SDI Productions

SDI Productions

When it comes to investing, I have found that it is important to be flexible in your beliefs. When new data comes to light, you should use that data to re-evaluate your investment decisions. This is especially true when it comes to value-oriented investments because, from time to time, you can get a company that is cheap because it deserves to be cheap. Late last year, in October to be precise, I found myself becoming bullish on a bank called Heartland Financial USA (NASDAQ:HTLF). At that time, I called the stock a bargain. Although deposits had dipped slightly in the second quarter of that year relative to the first quarter, the overall trend for deposits, loans, and other aspects of its balance sheet, were mostly positive. Shares looked cheap as well. And at the end of the day, I ended up rating the company a ‘buy’.

Since then, things have gone really well from a return perspective. While the S&P 500 has seen upside of 16.5%, shares of Heartland Financial USA achieved upside of 29.4%. Even after that increase, shares do look to be rather cheap, not only on an absolute basis, but also relative to similar firms. Despite this, I do see some other issues arising. Debt continues to rise, the value of securities continues to drop, and deposits have fallen once again. Uninsured deposit exposure has also risen as well. So although the institution is cheap, I would argue that, especially after seeing such nice upside, it might make sense for investors to look elsewhere for returns moving forward.

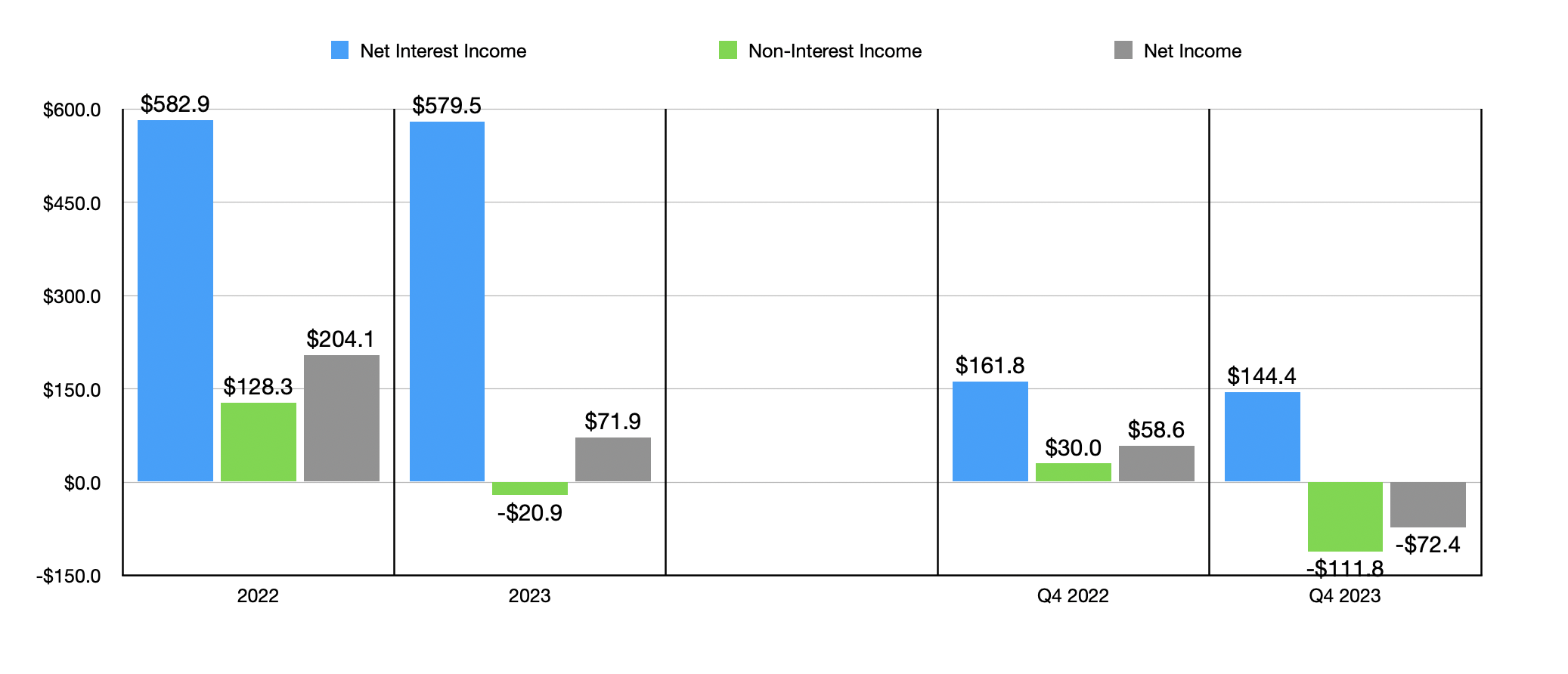

The clearest indication that the picture has changed for Heartland Financial USA can be seen when looking at financial data covering the final quarter of the 2023 fiscal year. While net interest income dropped from $161.8 million to $144.4 million, the bigger problem is that non-interest income plummeted from $30 million to negative $111.8 million. That, in turn, caused the company to go from generating a net profit of $58.6 million in the final quarter of 2022 to generating a net loss of $72.4 million during the final quarter of 2023.

Author - SEC EDGAR Data

It is very important to note that this significant change was driven by a decision that was enacted during late October and early to mid-November to sell off certain investment securities in exchange for $805.8 million. The company recorded a pretax loss of $129.1 million associated with this sale. The objective of management is to basically sell off its lower-yielding investments in order to reduce high-cost wholesale funding to improve the company's bottom line in the long run. Although this did result in a hit in the near term, management said that this repositioning will boost the firm's net profits by $24.3 million on an annualized basis. So investors should view this as a short term hit for long term gain.

Author - SEC EDGAR Data

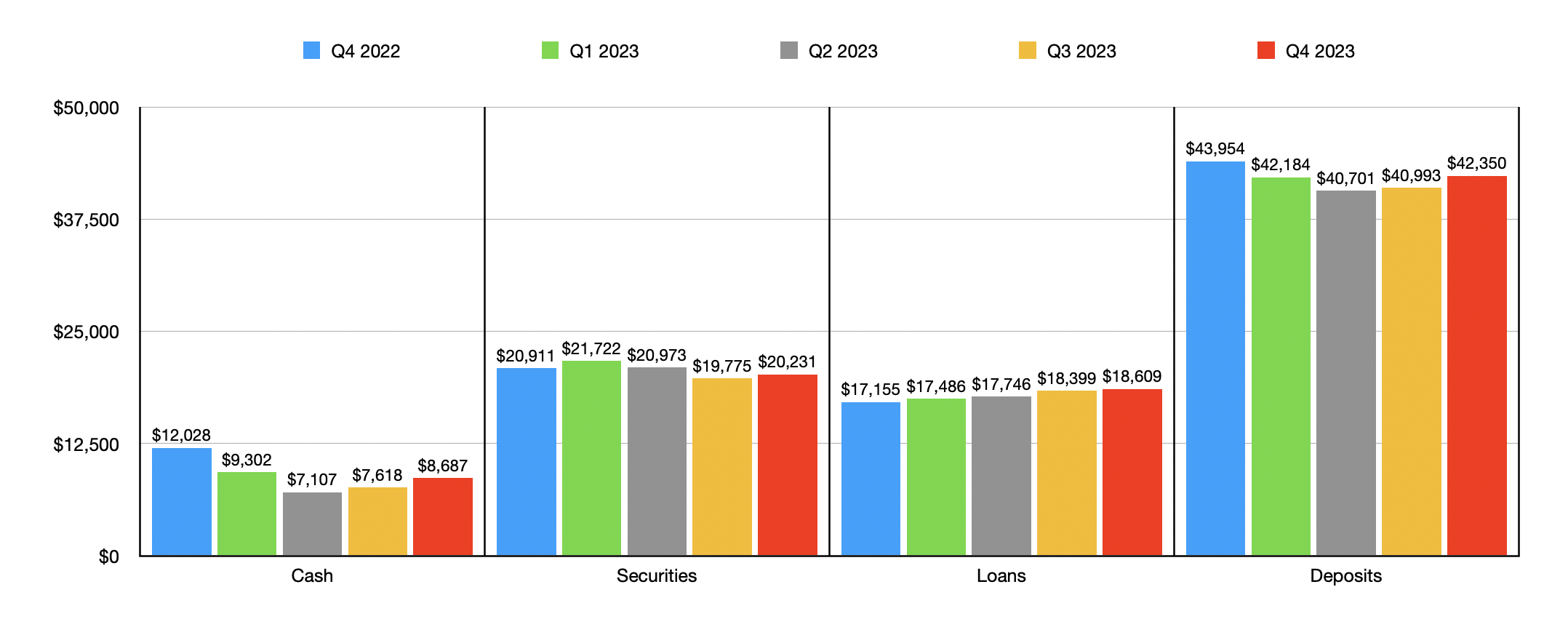

Naturally, this had a negative impact on the value of securities on the company's books. These dropped from $6.41 billion in the third quarter of 2023 to $5.58 billion in the fourth quarter. However, the value of securities had been dropping for some time. They were actually at their highest in 2021 when they totaled just under $7.70 billion. And this is not the only area where the company is showing some weakening. The value of cash has been declining since the second quarter of 2023 when it hit $400.2 million. By the end of the final quarter of the year it had fallen to $323 million. And on top of this, the value of deposits plunged from $17.10 billion to $16.20 billion.

Author - SEC EDGAR Data

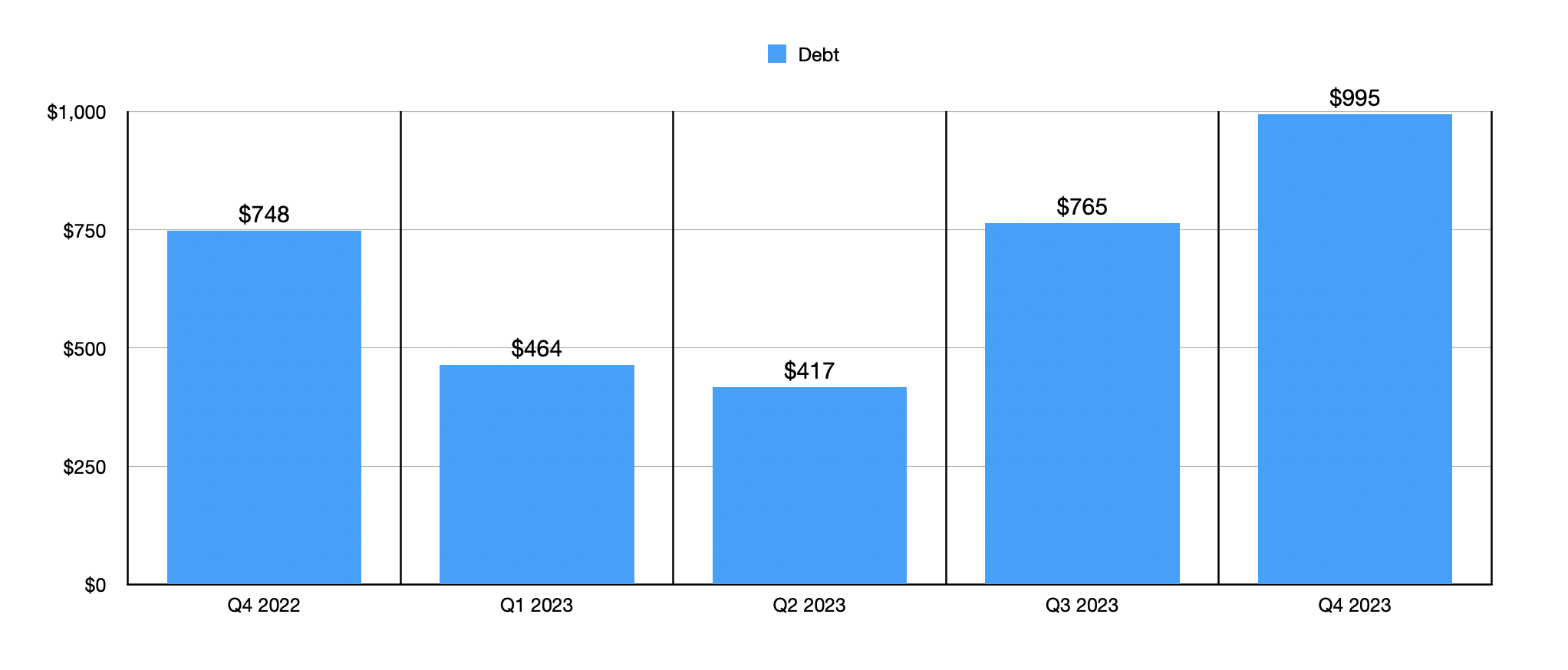

This is not to say that there weren't areas of improvement. The most notable was a rise in the value of loans. At the end of 2022, loans totaled $11.43 billion. They continued to climb each quarter thereafter, eventually hitting $12.07 billion by the final quarter of 2024. But even if you accept this positive development, you start to see some other negatives. As an example, debt totaled $416.8 million in the second quarter of 2023. It approximately doubled to $994.7 million by the end of last year. And on top of this, the value of uninsured deposits went from 34% in the second quarter of 2023 to 39% in the final quarter of the year. This is particularly problematic for me because I typically prefer uninsured deposit exposure to be 30% of overall deposits or lower.

Author - SEC EDGAR Data

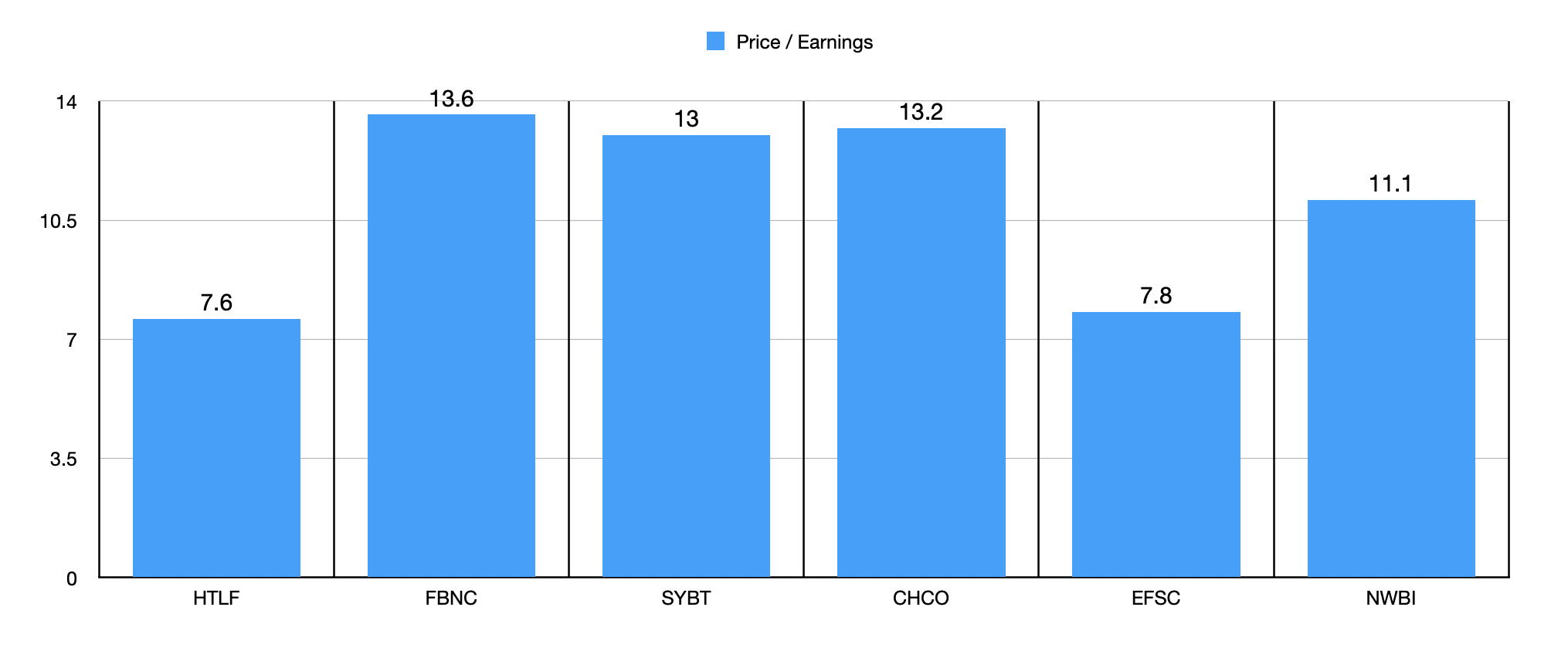

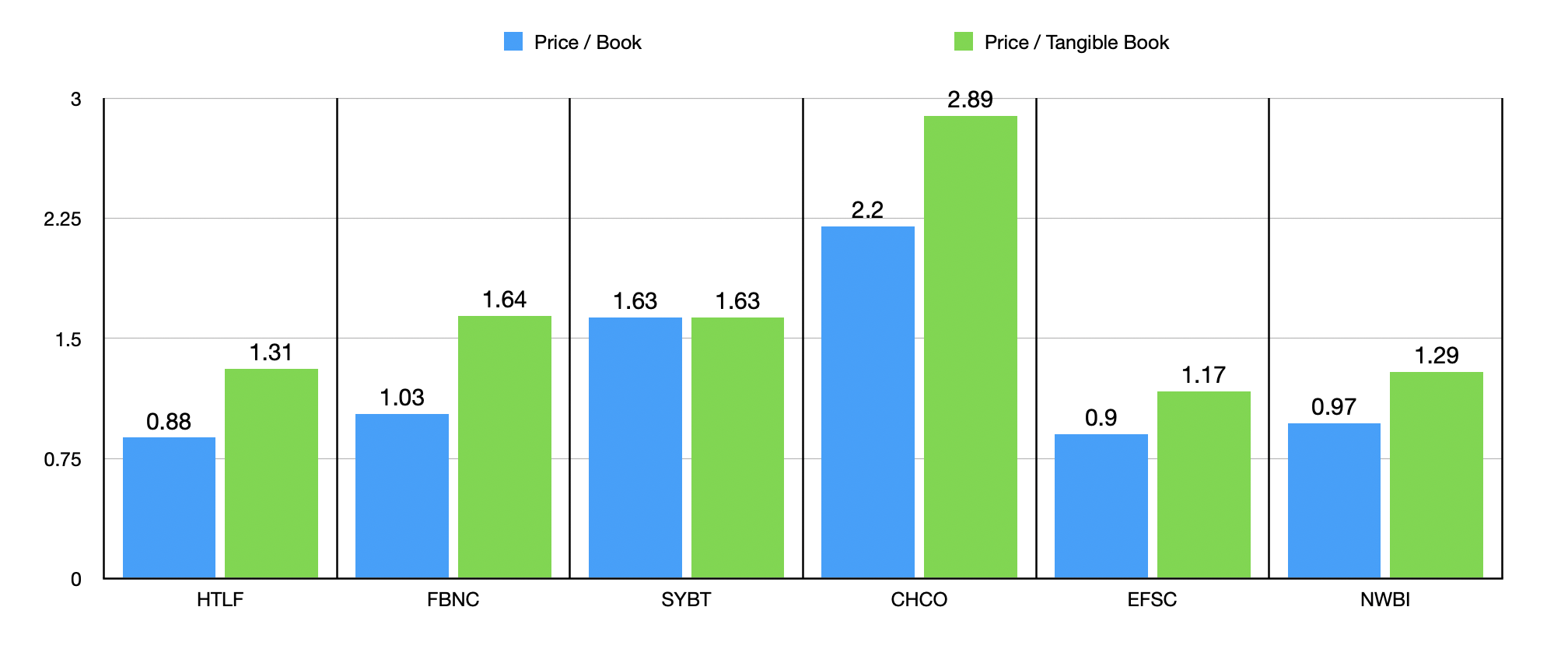

If we strip out the aforementioned one time hit that the company took on its asset sales, then 2023 profits would be around $188.8 million. That implies a price to earnings multiple on the institution of 7.6. When we look at five similar firms, as shown in the chart above, the stock ended up being the cheapest of the group. This is truly great news. I then, in the chart below, look to the business through the lens of the price to book multiple and the price to tangible book multiple. As the chart illustrates, Heartland Financial USA ended up being the cheapest of the group when it came to the price to book multiple. When it comes to the price to tangible book value approach, two of the five competitors are a bit cheaper than it is.

Author - SEC EDGAR Data

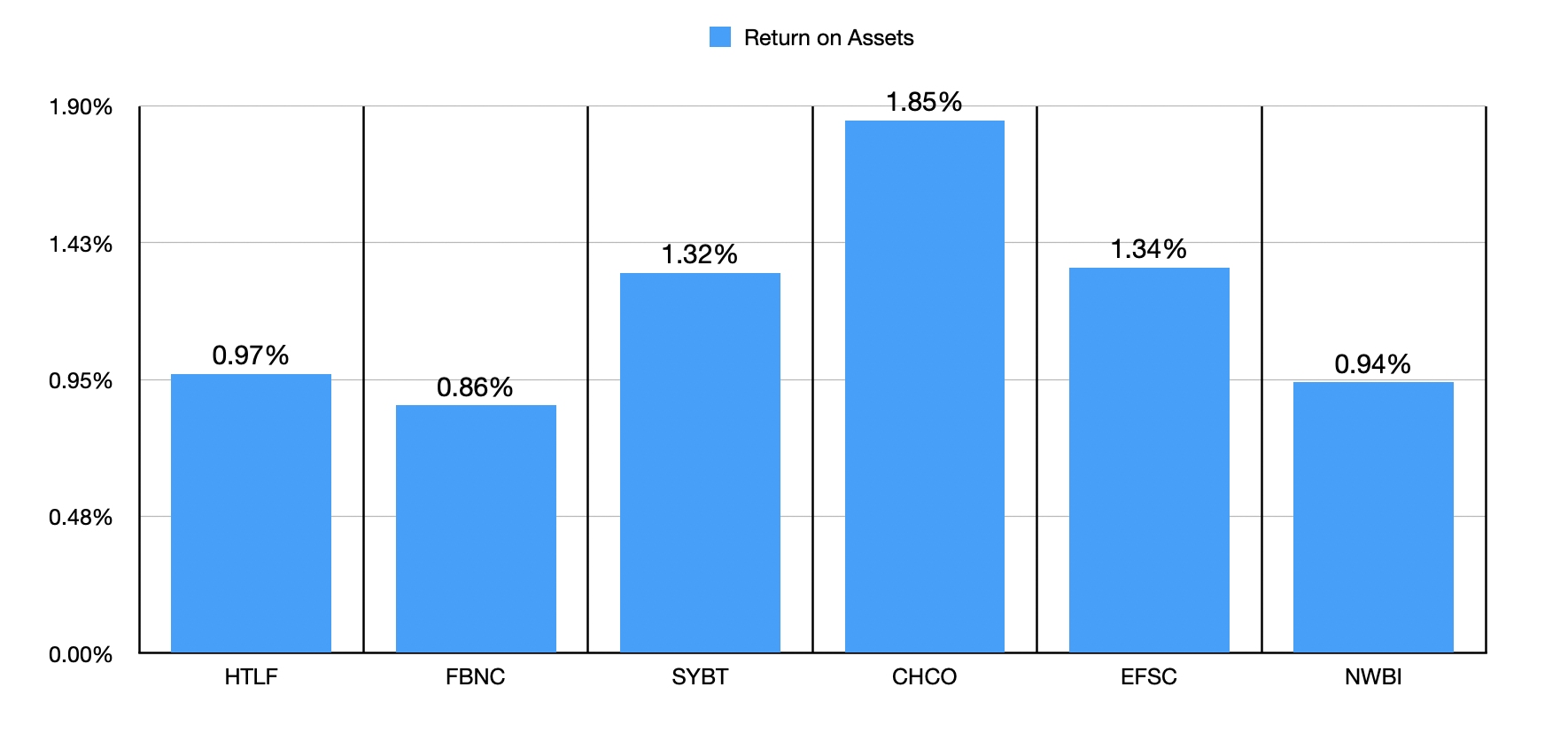

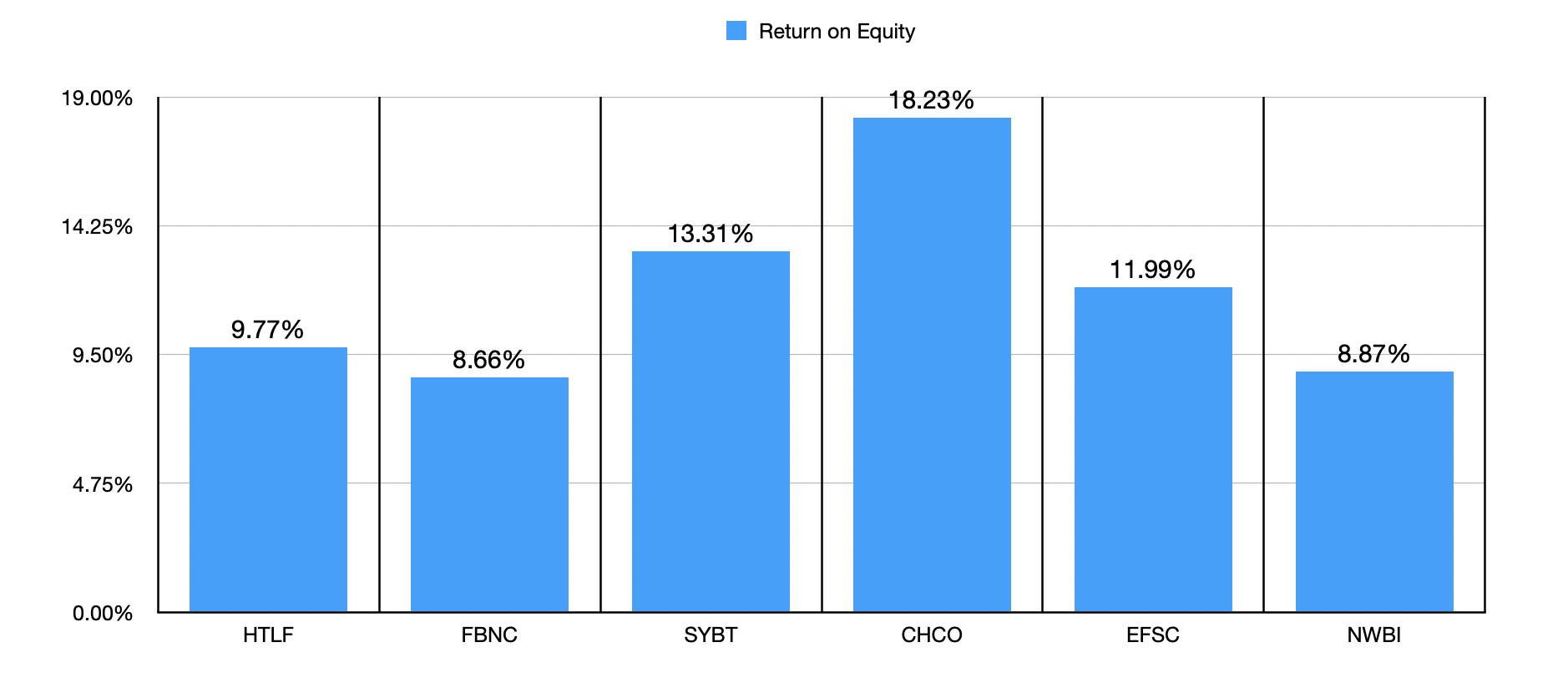

Given this relative valuation, you might think that I am crazy for downgrading the stock. But in addition to seeing debt increase while deposits, securities, and cash, all drop, there's also the fact that there are other ways in which the business falls short. In the first chart below, you can see its return on assets relative to five similar firms. Two of the five companies ended up being lower than it, while the other three are higher. So it does sit around the middle of the group. The same applies with the second table shown below that shows return on equity. And again, these are all using the adjusted numbers to strip out the one time hit.

Author - SEC EDGAR Data

Author - SEC EDGAR Data

It is true that, at the moment, Heartland Financial USA is trading on the cheap. This is true on both an absolute basis and relative to similar firms. It's great to see the value of loans increase. But once you get past that, you start to see other issues. When it comes to return on equity and return on assets, the firm is decent but not great. It certainly doesn't stand out. Deposits have started falling while debt rises. Uninsured deposit exposure is higher than I would like it to be and has risen recently. Cash balances and securities have dropped. To me, this paints a mixed and all-around mediocre picture. So even though the stock has risen nicely in recent months, I have decided to downgrade the stock to a ‘hold’ at this time.