claffra/iStock via Getty Images

claffra/iStock via Getty Images

Costamare Series E Preferreds (NYSE:CMRE.PR.E) are the most junior of the preferreds in the whole capital stack, above only common stock. Value drivers here are credit quality of Costamare (CMRE) and duration considerations, as they are basically ultra-long duration unsecured credit. We've discussed them in the past, and the core idea that the common stocks are more worth following has not changed, especially as trade disruption events could become recurring trading opportunities where the common stock articulates much better.

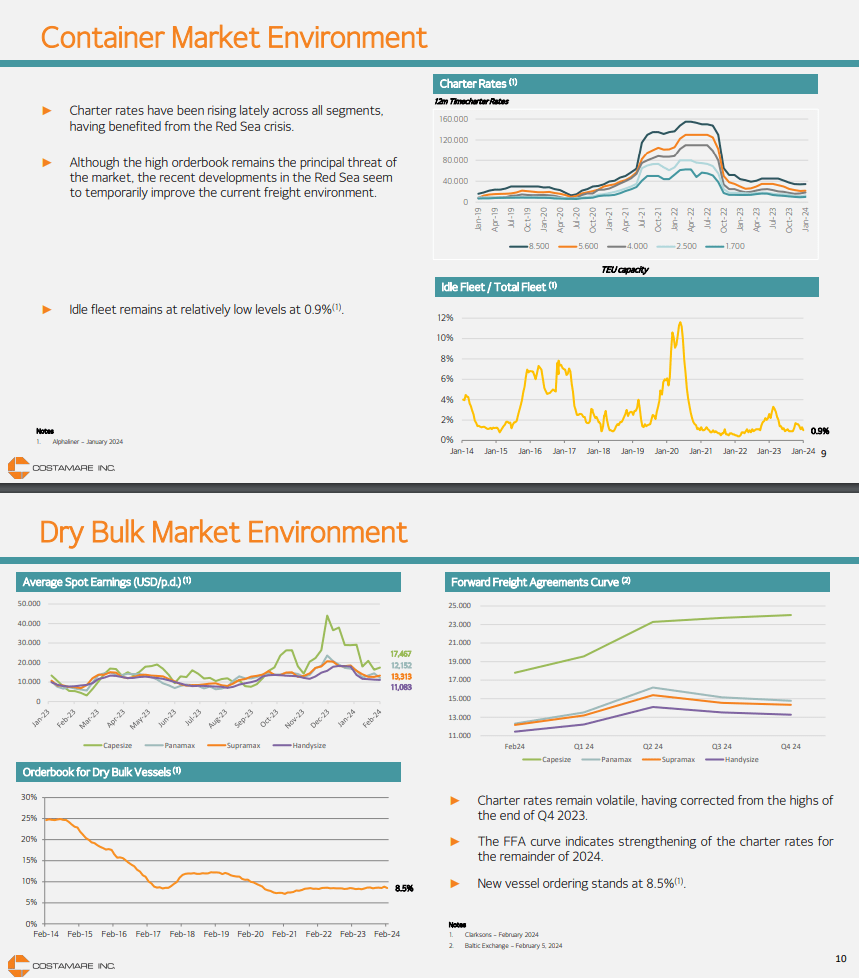

We have several considerations in their markets. Orderbooks for new ships were swelling during COVID-19, and the only reason that oversupply hasn't hit so hard is that there are major issues in the Red Sea that are reducing effective vessel availability, not just in dry bulk and containerships but also in RoRo and other markets. It helps though that CMRE is not in the highest TEU brackets, where supply pressures were growing much less alarmingly in CMRE's range. Guessing how long those disruptions will endure is speculative, but for now, things are at very healthy profit levels for containership and dry bulk, mainly benefiting the common stock.

This is a volatile and cyclical industry, where profits can go negative for long periods. The fleet has value, which lends itself to a somewhat safe liquidation if debt needs to be managed down even in a poorer market, but we feel that the implied credit rating for Series E is consistent with reality and that there's no obvious credit angle. Being effectively a long-duration instrument, it's tough to make a call on long-term rates. There is an emerging argument that long-term rates will be higher. Not only because the limits of globalisation have been reached, but also because the economy seems to have enough monetary velocity to sustain these higher rates without having a major turndown in the economy, at least until maturity walls fully hit which may change the narrative. We don't see a strong buy-case case for the Series E, and think that there is more optionality in the common stock.

Firstly, the series E is junior to the debt and the other series of preferreds. The preferreds dividend burden is insignificant relative to the debt. Interest expenses are over $100 million, while the total preferred dividend burden is just slightly above $7 million. The last $2.5 million of that burden is in the Series E dividend. The Series E doesn't get paid if the dividends don't get fully paid on any of the more senior preferreds. They are juniors in liquidation too.

In terms of profits, things are healthy. Operating income is $468 million, down from $662 million last year for the FY, reflecting that charter rates have averaged down but that there's more than enough excess income to service obligations.

Charter Rates Dry Bulk and Containership (Q4 Pres)

They declined as the general bucket switched somewhat from goods to services after the end of COVID-19. They would have declined further but general shipping routes have been affected by the conflict around the Red Sea, and consequently lengthened routes have reduced effective ship availability and kept idling rates which really started coming up at the beginning of 2023 at low levels. Also, during COVID-19 there was quite a lot of ordering of new capacity in shipping. It takes some time for it to all come to market, and thankfully, the TEU bracket that CMRE is in was least affected by swelling orderbooks, but oversupply has been looming over the industry as a concern in 2023. Scrapping was also relatively high in the CMRE bracket with a high concentration of older ships compared to higher TEU brackets above the 8k mark. CMRE has quite a lot of capacity above 8k TEU as well, but things get progressively worse at TEUs higher than 12k. They aren't immune but they are relatively advantaged compared to large-cap picks.

There isn't much doubt that without conflict in the Red Sea, the situation would be worse in the charter market, and it's also clear that there might still be economic headwinds outstanding in the US on account of maturity walls.

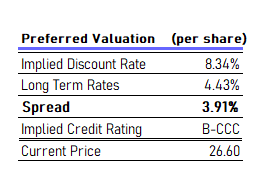

In light of that, we can have a look at what the preferred offers us, looking at current dividend yields as a yield figure for the instrument, and see what implied credit ratings are.

Implied Rating (VTS)

Looking at credit spreads, its implied rating is somewhere between B and CCC. That seems about reasonable, but it doesn't leave much credit upside, since the business is still highly leveraged at around 3x ND/EBITDA. In general, we find that across fixed income, credit spreads are too low with impending maturity walls, and in the case of shipping there is the added shoe to drop of less disruption which would be bad for market dynamics.

Our figures are very tentative and are reflexive in a poorer market environment, but we have them at over $3.5 billion in total vessel value, which is double the net debt as it currently stands. Not to be relied heavily upon, but it's an indication that the company has been given debt for a good enough reason and that the liquidation preference can probably save a small sliver in the capital stack of the preferred shareholders.

We aren't particularly worried about a dividend issue considering the company's vessel value and relatively in control leverage, although we don't see any special implied credit angle here either. Money might be made instead of duration considerations. Preferreds are like ultra-long fixed-income instruments with substantial sensitivity to long-term rate changes. The yield curve tells us rates are a little above 4% in longer horizons. It's almost impossible to guess where a fair long-term rate should be, however, the fact that the US has been resilient, and is even expansionary at this point in time, albeit before maturity walls, is a signal that a rate at which the economy is neither expansionary nor contractionary could be around the 4% rate level after all, a little down from current prevailing figures. We'd be surprised if rates went lower than that to the anomalous levels we got used to in the new normal environment of the 2010s. In other words, we don't see substantial re-evaluation of long-term rates in the future. Also, events that might lead to more supply disintegrations would play against the Series E with possibly higher long-term rates to combat more underlying inflation. Depending on the nature of that disintegration, trade flows would be reduced which would be bad for CMRE, or it could be good like it is with the Red Sea crisis, where routes are being disrupted and lengthened, but the edges of trade are still active. The common stock has more optionality in an at-risk trade environment, even if they are of a completely different risk profile than the preferreds. We don't see a strong case for the Series E.