Andrii Yalanskyi

Andrii Yalanskyi

Cherry Hill Mortgage Investment Corporation (CHMI) is an mREIT that earns income through the investment of mortgages. Like its peers, the company utilizes leverage (borrowing) to invest in and earn income from its assets. Since I last wrote about Cherry Hill two years ago, the restrictive rate regime put into place by the Federal Reserve has created a challenging environment for the company, but I believe that income investors can earn a great return with an investment in Cherry Hill’s B series preferred shares (NYSE:CHMI.PR.B).

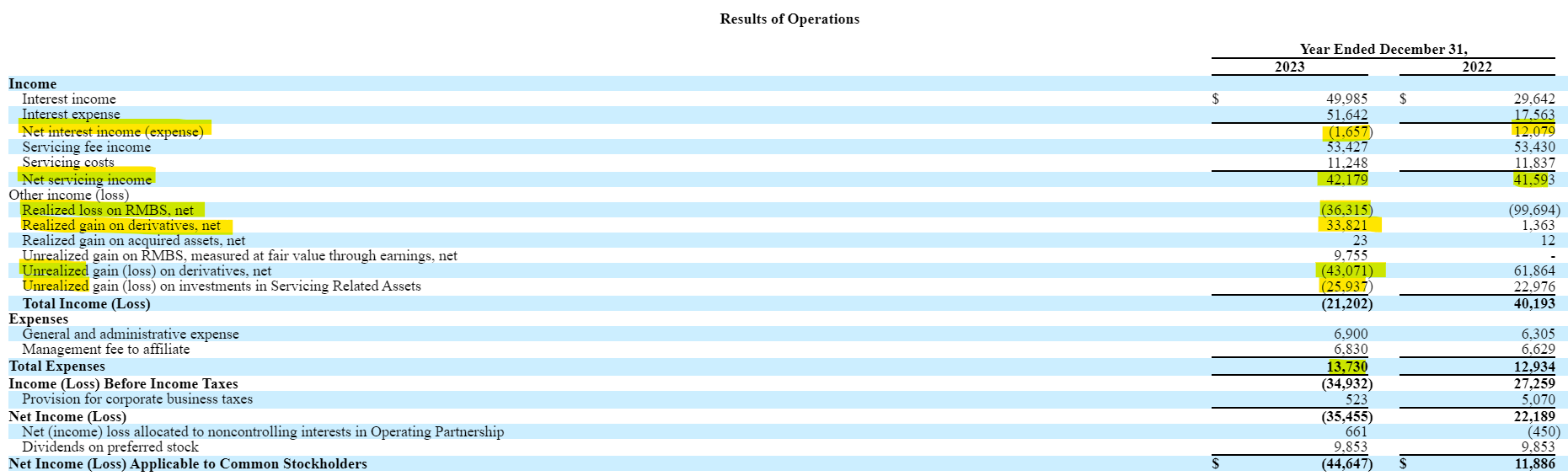

Cherry Hill’s income statement shows the extent to which the company is struggling with the high interest rate environment. Interest income has increased from $30 million to nearly $50 million, but interest expenses have exploded from $17.5 million to over $51.5 million. As a result, the net interest income swung from a profit of $12 million to a loss of nearly $2 million. Cherry Hill also books gains and losses based on changes in the value of its investments, whether they are sold (realized) or held (unrealized). Losses on the value of the company’s investments also dragged earnings down during 2023.

SEC 10-K

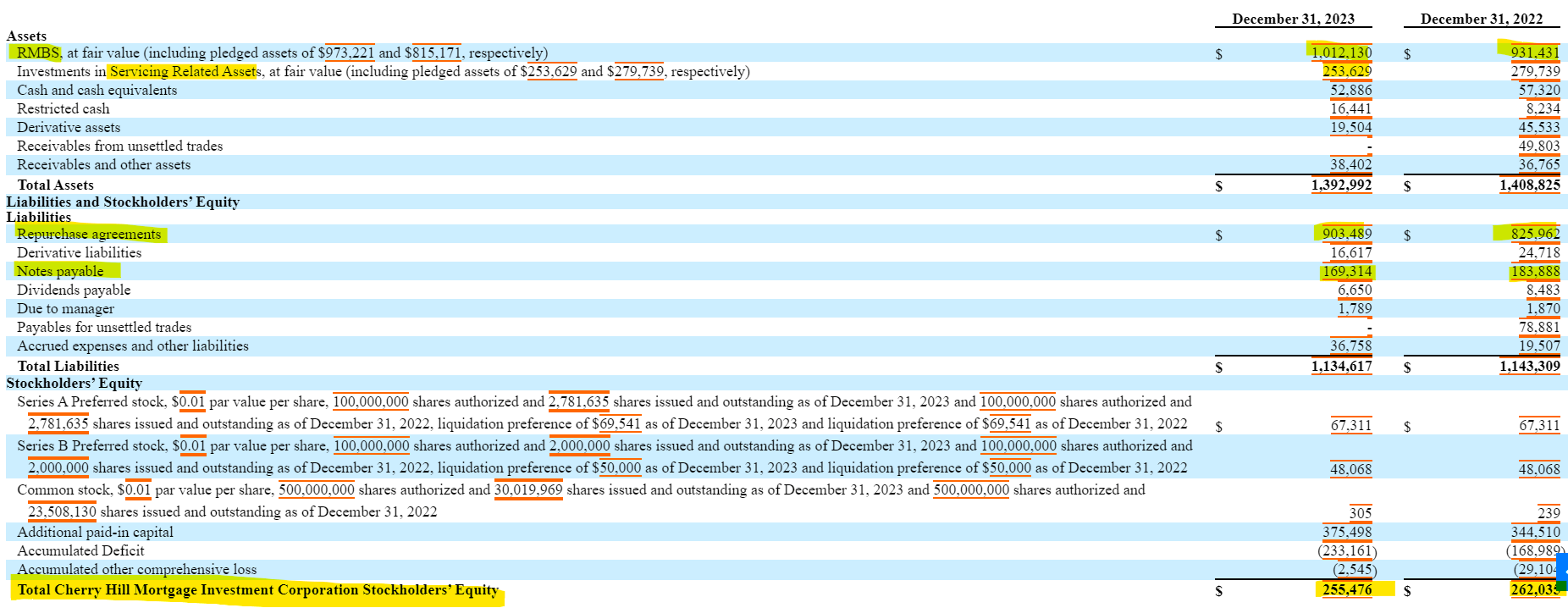

Cherry Hill Mortgage’s balance sheet describes the nature of the company’s investments and its use of leverage. Cherry Hill invests primarily in residential mortgage-backed securities (RMBs), but also services residential mortgages. During 2023, Cherry Hill increased its investment in RMBS and decreased its servicing assets.

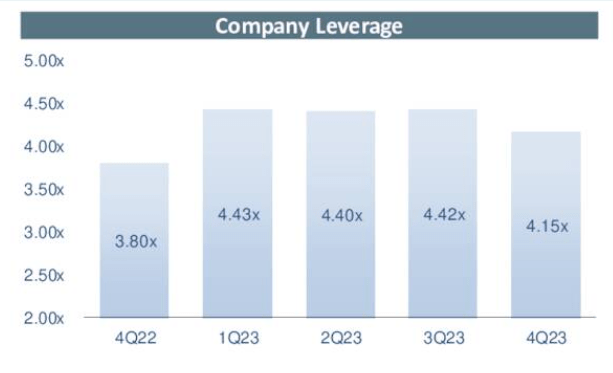

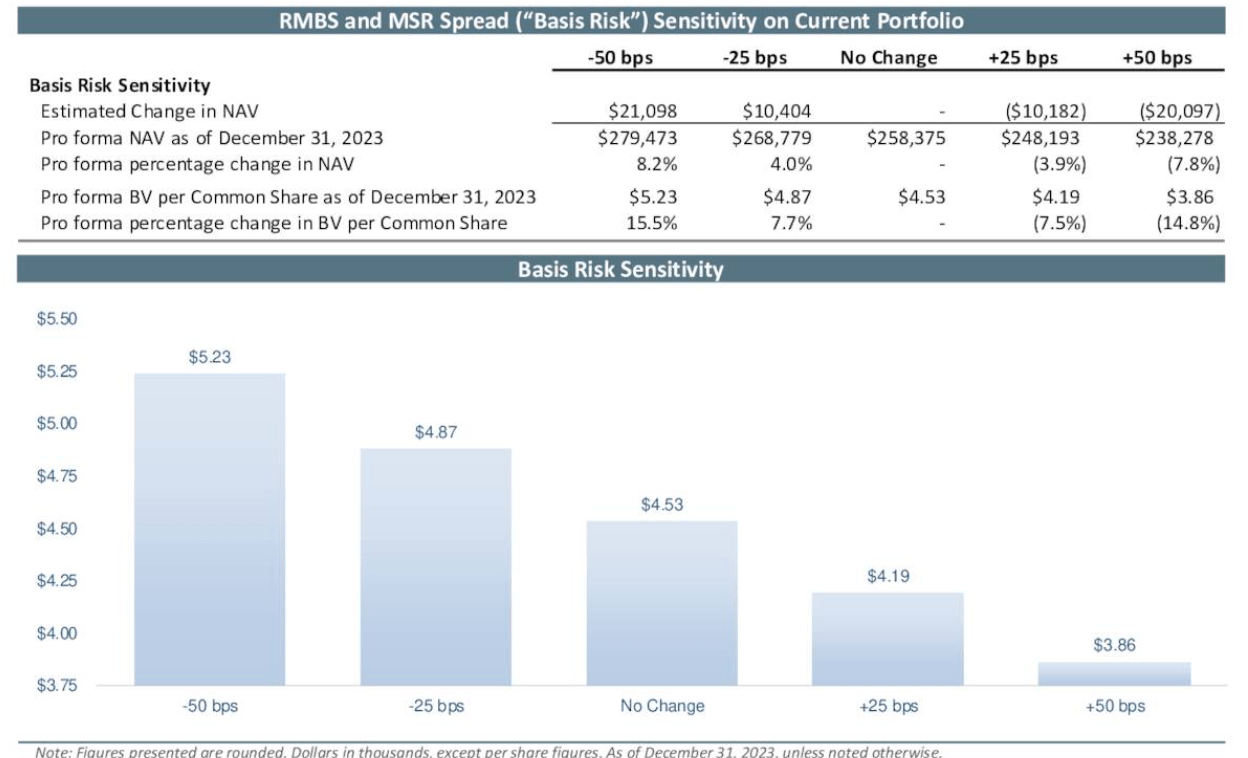

Additionally, the company shifted away slightly from long-term debt and increased its borrowing of repurchase agreements, which is a form of short-term financing. Overall, shareholder equity dropped slightly to $255 million in 2023. The company increased its leverage ratio at the beginning of 2023 and reduced it slightly by the end of the year.

SEC 10-K

Earnings Presentation

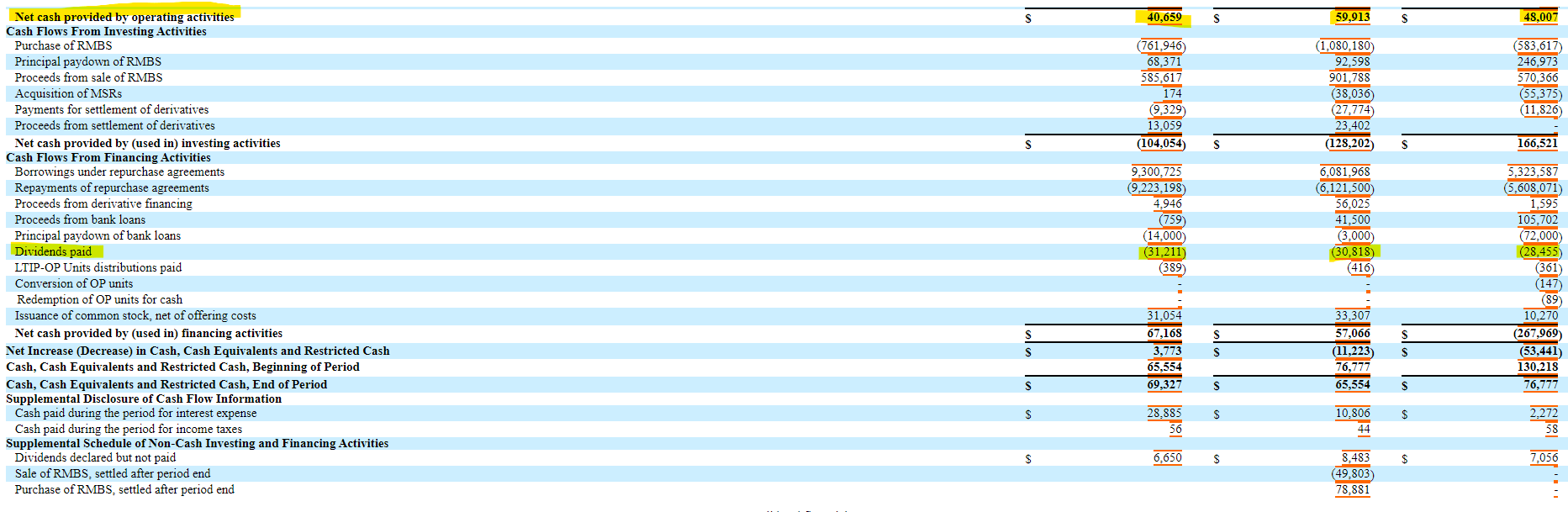

Typically, I like to examine the statement of cash flows when determining dividend sustainability. In the case of Cherry Hill, the company’s operating cash flow has been decreasing, but has been sufficient to cover the company’s dividends. One challenge in this analysis is that Cherry Hill and other mREITs utilize cash flow from investing activities in order to grow their balance sheets, hence making investing activities a part of day to day operations.

SEC 10-K

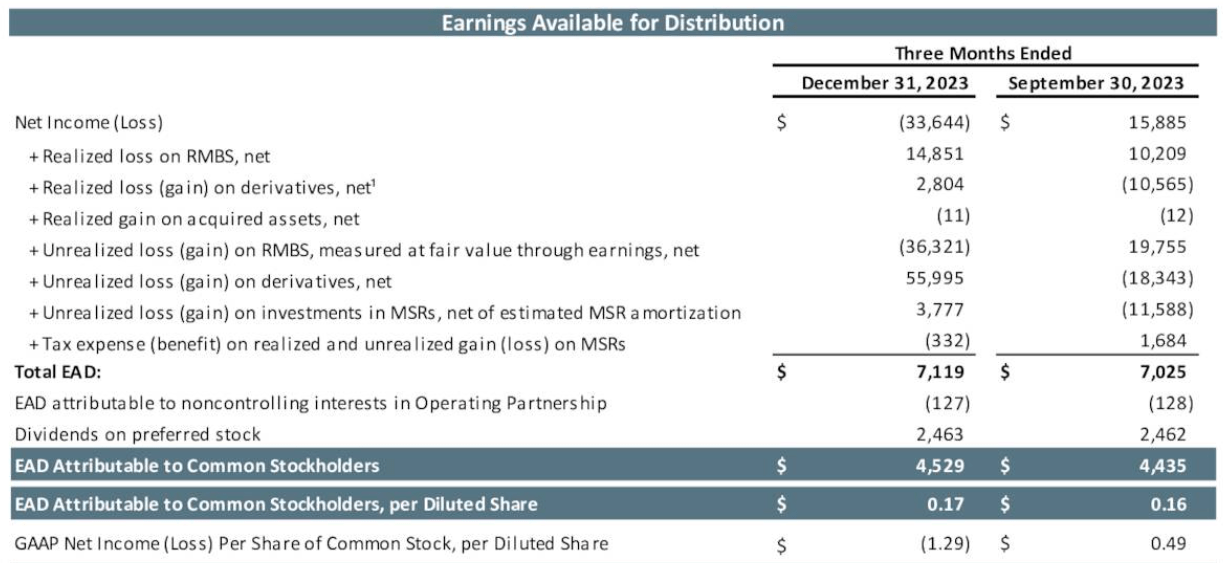

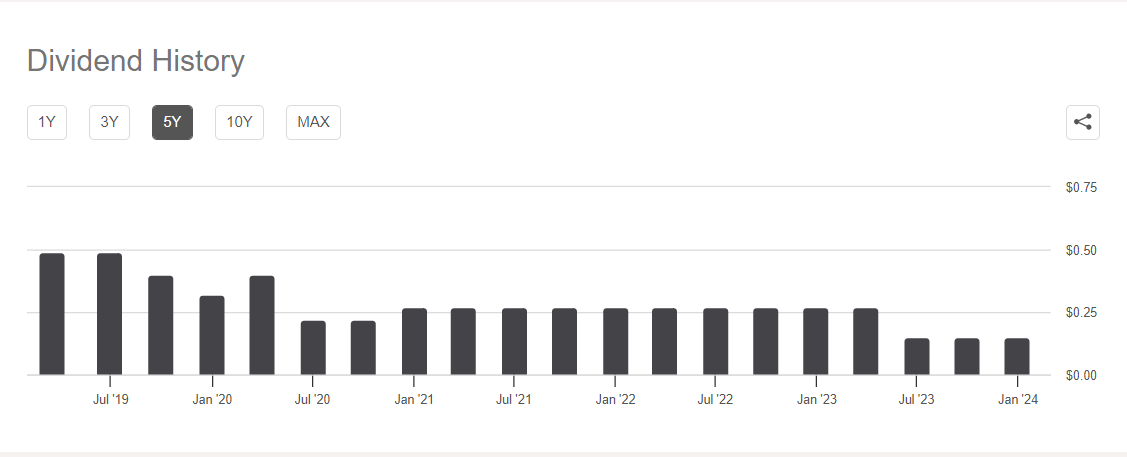

A better measure of dividend sustainability comes from earnings available for distribution, which is provided quarterly within the company’s earnings presentation. Earnings available for distribution have been stable for the last two quarters and is approximately three times higher than the preferred dividend obligations. The EAD is not sufficient to cover the common share dividends, and that may explain the drop in dividends from 49 cents per share to 15 cents per share in the last five years.

Earnings Presentation

Seeking Alpha

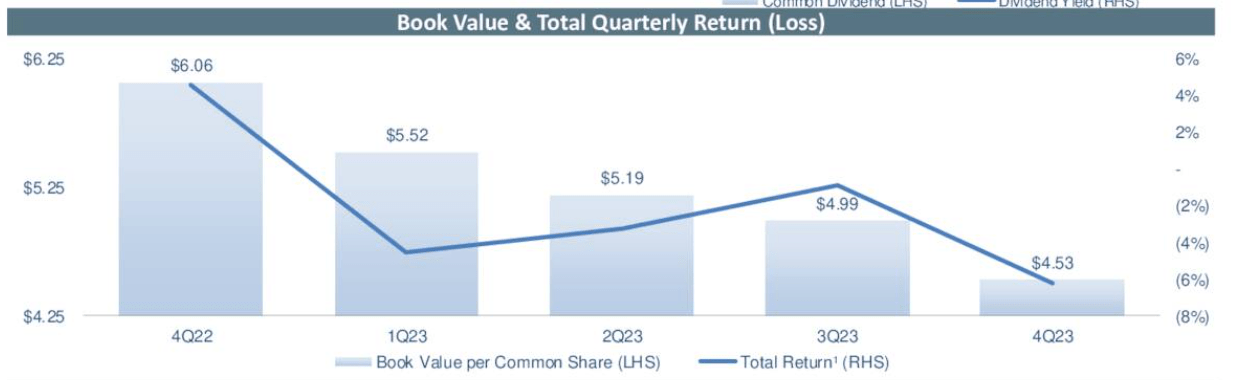

The unreliable dividend is one of two reasons why I’m not interested in investing in the company’s common shares. The other reason is book value per share. Due to the high interest rate environment, Cherry Hill’s book value per share has dropped from $6.06 per share to $4.53 per share in just one year. It is important to note that the company believes lower rates will boost book value per share, but I see the preferred shares as a better preservation of capital with solid income opportunity than the common shares.

Earnings Presentation

Earnings Presentation

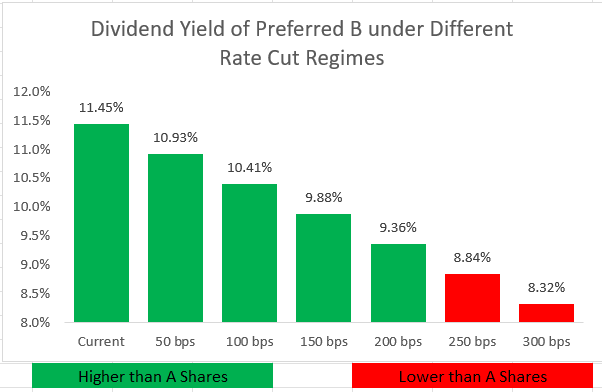

In terms of the preferred shares, Cherry Hill Mortgage Investment offers two series. Their A series (NYSE:CHMI.PR.A) is an 8.2% fixed rate dividend that is currently yielding 8.96%. The Series B is a fixed to floating preferred share that is currently yielding 8.6%, but the dividend is set to float next month to the three-month LIBOR rate plus 5.631%. Based on today’s rates and the projected rates if the Federal Reserve cuts, I believe that the B shares will pay a higher dividend as long as the Fed funds rate is cut no less than 250 basis points.

Market Data & Analyst Calculations

Based on Cherry Hill’s financial performance, combined with the current state of monetary policy, I believe that investors are best served by owning the company’s B series preferred shares. Cherry Hill continues to be capable to cover its preferred dividends with its EAD and the B series shares begin floating next month, offering an immediate dividend yield of 11.45% and will remain higher than the current income on A shares until the Fed funds rate reaches approximately half of its current level. Even if it takes years for the Fed to lower rates to those levels, the cumulative income premium collected over the A shares will continue to justify the investment.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.