Bloomberg/Bloomberg via Getty Images

Bloomberg/Bloomberg via Getty Images

One of the downsides to investing in technology related firms is that conditions can change rather quickly. Companies that were once thought to have a fantastic moat and that investors could count on for growth in perpetuity, can start seeing weakness and decline in price rather quickly. A great example that I could point to in this regard is online education company Chegg (NYSE:CHGG). Back in August of 2022, I found myself taking a bullish stance on the firm. I wasn't completely sold on it, but I did say that it was a ‘decent’ play on promoting academic achievement. Growth leading up to 2022 had been robust, though there was some weakness developing throughout that year. Long term, I felt as though the business offered upside, even though shares were not as cheap as I normally would have liked.

At the end of the day, I ended up rating the business a ‘buy’. But since then, it has been one of the worst performers of those that I have given that rating to. While the S&P 500 is up 15.7% since then, shares of Chegg have seen downside of 57.3%. It's worth noting that the most recent leg down that the business experienced came on February 6 as shares fell more than 6%. The day prior, management reported financial results for the final quarter of the 2023 fiscal year. Even though the company exceeded expectations when it came to revenue, profits fell short of expectations and management gave a rather disappointing outlook for the first quarter of the 2024 fiscal year. The decline in fundamental performance has not been enough to make the company look unattractive from a valuation perspective. In fact, shares are incredibly cheap right now. But with performance likely to worsen from here and tremendous uncertainty regarding the space because of technological changes like AI, investors would be wise to tread very cautiously.

Author - SEC EDGAR Data

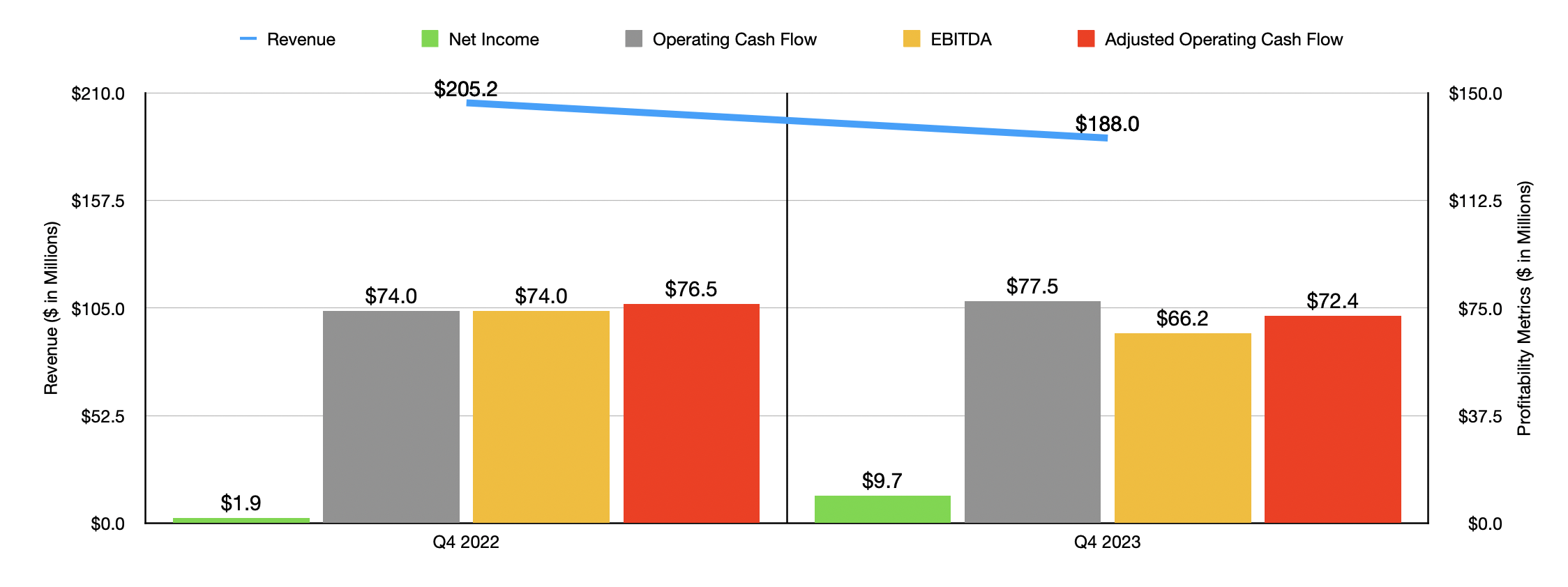

As I mentioned already, on February 5, the management team at Chegg announced financial results covering the final quarter of the 2023 fiscal year. During that time, revenue came in at $188 million. That is 8.4% lower than the $205.2 million generated one year earlier. This drop was driven entirely by a plunge in subscription services revenue from $177.5 million to $166.3 million. This, management said, was the result of a drop in subscribers from 5 million to 4.6 million. These days, management has been fairly quiet about the cause of subscriber declines. But last year, the firm acknowledged that the rise of ChatGPT and other AI chat bots was having a negative impact on its user base. These are often free compared to the services that Chegg offers. The only good news on this front was that revenue exceeded analysts’ forecasts by about $5.7 million.

Author - SEC EDGAR Data

Even though revenue declined during this time, profits went from $0.01 per share to $0.09 per share. Unfortunately, this didn't change the fact that earnings per share missed forecasts by $0.06. But on an adjusted basis, profits did manage to exceed forecasts to the tune of $0.01. The overall rise in profits per share year over year translated to an increase in net income from $1.9 million to $9.7 million. Interestingly, one other profitability metric also improved. Operating cash flow rose from $74 million to $77.5 million. But on an adjusted basis, it ticked down modestly from $76.5 million to $72.4 million. Meanwhile, EBITDA dropped from $74 million to $66.2 million.

Author - SEC EDGAR Data

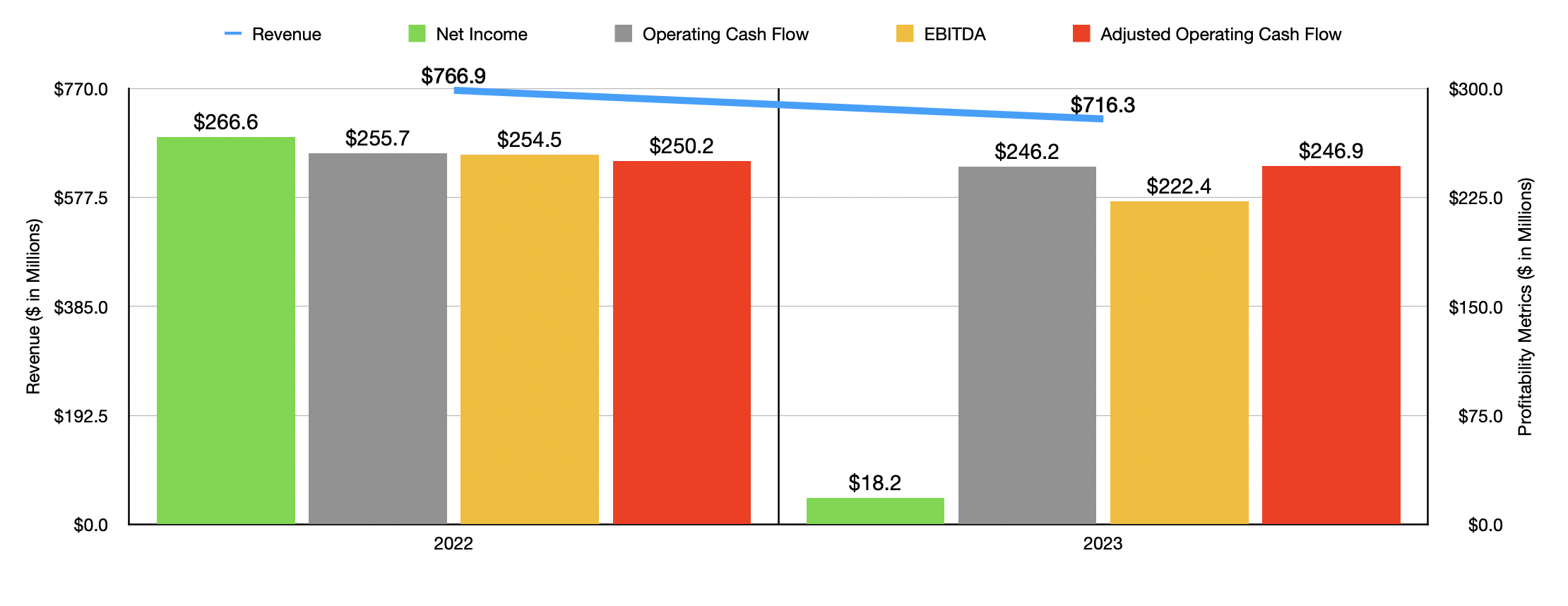

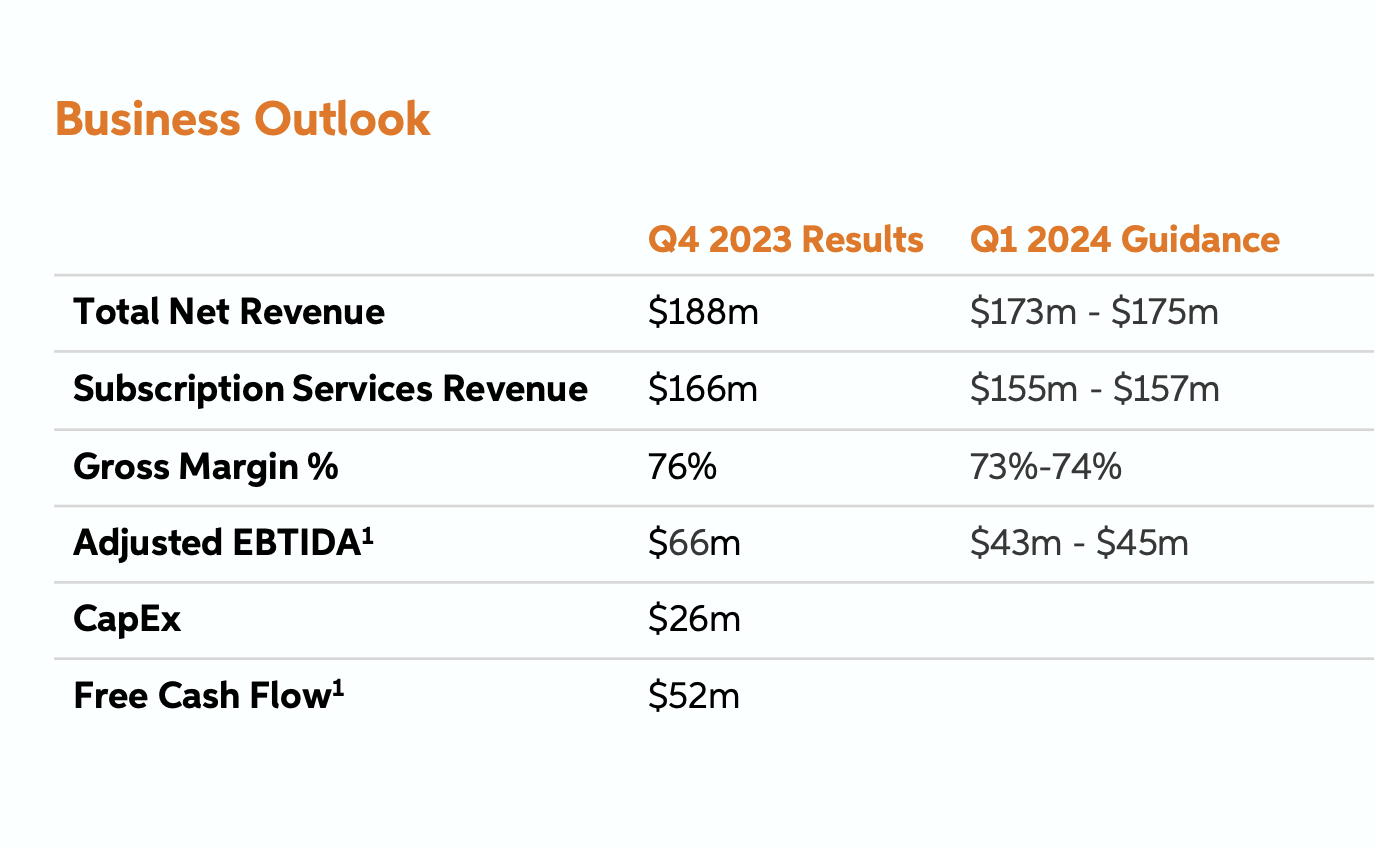

To get an understanding of whether or not this was just one bad quarter, or if it is part of a larger trend, I would like to point you to the chart above. In it, you can see results for 2023 as a whole relative to 2022. In this case, net profits, operating cash flow, adjusted operating cash flow, and EBITDA all worsened year over year. And to make matters worse, management is not terribly optimistic about the near term. In their press release, they said that revenue for the first quarter of the year should be between $173 million and $175 million.

Chegg

Analysts had been forecasting $186 million. And in the first quarter of the 2023 fiscal year, the company generated sales of $187.6 million. Management is now saying that net profits should be negative to the tune of $6.1 million for the quarter. Using guidance set by analysts, the expectation was $8.3 million compared to the $2.2 million in profits generated in the first quarter of 2023. Similar weakness is expected when it comes to EBITDA as well. During the first quarter of 2023, Chegg generated EBITDA of $57.6 million. But for the first quarter of 2024, the company is forecasting a reading of between $43 million and $45 million.

Author - SEC EDGAR Data

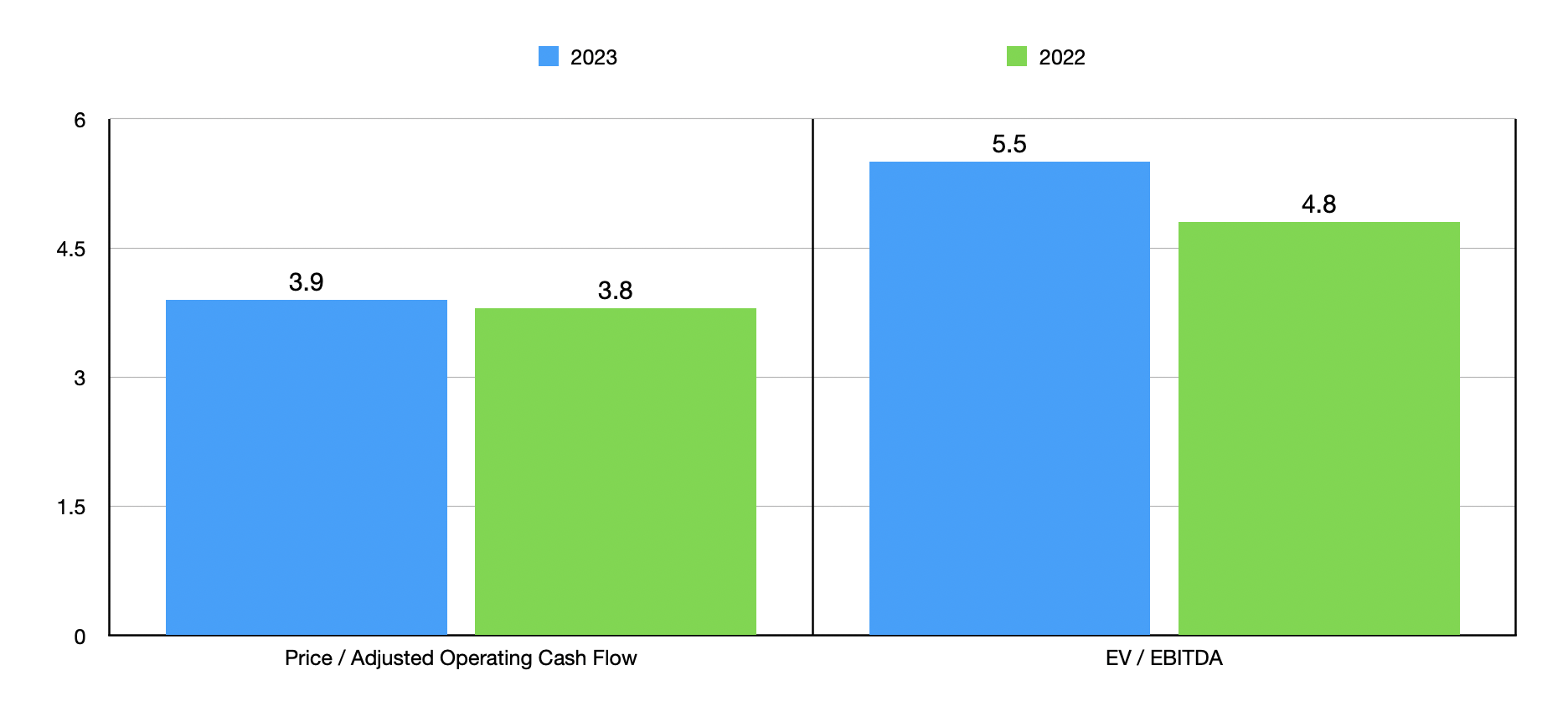

If we take the data from 2022 and 2023, we can easily value the company as shown in the chart above. It's always great to see a company trade in the low to mid single digit range. But that's so cheap that often you risk buying a value trap. The fact of the matter is that we are likely looking at a more painful 2024 than what we saw in 2023. So there is a real risk of catching a falling knife. On the other hand, for those who are optimistic about the company and its prospects, I can understand why.

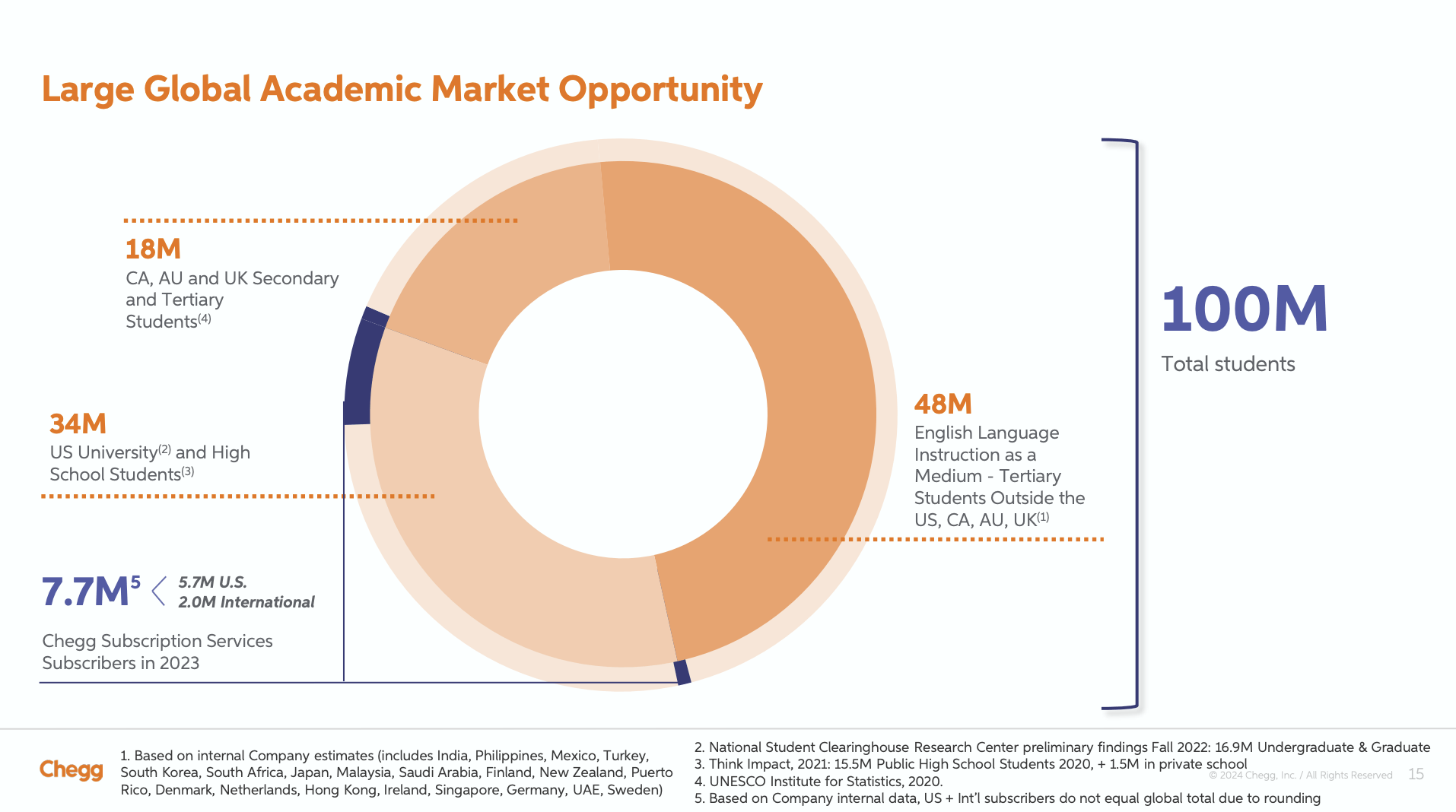

For starters, the education space is not insignificant. Management believes that the large global academic market opportunity facing it comes in at around 100 million students. This includes 48 million English language instruction as a medium spread across countries other than the US, Canada, Australia, and the UK. 34 million would involve US university and high school students. And the other 18 million would involve Canadian, Australian, and British secondary and tertiary students. Management also has data to support the view that its offerings are relevant. According to their own internal results, which should be taken with a grain of salt, 91% of its users say that they get better grades using the company's services than when they don't.

Chegg

The other reason why some investors might be optimistic involves the same reason that shares have tanked over the past year or so. This involves the use of AI. Management has said that the 2024 fiscal year will be one in which the company invests more into AI. In fact, the firm claims to not only be making use of its own personal learning assistant, it is doing so using its own LLMs (large language models). This allows the company to take a more custom approach and to rely less on other parties in order to achieve its goals. However, this is a very competitive space and some of the companies in it have billions upon billions of dollars to throw at the matter. I would argue that using AI in innovative ways would be more valuable than developing it.

I predict that, if we could travel into the future five to ten years, Chegg will either have turned out to be a fantastic investment, or it will go down tremendously from where it currently is. The good news is that cash flows are still significantly positive and shares are trading at very low levels. But the bad news is that there is a tremendous amount of upheaval in the space at the moment because of the rise of things like AI. Because I am a value investor, I rarely find myself drawn to winner-take-all outcomes or outcomes where only a few big winners end up coming out on top. And this is no exception. While the company could experience meteoric upside if things go right, there is not enough data to satisfy me that suggests this to be the case. So until we have further details, I'm downgrading the stock to a ‘hold’.