dan_prat

dan_prat

As Peter Lynch teaches, you make money in the stock market when the situation goes from terrible to mediocre, mediocre to good, or good to terrific. When it's terrific, it might be time to sell.

Canadian Natural Resource (NYSE:CNQ) (TSX:CNQ:CA), the crown jewel among Canadian O&G (oil and gas) producers, has already achieved greatness with its huge reserves, high diversification of resources, low costs, great management, recently achieved debt target, and a 100% payout ratio.

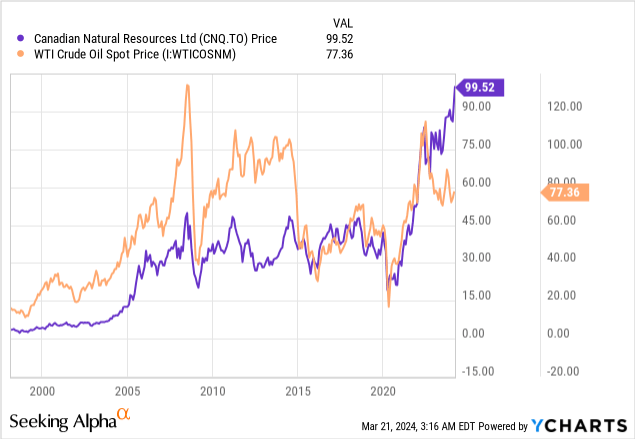

Just looking at the graph, you can see that the company is a compounder. Correlated with oil prices in the short term, while in the long term, benefits from intelligent acquisitions, a focus on efficiency, and disciplined return of capital to shareholders with 24 years of growing dividends.

I congratulate all investors who bought the stock before the massive run from 2020 lows, which was driven by rising O&G prices as well as improvements in the Canadian oil export capacity from TMX expansion and, most recently, by the achievement of the C$10B debt target and the switch to 100% payout to shareholders.

But, as a value investor, I am asking myself: "What's there left to improve?"

Before I jump into it, here is a quick review of CNQ.

Founded in 1988, Canadian Natural Resources (CNQ:CA) (CNQ) grew into the largest Canadian integrated O&G producer through a series of clever acquisitions. The scale of its reserves is comparable to that of oil majors like Shell or Chevron.

With 32 years of proven reserves, the company has room for growth and development. I believe that 30 years later, even without future acquisitions, the company would still have 30+ years of reserves due to its large acreage, future exploration, and technological advancement.

The production level reached in 2023 was 1,332,155 boe/d (barrel of oil equivalent per day). The production mix is well diversified with 27% natural gas, 20% thermal oil, 9% heavy oil, 10% light oil and NGLs, and 35% of their core profit maker synthetic crude oil from oil sands. With a majority of production in Canada, the company also has small production in the North Sea and Offshore Africa.

There is a lot to like and very little to dislike about the company. It is superior to its peers in almost every aspect. I see several long-term advantages that deserve to value CNQ at a premium.

I believe these competitive advantages will cause CNQ to outperform over a very long time, and thus, CNQ deserves to be valued higher over its peers.

Apart from their conventional production, oil sands have no decline rate, meaning no reservoir risks. On the other hand, freezing weather might be challenging. The production is expected to run 365 days a year to achieve the targets. During Canadian winters, temperatures can drop to -50°C (-58°F). Even -20°C already presents a risk for the workers as well as the equipment. Potential heavy blizzards might have a negative effect on production in the future.

When you mine from a surface, a large acreage needs to be deforested. This presents future environmental costs, as CNQ is obligated to bring the land back to its original state. CNQ spent significant money in this area, with C$509M for the last year. This will continue, together with capital spent, to meet its decarbonization targets.

The debt target was achieved. Due to the low-cost structure, it does not present a risk worth a debate.

Oil prices present the most critical risk to the company's financials. I will review the impact of different pricing environments in the valuation section.

As Howard Marks says: "Success in investing is not a function of what you buy. It’s a function of what you pay. An asset of high quality can be overpriced and be a bad investment; an asset of low quality can be bought cheaply and be a good investment."

Valuation is always based on the future. Let's see how it looks for CNQ. I am building the projection model with a base case WTI of US$75 with a WCS differential of only US$11, reflecting on the coming TMX expansion.

Further, I am assuming AECO rising, with prices of futures reaching C$3.5 in 2026 from current depressed levels. This is a reflection of the improvement in AECO with the increase in LNG export capacity from LNG Canada and other hubs.

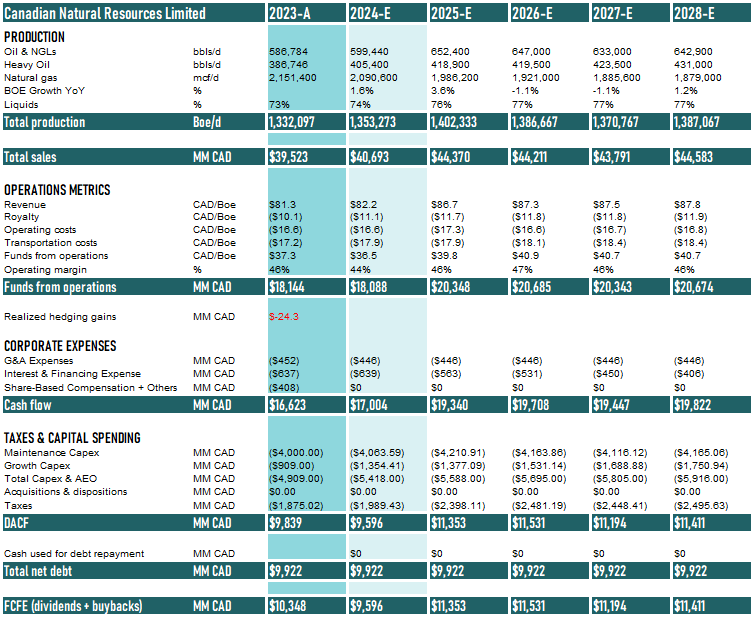

CNQ is guiding for C$5.4B in Capex for next year. Management presents the production growth on a per-share basis of 3-7%, which already includes the buybacks in it. Excluding buybacks, the base production is expected to grow by around 2%. Analysts expect nearly flat production for the next five years with higher liquids production and lower gas production, ultimately increasing the revenue per barrel.

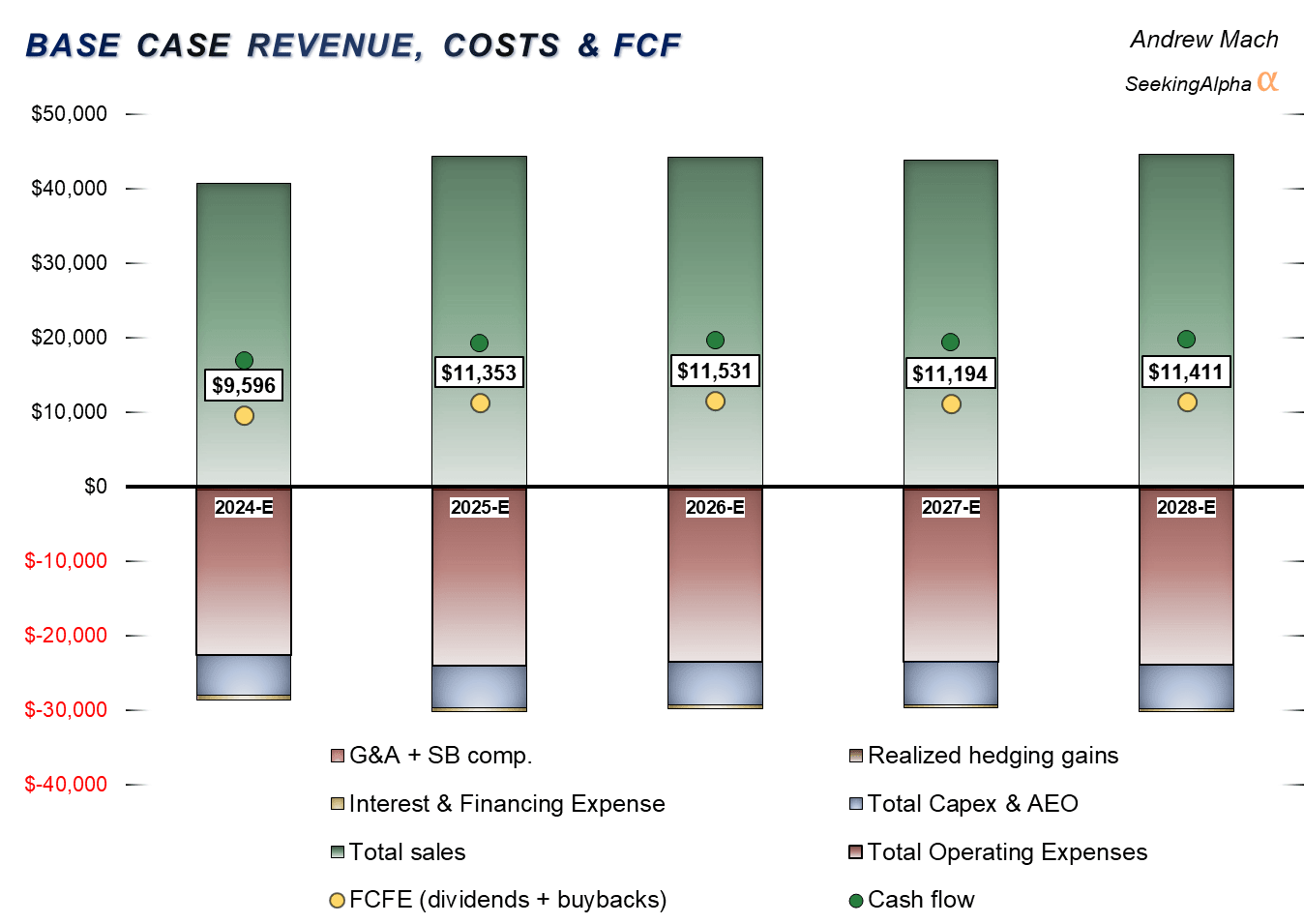

5 years projection (Author's Calculations)

The graph above summarizes the projection. You can see a nice jump in 2025 FCF, which is due to the improvement in WCS differential and expected higher liquids production.

You can review all assumed numbers in the projection table below.

5 years projection (Author's Calculations)

Now, I am discounting the resulting dividends and buybacks by a cost of equity of 12.5%, which I use across the Canadian O&G upstream sector, so I can easily compare companies inside the industry.

DCF Valuation (Author's Calculation)

After discounting dividends, buybacks, and terminal value based on maintenance FCF, the base case scenario results in a fair price of C$93 per share. Not far from today's C$100.

The current WTI 12-month strip is at US$78.5. With that pricing in the future, the valuation for a 12.5% return would increase to C$106, making the company fairly valued.

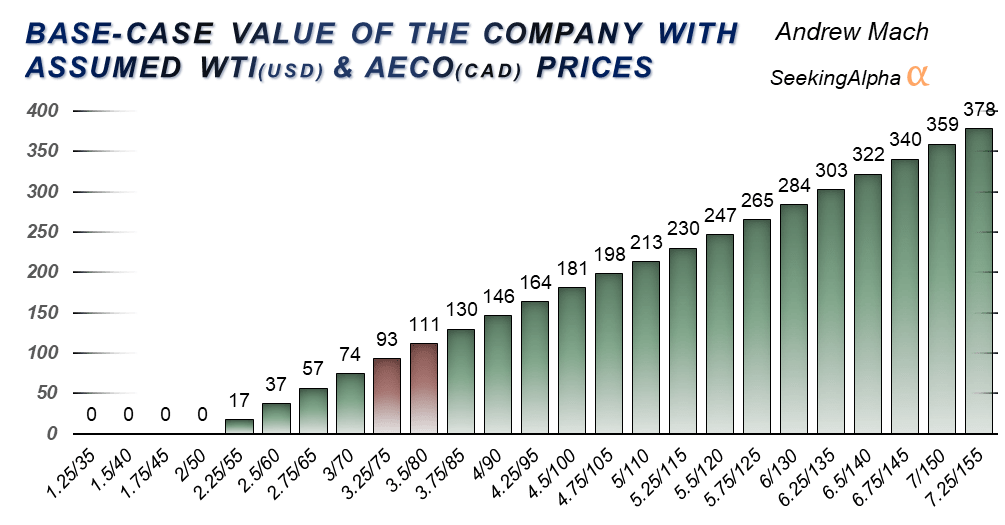

The table below shows fair prices under different long-term O&G pricing environments.

DCF under different O&G prices assumptions (Author's Calculation)

The company is fairly priced for an assumed 12.5% return going forward, which, considering its quality, would make it a "HOLD" for the long term.

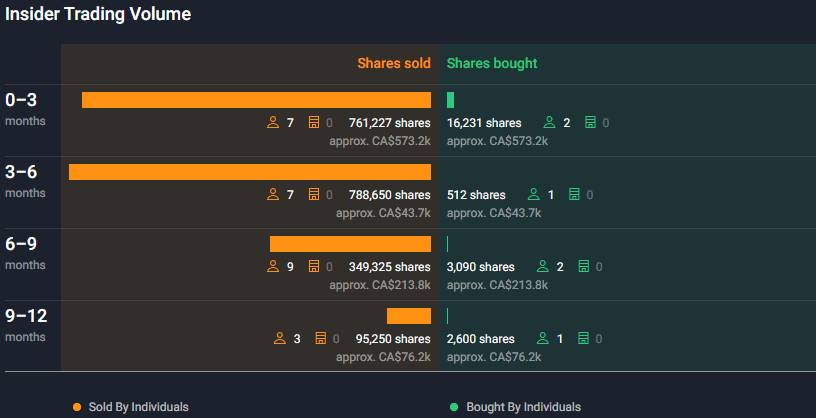

Yet there are further factors, such as recent strong insider selling with 1.5 million shares sold by insiders in the last six months, which is definitely sending a bad signal.

Insider selling activity (simplywall.st)

More importantly, CNQ is one of the fully priced names in the Canadian O&G space, with many names offering 20+% returns going forward. You don't even have to go to the small-cap world to find those.

From a more gas-weighted part of the industry, high-quality names like ARC Resources (ARX:CA) or Peyto Exploration (PEY:CA) both offer over 20% yearly returns under current strip prices. You can review my recent articles with detailed valuations for Peyto Exploration and ARC Resources.

From the oil world, I see much higher potential returns in Crescent Point Energy (CPG:CA), which I believe will strongly outperform CNQ. You can review my CPG thesis and valuation.

In the end, it depends on how much you value quality. You might want to stick to the industry leader, and I believe you will do just fine. Even though I believe the stock could pull back by 10-20%, it might continue growing with the momentum and buybacks in place.

The valuation gap, compared to just a bit lower quality names, makes me join the insiders and sell the stock. Despite the quality, I am leaving CNQ to pension funds and market-cap-weighted ETFs that don't look at valuation and buy the most expensive stuff.