FreshSplash/E+ via Getty Images

FreshSplash/E+ via Getty Images

As an investor that values dividend income and growth, I am frequently on the lookout for companies that can provide a reliable, predictable, and growing stream of dividend income. There are only 55 companies that have earned the title of Dividend Kings. Dividend Kings are companies that have managed to increase their dividends for at least 50 consecutive years. The Kimberly-Clark Corporation (NYSE:KMB) has reached this dividend milestone and currently sits at an attractive valuation. The dividend sits slightly over 4% and was recently raised.

However, I do not think the dividend reputation alone is enough to convince me to start a position here. The outlook for the next year is quite poor, and the growth is projected to be lackluster. In addition, it seems like the strategy to offset lower sales volume is to simply increase prices. While this is a nice band-aid solution, I don't think it's sustainable.

Kimberly-Clark manufactures and sells personal care products in the U.S. It operates through three segments: Personal Care, Consumer Tissue, and KC Professional. The Personal Care segment includes brands like Huggies and Kotex which are known for their portfolio of baby products and feminine care products. The Consumer Tissue segment provides things like napkins, paper towels, toilet paper, and more. Lastly, the KC Professional segment offers products like cleaning wipes, sanitizers, and other sanitary products.

During the pandemic era, we saw a wide range in the price movement, with prices reaching over $150/share and briefly falling below $110/share in late 2022. So the question arises, is now a good time to enter since the price has fallen back to the $120/share level? There's a bit of a mixed picture here between the subpar future outlook and current financials, so let's dig in.

KMB recently reported their Q4 earnings in January 2024 and that closed out their 2023 fiscal year. KMB reported slow growth for the period and also missed expectations. They pulled in net sales of $5.0B for the year, as well as an organic sales growth of 3% for the year. Net sales were in line with the prior year, but fortunately, sales growth did manage to rise because of price increases. The negative here is that price increases were the only reason that sales growth happened, since management confirmed that product sale volume was in line with the prior year.

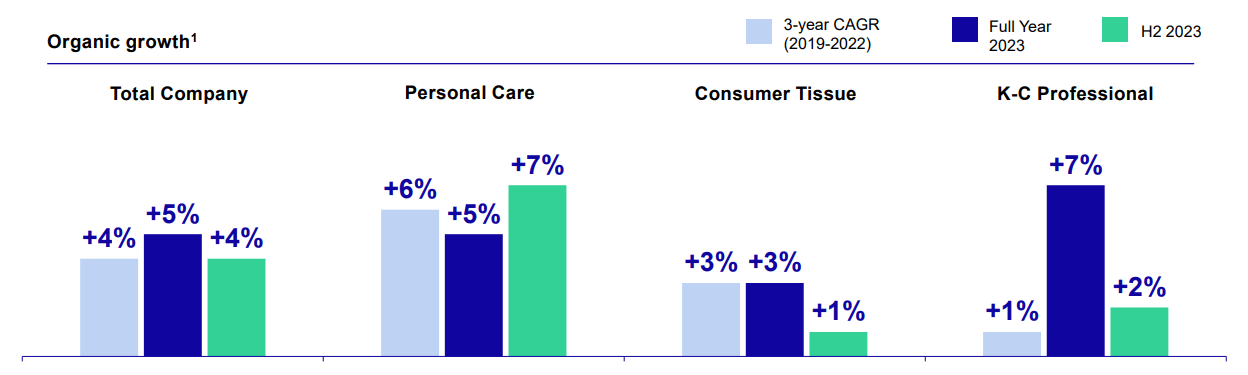

Q4 2023 Presentation

For the chart above, I will focus exclusively on the 3-year CAGR, as they give us a more accurate picture of what kind of growth average we can expect going forward. As a whole, the company grew at a CAGR of 4% over the last 3 years, while personal care was the strongest segment with 6% growth and K-C Professional was the weakest segment with a 1% CAGR. Consumer Tissue falls right in the middle at 3%. The problem I see here is that the current growth trajectory seems limited if the only way KMB can bring in increased revenue is by increasing prices.

You can only increase prices so much before consumers shift where they spend their dollars. The strategy of increasing prices to cover up slower sales volume is flawed because it eventually results in a competitor filling the gap with a cheaper alternative. If you were to ask me the difference between KMB's Scott branded toilet paper or Costco's (COST) Kirkland brand tissue, I wouldn't be able to tell you the difference. All I know is, the quality is about the same and the cheaper store brand option is usually cheaper, so that's what I'd choose. I don't think I'm alone with these thoughts, either!

Management's outlook for 2024 suggests a moderate increase in organic net sales going forward. We are likely to see a slow growth in the range of low to mid-single digits, it seems. Let me get it out of the way now and say that I think if you are after total return, there are better options out there if you'd like more growth.

This growth projection relies on continued price increases. As just mentioned, this is a flawed strategy in my opinion. During the last earnings call, management stated that the price increases are estimated to be 200 basis points in order to boost revenue from regions experiencing hyperinflation. However, we've seen inflation cool, so my thoughts are that this will simply make some consumers shift where they spend their dollars.

On the top-line, we are expecting low-to-mid single digit organic net sales growth, a range of organic growth that we expect will include approximately 200 basis points from pricing in hyperinflationary economies. At the same time, reported net sales growth is likely to be negatively impacted by roughly 300 basis points from currency translation and another 60 basis points from divestitures. - Nelson Urdaneta, Chief Financial Officer

It seems like a lot of the negative sentiment is being placed on currency translation effects. Operating profit is forecasted to show better growth in the high single digit to low double-digit range, but it was also mentioned that growth here is likely to be hampered by currency translation effects.

The only good thing I recognize is the estimated EPS (earnings per share) growth in the high single digits. However, I stay pessimistic here as I struggle to see how this kind of growth is expected when sales volume is slowing, and we remain in a higher interest rate environment. In addition, I believe a lot of customers will opt for 'store brands' instead of KMB's due to these price increases.

When it comes to groceries, data tells us that 54% of shoppers say they'll choose the store brand over national name brands. Even though KMB isn't within the grocery segment per se, I do believe that this shift will bleed over into the household products industry as well. As the general cost of living continues to rise, I do believe it's very likely that 'store brands' will continue to gain market share in all consumer categories.

The main concern here for me is under performance. I initially started my research really wanting to like Kimberly-Clark, but I don't think their product mix is special enough to retain a loyal customer base. As previously mentioned, the data tells us that shoppers are willingly moving towards the store branded items that are popular in places like Kroger's (KR) or Costco (COST). I think until management finds a way to regain the sales volume without the need to offset the decrease with higher pricing, I shall remain on the sidelines for now.

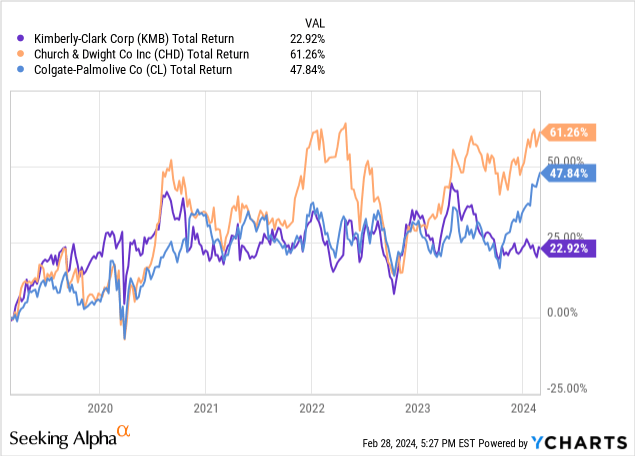

We can see that KMB really underperforms when compared against peers such as Church & Dwight Co. (CHD) or Colgate (CL). I believe this trend will continue as their product mix aren't generally considered "specialty" items where people have a hard time using an alternative. I think it comes down to perception.

Generally speaking, I think a lot of people are more inclined to use different brands of paper towels as they are switching their trusted brand of toothpaste from Colgate. That may not be the case for everyone, but I am certain that's relatable to a lot of you.

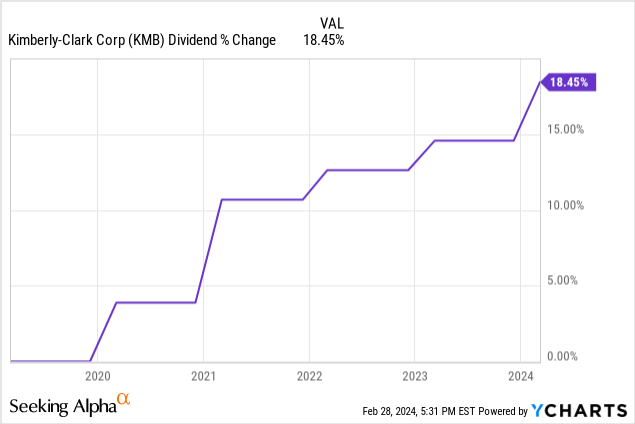

There's a saying that goes, "the safest dividend is the one that was recently raised". However, I do stay cautious about whether or not the dividend is hurting future growth. The distribution was recently raised by 3.4% to a quarterly dividend payment of $1.22/share. The dividend payout ratio sits at about 72% which is above the 5-year average dividend payout ratio of 67.84%. I do hope that eventually this number can come back down to the average. It all depends on how sales and revenue grow once the market slump and consumer spending turns around.

On the bright side, the debt interest coverage ratio remains high at 9.78. This ratio represents how comfortably KMB can pay the interest on their debt. In addition, the company currently has approximately $3.5B in cash from operations, which is a large cushion to ride out these recent headwinds.

While it's hard for me to recommend starting a position here, the dividend is likely to keep growing. For all I know, I can be completely wrong about my thoughts on changing consumer habits. If the payout ratio can eventually come down, this would be a great thing that further reinforces the strength. The dividend growth has been solid in my opinion with a 3 year CAGR of 3.32. Zooming out to a 10-year horizon, the dividend growth is even better at a CAGR of 4.28%. If you are already a holder of KMB, you are likely to continue receiving those steady dividends over the next decade.

The current P/E (price to earnings) ratio sits at 18.45 which aligns perfectly with the sector median of 18.45. However, this current P/E sits below the 5-year average P/E of 20.37. The average Wall St. price target is $127.98/share, which represents an upside of 5.57% from the current level. While I think this sits around fair value due to the limited growth ahead, I will run a DCF (discounted cash flow) calculation to confirm.

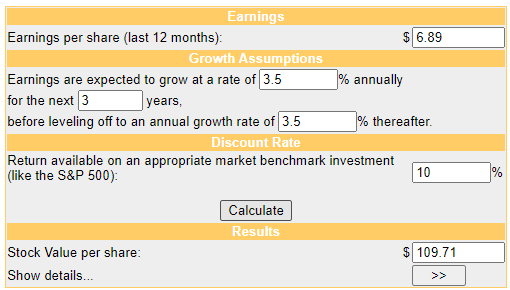

We will use the average estimated EPS of 6.89 for fiscal year 2024 for our input. In addition, total company growth has averaged 4% over the last 3-year period. Management estimates an EPS growth in the high single digits, but I do not think this is likely considering all of the mentioned headwinds. Revenue has grown extremely slow, with an average growth of about 3% over the last 5-year period. So in an effort to get an accurate estimate, we will use a conservative growth input of 3.5%.

Money Chimp

As you can see, we determine a fair value of about $109.71/share. This means that the stock is currently trading at a premium of about 10% at the moment. While the dividend is nice, I don't think it's worth the opportunity cost of waiting for a turnaround story here. Therefore, I rate KMB a Sell.

I rate Kimberly-Clark as a Sell due to the poor growth prospects and a portfolio of products that is easily replaceable by cheaper store-name branded items. The growth strategy laid out by management is to continually increase prices and I think that it may work in the short term but ultimately has a limited runway. The market is shifting and data tells us that customers are open to switching to private labeled store brands in an effort to save money.

Additionally, while the dividend remains attractive at 4%, I do not believe this is compelling enough to warrant a buy. The business itself has issues to work out, and they need to find a way to increase organic growth. The dividend payout ratio has risen above the 5-year average. Management blames the lack of sales on hyperinflation, but we've seen inflation slowly cool over time already. The stock currently trades at a premium to fair estimated value of $109.71/share.