Brandon Bell/Getty Images News

Brandon Bell/Getty Images News

Shares of CenterPoint Energy (NYSE:CNP) have been a poor performer over the past year, essentially treading water during what has been a strong bull market run. Since recommending shares as a “buy” in November, CNP has continued to trade flat, lagging the S&P 500’s double-digit return. I continue to believe the company has very favorable geographic positioning and is poised for solid dividend growth, though recent developments have been somewhat mixed. On balance, I still view shares as a buy.

Seeking Alpha

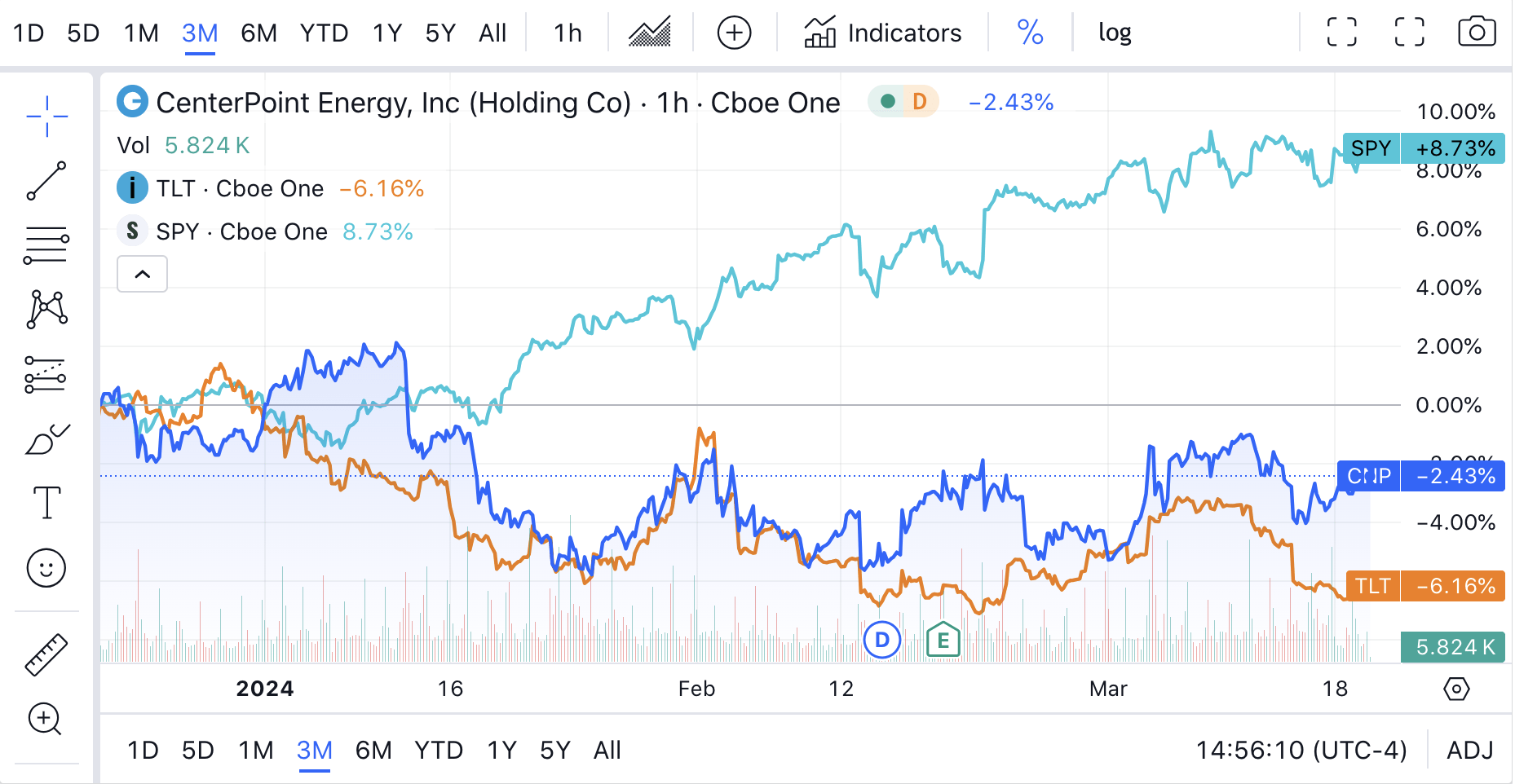

Before turning to company fundamentals, I believe investors should recognize the extent to which bond yields drive utility stocks. Utilities are usually seen as a “safe haven” sector given their noncyclical nature and higher dividends. These are more traditionally income than growth stocks. As such, they are sometimes seen as “fixed income” replacements, and as you can see, CNP exhibits a much closer relationship to how treasury bonds trade (TLT) than the S&P 500 (SPY). Ultimately, the more you can earn on risk-free treasuries, the higher dividend yield you are likely to require to own a dividend stock.

Seeking Alpha

Now, in the long run, I do believe a well-run utility should outperform treasuries because they can grow their dividend payout over time whereas a treasury bond’s coupon is fixed until its maturity. However, in the short run, interest rate movements clearly drive share price movement to a meaningful degree. While I do not expect a material fall in yields, I do believe the Fed is more likely to lower rates than raise them. If, however, we do see long-term yields continue to rise, that is likely to be a headwind for CNP and utility share price performance in general.

Turning to its own financial performance, in the company’s fourth quarter, it earned $0.32 in adjusted EPS, in line with expectations and up from $0.28 last year, as rate recovery and demand growth offset higher interest expense. In 2023, EPS and dividends rose by 9%. Full-year earnings were $1.50 even with interest rate expense a $0.27 headwind. Last year, revenue declined by $625 million to $8.7 billion. This was due to lower pass-through of energy costs with utility natural gas expense declining by $826 million.

It is important to remember that utilities like CenterPoint do not take energy price exposure; they buy gas and pass that cost on to consumers. Non-energy revenues rose by $201 million or just over 3%, which reflects its growing rate base and increased customer base. Operations & maintenance costs rose by 0.5% to $2.887 billion. As has been its history, CNP showed tremendous cost discipline and operating leverage with expenses rising just 20% as fast as revenue. Interest expense rose $167 million to $701 million due to higher rates and increased debt.

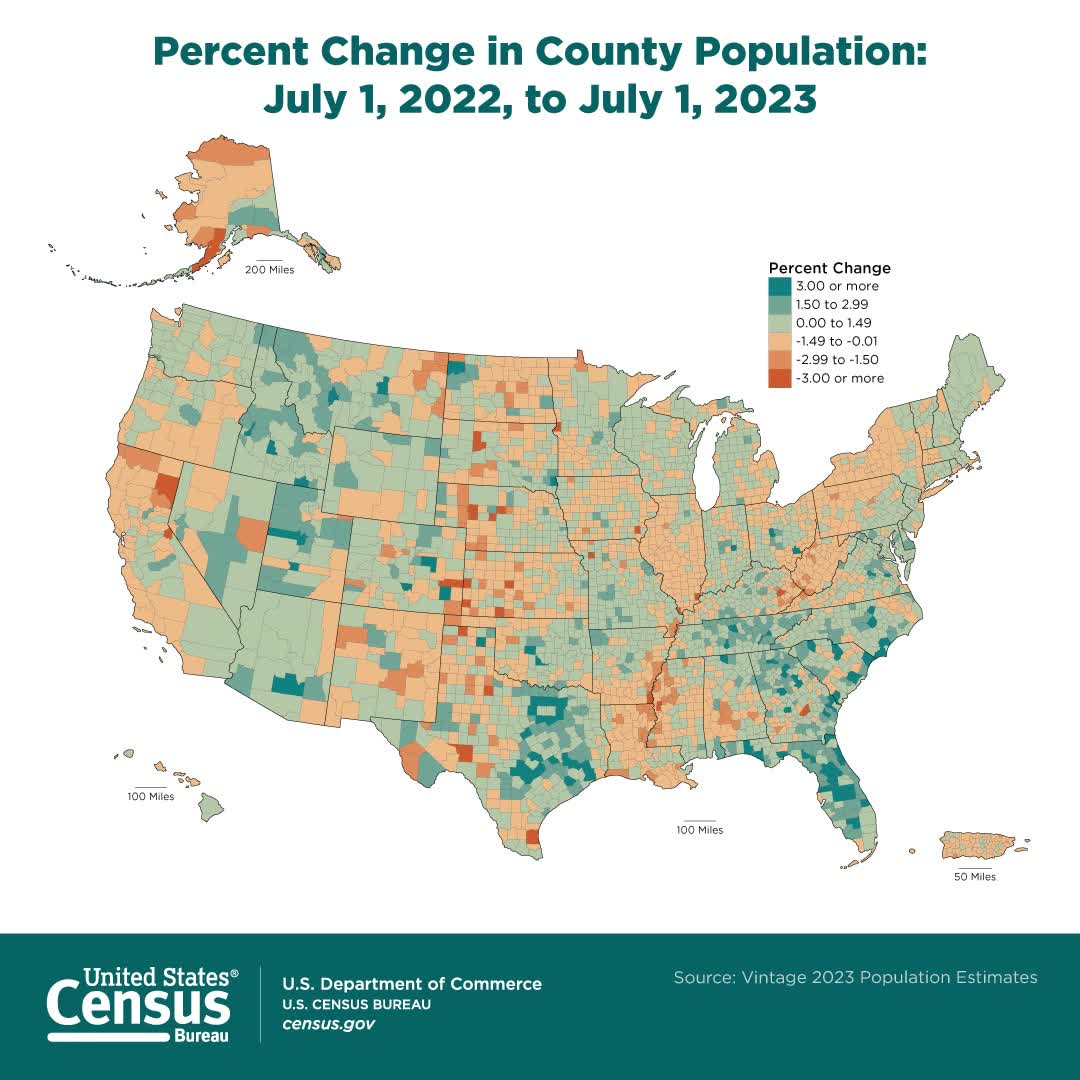

CNP is enjoying solid revenue growth because it primarily serves Texas, in particular Houston via its Houston Electric Subsidiary. Utilities cannot pick up and move their infrastructure to where people move; they are subject to their local economy and population dynamic to grow customers. For CNP, this is a good thing. In 2023, Harris County (home to Houston) was the fastest-growing county in America, adding over 50,000 residents. As you can see below, the Eastern Texas region where Houston Electric operates is among the fastest growing in the country.

Census Bureau

This provides a runway for growth for CNP. Indeed, CNP is doubling down here, essentially becoming a pure-play Texas utility. In February, the company announced it would be selling its Louisiana and Mississippi gas assets for $1.2 billion. These sales were at 32x earnings and 1.55x the rate base. The company will retain $1 billion in proceeds after taxes, which will be deployed into its growth cap-ex plan. As you can see above, LA and MS are both seeing population loss; CNP is exiting relatively unattractive markets to increase its capital spending in the high-growth TX market. I also view the 1.55x rate base multiple attractive given all of CNP trades at ~1.62x its $22.3 billion rare base. Given worse demographics, LA & MS are deserving of a lower multiple than Houston Electric; to sell out at just a 5% discount is likely to prove accretive over time. This sale completes CNP’s transformation into a simpler, more stable utility. Prior to this action, in 2022, the company sold its MLP, Enable, to Energy Transfer (ET), exiting its foray into the midstream business.

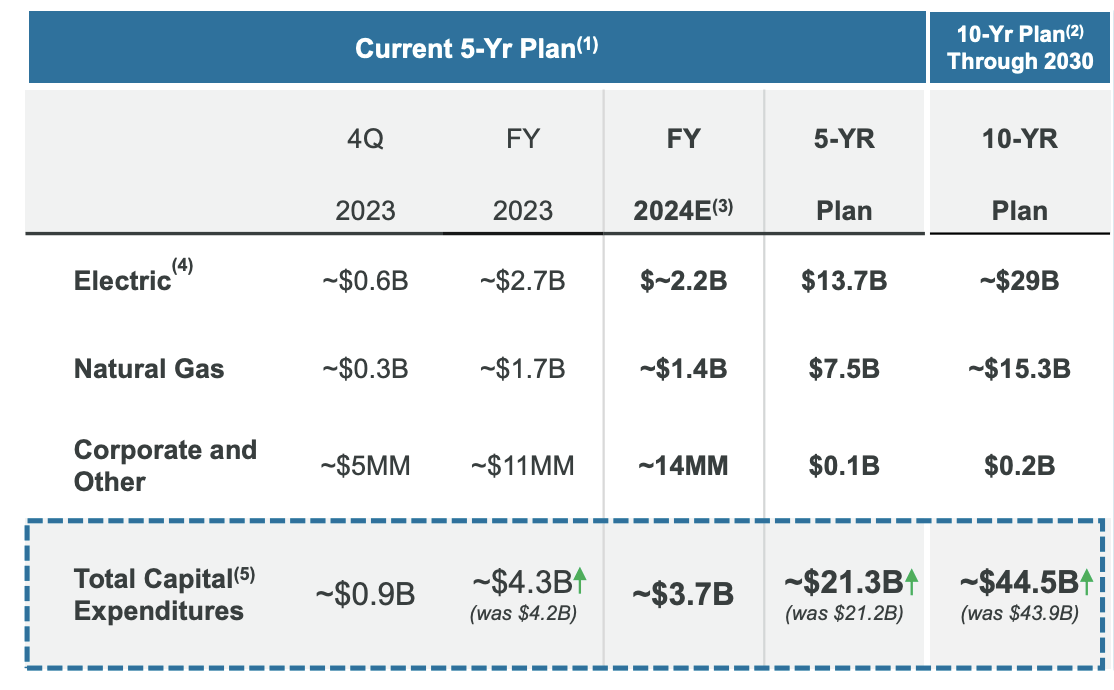

Indeed despite this sale and alongside Q4 results, management reiterated its $1.61-$1.63 2024 EPS target, up 8% from last year. This is at the high end of its 6-8% annual target through 2030. It expects to do this even with the divestiture of the LA & MS operations because it will be reinvesting that $1 billion into its business to more quickly grow the rate base. As you can see below, it has raised its 10-year capital plan further, to $44.5 billion, even as $1 billion had been earmarked for these divested states.

CenterPoint

With this cap-ex plan, CNP aims to grow its rate base at 10% annually to $41 billion in 2030, with 67% of that electric and the remainder gas. A critical way utilities grow cash flow and earnings over time is by investing in cap-ex to grow their rate base, which is the amount on which they earn a regulatory-approved return. By growing the rate base, a utility generates greater cash flow over time. A key part of this is to get regulatory approval for this spending to be added to the base.

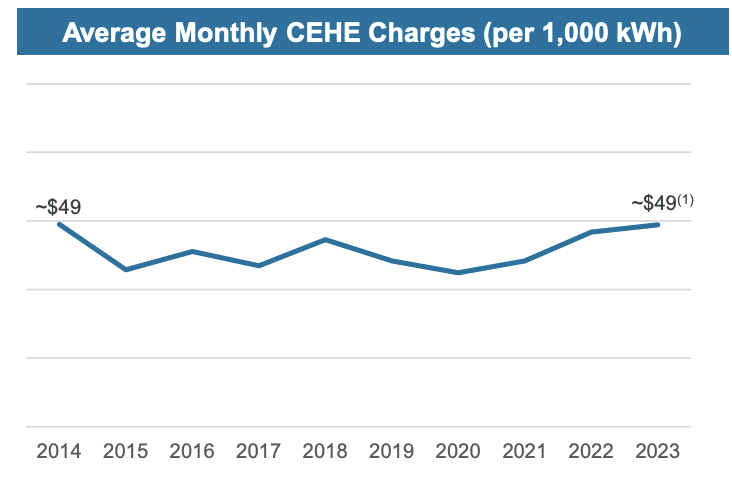

Texas has been a favorable environment, and a key reason for this is that CNP has been able to keep utility bills flat over 10 years, significantly undershooting inflation. Its austere operating expenses are a key contributor, but population growth here also helps. If you grow the rate base by 5% in a year, but your customer base also grows by 3%, then the per capita growth is just 2%. With Houston growing so rapidly, CNP has been able to spread its growing rate base across more and more customers, helping to limit the pricing impact of its growing base. With Houston continuing to grow, I expect this dynamic to persist, helping to sustain its solid relationship with regulators.

CenterPoint

Now, the other major factor is paying for all of this growth. Here is where things become less positive. First, of course, CNP is able to pay for some cap-ex out of its retained cash flow. Looking at 2023, for instance, it generated $3.88 billion of operating cash flow and spent $485 million on common stock dividends. That left about $3.4 billion of cash for cap-ex. It spent $4.4 billion on cap-ex, meaning $1 billion has to be funded by capital markets. Right now, CNP carries $18.6 billion of debt for a 14% FFO/Debt; in line with the 14-15% target. That means it can continue to grow debt as it grows cash flow; at an 8% return on investment, it essentially can use a 50%/50% mix of debt and equity.

To cover the rest, it announced last year it would issue $500 million of equity from 2023-2025. Of course, equity issuance is dilutive. However, particularly with interest rates elevated, it is important not to over-leverage a balance sheet. Alongside results though, the company said it would continue to issue about $250 million a year through 2030 to fund its capital program. It has to do this because CenterPoint will face a higher cash tax liability due to the alternative minimum tax, which is driving the increased tax funding. This will be about $150 million per year. In order to meet its capital program needs without relying on excess debt, more equity issuance is needed.

At its current share price, that equates to about 1.5% of annual dilution. Despite this dilution, CNP is continuing to guide 6-8% EPS growth from 2024-2030 with dividend growth that is in line with earnings growth. I continue to believe CNP the company will do as well as I had previously, given its favorable geographic position and strong rate base growth. However, with increased share count growth, there is a risk CNP the stock does not do as well as this growth is spread across more shares.

Shares today have a 2.86% dividend yield, at 6-8% annual growth, which creates a total return potential of 8.8-10.8%. I view a ~10% long-term return potential as the threshold for “buy,” so at essentially the midpoint of guidance, this double-digit return potential threshold is met. The increased share issuance beyond this year does raise some concern that CNP could come in the bottom half of guidance, though that still offers a solid return potential. Given its favorable operating environment, I believe CNP can achieve its guidance, and the fact this year will be closer to 8% than 6% despite share issuance and an asset sale speaks to the power of its Houston Electric operation. As such, I continue to view CNP as a buy and suitable for investors seeking dividend income, though there is a little more uncertainty than a few months ago.