Pla2na

Pla2na

Core Laboratories Inc. (NYSE:CLB) did not deliver better net sales than expected in the last quarter, however the outlook with regards to international recovery of exploration efforts was beneficial. Additionally, management noted demand for reservoir description services thanks to automation and digitalization, and we could expect the same to happen in the future. I do see certain risks from supply chain disruptions, lower investments in explorations, and volatility in the stock price, however CLB could trade a bit more expensively in my view.

Core Laboratories was founded in 1936, and has achieved a leading position at an international level in terms of providing specialized services for clients in the oil and gas industry, punctually regarding the study of reserves, and the development of product improvement.

Operations are divided into two segments: reserve description and product improvement. Services are provided through an international network of company agents, while production is carried out in five global-based production facilities. In some cases, the services of both segments are offered in parallel to the same client, and are accompanied by advice for the start of extraction and oil projects.

The first segment carries out studies on the reserves to optimize the extraction processes as well as to improve the recovery of crude oil in the model of its clients. The service includes field analysis and subsequent treatment of the fluids in specialized laboratories for this purpose. Analysis and description services are not limited only to oil reserves, but also reach clients seeking to make energy transitions in their production, reduction of their carbon footprint, hydrogen storage, geothermal projects, and preparation for mining activities linked to lithium among others.

The product improvement segment provides comprehensive diagnostic services for the optimization of extraction, drilling, stimulation, and production processes. The main objective of these services is to monitor the completion of projects as well as to analyze each phase of development to optimize both the productivity and raw materials recovery circuits.

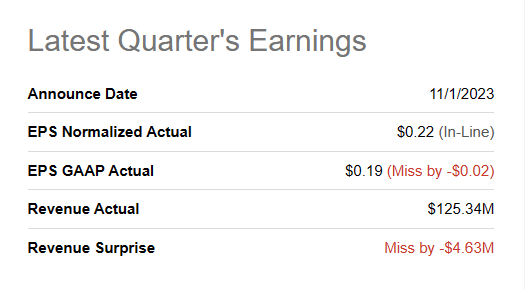

With that about the business model, it is worth having a look at the most recent earnings release and the current valuation. In my view, the market did not digest the recent EPS GAAP numbers, which were lower than expected, close to $0.19 per share. Quarterly revenue was close to $125.34M, a bit lower than expected.

Source: SA

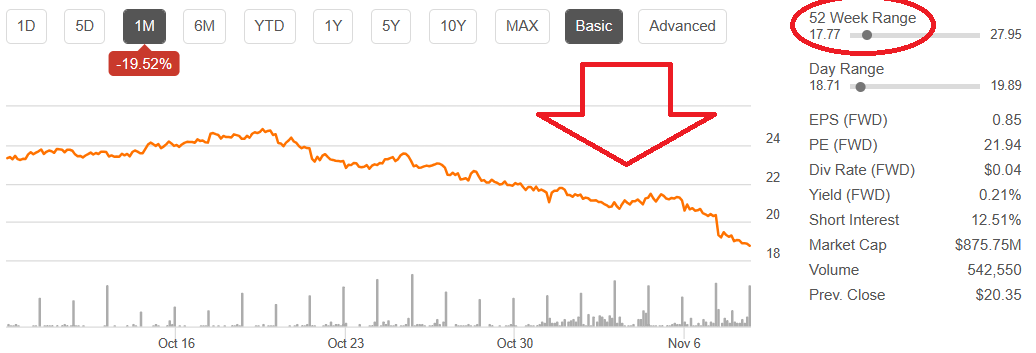

As a result, the company saw a decline in its shares from about $24 per share to close to $18-$19 per share, which is close to the lowest part in the 52 weeks range. Even before having a look at the valuation, I believe that the company may represent an opportunity in terms of its stock price.

Source: SA

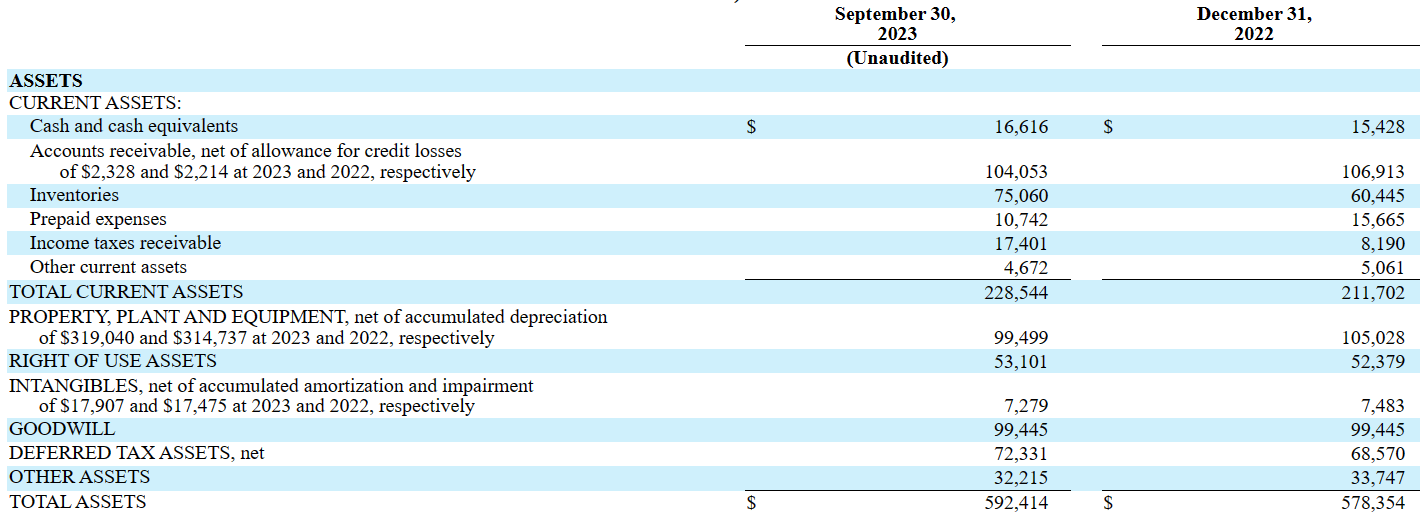

As of September 30, 2023, the company reported cash and cash equivalents of about $16 million, accounts receivable worth $104 million, inventories close to $75 million, and total current assets of $228 million. With current liabilities of about $84 million, I believe that the current ratio appears very healthy.

Core Laboratories also reported property, plant, and equipment of $99 million, intangibles of $7 million, and goodwill close to $99 million. Finally, total assets are equal to $592 million, and the asset/liability ratio appears larger than 1x. In sum, I believe that the balance sheet is quite stable.

Source: 10-Q

I do not think that the total amount of liabilities appears worrying, however shareholders may want to have a look at the total amount of debt and the interest being paid.

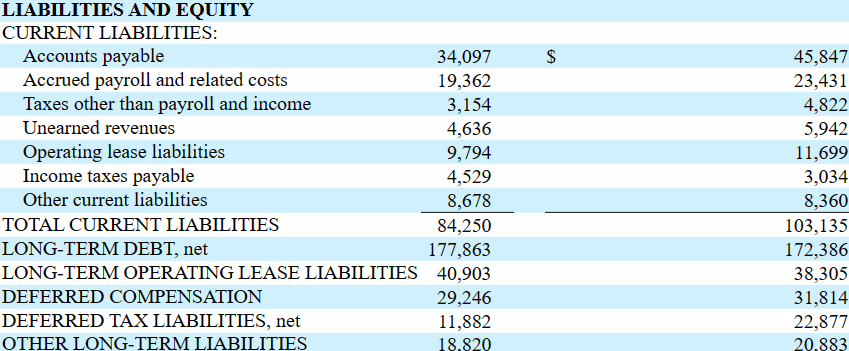

Accounts payable stood at $34 million, with accrued payroll and related costs of about $19 million, unearned revenues worth $4 million, and long-term debt of about $177 million. Finally, with long-term operating lease liabilities of about $40 million and deferred compensation worth $29 million, other long-term liabilities were equal to $18 million.

Source: 10-Q

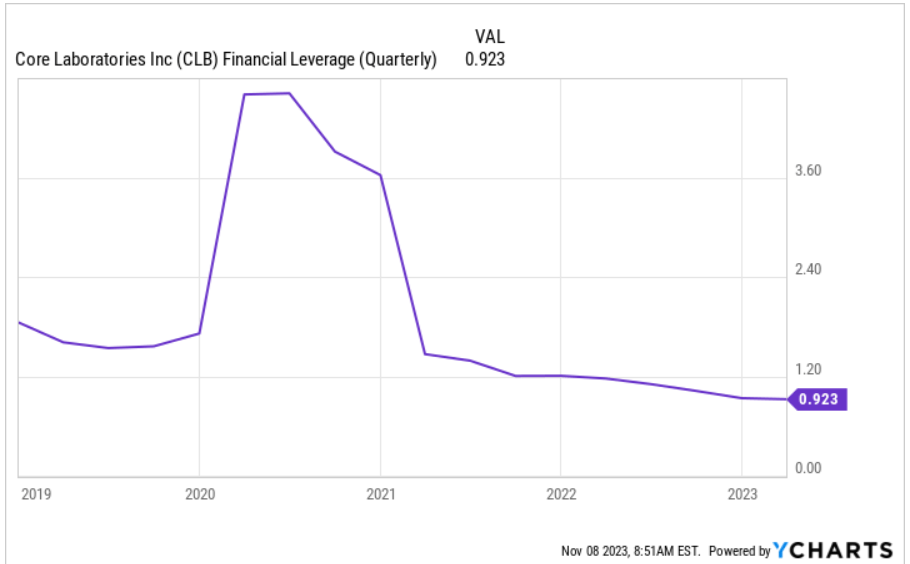

The total amount of leverage does not seem significant, however Core Laboratories recently reduced its financial leverage significantly. I believe that a further decrease in the total amount of leverage would most likely lead to more interest in the stock from the investment community.

Source: YCharts

The assessment of the senior notes indicates that Core Laboratories pays interest rates close to 4% and 7.5%. I believe that a conservative cost of capital would most likely stand at close to 5%-7%.

Source: 10-Q

In my view, further automation, digitalization, and operational efficiency improvement could continue to accelerate the demand for Reservoir Description services offered by management. As a result, we may see increases in FCF growth and net income growth. Note that I am not really thinking out of the box. In the last quarterly report, the company noted that this type of services continued to offer operating margin increases. Read the following lines in this regard.

Demand for Reservoir Description services continued to expand in the third quarter of 2023, with sequential improvement in both revenue and operating margins. Execution of our long-term strategy to improve operational efficiencies through technological innovations, automation and digitalization is also yielding results, as Reservoir Description’s operating margins for the third quarter were 17%, the highest in three years. Source: Quarterly Release

There is an international recovery of exploration efforts in many countries in the Middle East, South Atlantic Margin, certain areas of Asia Pacific, and West Africa. If management is not wrong about its international expectations, I believe that we may see business growth in the coming years.

Core continues to anticipate a multi-year international recovery supported by increased spending on exploration in many regions across the globe and expanded development of existing fields to fortify crude oil and natural gas reserves. This underlies Core's outlook for continued improvement in international onshore and offshore activity, with on-going projects around the globe, most notably across the Middle East, South Atlantic Margin, certain areas of Asia Pacific and West Africa. Source: Quarterly Release

Let us also remember that the company is carrying out the restructuring of its model to have a better centralized positioning in relation to international activity, with a view to strengthening its international service network and achieving customer scale.

I would expect further increases in the portfolio of products developed from the particular needs of each client, therefore expanding the geographical footprint of its international network, and keeping the door open for the acquisition of new potential technologies to be integrated into the company's current analytical and productive capabilities.

The company's Production Enhancement team appears to have substantial experienced technical services personnel to support clients and rapidly introduce new products. I cannot go through all the products designed, but perhaps a clear example of broad acceptance is FLOWPROFILERTMEDS, an engineered delivery system that will most likely continue to bring more net sales growth in the coming years. I think that existing clients using these technologies may give a try if the company designs new systems.

There has been a broadening acceptance of FLOWPROFILERTMEDS, a proprietary technology, which is an engineered delivery system. The break-through EDS technology delivers time-released diagnostics for evaluating the crude-oil flow from each stage of a hydraulically fractured completion. Source: 10-k

In recent years, Core Laboratories expanded its functionalities towards carbon capture projects, and it is part of the current objectives to deepen this trend, taking advantage of market demand in this sector. Given the expectations about these services and double digit growth of the global carbon capture, utilization, and storage market, net sales growth of Core Laboratories could increase.

Carbon Capture, Utilization, and Storage Market Overview-2030. The global carbon capture, utilization, and storage market was valued at $1.9 billion in 2020, and is projected to reach $7.0 billion by 2030, growing at a CAGR of 13.8% from 2021 to 2030. Source: Carbon Capture, Utilization, and Storage Market AnalysisWe intend to continue concentrating our efforts on services and technologies that improve reservoir performance, increase oil and gas recovery, CCS projects and other projects directed at the global objectives in reducing carbon emissions. Source: 10-k

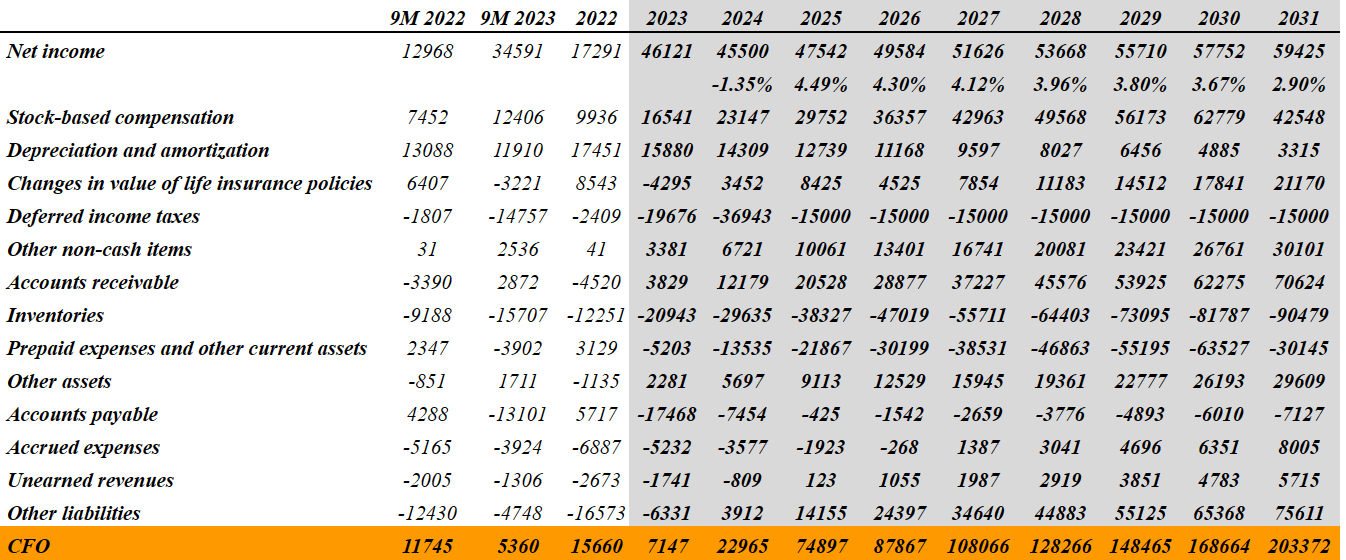

My cash flow model includes 2031 net income close to $59 million, stock-based compensation worth $42 million, depreciation and amortization of $3 million, and changes in value of life insurance policies close to $21 million.

Besides, I also took into account deferred income taxes worth -$15 million, other non-cash items of about $30 million, changes in accounts receivable close to $70 million, and changes in inventories of -$91 million. Finally, taking into account 2031 prepaid expenses and other current assets of -$31 million, changes in accounts payable close to -$8 million, and changes in other liabilities of $75 million, 2031 CFO would be close to $203 million. If we also assume 2031 capital expenditures of -$7 million, 2031 FCF would be $196 million.

Source: CW Capital Source: My DCF Model

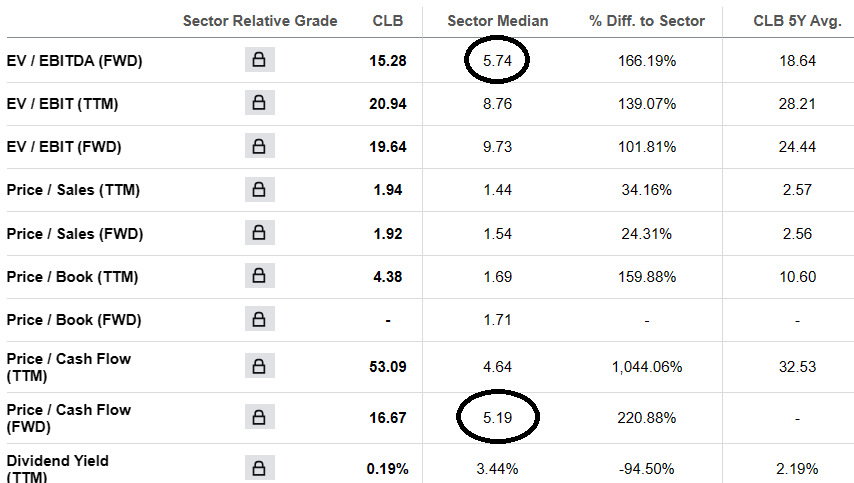

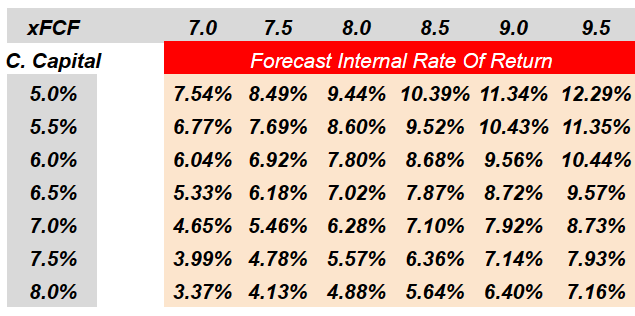

For the assessment of the exit EV/FCF multiple, I took into account that the sector median EV/EBITDA is close to 5.7x, and the price/cash flow is 5.19x. The company currently trades at more than 15x EBITDA. With these figures, a sensibility analysis around 7x-9.5x appears reasonable.

Source: SA

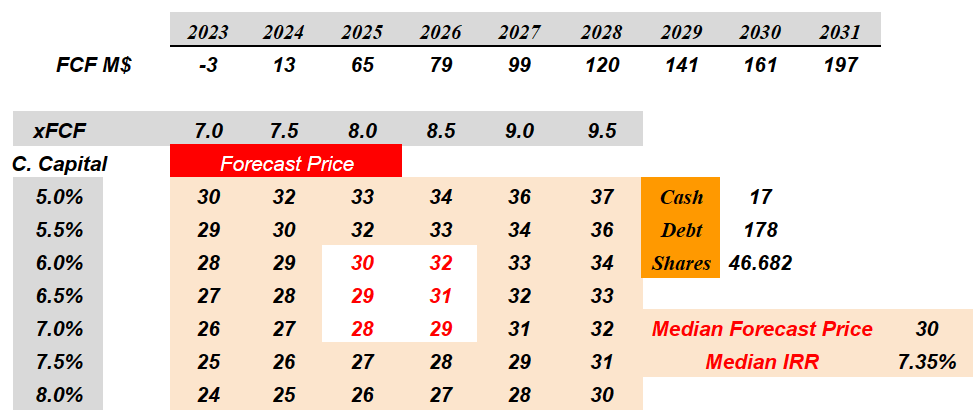

With a forecast of FCF of around -$3 million and $197 million, cost of capital of 5%-8%, and EV/FCF of 7x-9.5x, the implied forecast price would be close to $24-$37 per share. The median forecast price would be $30 per share, and the median IRR would not be far from 7.35%, however I also obtained results close to 3% and 12%. In any case, I believe that there exists certain undervaluation.

Source: CW Capital Source: CW Capital

There is not really established competition in all lines of business for Core Laboratories, which means that it receives active competition from mainly regional suppliers over specific reserve areas for each segment. Also, joining the competition are the subsidiaries or internal divisions of some companies in the oil sector that have sufficient structure to carry out their own technological developments and analysis procedures without the need to hire third parties.

One of the main risks at present involves the success of the company's restructuring, particularly whether or not it results in an overall reduction in the company's overall costs.

Source: 10-k

Along with this, volatility or behavioral changes within the oil industry also mean a risk for operating margins for Core Laboratories.

International exposure due to its presence is also a risk, and particularly to the commercial activity that the company maintains in Russia, faced with the possibility of new sanctions, or legislation in relation to border crossing of products, for both imports and exports.

The geopolitical conflict between Russia and Ukraine, which began in February 2022 and continued through December 31, 2022, has resulted in disruptions to our operations in Russia and Ukraine. The Company’s operations and assets in Ukraine are immaterial. As of December 31, 2022, all laboratory facilities, offices, and locations in Russia continued to operate and remained profitable and no specific asset losses were identified. Source: 10-k

Even delivering lower quarterly EPS than expected in the last quarter, Core Laboratories is definitely a must-follow stock considering the international recovery of exploration efforts noted by management. Additionally, further demand for reservoir description services may continue to grow thanks to automation and digitalization, which may lead to further FCF growth. I do see risks from lower exploration efforts overseas, supply chain issues, lower crude oil prices, or failed introduction of new products. However, I believe that the stock could trade a bit higher from here.