John M. Chase/iStock Unreleased via Getty Images

John M. Chase/iStock Unreleased via Getty Images

The electric vehicle ("EV") charging station segment continues hitting speed bumps, with the sector now facing vehicle demand issues. ChargePoint Holdings, Inc. (NYSE:CHPT) was a prime example of a company lacking the business model to handle problems faced along the supposed path to profitability. My investment thesis remains Neutral on the stock with ChargePoint now trading below $2, though the risk remains more to the downside than any major rally.

Source: Finviz

ChargePoint has seen sales collapse over the last year, with the company reporting the following FQ4 '24 numbers:

Source: Seeking Alpha

Not only did ChargePoint report a revenue decline of 24%, but also the company missed analyst estimates by over $4 million. While the bad news is that revenues slumped, the EV charging station company did generate sales growth in the key Subscription business.

The issue with the business was always the mismatch of the operating expense base with the limited gross profits from Network equipment where the majority of sales were focused. At the same time, the stock valuation soared based on sales growth of products, though these sales provided limited financial value to the company.

ChargePoint still managed to report a $52 million net loss for the quarter, along with an adjusted EBITDA loss of $45 million. The EBITDA loss actually grew from the $42 million loss last FQ4 in a sign of how cutting out low margin product sales haven't really helped the company improve their financial picture.

The EV charging station company only produced a gross margin of 22% with a gross profit of $25 million. In essence, ChargePoint has to reduce the operating expense base to this level in order to be breakeven, or the company must hike margins and sales dramatically to boost gross profits.

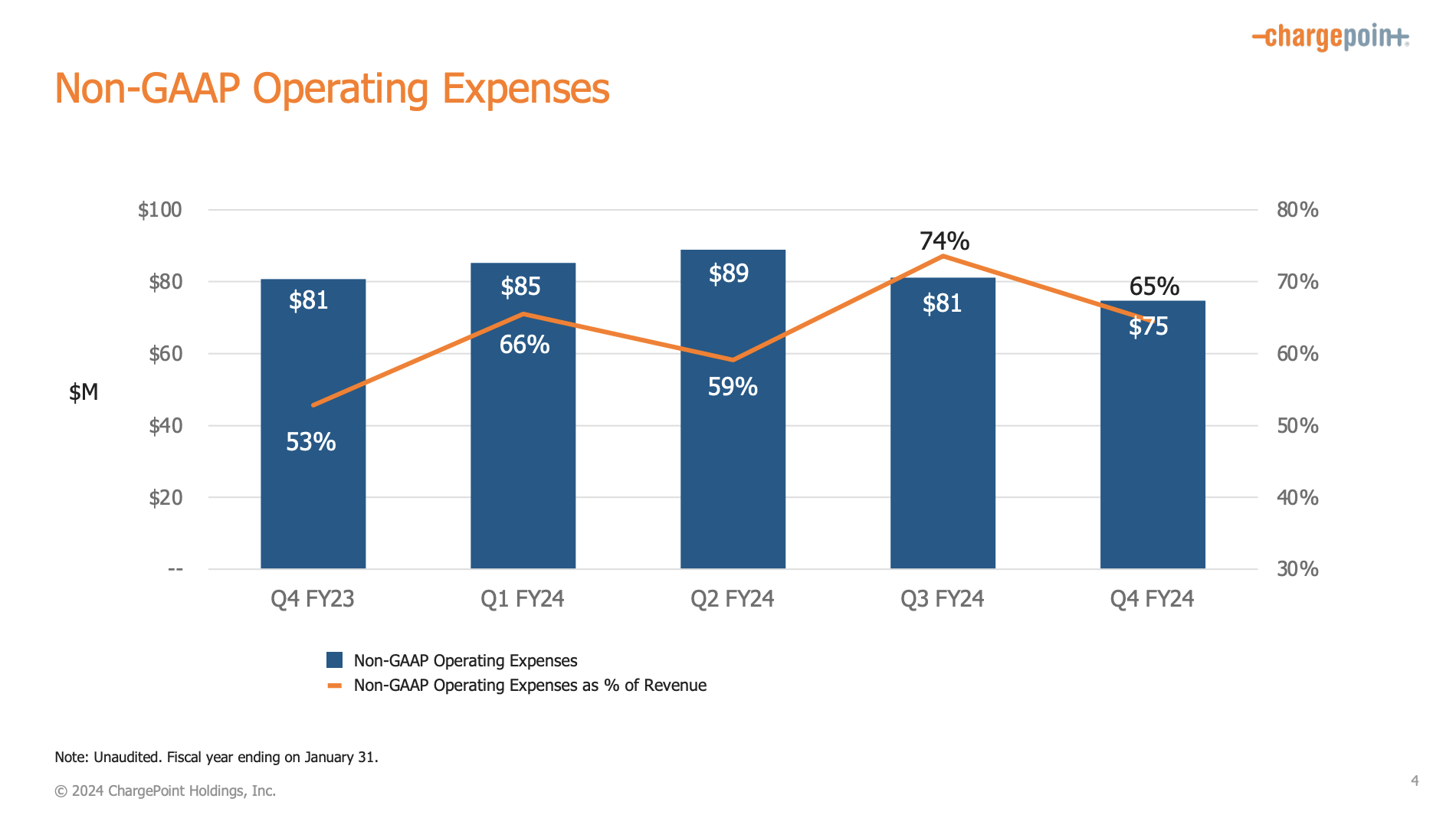

The company has cut operating expenses from the $89 million peak back in FQ2, but ChargePoint is still spending a whopping $75 million on opex. Management projects being adjusted EBITDA profitable by year-end FY25, but the gap is currently massive with gross profits needing to triple from current levels even with quarterly opex forecast to dip below $70 million based on the latest job cuts.

Source: ChargePoint FQ4'24 presentation

As mentioned above, the one good news tidbit from the January quarterly report was the Subscription business still growing 30% to reach $34 million. The segment even produced the majority of the FQ4'24 gross profits at $14 million.

The big question is how much ChargePoint can drive Subscription growth going forward without selling more Networked equipment used to drive recurring revenues. The Subscription business still only has annual revenues base of $134 million.

ChargePoint guided to FQ1'25 revenues of only $100 to $110 million, down sequentially from the FQ4 level of $116 million. The dip is due to normal seasonality, but the EV charging station business doesn't have the margin of safety to handle the dip.

The company ended the quarter with a cash balance of $358 million and with debt of $284 million. ChargePoint hardly has a net cash position now after burning nearly $42 million of cash from operations during the last quarter and $329 million from operations for all of FY24.

Management made a lot of promises regarding improved margins from the manufacturing deal with AcBel and Kinpo, but ChargePoint didn't provide any solid metrics to support how the business improves enough to eliminate these massive losses. The deal was just announced a few weeks ago, and these types of deals can take a year or so to be fully implemented and beneficial to operations.

The consensus estimates only forecast FY25 revenues of $562 million, yet the guidance for FQ1 is already below analyst estimates. Even with ChargePoint producing $50 million in additional quarterly revenues, 20% gross margins only add $10 million in gross profit while the company would need $150 million in quarterly revenues and 30% gross margins (8 percentage points above FQ4) in order to produce just $45 million in gross profits.

ChargePoint already has a huge hurdle to overcome and most companies struggle to reinvigorate growth after cutting so many expenses from operations. The company estimates nearly $70 million has now been cut from the non-GAAP operating expense base and the reduction in R&D and sales/marketing typically lead to unintended impacts on future sales.

The market cap is down to ~$800 million and will likely trend lower until the ongoing losses are eliminated. ChargePoint just doesn't warrant much upside because getting to adjusted EBITDA profitable during the peak quarter isn't the same as the company being profitable, considering interest expenses and depreciation charges are legitimate cost hurdles.

The key investor takeaway is that ChargePoint Holdings, Inc. stock has no margin of safety and the EV charging station business is now struggling. The company must grow sales and boost margins dramatically to just eliminate ongoing losses and cash burn. The stock still doesn't offer any upside for shareholders until the company shifts the business beyond just getting to adjusted EBITDA profitable, yet that is already a big speed bump.