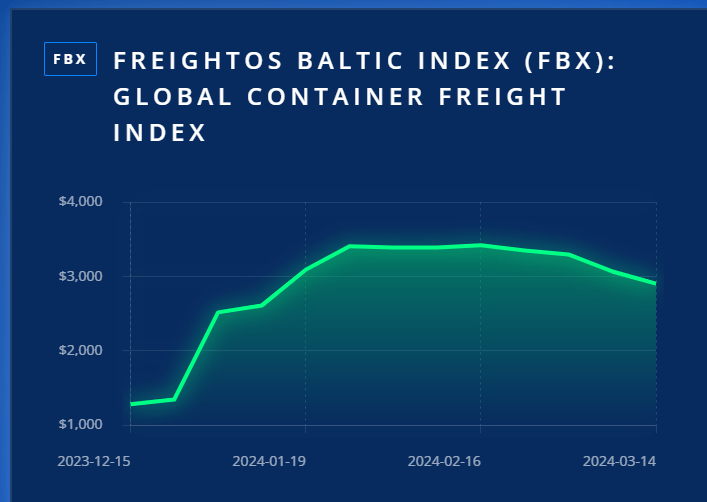

On the other hand, gross margin performance was the highlight. Investor sentiment was clearly negative before this set of results, as can be seen from the share price movement (coming down from ~$30 to a low of $20), which I believe is largely related to cost concerns over shipping disruptions in the Red Sea. The 4Q23 results proved the bears wrong. As I stated above, COCO reported strong 4Q23 gross margins of 37.5% and guided to healthy gross margin guidance for FY24 (the guide implies another 40 bps of margin expansion at the midpoint). This effectively eased the concerns that investors had and, hence, drove the stock price up. I remain confident that the guided 36% to 38% gross margin is achievable given that COCO has little exposure (i.e., is not significantly locked in) to forward shipping contacts compared to historical levels, which should allow the company to be nimble in the spot market in the event freight rates continue to move lower (note that they have been moving down).

FBX

Moreover, COCO is now a much bigger business than it was in the past, which should enable it to better negotiate terms with shipping companies. Even in the event that freight rates pop up, COCO should easily raise prices (rmb growth in 4Q23 was largely volume-driven, indicating room for price to go up) to pass through the cost. Note that current guidance assumptions do not take into account any material price increases, so this poses a potential upside risk. Longer term, I continue to see significant gross margin expansion potential, particularly as shipping costs normalize further, and behind COCO’s innovation, that should improve volume operating leverage. Specifically, management believes it is in the early innings of its multi-pack rollout (more volume in a single sale = operating leverage) with continued distribution opportunities (increase capacity to drive more volume sales).

Multipack in coconut water remain significantly underdeveloped versus other categories, and as the largest brand in the category, we firmly believe we are uniquely positioned to seize this opportunity. 4Q23 call

Author's work

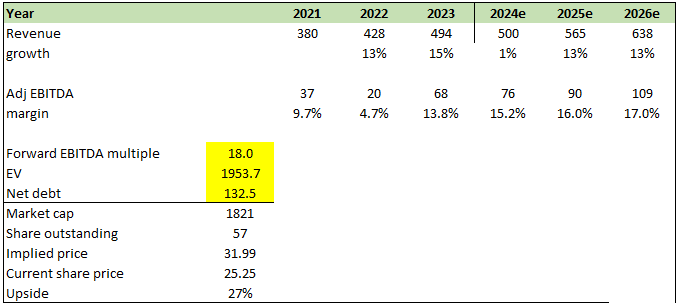

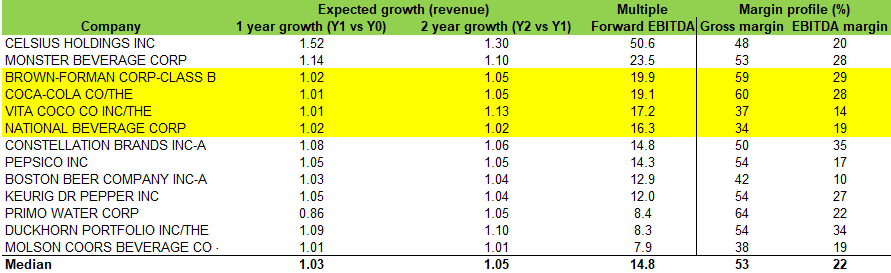

I believe COCO can grow low teens post FY24. As I noted above, FY24 is a down year because of the multiple one-off headwinds and also the tough comp in FY23. My estimate for FY24 is based on management guidance. Post FY24, I have revised my growth assumption downwards by 200 bps (to match FY22 levels) as FY23 was a year that COCO did multiple promotional events (I assume they won't do it at the same scale for FY25/26). That said, I now have a more positive view on margin expansion, expecting the adjusted EBITDA margin to expand to 17% in FY26 given the strong outperformance in gross margin seen in 4Q23. Comparing COCO to other US beverage peers, I believe COCO deserves to trade at a high-teen EBITDA multiple given that my expected growth rates are higher than peers in the same multiple group and that COCO has shown positive progress in EBITDA margin expansion.

Author's work

COCO has done a great job managing the situation at the Red Sea. However, if the conflict worsens, we could see a major surge in freight rates again that even COCO might not be able to avoid. The exposure to more spot rates would then become a big disadvantage for the business.

My recommendation is still a buy. While FY24 will see subdued growth due to one-off reasons, core demand remains robust. Notably, I was really impressed by management's handling of logistics challenges, which has led to significant margin expansion, and I expect this trend to continue. Reduced freight costs and product innovation like multi-pack rollouts should further improve margins and operating leverage. The main risk is a renewed escalation in the Red Sea conflict, which could disrupt shipping and raise freight rates. However, COCO's reduced reliance on forward contracts and its ability to raise prices mitigate this concern.