VioletaStoimenova/E+ via Getty Images

VioletaStoimenova/E+ via Getty Images

The emergence of generative AI has produced many winners in recent months, but there're always two sides to the story and companies like Concentrix (NASDAQ:CNXC) are an example of this, since market has been punishing them heavily in the last year because of the rise of AI.

However, I do not find evidence to conclude that artificial intelligence has the capacity to replace the services of customer support companies and rather it will be just another tool, which would make the current valuation end up being ridiculously cheap, which is why I think that at current valuation Concentrix would be a strong buy.

Concentrix offers outsourcing services with a focus on customer experience through process optimization, customer support, analytics, sales support, among other high-value services for the clients of the company.

For example, airlines and banks are businesses that constantly require direct attention to customers who usually have critical and stressful problems, such as missing a flight or money-related issues. Furthermore, they operate in quite competitive sectors, where it would make little or no sense to dedicate numerous resources to implementing customer service solutions when you can simply outsource it to a provider with the scale and reputation of Concentrix. That is why these services are in great demand and different reports project growth of 8-10% annually by 2030 in the United States, although currently this growth doesn't seem to be reflected at all in the valuations of companies in the sector, as we'll explore below.

Concentrix Investor Day

One of the issues that has filled the environment of Concentrix and other companies in the sector with negativity is the emergence of Artificial Intelligence (AI) as a generator of answers to specific questions, such as ChatGPT itself with which we're all already familiar. This has raised doubts about whether it could completely replace the services of customer support operators by being able to use artificial intelligence that read/listens, interprets and answers user requests.

Here are some important nuances to mention. The first is that, at least with current technology, artificial intelligence could not replace the capacity for empathy and trust generated by a human being, for example, a user who is having problems with their credit card while in a foreign country and that requires urgent help from the bank because they ran out of cash. In this situation, anyone would like to hear a human being who would give you emotional support, understand your situation and guide you until there's a solution.

Furthermore, there has been cases in which an artificial intelligence failed to apply common sense to a user's requests and caused companies like Air Canada to have to refund flights that a chatbot promised. On the other hand, an AI could automate more routine tasks, so instead of being replaced, businesses like Concentrix would end up being more profitable thanks to the possibility of using fewer employees on tasks that require little human judgment.

So, if AI is not a disruptor of this industry, why are companies reporting lower growth than usual and their outlooks for 2024 are bad?

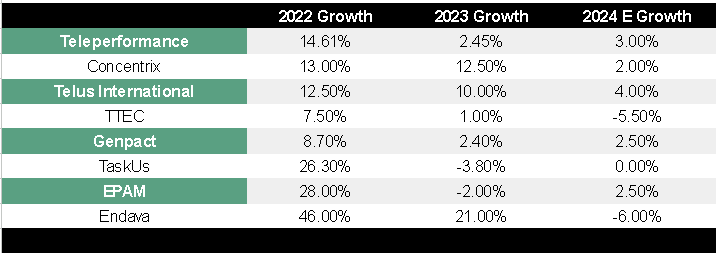

This is a valid question, since if we look at Concentrix and its competitors, during 2022 revenue grew 14% on average. But during 2023 the average decreased to 4% and the guidance for 2024 is only 1%. A clear slowdown that could be caused by AI... or not?

If we observe the behavior of other B2B services companies, such as EPAM (NYSE:EPAM) or Endava (NYSE:DAVA), which carry out the digital transformation of their clients (a business that has little to do with AI), the behavior is exactly the same: A good 2022, bad 2023 and projections of 2024 being worse.

Author's Representation

This gives us clues that the slowdown would not be related to AI and if we delve into the comments of the management of the different companies, everything seems to indicate that the explanation is the fear that their clients are having thanks to inflation, possible recession and high interest rates. At the end of the day, both Concentrix and EPAM clients are other businesses, sometimes small, which are highly sensitive to the macroeconomy and in an adverse environment they will most likely prefer to pause their investments so as not to risk their financial stability.

But in the medium term, these investments should return, since they solve a problem for their clients and improve operational efficiency, because customer service is key in any business and outsourcing these services has a lower cost than developing it in-house. Also provides the flexibility of not having to hire employees with the necessary experience to carry out this job.

Another key aspect is that, assuming that an AI could completely replace customer services, it would have to be implemented by someone because it's not as simple as going to AI dot com and installing it with two clicks. Implementing artificial intelligence is complex, not only because of the front costs involved, but also because it requires knowing the specific processes of each business, designing the flow charts on which the AI will work, and training it to be able to perform these tasks. Therefore, it may make sense for Concentrix clients to choose to outsource this task to operators with the most current know-how and tools, allowing them to focus on their core business.

In this regard, I consider that the companies with the largest scale will be the ones that will be able to face this investment without risking their financial position so much, in order to be able to reap the benefits of it as soon as possible. In this sense, Teleperformance (OTCPK:TLPFF) would be the largest company in the sector, generating just over $10 billion euros in revenue (post-acquisition of Majorel) and in second position would be Concentrix with $9.6 billion dollars (post-acquisition of Webhelp).

Author's Representation

The table above shows some competitors of Concentrix and Teleperformance, showing that despite being the two companies with the largest scale and expecting organic growth in 2024, they are the two that are also trading cheaper in EV/EBITDA for the next twelve months. .

Part of this explanation may be the issue that making such large acquisitions saddled both with a lot of debt, in addition to reducing ROIC. Even so, it doesn't seem to me that it deserves a valuation between 40 and 50% lower than that of Genpact, for example, which has similar margins and expects to grow practically the same during 2024.

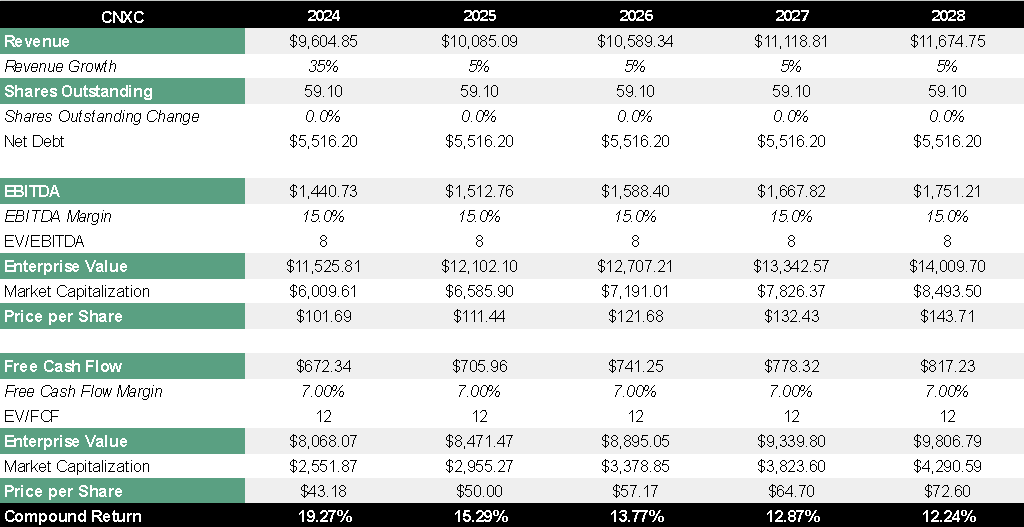

For this year, revenue should grow approximately 35% thanks to the aforementioned acquisition of Webhelp. Assuming a negative scenario where revenue grows only 5% annually due to the hypothetical negative effects of AI, margins decrease slightly and the multiple remains at 8x EV/EBITDA and 12x EV/FCF, the expected return from the current price would be of 12%.

Author's Representation

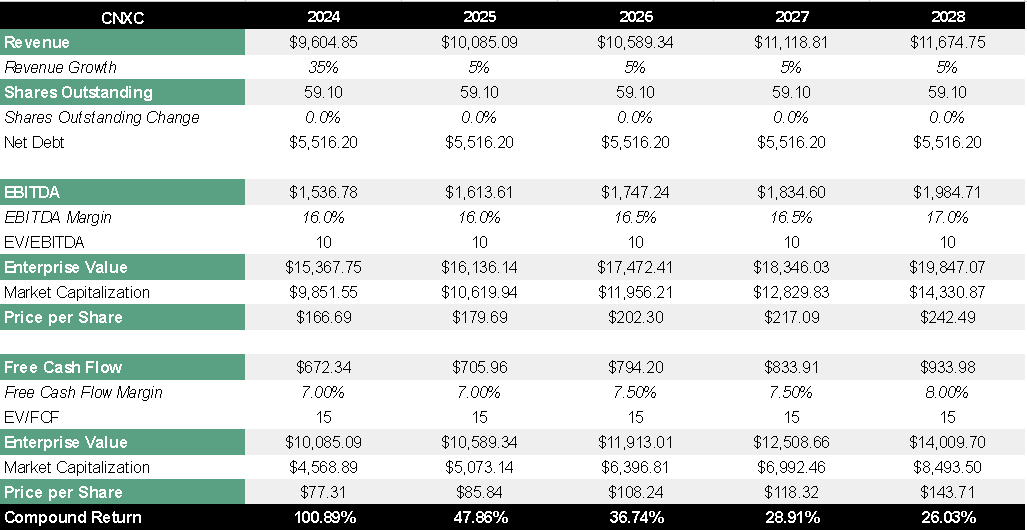

Now, in a little more optimistic scenario where we maintain the growth of the top line, but with a slight improvement in margins thanks to the synergies of the acquisition of Webhelp and consequently the market ends up being less negative so the company is valued at 10x EV/ EBITDA and 15x EV/FCF, then the potential return five years from now would be 26% annually.

A crazy return in a scenario that doesn't seem excessively optimistic to me either, it would simply be a scenario where AI, more than damage, would be just another tool for Concentrix.

Author's Representation

Although it seems that AI doesn't pose an imminent risk for the company and the valuation already seems to discount any bad scenario, there are still two risks that are worth mentioning.

The first risk is the fact that this industry is very competitive, with numerous providers offering services with little differentiation from each other. Such a competitive market with little differentiation usually ends in price wars and reduced margins. Concentrix will have to manage to maintain the added value of its services if they want to remain profitable and growing.

Also Webhelp integration adds complexity to the company's situation, since making a large transformational acquisition is not usually easy to carry out because one need to bring together two large businesses. It's also usually expensive for the buyer and, as we already saw, this left Concentrix loaded with debt. If the integration doesn't go as expected, inefficiencies, worse operating performance, a lower return on investment and even goodwill impairments can be generated, affecting the profitability of the business.

The market's negativity towards the company could not be greater and current valuation demonstrates it. The thing is that even in a scenario where AI does end up affecting the business a little and multiples remain depressed, we could obtain an attractive return that could be improved through dividends, buybacks or debt payoff.

I don't see any evidence that companies in the sector are going to disappear because of AI and it seems to be a total inefficiency or misinterpretation of the business, therefore, I think that at the current price, companies in the industry are a strong buy, although if I had to buy one maybe it would be Teleperformance, which is the leader and has less debt than Concentrix. Also Genpact could be an interesting option because it has a division more focused on digital transformation. In any case, I don't think investing in Concentrix is a bad decision at the current valuation.