Haris Calkic/iStock via Getty Images

Haris Calkic/iStock via Getty Images

Chipotle (CMG) and Domino's (DPZ) have been amazing compounders in the past. They possess qualities that every business owner would wish for: a strong brand, excellent service, significant market share, growth, high margins, and high returns on capital. However, despite their past performance, both companies are facing challenges for investors now. I don't see either of them as a good buy right now.

I'll compare the businesses, explore their qualities, address their problems, and conclude what needs to happen for me to become interested. I'll also attach an entry price for each. Let's dive in.

Each has a good business model and is unique in its own right. The main difference between the two is that Chipotle's focus is on the quality and freshness of the food, while Domino's is focused on delivery and convenience.

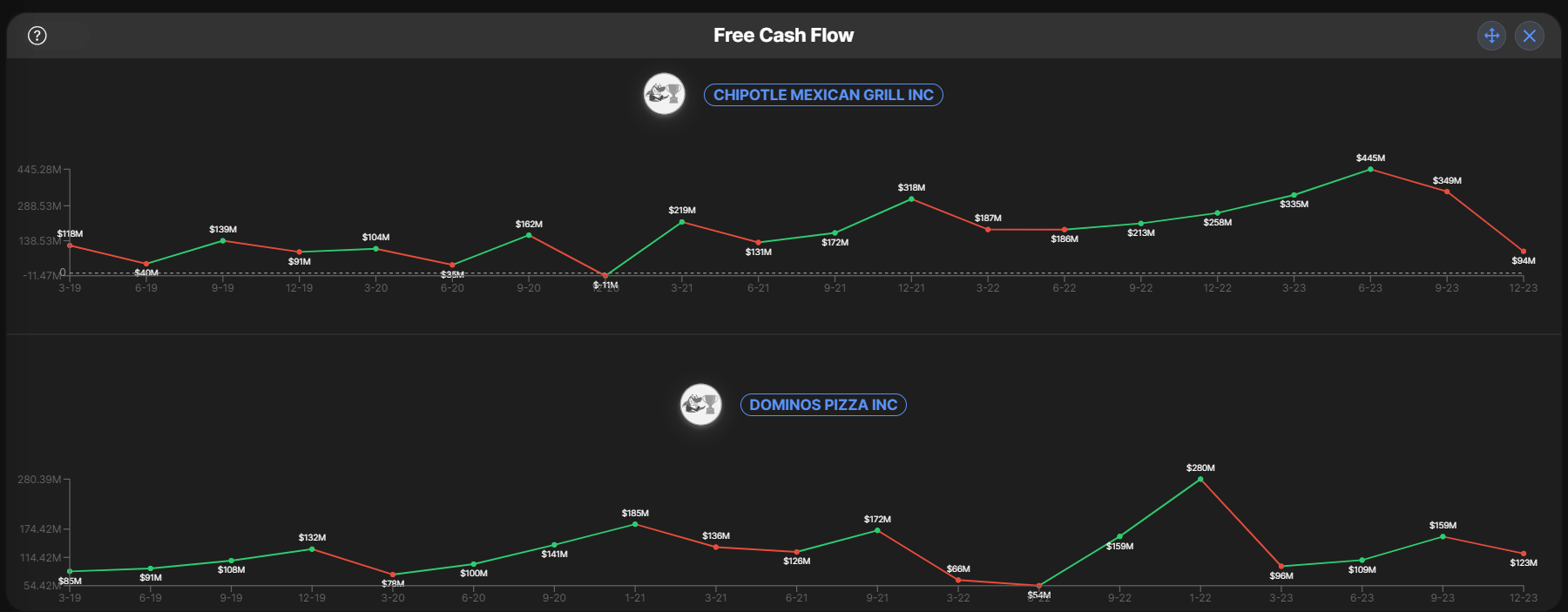

FCF growth (bigger-fish.com)

Chipotle made its brand name on high-quality food, in contrast to the McDonald's (MCD) and Burger Kings (QSR) of the world. They prepare food in front of the customer, unlike McDonald's, which usually uses frozen beef or fries. Chipotle is known for its freshness. However, this business method caused them serious problems in the past when there were food poisoning incidents that crushed their stock. Ironically, this was the best time to buy Chipotle. McDonald's hasn't faced serious food poisoning incidents in its long history, as far as I know and checked. Chipotle has serious tailwinds driven by the transition to healthier food, as concerns about obesity and unhealthy eating habits continue to make headlines.

Some would say this is an advantage, while others would say it's an inefficient way to operate, but Chipotle owns all of its stores. This gives them advantages in terms of more control over the supply chain, workers, work habits, food quality, service quality, and overall business control. Judging by the stock price, this has made them very successful thus far.

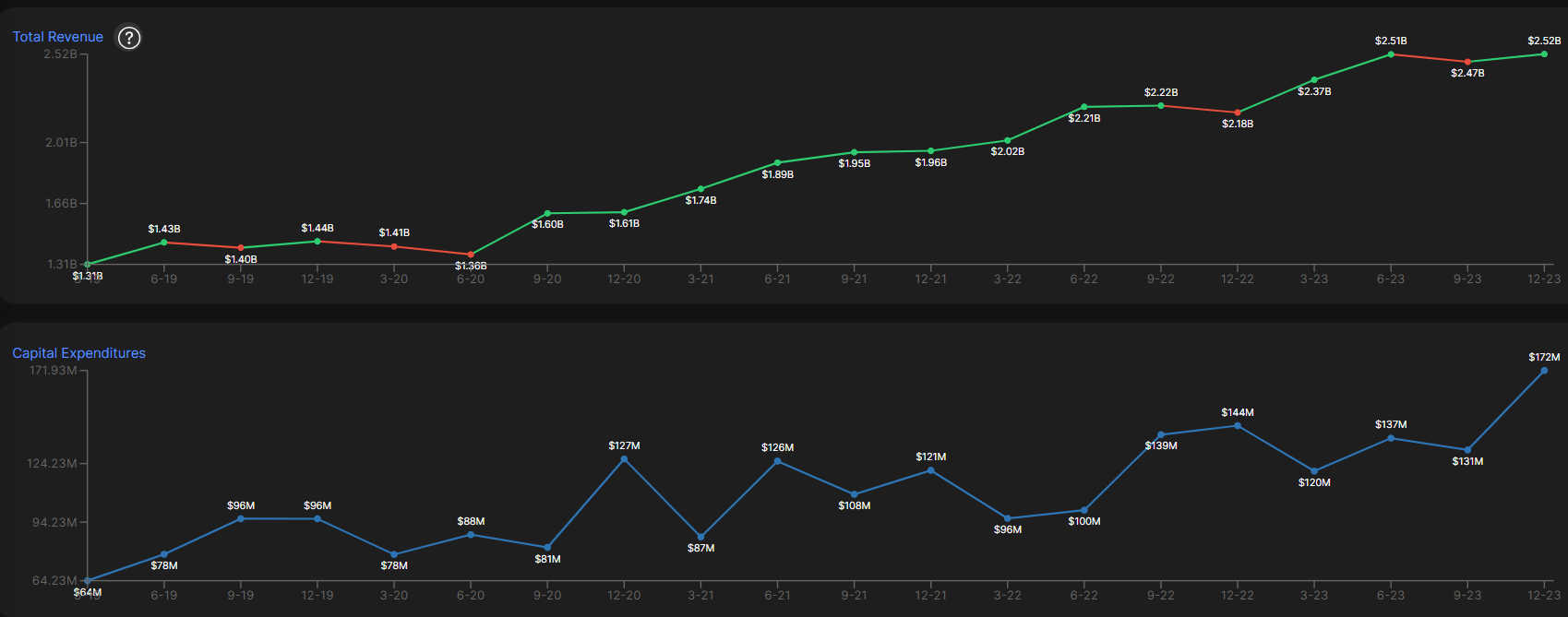

However, some disadvantages of such a business method include the capital-intensive nature of the model and exposure to real estate risks that could cause impairment issues in the balance sheet. The nature of the business requires significant capital expenditures, which can reduce free cash flow. But, as seen with many other businesses like successful retailers, if done systematically, the capital expenditure out of revenue is not significant, and the business can thrive.

CMG capex & revenue (bigger-fish.com)

In contrast, Domino's Pizza is not known for its high-quality or best-in-class food. They offer tasty food, but that's probably not why people choose Domino's. With plenty of other options available, people buy Domino's because it's convenient, fast, and affordable.

Earlier in Domino's history, they opened stores next to military bases and universities, targeting customers who needed a quick and convenient dinner option. Around 09', Domino's faced its lowest point, with some videos claiming their food was terrible and of low quality. In the late '00s', the new CEO Patrick Doyle decided to change things. Domino's made changes to its menu and improved the quality of its food, leading to a significant increase in its stock price. They captured more market share by using smart delivery and innovative systems to maximize efficiency, surpassing Pizza Hut and becoming the number-one pizza chain in the quick-service restaurant world.

Domino's has small stores with little or no seating because their focus is on delivery or carryout; they do not aim to provide a sit-down dining experience. Known for its innovative delivery systems, Domino's is essentially a technology company that delivers pizza. It boasts one of the best returns on capital in the market (Also, because of the high debt load), achievable due to the franchisee nature of the business. Essentially, 99% of Domino's business is franchised, allowing Domino's to collect fees on the brand as well as sales from its supply chain.

Domino's success is attributed to the highly profitable nature of the pizza business compared to other types of food. It is profitable for franchisees due to high-profit margins and profitable for Domino's as they avoid the capital-intensive nature of company-owned restaurants. Domino's owns around 288 restaurants, primarily serving as a test field for various delivery and efficiency methods. Some consider Domino's to be the ultimate food choice during recessions and periods of inflation because it remains affordable, making it less affected by economic downturns.

Essentially, to beat the market for a long period of time, you need to outperform expectations, especially when trading at a higher multiple than the average market multiple. You will likely need double-digit top-line growth, margin expansion, and, in Domino's case, buybacks as well. If we look back five years, Chipotle has exceeded expectations, leading to the company trading at very elevated multiples today, more than 60 times earnings. However, as we will see further down the article, Chipotle will need to achieve outstanding growth, which is unrealistic to justify today's multiple in my view. In fact, I owned Chipotle until recently and took advantage of the price hike after the split to sell. My philosophy is not selling; I want to hold my winners, but I have a limit. My limit is when the price can't justify the most optimistic outcome, and I think this is where Chipotle is now. But I will talk about it later in the valuation section.

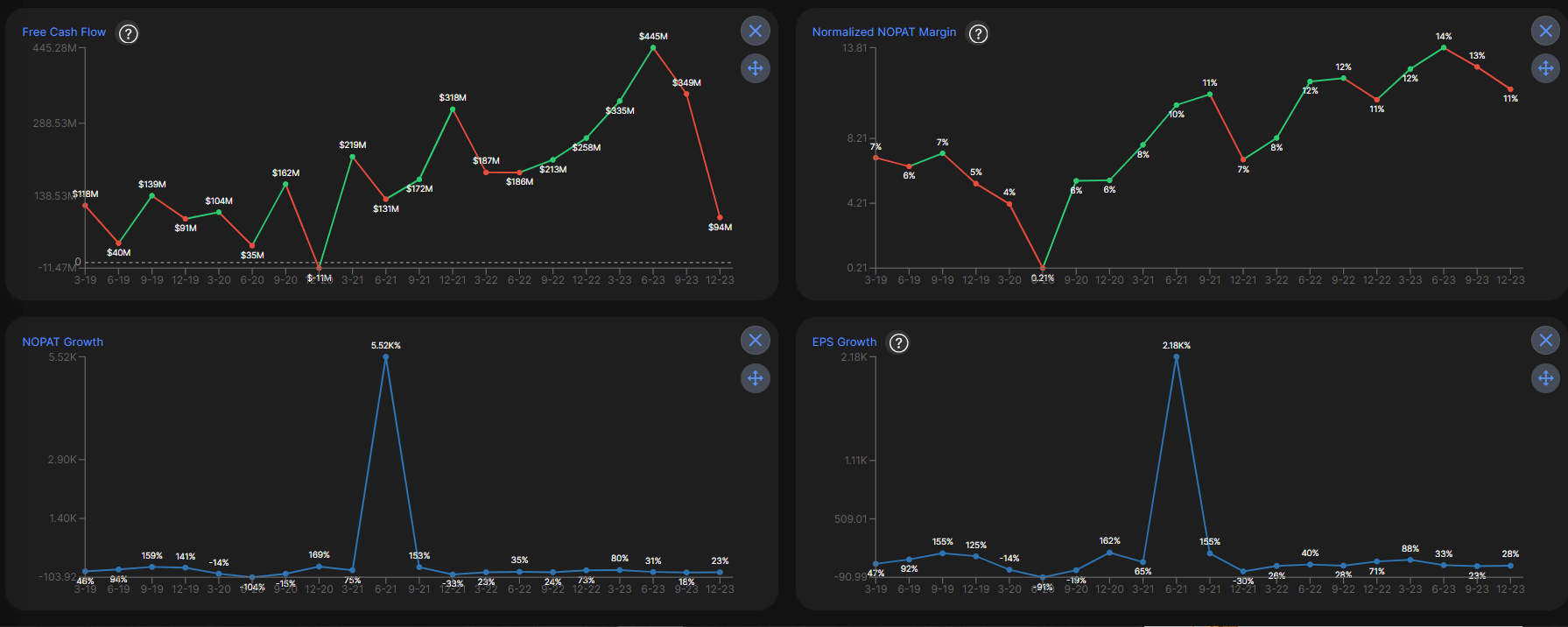

CMG growth in FCF & NOPAT (bigger-fish.com)

In contrast to Domino's, Chipotle achieved a high overall CAGR with more linearity. Especially linearity is something investors really appreciate.

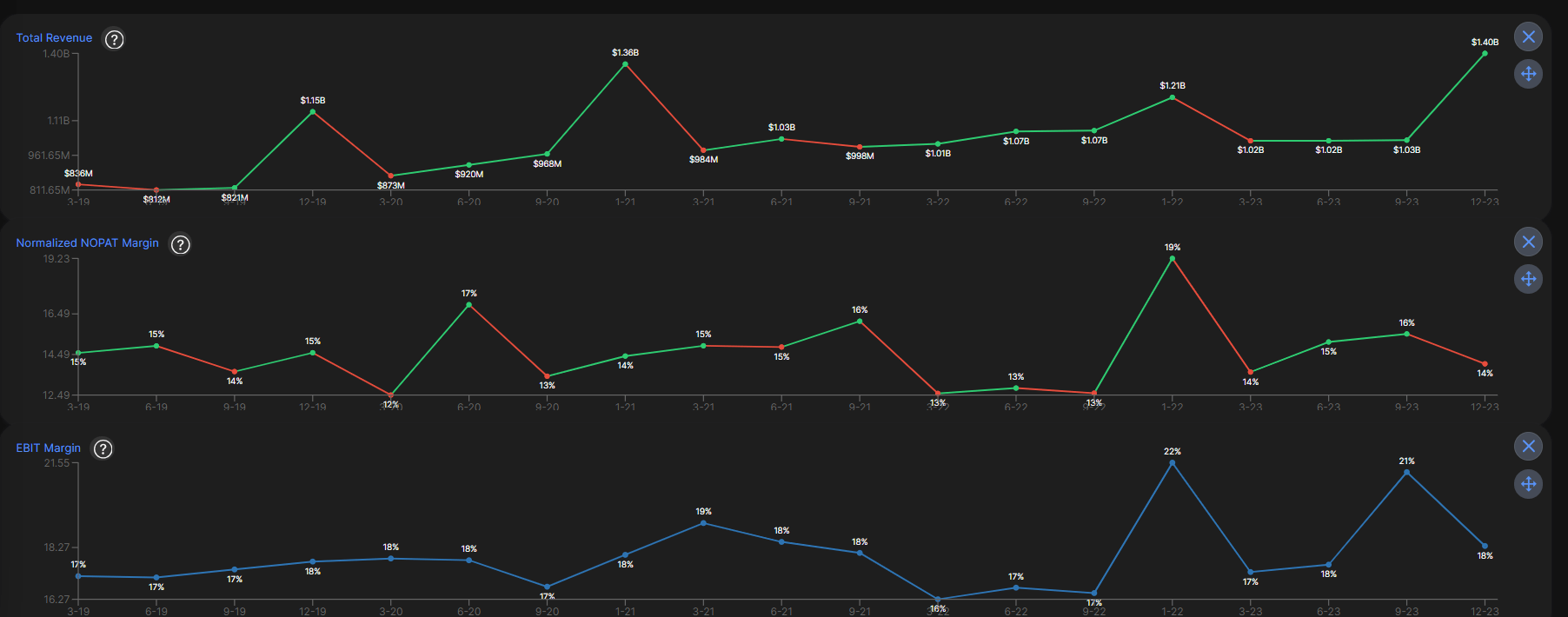

However, Domino's only achieved mid-single-digit CAGR, and to me, it is not surprising that they haven't beaten the market as the starting point was with a high multiple. I'm sorry, 30 times earnings can't be justified by 5% annual growth in the top line even if they manage to have significant operating leverage. As you can see in the chart below, this is not the case for Domino's. NOPAT margin as well as EBIT margin are pretty volatile and haven't grown since 2019.

Top line & margins for DPZ (bigger-fish.com)

For Domino's, this could be the result of higher competition from players like DoorDash (DASH) and Uber Eats (UBER). I'm glad to see from the management the new collaboration with Uber Eats. I like this collaboration because the efficient delivery system of Domino's will still be in use, but new customer flow can come from the Uber application. Domino's will still have control over the delivery and could maintain its trademark as the fastest and most efficient delivery restaurant.

Well, in my view, for Chipotle, it is only one reason: valuation. Generally, I'm pretty comfortable paying high multiples for high-quality businesses, especially if I think the growth path is going to be long-lasting. But I too have limits. Essentially, in the end, investing is all about valuation.

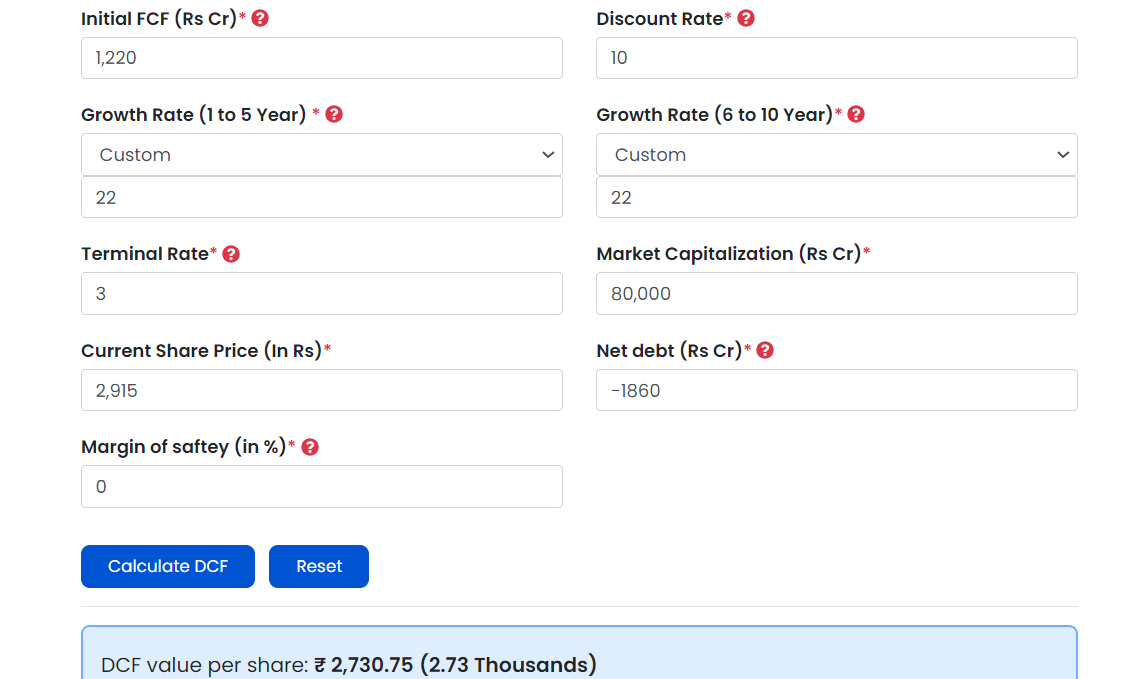

Let me give you some numbers: trading at above 60 times TTM earnings, even if CMG grows by 30% on the bottom line, the PEG ratio is 2, which is also pretty expensive. Assuming the top-line growth will be in the 15% CAGR area, which is outstanding for a mid-cap, there is simply not enough operating leverage here to further enhance margins and boost the bottom line. Here are more multiples for context. Just to grasp the valuation, many say Nvidia (NVDA) is in a bubble; yet, Nvidia trades at a forward P/E of 36, and Chipotle is at 54. I'll make a simple reverse DCF to further enhance the point. To justify today's price, starting with TTM free cash flow, Chipotle would need to grow 22% in the next 10 years. It is unrealistic in my view, especially as the business grows and faces the law of large numbers.

DCF (finology)

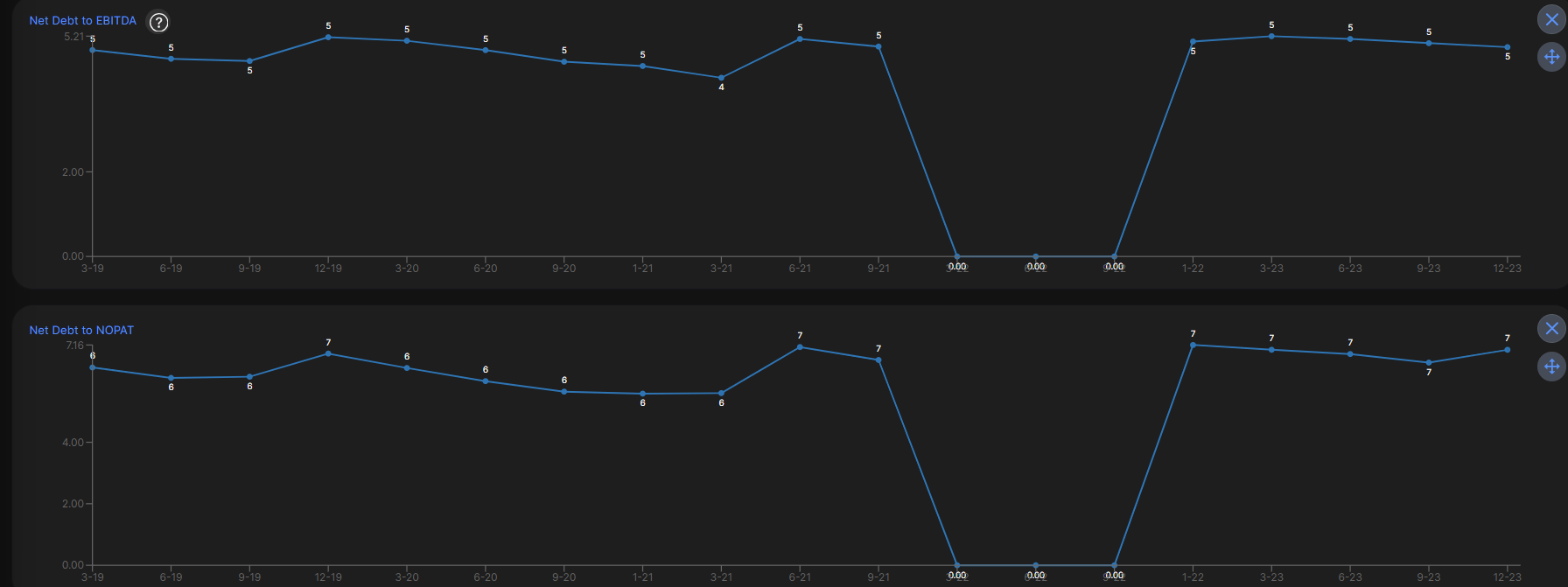

As for DPZ, it has two problems. First and most pressing is that the business needs debt to run itself. Essentially, all of the business' capital allocation is through debt, including dividends and the good buyback program that we have seen in the past decade. The most disturbing part of this is that it needs to take on more debt just to pay one year's principal. For example, in 2025, DPZ's principal payment will be $1.1 billion. I will compare it to the current free cash flow DPZ is generating of around $500 million and will add to that the current cash on hand (114M$), and I still don't come close to the debt payment next year.

Solvency (bigger-fish.com)

Now, don't get me wrong; Domino's has been highly leveraged in all of its recent history, and it played out pretty well for them. But as far as I learned from Mr. Buffett and others, a business that needs debt to run itself is a bad business.

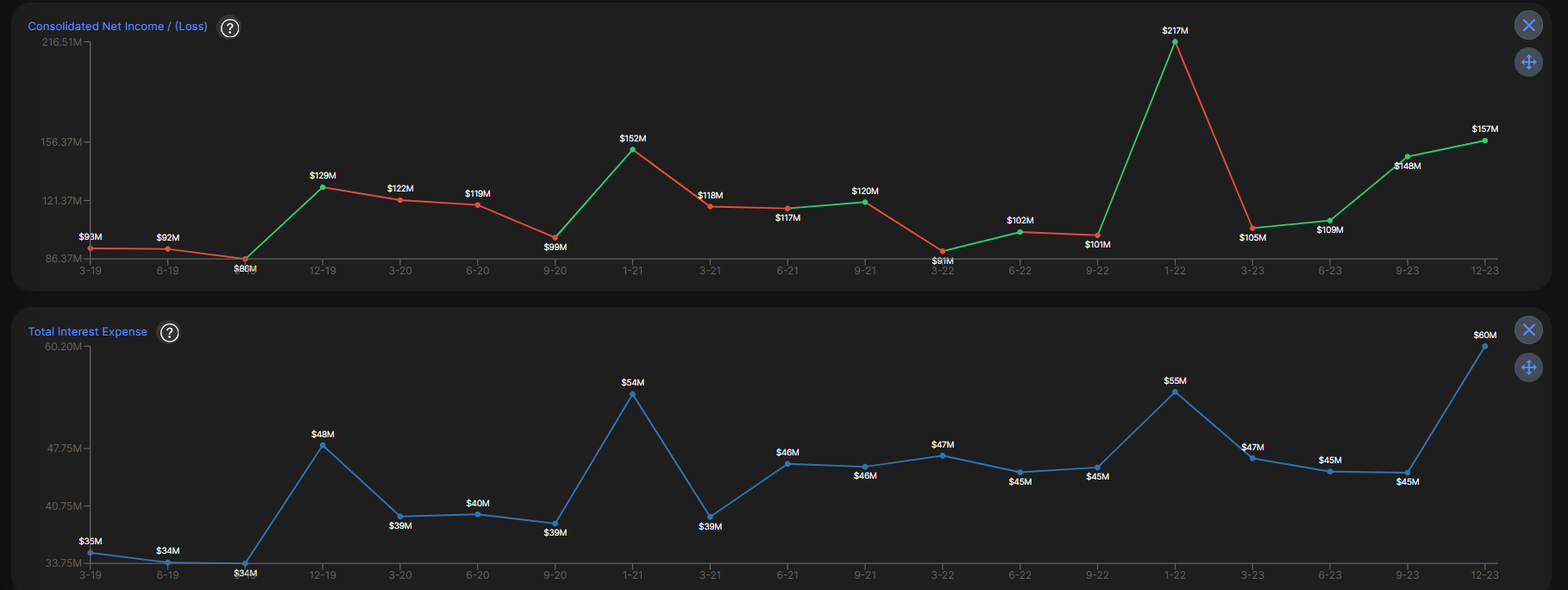

Let me illustrate the debt load further. About 38% of DPZ's net income is interest payments. To add to that, in the last decade, maybe it was smart to use a lot of debt in the low-interest rate environment, but as we are getting into the middle of the decade, low interest rates aren't the thing now, and we have almost two years of high interest rates already. Now, I'm not the expert on predicting macro movements, but I wouldn't bet we will get to the zero interest rate era anytime soon. That means Domino's will likely have more and more interest payments, and as illustrated before, they will most likely need to take on more debt to pay the current debt in a high-interest environment.

Interest expenses vs net income (bigger-fish.com)

The other problem of DPZ is its valuation. To put it simply, current growth can't support the current multiple. In my view, to justify 30 times earnings, you either need double-digit top-line growth or, in contrast, high operating leverage so you can achieve at least mid-teens EPS growth. Now, management's target is around 7% top-line growth, and that's if they would manage to revive the growth rates from the mid-single digits. Moreover, enhancing EPS via buybacks, would be inefficient at the current multiple, and it might even destroy value.

So essentially, to get to those mid-teen EPS growth rates, you will need significant margin expansion, and given the last five years, that doesn't seem to be the case right here. At least for me to invest in a business with loads of debt in a high-interest-rate environment, especially given it needs more debt to pay its current debt, I will need a significant margin of safety, and I don't see it here.

For me to get interested in Chipotle again, it will need to wait for the earnings to catch up to the price, or in contrast, the price will catch up to the earnings. It will be interesting again for me in the 30 times earnings area. I can't see Chipotle beating the market at its current prices. For Domino's to be interesting to me, it will need to be at around 15 times earnings. I need a good margin of safety for this type of balance sheet, especially with the delivery business getting more and more competitive.

I will give both companies a hold rating, and I will be waiting for better times to grasp these two great businesses.

Looking forward to your comments.