MicroStockHub/iStock via Getty Images

MicroStockHub/iStock via Getty Images

Cornerstone Strategic Value Fund, Inc. (NYSE:CLM) is a closed-end management investment company, originally incorporated on May 1, 1987. The vehicle is an equity CEF, aiming to provide investors with high dividends from a portfolio of equity holdings. Long term, the fund's total return matches the one exhibited by the S&P 500, but CLM is a classic story of a CEF marketing itself via a high dividend yield, with the vehicle now paying 18%.

In this article we are going to have a closer look at this CEF, its composition and financial engineering, and derive an opinion on whether retail investors are well served by entering this name at the current juncture.

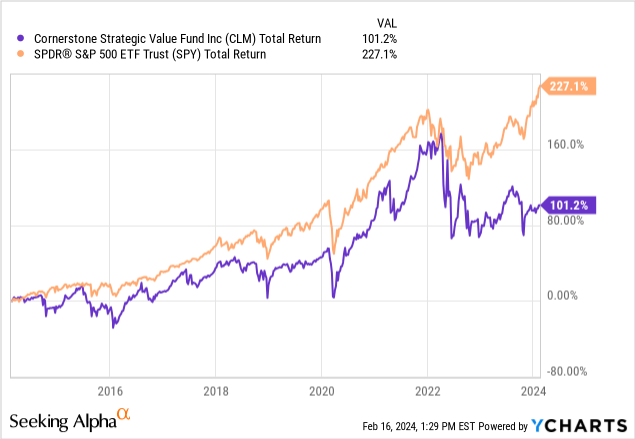

If we have a look at the total returns posted by the fund over a long period of time, we can notice CLM did a fairly good job of mirroring the S&P 500 total returns until the start of the 'AI revolution', and the run-up in prices for names such as Nvidia (NVDA):

An equity CEF which pays a very high dividend yield needs to be analyzed from a total return perspective, because that is what the CEF structure ultimately does - transform risk factor returns (in this case equities) into dividends. Up to the middle of 2022, CLM's total return closely matched the one exhibited by SPY, but then started lagging.

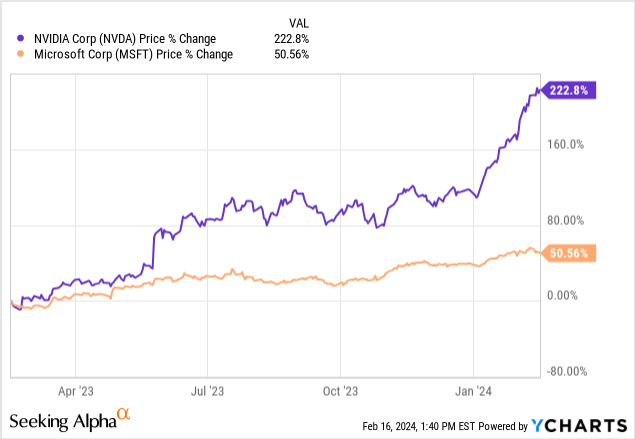

If we look at the fund's composition, we can see it is underweight certain AI names, namely NVDA, which represents only 3% of the CEF, versus 4.35% for the S&P 500. Similarly, another mega-cap tech winner, namely Microsoft (MSFT) is only 6% of CLM versus 7.2% for the S&P 500. Looking at the performance of these two names in the past year, we can begin to understand why these small differences start to matter:

In the past year, NVDA is up 222%, while MSFT is up 50%. If CLM would have been overweight AI names versus the index, it would have outperformed.

The CEF has a managed distribution plan:

The Fund has maintained its policy of regular distributions to stockholders which continues to be popular with investors. These distributions are not tied to the Fund’s investment income and capital gains and do not represent yield or investment return on the Fund’s portfolio. As always, the monthly distributions are reviewed and approved by the Board throughout the year and are subject to change at their discretion. In any given year, there is no guarantee that the Fund’s investment returns will exceed the amount of the distributions. To the extent that the amount of distributions taken in cash exceeds the total net investment returns of the Fund, the assets of the Fund will decline. If the total net investment returns exceed the amount of cash distributions, the assets of the Fund will increase.

Source: Semi-Annual Report

As a retail investor you need to understand that a CEF structure can set any dividend it wishes to do so. Certain CEFs utilize high dividend yields to attract investors, even if the underlying asset class cannot provide the cash-flows and capital gains to sustain those distributions.

CLM is very straight forward in the assertion that in any given year, the fund's assets might not generate the return necessary to cover the distribution, and thus in those instances the net assets of the fund will decline.

In effect, if we look at the long term returns provided by the S&P 500, they currently tally up to 12.5% annually on a 10-year lookback:

S&P 500 Returns (Morningstar)

This translates into the underlying equity portfolio in CLM only being able to generate 12.5% annual dividends, as long as the CEF mirrors the S&P 500 (which it has not). The current 18% yield the fund is paying is not supported, and based on empirical data, never will. Thus, you are looking at 5.5% (18%-12.5%) as always being a return of your own capital, rather than a true dividend yield.

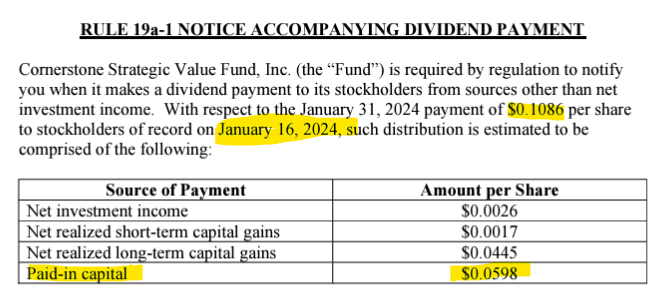

The fund's Section 19 notices also show a very heavy return of capital utilization:

January 2024 Section 19 Notice (Fund)

For the January 2024 payment date, over 50% of the dividend represents return of capital.

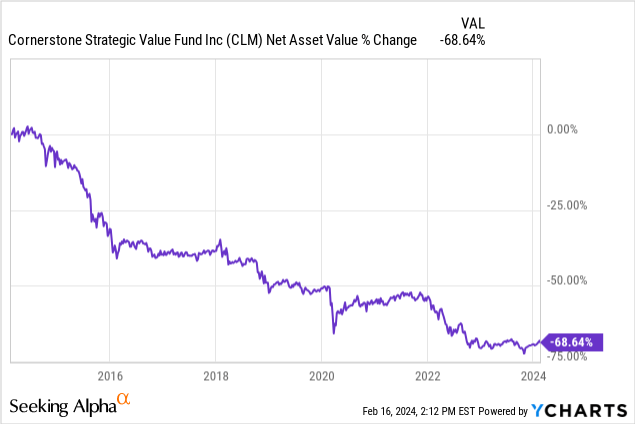

The discrepancy between what the S&P 500 can make annually (and thus CLM), and what the fund pays out in dividend distributions, can clearly be seen in the fund's historic NAV performance. As per the fund's own words, when they overdistribute, the net assets of the fund move down:

In the past ten years, the fund's NAV is down -68%, or roughly -6.8% per year, which equates closely to the figure we calculated above as the difference between dividend yield and what the S&P 500 generates. Expect this state of affairs to persist, since the S&P 500 will not be able to consistently generate 18% annual returns.

There are two main risk factors for this CEF:

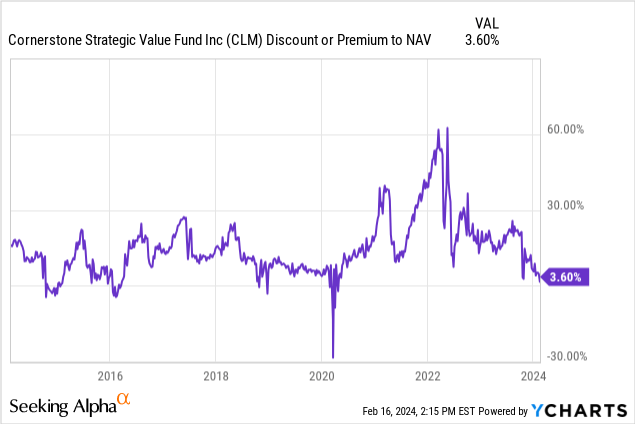

1. The fund has often times historically traded at very large premiums to NAV:

During the zero rates environment that characterized 2020/2021, the fund moved to an unreal 60% premium to net asset value. The good news is that the discount to NAV has normalized to a low level of only 3.6% premium to NAV. We expect the fund to trade in this range, absent a significant risk-off event which would push the CEF into discount territory.

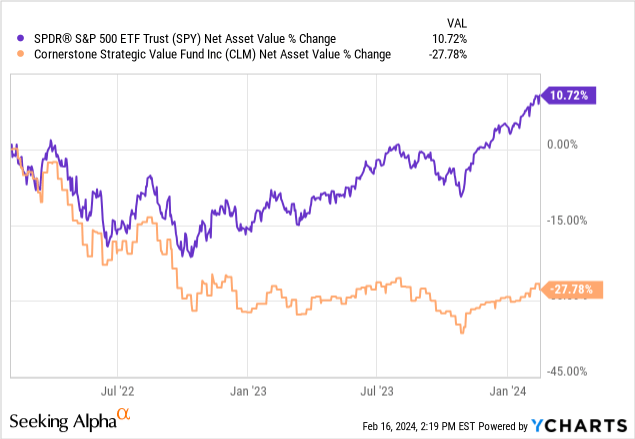

2. CLM will perform as long as the S&P 500 performs. If the overall equity market sells-off, the CEF will also lose value:

We can see the close correlation in CLM's NAV performance with the S&P 500 during sell-offs. We are looking at CLM's NAV here in order to eliminate any movements in the premium to NAV from the equation.

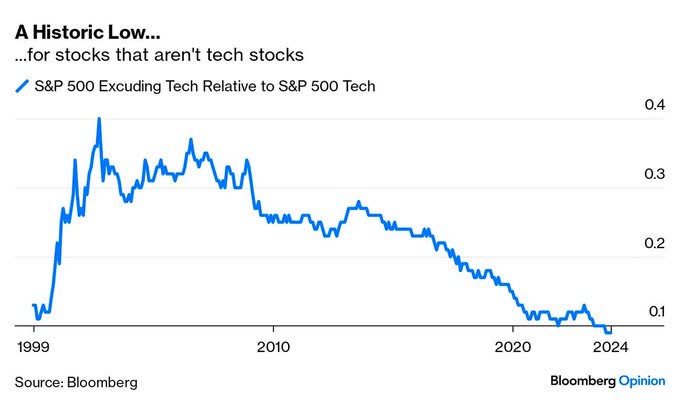

We believe the overall market is overbought here, driven by the AI names and tech mega-caps:

S&P 500 Tech vs Non-Tech (Bloomberg)

While AI related names and tech mega-caps have seen their P/E levels explode, stocks that are not tech stocks are at a low relative to the S&P 500 Tech names, and in fact have reasonable P/E ratios.

While some participants are arguing for a rotation from tech to other sectors, we feel the overall euphoric feel will be cured by a risk-off event, rather than witness a perfect soft landing.

CLM will sell-off with the market when that happens, and it might even move to a discount to net asset value on the back of such an event.

CLM is an equity CEF which has been in the market for over 30 years. The vehicle generally mirrors the S&P 500 total returns over long periods of time, but has lagged as of late, being underweight the AI names which have moved the market higher in the past year. This positioning has seen the fund's premium to NAV collapse to more palatable levels, the vehicle being now almost flat to NAV from a premium of almost +60%.

CLM pays a 18% managed distribution, but is very straight forward about the fact that fund assets will decrease if the underlying equities do not produce those types of annual returns. The S&P 500 in fact doesn't, with annualized figures over a decade coming in at 12.5%. The result has been an ever decreasing NAV for the fund, which investors should expect to continue.

While the premium to NAV risk factor is now within more normal parameters, the fund is still subject to overall equity market moves, and we feel we will witness a significant risk-off move this year. In our view, CLM's risk is skewed to the downside in the next 12 months, driven by the fund's equity risk factor. The fund's 18% yield is a mirage, and a long term investor should expect a true yield closer to 12.5% if the CEF is bought close to market bottoms rather than interim tops. We would find this name appealing -15% lower from here, and would like to see the name move to a discount to NAV first on the back of an overall market risk-off event.