Dizfoto/iStock via Getty Images

Dizfoto/iStock via Getty Images

Industrials have been hit hard both by the spread of the Covid-19 pandemic and the subsequent inflationary crisis around the world. Despite rising input costs and macroeconomic uncertainty, businesses like Cummins Inc. (NYSE:CMI), a leading manufacturer of powertrains, have managed to persevere and even record strong financial performance over the past couple of years.

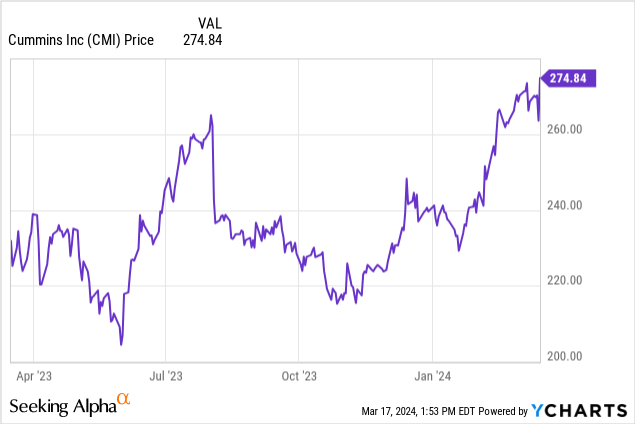

After a record year in 2023, with revenue and profitability margins showing strong momentum, Cummings share price increased 19.24% over the TTM. Currently, CMI trades at $274.84 per share ($38.99B market cap), near all-time high levels of $276.92, and pays a 2.45% dividend yield.

As a leading American manufacturer of different types of powertrains and related components, Cummins has been in business for over 100 years (since 1919) and has served all kinds of industrial mobility applications through an innovative and reliable range of products.

Today, Cummins manufactures diesel, natural gas, electric, and hybrid engines, as well as components and peripherals like filtration systems, turbochargers, fuel systems, controls, transmissions, and more. The company serves approximately 190 countries around the world through an extensive dealership network.

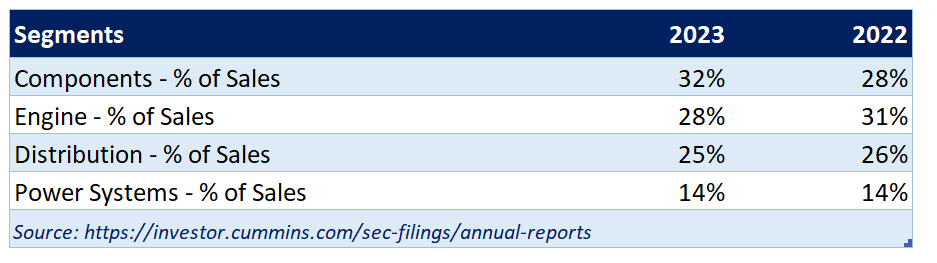

After some business realignment efforts in 2023, that resulted in the renaming and refocusing of some key business functions, Cummins now operates in five segments; Components, Engine, Distribution, Power Systems, and Accelerate.

The Components segment specializes in products like axles, brakes, emission solutions, filters, transmissions, and many more, and acts as a supplier for the other four segments. The Engine segment manufactures powertrains for heavy-duty trucks, buses, commercial vehicles and off-highway users like rail, marine, mining, and others. The company's primary sales, service and support channel is organized under the Distribution Segment, while the Power Systems segment focuses on generator technologies, and the Accelera Segment, which is currently in an early commercializing stage, engages in the design, production, and sales of innovative hydrogen production technologies.

10K Report (10K Report)

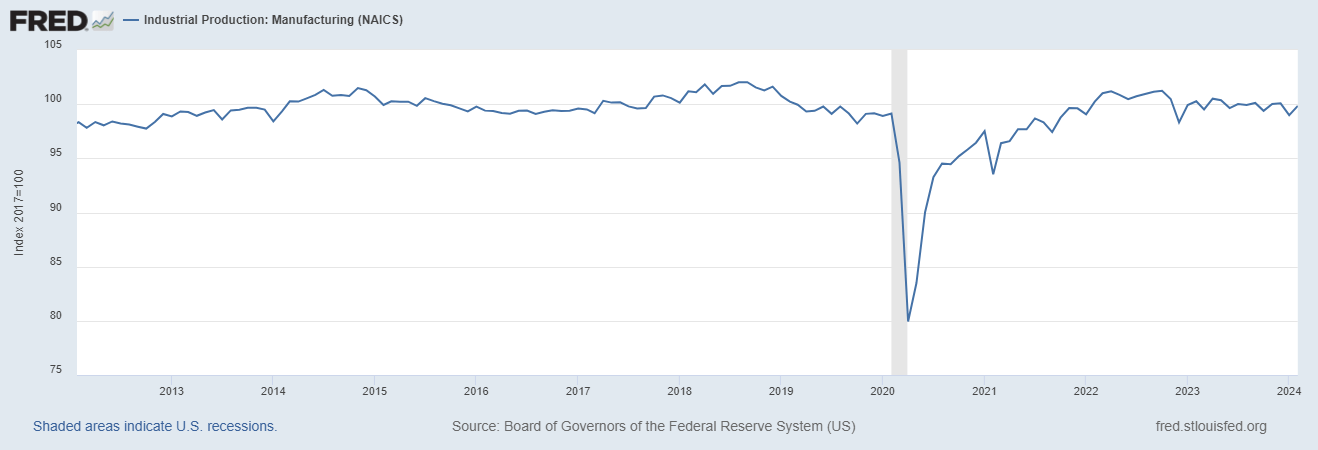

While a few sectors in the U.S. economy have displayed impressive growth attributes and potential over the past decade, namely the Technology sector, consumer Discretionary, Real Estate, and others, the country's industrial production has not seen highly noticeable increases in output. While this is expected as the United States has been, for decades now, a mature economy, operating near long-term output levels, it also indicates that growth has to come from areas like cost effectiveness, innovation, and product differentiation for individual companies.

As shown in the Manufacturing (NAICS) index below, industrial production appears to have fully recovered from the Covid-19 pandemic and to have stabilized slightly above 10-year average levels in the past couple of years.

fred.stlouisfed.org

The industrial sector, and especially manufacturing, is characterized by elevated sensitivity to cyclicality in the economic activity. Economic downturns significantly hamper sales and profitability, while inflationary pressures dictate input costs on the materials, energy, and wages levels.

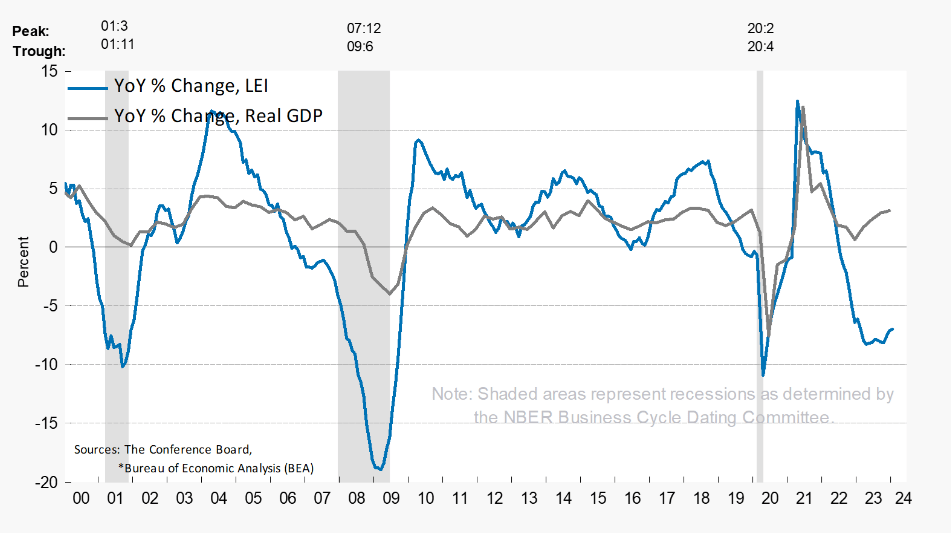

Published by the Conference Board the Leading Economic Index (LEI) "provides an early indication of significant turning points in the business cycle and where the economy is heading in the near term".

In late 2022 and for the duration of 2023 LEI has decreased significantly reaching levels that have historically coincided with major recessions in 2008 and 2020. However, economic activity seems to hold strong with GDP growth actually returning to moderate increases on an annual basis. Despite that, headwinds in economic activity should be expected to persist, yet a major recession might be avoided, as for the first time in the past two years, six out of its ten components of LEI turned positive indicating improvements in the macroeconomic environment are anticipated.

conference-board.org

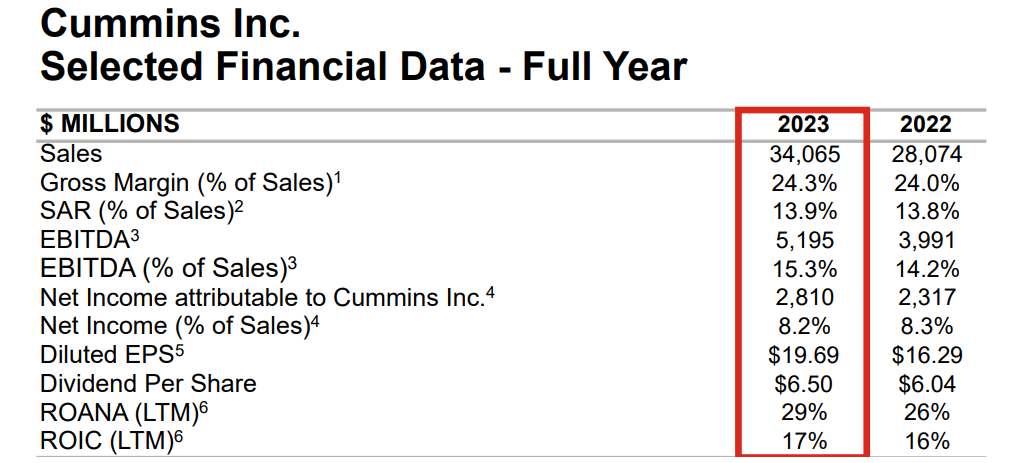

Fiscal year 2023 was one full of records in terms of financial performance, with sales growing by 21% to reach $34.07B (up from $28.07B in 2022) and profitability also improving across the board. Specifically, the gross margin improved from 24.0% to 24.3%, EBITDA margin increased from 14.2% to 15.3% and ROIC reached 17%. The net margin only slightly decreased to 8.2% (not including a non-recurring $2.0B charge relating to a regulatory settlement). Dividends also increased to $6.50 per share.

Investor Presentation 2024

Fourth quarter results also came in marking significant YoY increases, indicating that Cummins is carrying strong momentum entering 2024. Quarterly earnings increased from $7.77B in Q4 2022 to $8.54B in Q4 2023, while the apparent hit that EPS took ($4.14 compared to $4.54 in Q4 2022) is entirely attributed to the non-recurring regulatory charge mentioned earlier, as well as to some restructuring charges.

Cummins maintains a healthy balance sheet, presenting adequate liquidity (current ratio of 1.2x) and moderate financial leverage (debt/cash flow of 5.3x and debt/total capital of 0.3x). The $4.83B long-term debt balance that is currently outstanding, amounts to less than 15% of market cap and is sufficiently serviced through the company's cash flow generation.

Going forward, management sees revenue normalizing after the record year in 2023, forecasting a 2% - 5% decrease (a similar decrease is expected in earnings). EBITDA margins are expected to remain around 15% (higher than the sector average of 13.7%) and capital expenditure at $1.2B to $1.3B. From 2025 forward, however, analysts seem much more optimistic, forecasting growth in the low-double digits in EPS and mid-single digits in revenue.

Regarding the lowered 2024 expectations, management notes that they anticipate slowing demand, particularly in North America, as they explain that the commercial vehicle market hit its peak in mid 2023 and is expected to retract slightly going forward. This will be evident by a decrease in the production of heavy-duty trucks as well. The China outlook for the company also remains hard to accurately forecast.

Industrial stocks are often favored by dividend-oriented investors as they tend to deliver dividend yields higher than market averages, and also display relatively attractive dividend growth prospects. Specifically, the Industrial sector currently offers an average 1.62% dividend yield compared to the market's 1.40%, while dividends in the sector have grown at a 7.0% annualized rate over the last 5 years.

Cummins offers an even better dividend profile compared to sector averages. CMI's 2.60% dividend yield has grown at a 7.0% CAGR over the last 5 years, with a 7.6% growth projected on a one-year-forward basis. Dividend growth appears sustainable as the company is increasing EBIDTA at 8.3% (3-year annualized growth) and free cash flow at even higher rates. With a payout under 35% and 18 consecutive years of dividend increases, Cummins receives an A score for dividend safety and an A+ score for consistency from Seeking Alpha.

Shares outstanding have also decreased over the past years, further enhancing shareholder returns. CMI's diluted share count has reduced from 162.8M in 2018 to 142.7M at the end of 2023.

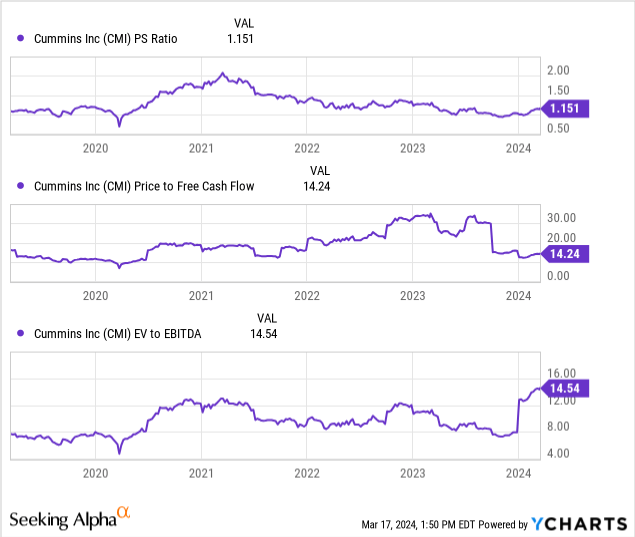

Despite a significant share price run-up over the past 12 months, CMI's valuation multiples remain at reasonable levels, offering investors an attractive value proposition going forward. Disregarding for a moment the GAAP P/E ratio of 53x (which is misleading as it includes the regulatory settlement charges mentioned earlier) we can observe, on a non-GAAP basis, a 13.95x P/E which seems rather appealing compared to the sector's 19.3x average P/E.

Moreover, as shown in the chart below, Cummins trades below 5-year averages both in terms of P/S ratio (1.15x compared to 1.5x for the sector) and P/FCF ratio (14.2x TTM). The EV/EBITDA ratio, on the other hand, indicates a slightly elevated valuation.

As with any cyclical industrial business, the macroeconomic risk could present arguably the biggest challenge going forward. A broader economic retraction or another flare up in inflation will hurt both the company's growth prospects and profitability. Delays in Cummins business model regarding the transition to a more environmentally friendly range of powertrains may also hamper growth in the long-term. On that note, competition from EVs (in the case than faster-than-anticipated technological progress is achieved in electric engines) in commercial vehicles' engines could, in theory, also affect the company's ability to market their products effectively. Finally, failure to maintain a positive, mid-single digit sales growth rate going forward, could lead to concerned investors lowering expectations and trigger a selloff.

After all things are considered, Cummins offers a respectable choice in the industrial sector for both dividend-oriented and value investors alike. Strong financial performance, coupled with a 100+ year track record of delivering quality products seems like an obvious choice in the sector, as valuation multiples also seem overall reasonable. For these reasons, I would rate CMI as a buy.