da-kuk

da-kuk

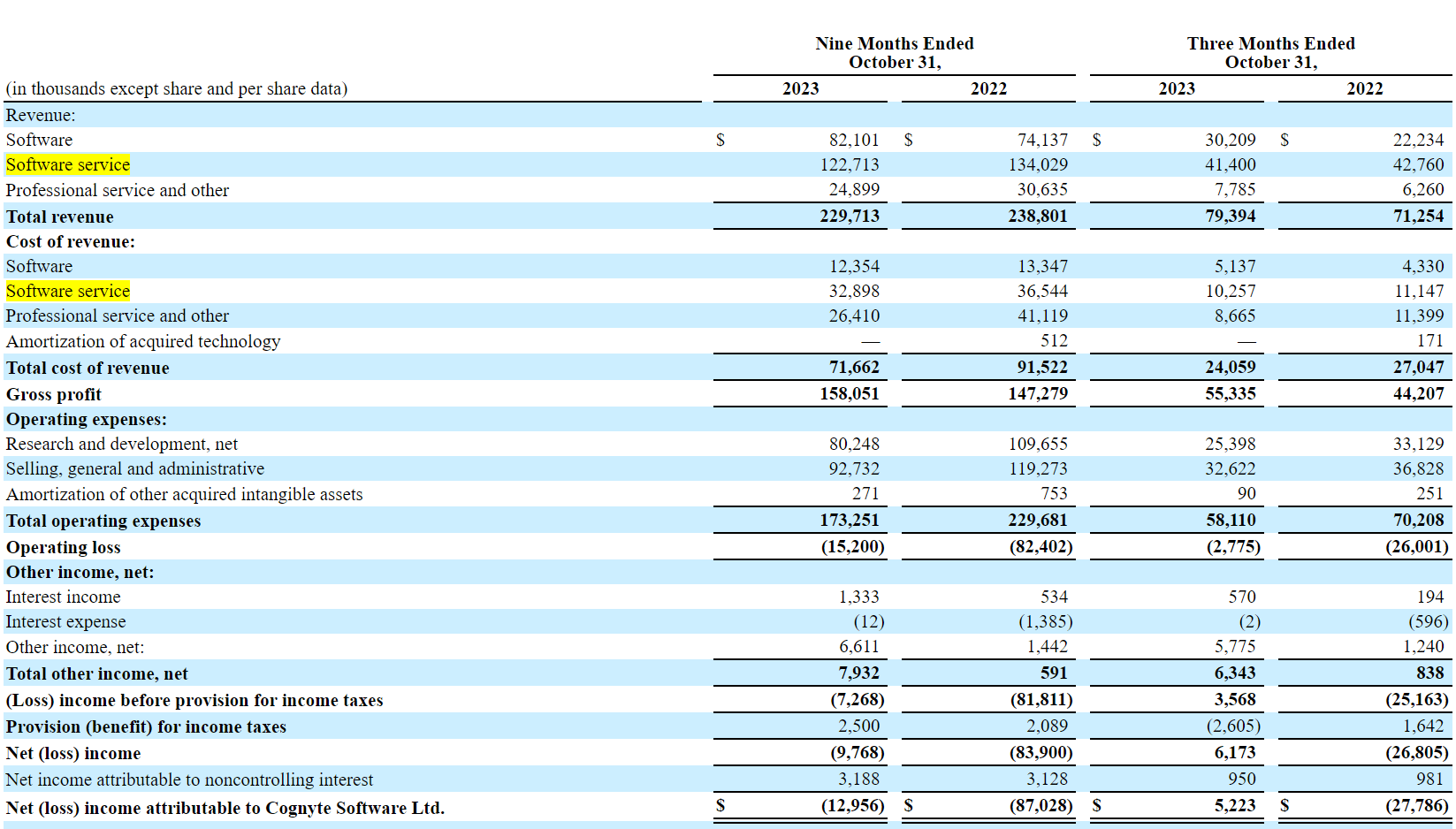

Cognyte Software (NASDAQ:CGNT) is benefiting from sales growth, lower fixed costs, and mix effects, with the tight budgets and more difficult budget conversion improving a lot since last coverage. They are also managing to make headway in the US in terms of revenue growth. While the company is executing well, and there shouldn't be too much of an issue with maintaining growth, we have some gripes with their model and their economics that we'd like to point out, which is that it depends heavily on new wins to drive software revenue in the mix, which also tends to be non-recurring in nature with no long tail like in subscription-heavy businesses. We think in light of everything the valuation looks about fair.

Cognyte has a lot of government customers, leading to pretty lumpy backlog conversion and persistently high receivables. They started to make headway in the US, which would be a tough market to break into. They have done around $100+ million in contract wins from national security and law enforcement entities in the US in this latest quarter. They continue to expect growth of 10% for the year, in line with the growth in this quarter YoY, which also means expected sequential improvement in the Q4 (around $81.3 million in Q4 expected sales). YoY revenue growth improvement will likely look rather high in terms of revenue in the Q4, but this will be because of comp effects, as in late October 2022 a meaningful disposal was conducted making the Q4 comp easier.

Given our performance during Q3 and current visibility, we are raising our revenue guidance for the year to $311 million, plus or minus 1%, representing approximately 10% year-over-year growth at midpoint on an SCS adjusted non-GAAP basis.

Elad Sharon, CEO of CGNT

IS (PR)

Cost controls have been good on fixed costs as well as variable, with total operating expenses down almost 20% in the 3 month figures YoY, and cost of revenue down while revenues are up YoY. Some decline in operating expenses could have been expected related to the SIS disposal, but revenue growth coupled with less COGS is a major win. Furthermore, within software revenue, growth was around 50%, while associated COGS only grew around 20%. Operating losses are therefore substantially thinning. Any further contract wins and revenue growth will be passing through a much more efficient fixed cost structure and create positive scale effects from within software revenue. In terms of gross margin, management is guiding to a 69% overall GM for the full year, meaning around $214 million in gross profit. That implies that compared to the Q3, Q4 GMs are expected to slightly decline. However, management indicates that the GM lift that comes from mix effects around software revenues are still possible going forward, although we have no guidance as to how far or to what extent those dynamics can be extrapolated.

You can see that over the last few quarters, our gross margin is growing in the software and also in the - overall in the professional services. So you can see that the dynamics behind the gross margin are the right dynamics.

David Abadi, CFO of CGNT

Since investigative analytics is in the realm of cybersecurity, there is a good chance of sustained revenue growth on a secular basis, but due to the government end markets and history of quite lumpy economics, it's anyone's guess exactly what revenue growth will be any given year, but it would be reasonable to extrapolate the current pace of growth forward. Compounding sequential quarterly improvement expected of around 3% ahead four quarters, you get around 12% YoY growth as a crude estimate which at least avoids comp effects around the SIS disposal, with 12% not being a bad figure and representing slight acceleration or at least on par growth with current Q3 run-rates.

It is very in vogue now for businesses that sell perpetual licenses to start shifting their model over to subscription, which is more recurring in nature. Companies like Avid Technology (AVID) were in the process of doing this with their digital audio workstations software before they were acquired. Cognyte sells substantially perpetual licenses on the software side, and therefore maintenance contracts on the software service side separately, where maintenance would otherwise be included in the subscription price for companies selling software on that model. While we don't know exactly what the breakdown is for different products and services in each of the segment revenue lines, features of this sort of revenue recognition have an effect on the economics of the business, particularly as software revenues, the line item that would include these perpetual license sales, are going to be of higher margin. The details of revenue recognition and what activities are conducted in each of the segments can be found in the latest annual report.

Service contracts are recurring in nature, and contribute meaningfully to recurring revenue which is disclosed annually, and at the FY was around 66% of revenue was recurring. In the 3 months data, service revenue was relatively flat, and the growth was being driven by software which scales much better as mentioned before and offers better baseline GMs. Software substantially represents sales from perpetual licenses, and to a lesser extent for subscriptions of other kinds. This is where the nonrecurring revenue is focused.

As new contract wins happen, revenues are recognised in software in a frontloaded manner as it is largely in perpetual license sales, while the maintenance contracts are going to be recognised over time and later on with less margin contribution. The margin lift is frontloaded with a contract win and recedes with time, as software which is higher margin and less recurring when sold as perpetual licenses grows in the mix on new contract wins. The contribution from maintenance which is lower margin comes later. This means that structurally, it's important for Cognyte to keep generating new business and perpetual license sales, otherwise margins will average down towards that of the software service segment. This effect is in addition to the gross margin lift we see within software revenue when it grows, which management seems to indicate can continue for some time.

Cognyte will do well as long as it can continue to keep the pace of winning new business, and ideally accelerate growth to keep perpetual licenses high in the mix and to continue to scale the software gross margins. Due to the idiosyncratic nature of the contracts they win, particularly with government bodies, we can't predict how these dynamics will evolve beyond saying directionally that the pace of contract wins is proportional to margins.

Regardless of mix effects, new wins will also help a lot with substantially lower fixed costs YoY. Even if wins slow, while it will have a negative margin effect, recurring maintenance revenue still mitigates trouble for the business. Demand for investigative analytics software seems pretty high with their primarily government contracts, there's not any major reason why they can't keep copping wins.

In terms of valuation, we can't compare CGNT to the typical array of cybersec companies, since their economics are quite different from Cognyte's and they're of a completely different scale. CGNT has a P/S of 1.67x based on this year's expected $311 million in revenue. Average IT is around 2.8x based on figures from Seeking Alpha. Initially it looks compelling, but we point out that while they are inflecting into profitability, they still aren't profitable yet unlike IT companies, even though it's very achievable for CGNT thanks to all the margin lift effects we explained, helped disproportionately by a strong pace of new contract wins. CGNT's position and scale has it facing government customers to a large extent, leading to structurally higher working capital as seen with the large receivables balance. Lower margin on the recurring component also creates that negative margin effect on slowdowns, which is the opposite of what's typical for sell and service businesses, like automotive and other industrial businesses. It's tough to define an exact fudge factor on the valuation, but we feel more of a discount would be nice, and don't think the difference in multiple is enough for CGNT to be especially compelling given the lack of margin mitigation on slowdowns due to perpetual licenses having positive mix effects, and the high structural working capital.