Brothers91/E+ via Getty Images

Brothers91/E+ via Getty Images

After covering a wide range of macro and income-focused articles, I wanted to take a detour to focus on a company that I have never discussed before.

As the title of this article already gave away, that company is Chewy Inc. (NYSE:CHWY).

I've had this company on my radar for a while. As the company just released its earnings, this is a fantastic time to dive into a stock that may be one of the most undervalued stocks on my radar.

The problem is that it's only undervalued if management is able to bring growth back on track.

So, with that said, let's dive into the details!

At this point, you may be wondering what Chewy does.

Chewy, which was formerly operating under the name Chewy.com, is an online store for everything "pet parents" need.

Founded in 2011, the company sells high-quality products and services at competitive prices. This includes a selection of roughly 115,000 products and partnerships with more than 3,500 brands in the pet industry.

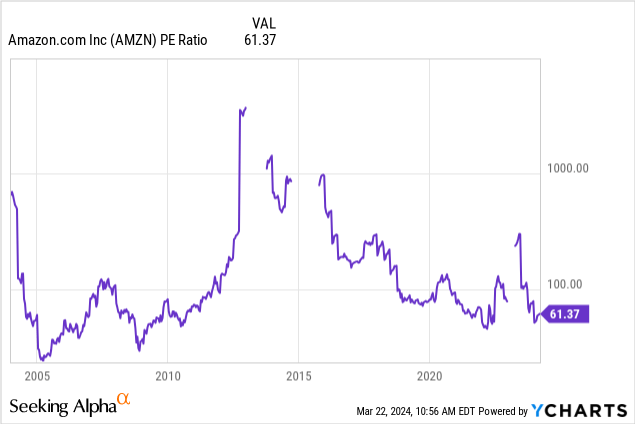

Or to put it differently, Chewy is like an Amazon (AMZN) for pets.

This is what their website looks like:

Chewy

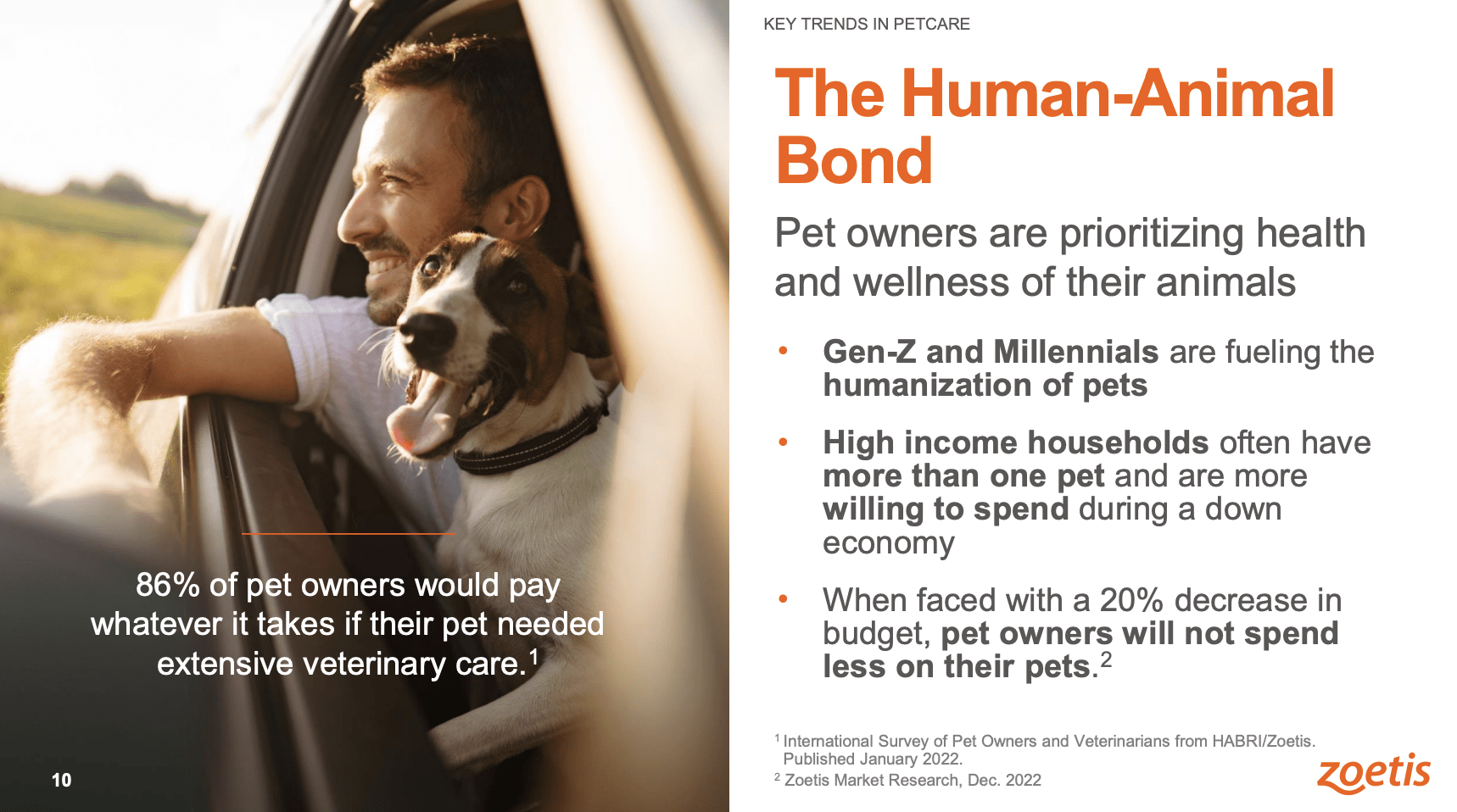

As some readers may remember, another pet-focused stock on my radar is Zoetis (ZTS), a veterinarian healthcare company.

One of the biggest reasons Zoetis is bullish about its future is secular growth in spending for our pets.

Zoetis Inc.

Chewy sees the same developments as it tries to benefit from trends like "pet humanization" and "premiumization," where pet owners increasingly view their pets as family members.

This includes a higher willingness to spend.

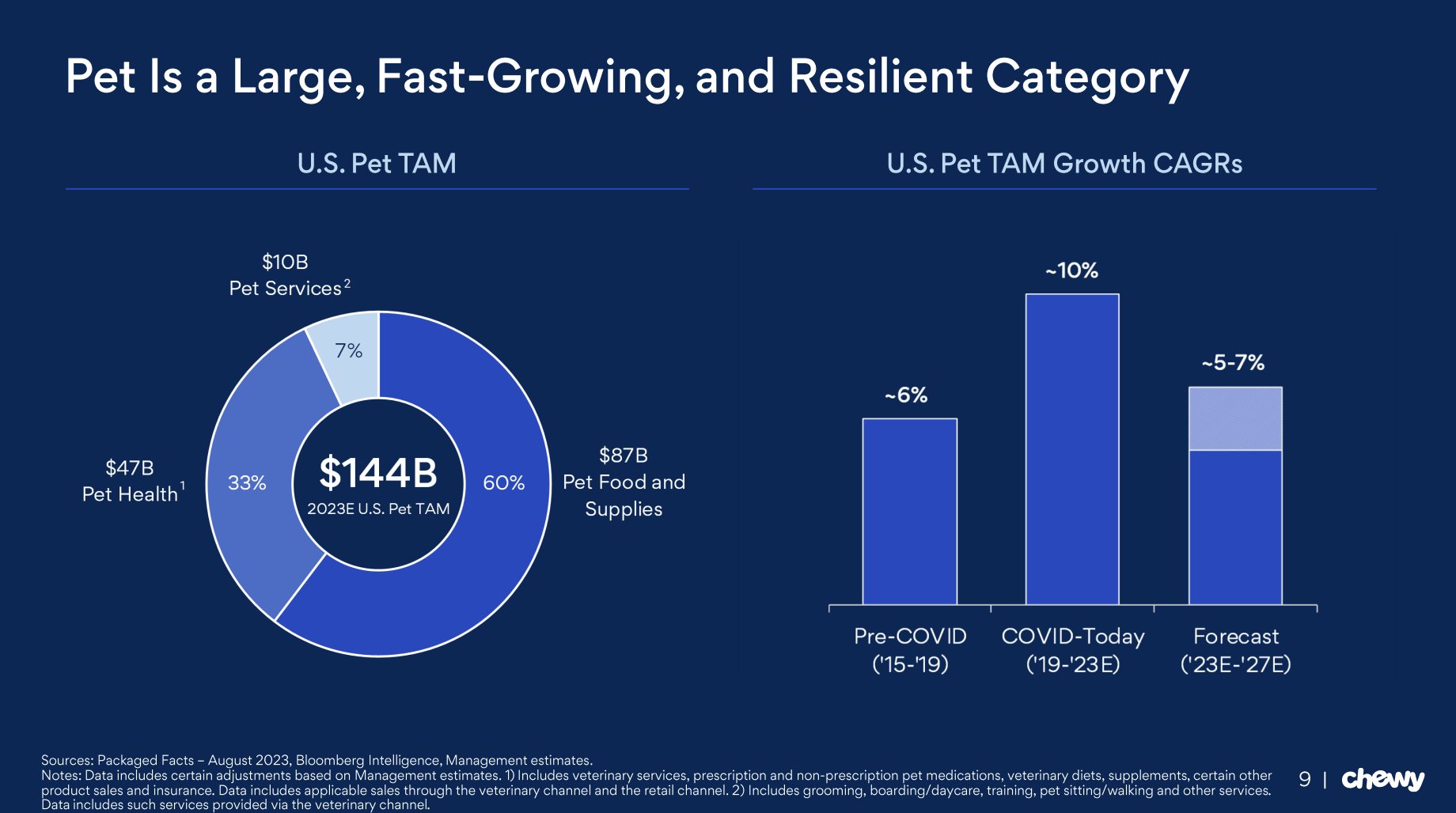

Using data from August 2023, we see that the total addressable market for the company is $144 billion. Most of this consists of food and supplies.

Chewy

This market is expected to maintain 5-7% annual growth through 2027. That's roughly in line with pre-pandemic growth.

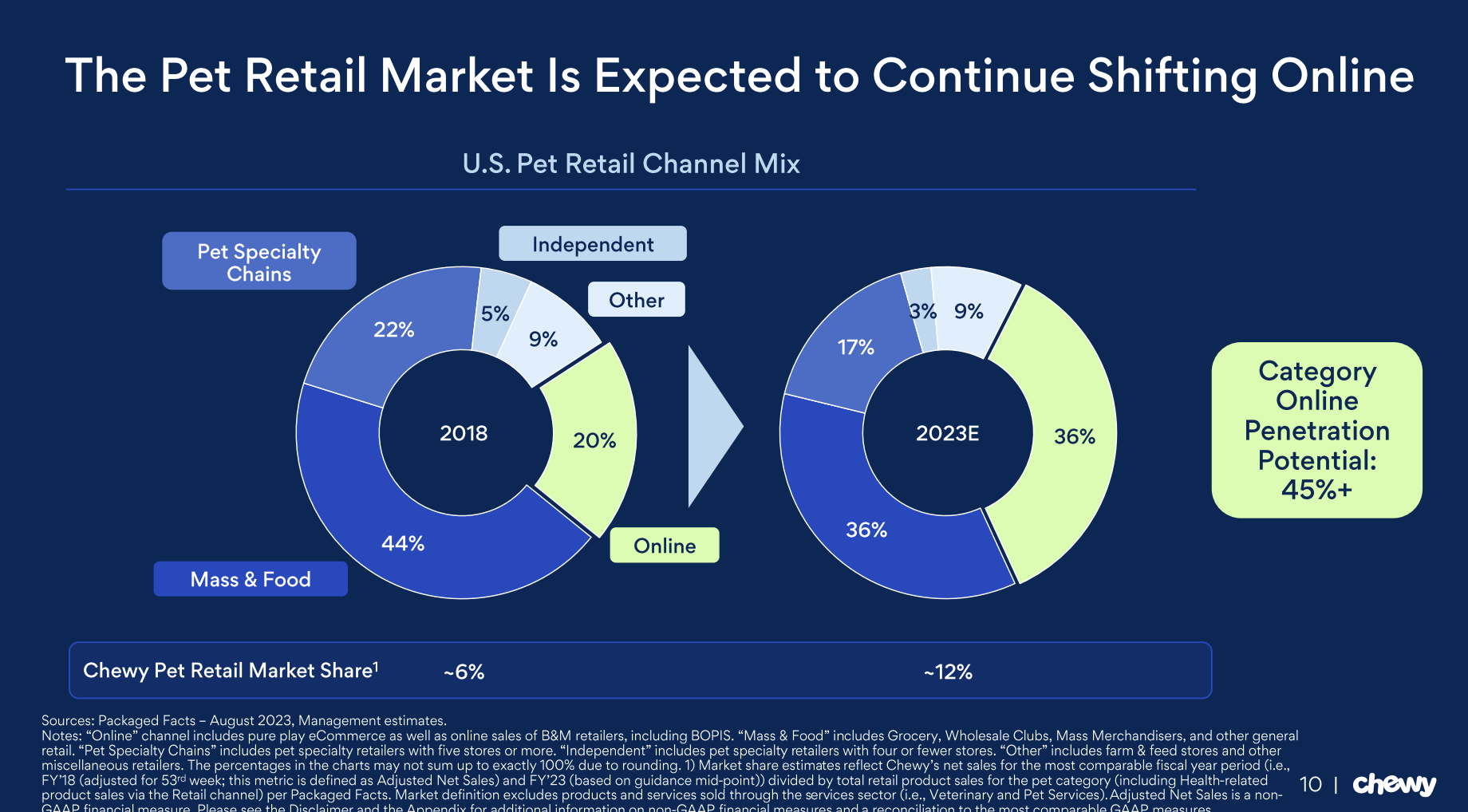

Even better, e-commerce is expanding even faster. Last year, 36% of the pet retail market was online. That's up from 20% in 2018.

In the pet retail market, Chewy enjoys a 12% market share. That's double its market share in 2018!

Chewy

You know what's even better? The fact that subscription-based selling is gaining popularity. This means higher recurring revenue and better visibility.

According to Chewy, nearly 40% of pet product shoppers subscribe to services for pet food, treats, and grooming products.

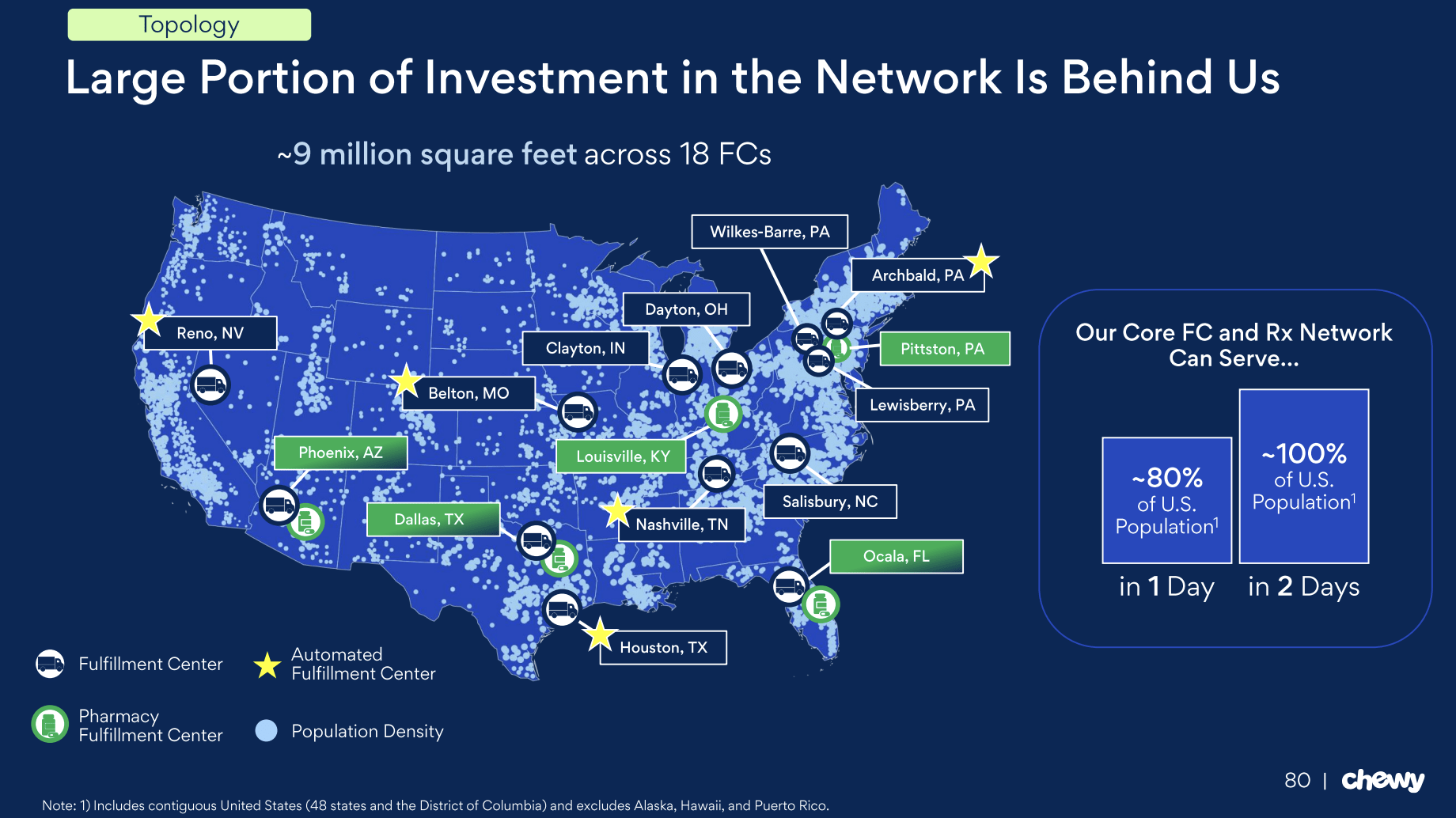

In light of these numbers, it helps that the company has spent aggressively to boost its distribution network. Having a solid distribution network is one of the most important attributes of a company that wants to compete based on service quality.

Using the company's own data, it can reach 80% of the U.S. population within one day. It reaches every single American within two days.

Chewy

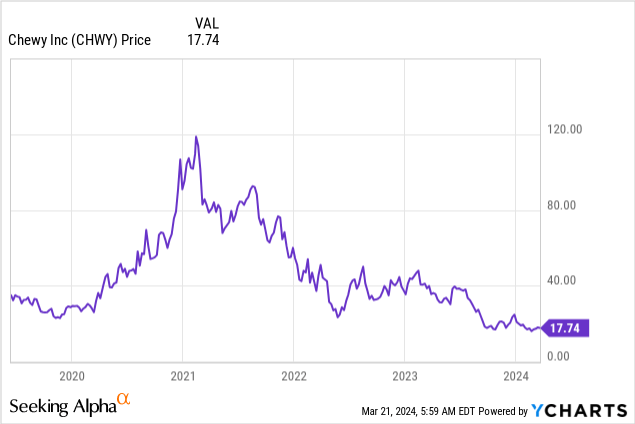

Having said all of this, if you didn't know what the Chewy stock price looks like, you would probably guess that it looks good, right?

Unfortunately, for the company, that is not the case.

After going public on June 14, 2019, the company massively benefitted from the pandemic, which caused its stock price to rally to roughly $120.

Since then, things have gone south very consistently.

While I am writing this, investors are paying close to $18 for a share of this Florida-based internet retailer.

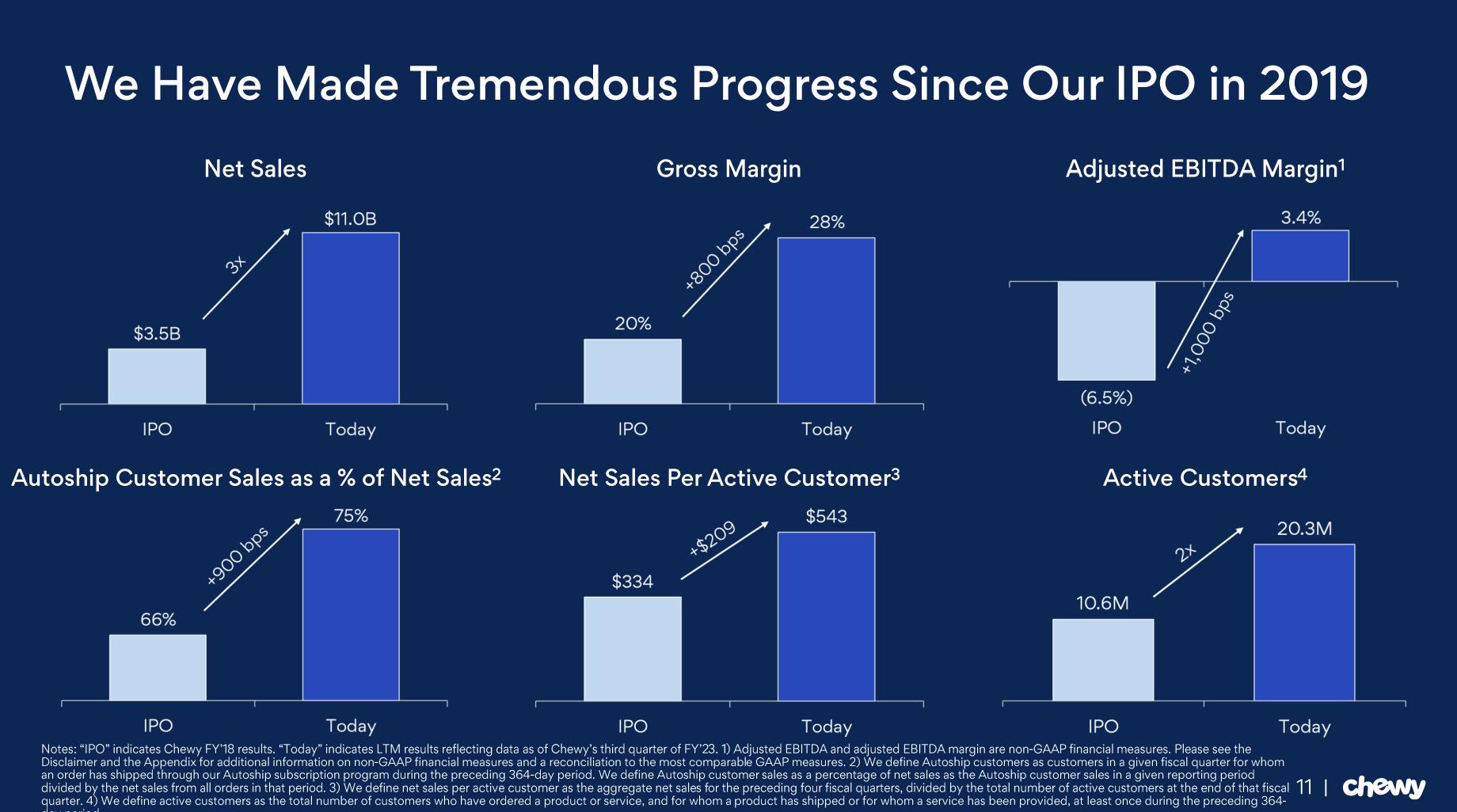

What's even "weirder," is that the company has done quite well since its IPO.

Chewy

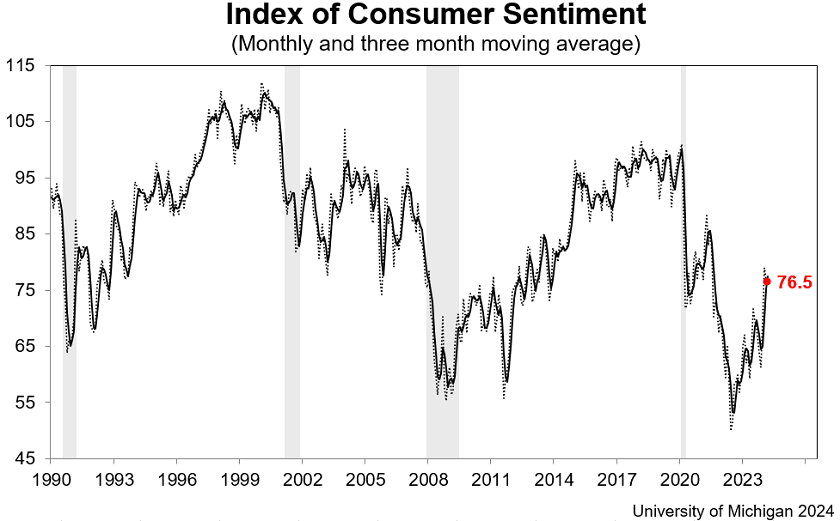

This begs the question, how cheap is Chewy? And what is going on?

The problem is that the pandemic was followed by elevated inflation and an implosion in consumer confidence.

University of Michigan

Essentially, there are three (related) problems:

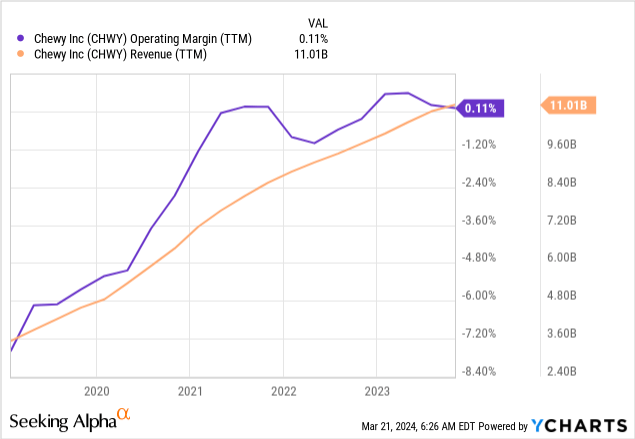

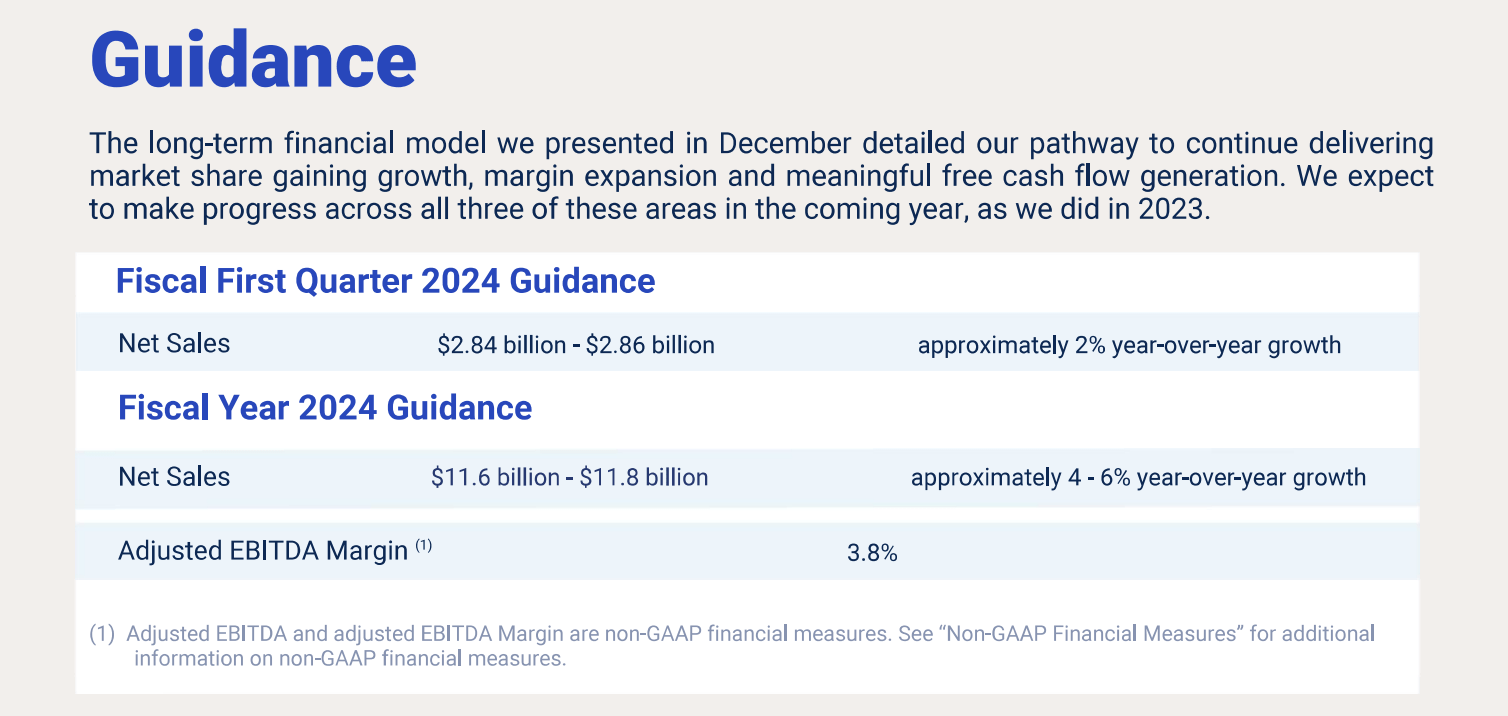

With that in mind, CHWY just released its 4Q23 earnings.

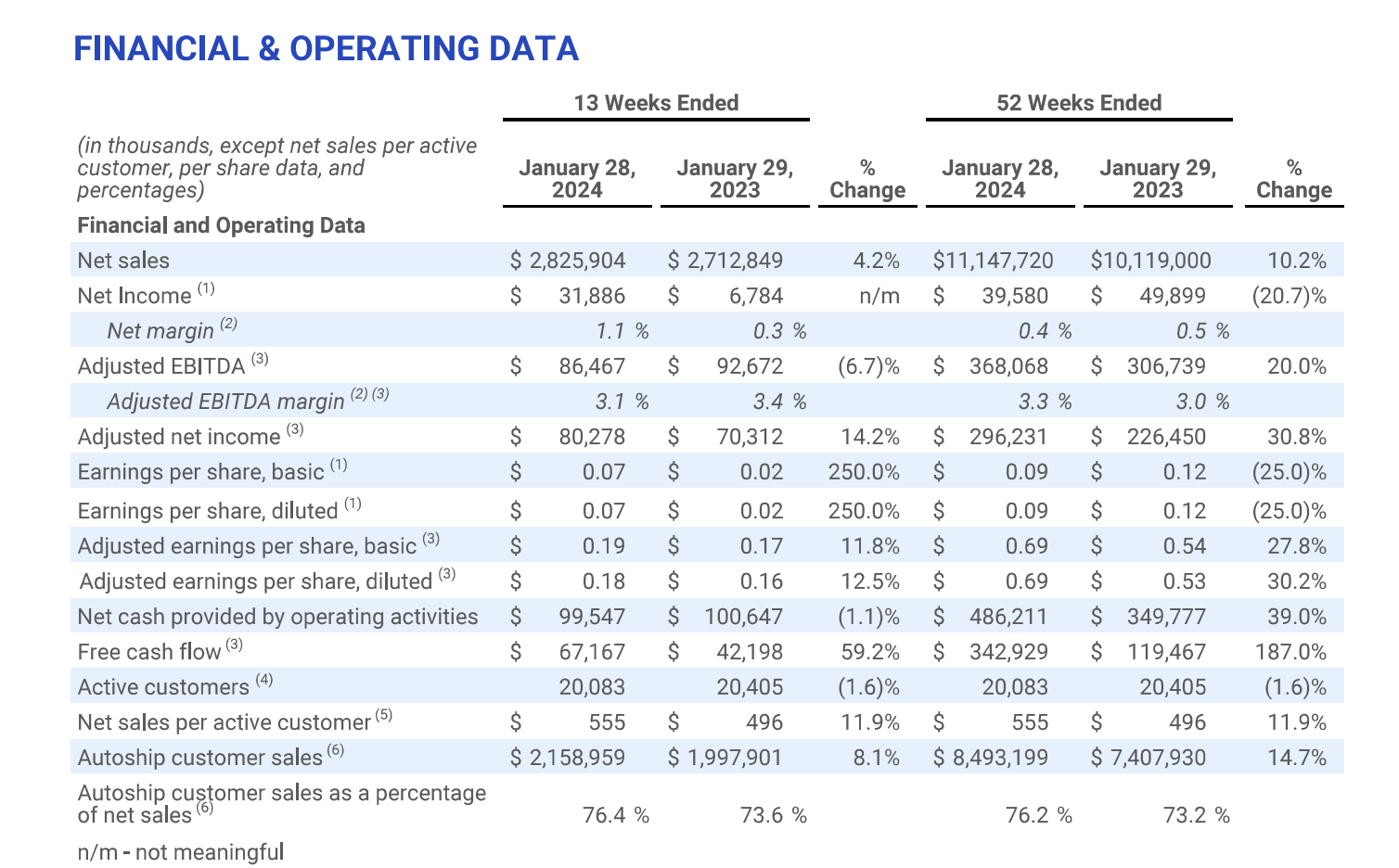

Chewy's fourth-quarter net sales increased by 4.2% to $2.83 billion. Full-year net sales reached $11.15 billion. This is above the company's guidance.

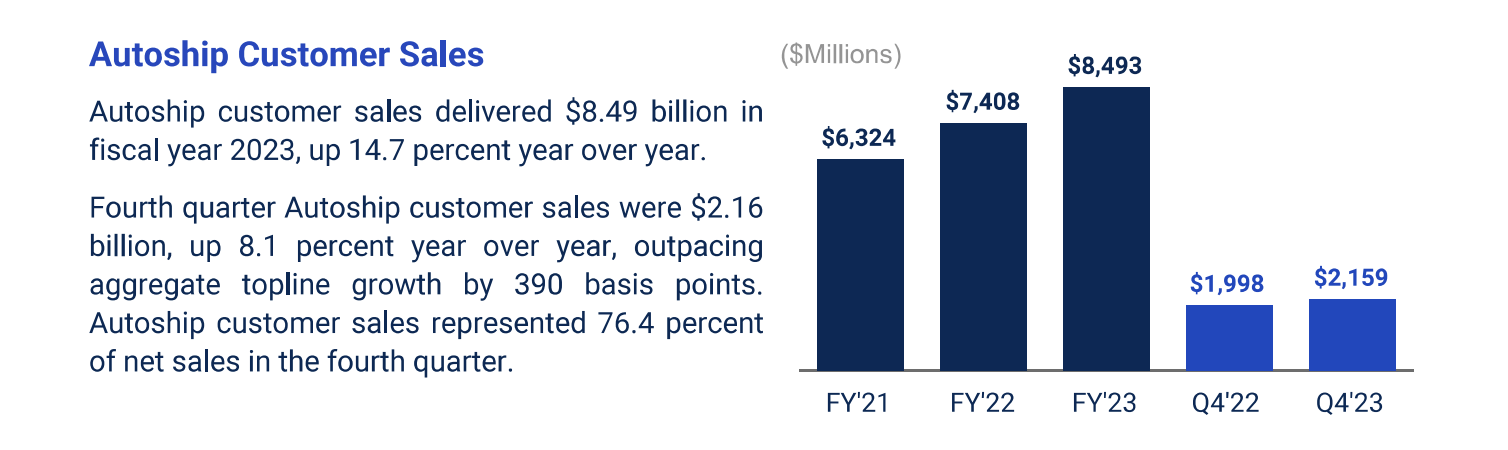

Moreover, Autoship customer sales accounted for 76.4% of total net sales in Q4 and 76.2% for the full year. Full-year Autoship sales were up 14.7%.

Chewy

The bad news is that the company saw another decline in active customers. Total active customers dropped by 1.6% to 20.1 million. The good news is that net sales per active customer ("NSPAC") reached a new all-time high of $555 in 4Q23. That's up 11.9% compared to the prior-year quarter.

Chewy

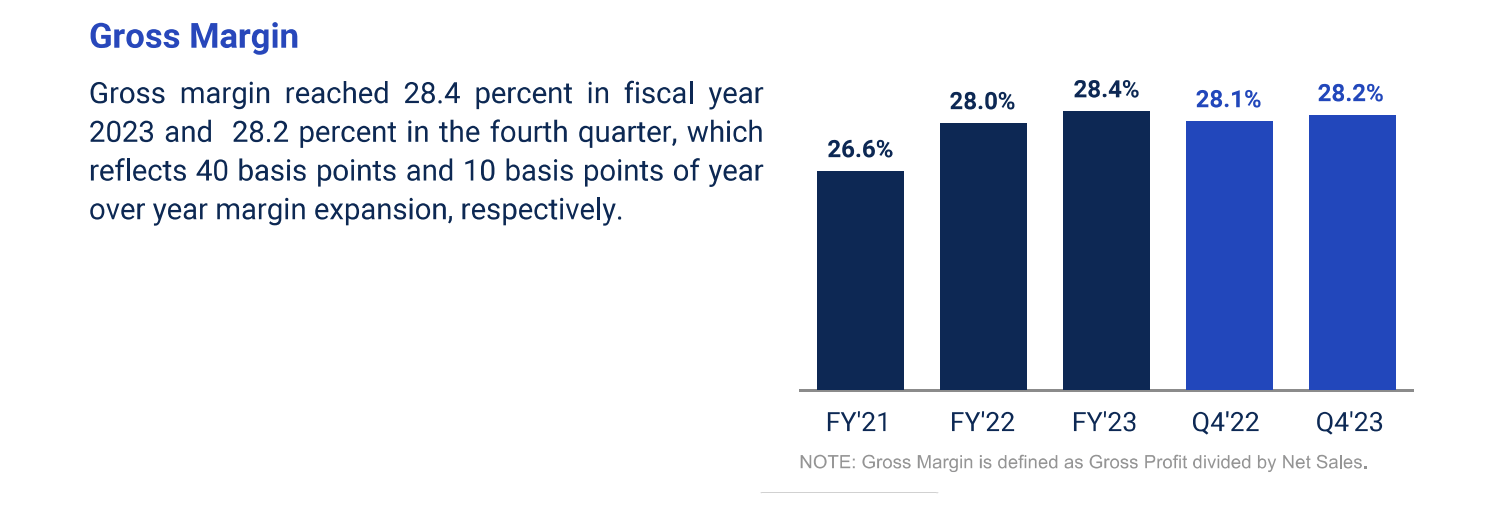

With regard to margins, gross margins for Q4 and FY2023 were 28.2% and 28.4%, respectively.

Sequentially, the gross margins in the fourth quarter decreased due to promotional activities. However, on a full-year basis, gross margins expanded by 40 basis points.

Chewy

The company also maintains a healthy balance sheet, as it ended the year with $1.1 billion in cash and cash equivalents.

This allows it to maintain a debt-free status and roughly $1.9 billion in liquidity.

The company spent 1.3% of its sales on capital expenditures, most of it aimed at fulfillment center automation and other technology projects.

With that said, going forward, Chewy expects elevated growth on a long-term basis. However, 2024 growth is expected to be below average due to factors that include lower unit growth and limited pricing benefits.

This is no surprise, given the challenging macroeconomic environment.

Despite these challenges, Chewy remains optimistic about its position within the industry and expects to continue gaining market share in 2024, driven by its strategic initiatives and the aforementioned competitive advantages.

To add some numbers, the company expects roughly 2% sales growth in 1Q24 and at least 4% growth on a full-year basis.

Chewy

Factors driving growth include NSPAC expansion, although active customer growth is expected to remain flat.

Moreover, free cash flow conversion is expected to remain above 80%, which is a great sign of quality.

So, what about its valuation?

Using the data in the chart below, analysts believe Chewy will be able to grow its earnings per share over time.

FAST Graphs

As the data above may be hard to read, I put the data into the table below:

| Year | EPS |

| 2024E | -$0.03 |

| 2025E | $0.13 |

| 2026E | $0.36 |

| 2027E | $0.80 (+122%) |

Note that I only added growth rates to the 2027 number, as the growth rates through 2026 are "off the charts" due to the expected transition to profitability.

The good news is that if management is able to return to profitability and maintain elevated growth, it could unlock tremendous value.

After all, using a 30x multiple for 2027 earnings gives us a fair stock price target of $24. That's 40% above the current price and a low multiple if the company were to maintain elevated double-digit annual EPS growth.

It could easily trade at 50x EPS, implying a 130% upside, if it were to maintain >20% annual growth rates.

In this case, it's hard to say what the stock might trade at, as valuations depend on various factors, including expected future growth, competition, the general market environment, and other risks.

If the company is able to maintain long-term double-digit EPS growth well beyond 2027, it would be fair to apply a multiple of at least 30-40x earnings.

Amazon, for example, traded at more than 100x earnings when it started to become profitable on a more consistent basis.

This is what makes companies in the early stages of an aggressive expansion so tricky. It's hard to put a price target on it, which allows some investors to come up with outrageous estimates, while others use elevated short-term multiples to make the case that a company is a clear short candidate.

Another problem is uncertainty.

There's a reason why CHWY got "whacked" on the stock market. There's little confidence to bet on a company that needs to grow its customer base in an environment of elevated inflation.

Given the stock price decline and my belief that the risk/reward is good, I will give the stock a Strong Buy rating.

However, I need to add a few things:

Personally, I have not yet initiated a position in the company, as I'm in the process of figuring out which long-term investments I will be buying. As I mentioned in prior articles, I had to pay more taxes than expected and aggressively bought energy stocks earlier this year.

However, the odds are I will start a small position in CHWY in my trading account in the weeks ahead.

Chewy presents a compelling investment opportunity despite its recent challenges.

While the stock has faced downward pressure, its strong fundamentals and strategic initiatives suggest significant upside potential.

With a solid track record of revenue growth, expanding market share, and a loyal customer base, Chewy remains well-positioned to capitalize on the growing pet industry.

Pros:

Cons: