Stadtratte

Stadtratte

The Carlyle Group (NASDAQ:CG) is a Washington, D.C.-based multinational private equity and asset management financial services company with >$426bn in AUM. The company focuses on three primary verticals; Global Private Equity, which comprises the bulk of its operations; Global Credit, focusing on collateralized private credit markets and derivative securities; and Global Investment Solutions, encompassing the firm's more secular asset management streams.

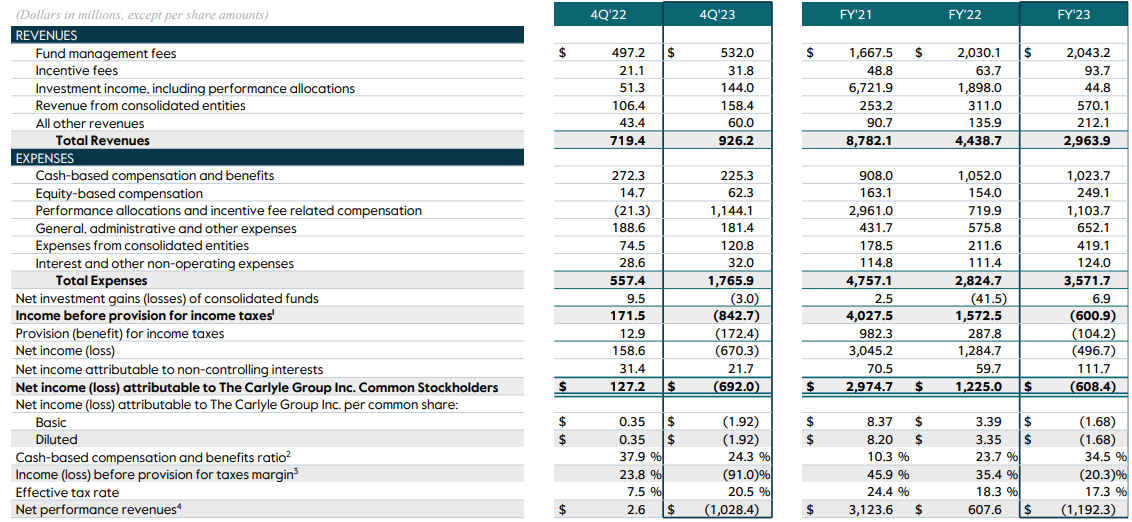

Carlyle FY23 Presentation

Through these activities, across FY23, Carlyle has achieved revenues of $2.64bn- down 44.66% YoY from FY22- alongside a net income of -$608.40mn- a 149.67% decline- and a free cash flow of $875.00mn- a 14.84% increase driven by increased cash from investing activities.

In my last article, I focused on Carlyle's increased interest in alternative credit platforms, specifically collateralized loan obligations geared towards commercial debt. While this remains an important growth driver for the firm, Carlyle has since returned ~38% net of dividends, exceeding my price target. However, also since then, Carlyle has outlined its strategy for the year ahead, leading to revised valuations.

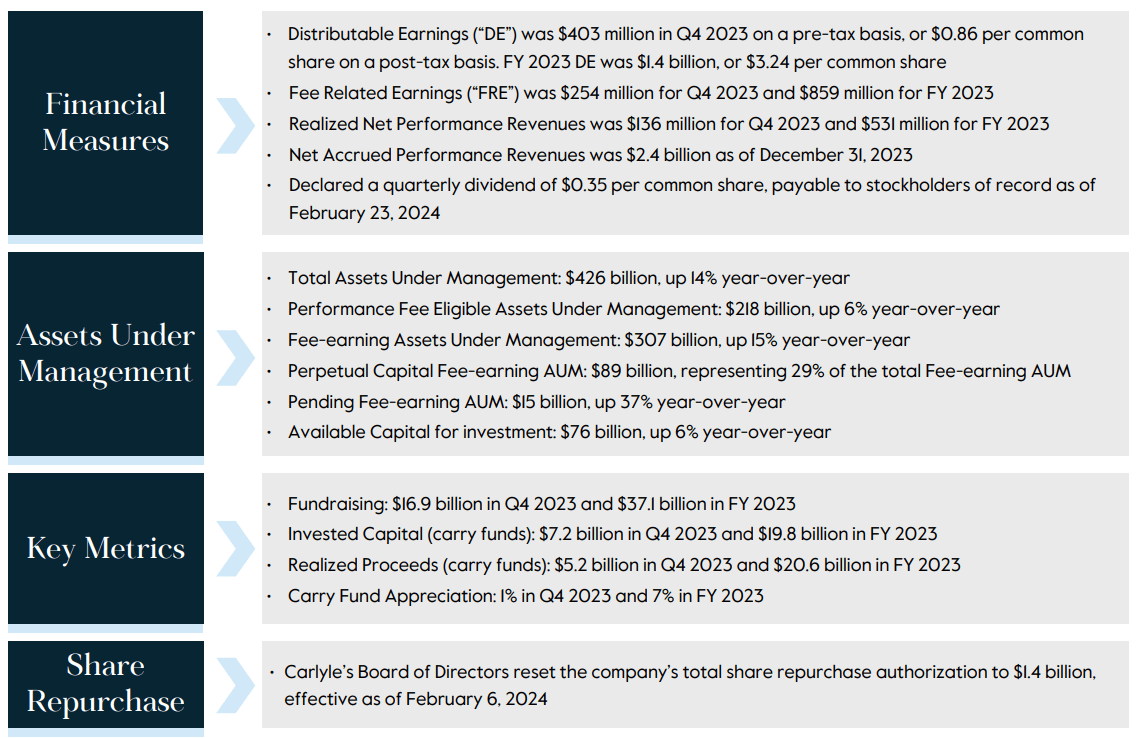

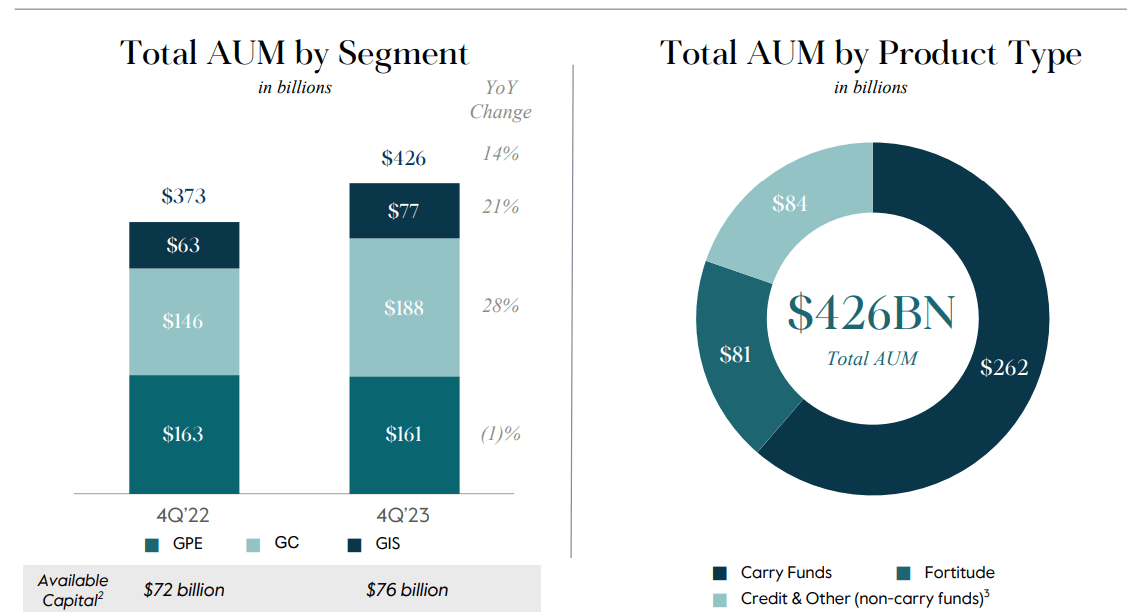

Before we can assess the changes in the firm, though, we must evaluate the firm's holistic positioning; Carlyle previously announced a $0.35 dividend/common share, supported by material expansions in fee-earning AUM- FAUM- with total AUM up 14% YoY in spite of inflation and interest-related difficulties. Additionally, Carlyle has fundraised $37.1bn over FY23 and authorized repurchases of ~$1.4bn.

Carlyle FY23 Presentation

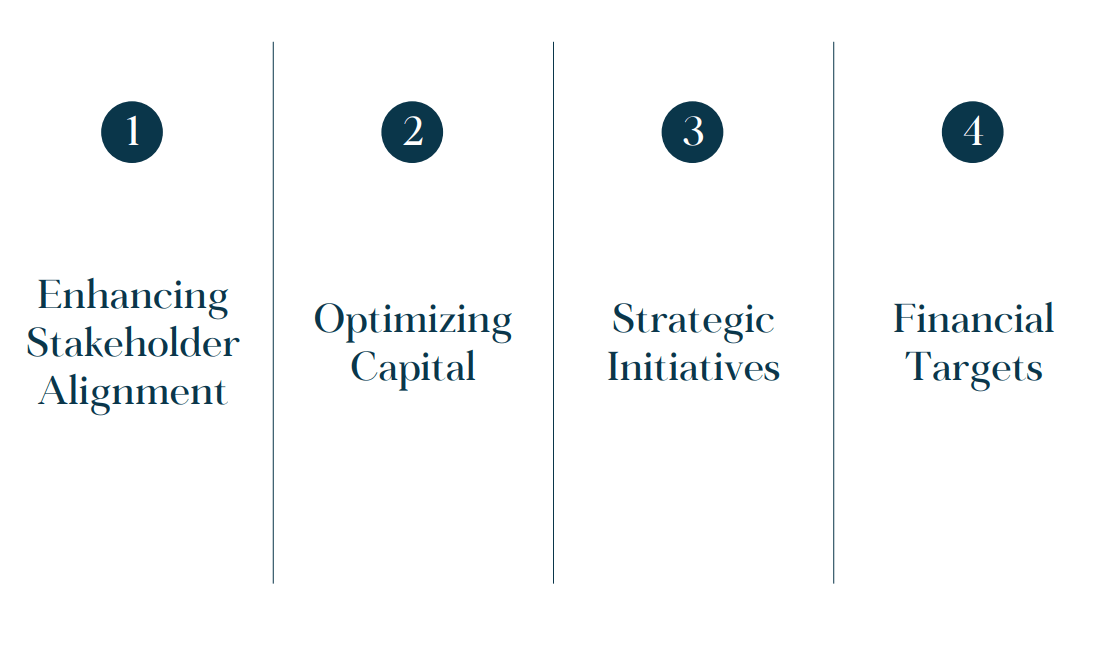

In doing so, Carlyle aims to fulfill its four broad guiding themes, including driving stakeholder alignment across shareholders and fund investors, optimizing capital efficiency and lowering capital costs, emphasizing general strategic initiatives across its private assets, and achieving financial targets above all else.

Carlyle FY23 Presentation

Due to these actions, in addition to favourable macro circumstances, I would rate Carlyle a 'buy'- but the firm trades at a premium, leading me to rate Carlyle a 'hold', leaning towards a 'buy'.

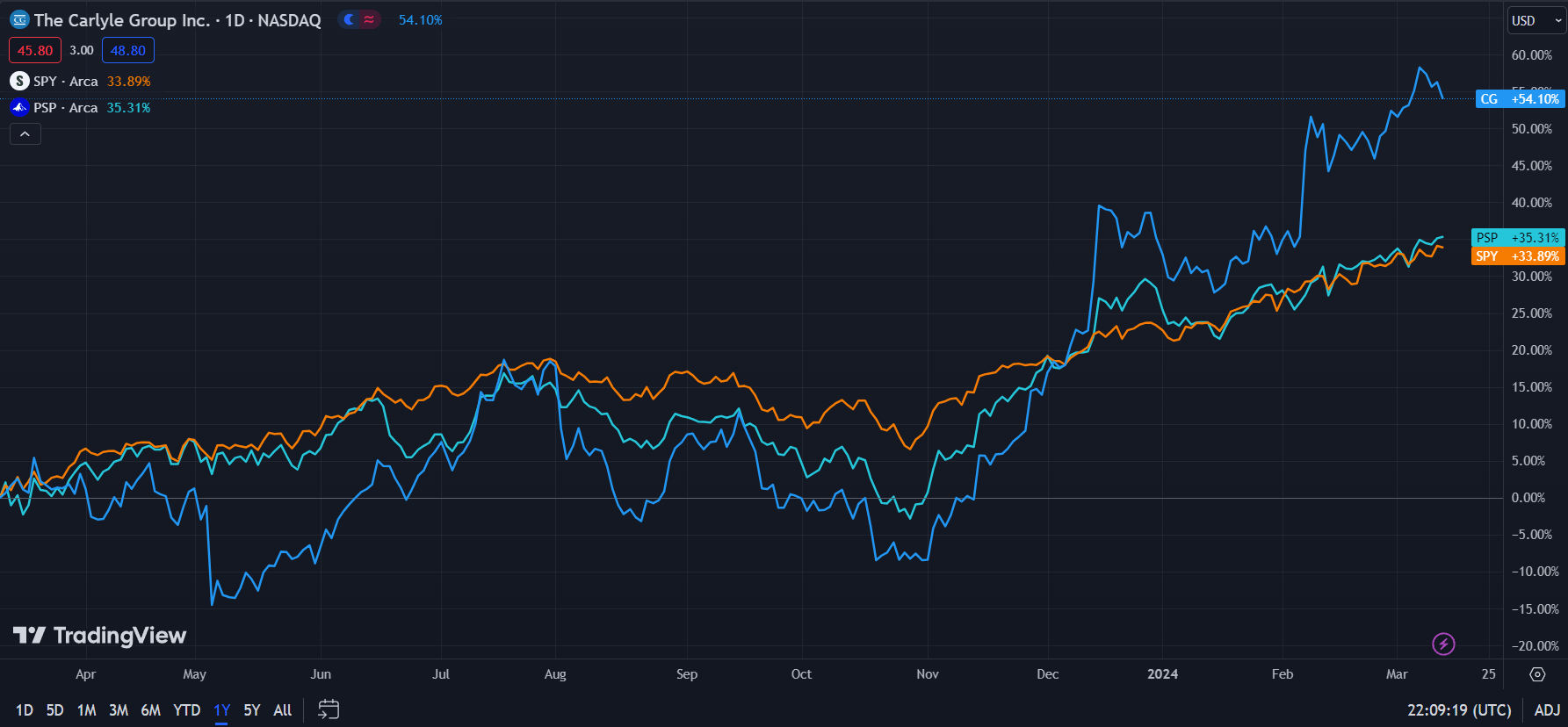

In the past year, Carlyle's stock- up 54.10%- has outperformed both the Invesco Global Listed Private Equity ETF (PSP)- up 35.31%- in addition to the broader market, as represented by the S&P 500 (SPY)- up 33.89%.

Carlyle Group (Dark Blue) vs Industry & Market (TradingView)

While the market and private equity industry have generally seen upward movement propelled by a recovery theme from higher interest rates and outperformance from poor analyst expectations, Carlyle in particular has consistently beaten earnings, most recently outperforming by $0.08 normalized EPS.

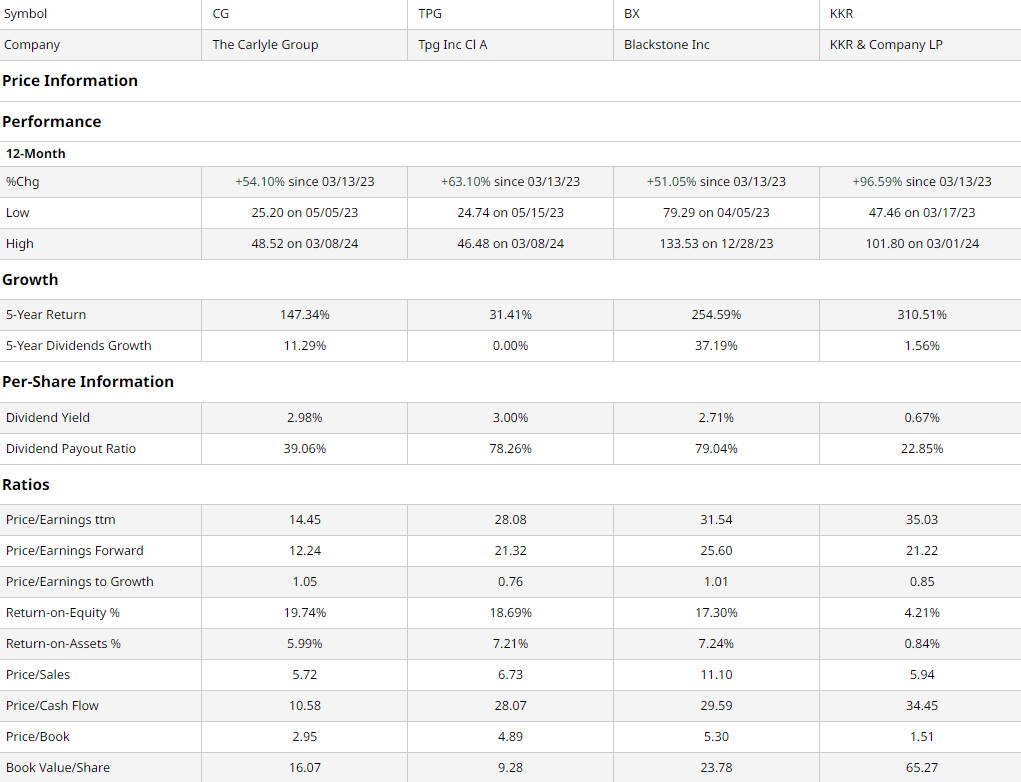

While private equity companies have made a point of differentiating their cash flows, with some reorienting towards the growing private credit business and others doubling down on deal flow, they remain largely comparable. As such, I sought to compare Carlyle to other major public private equity firms of similar operations, as listed on the 'Peers' tab of Seeking Alpha's page of the stock. This group includes the New York City-based alternative investment manager, TPG Angelo Gordon (TPG), the largest private equity firm in the world, the real estate-focused Blackstone (BX), and leveraged-buyout titans, the New York City-based KKR & Co. (KKR).

Barchart

As demonstrated above, in parallel with other private equity firms, Carlyle has experienced strong TTM growth, with KKR's 96.59% growth leading the peer group. Despite this strong growth, Carlyle maintains strong value indicators, indicating the industry premium more so than the inherent value on Carlyle's part.

For example, Carlyle maintains the best-in-class trailing and forward P/E ratios, alongside the lowest P/S, P/CF, and second-lowest P/B ratio demonstrating strength across all three financial statements.

Moreover, Carlyle's peerless ROE and third-best ROA signal superior growth capabilities over other private equity shops. Additionally, investors can enjoy a strong and growing 2.98% dividend off of a conservative 39.06% payout ratio.

However, Carlyle does maintain the highest PEG ratio, suggesting the aforementioned growth is largely priced in. This is alongside the second-lowest book value per share, increasing equity risk for investors.

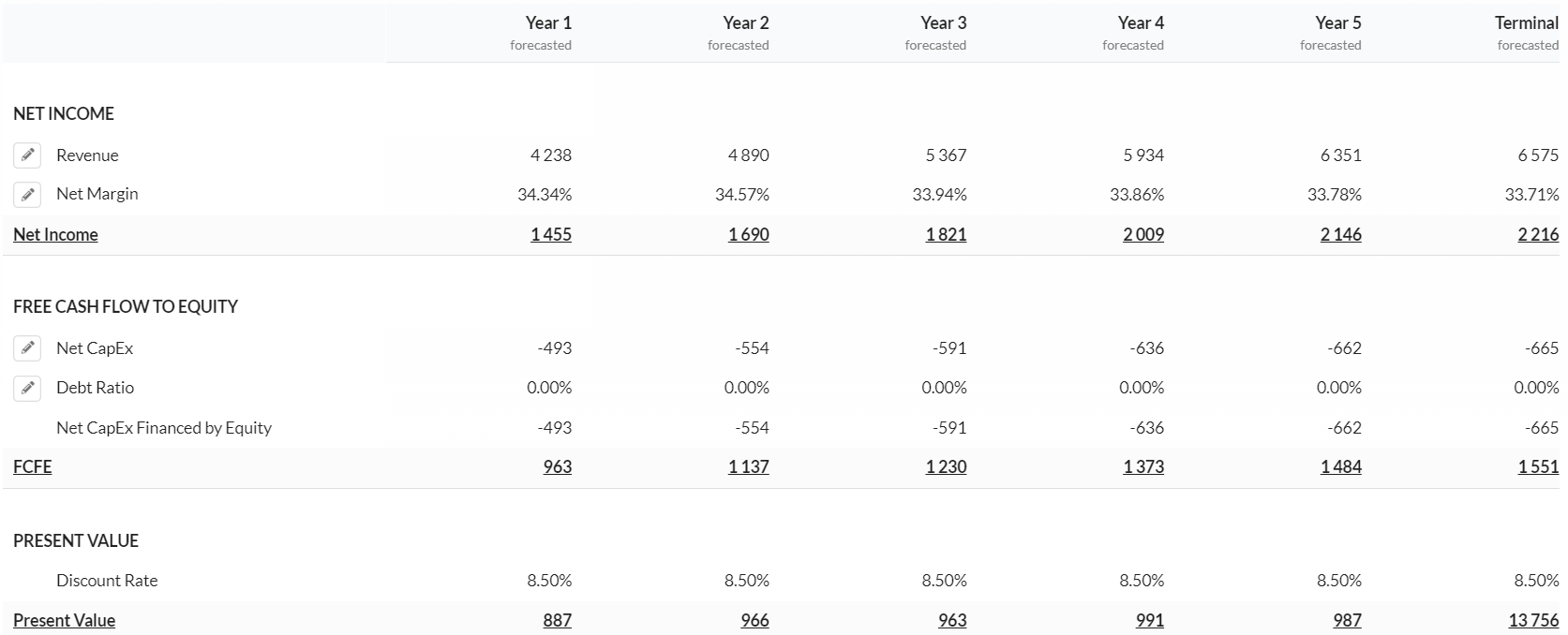

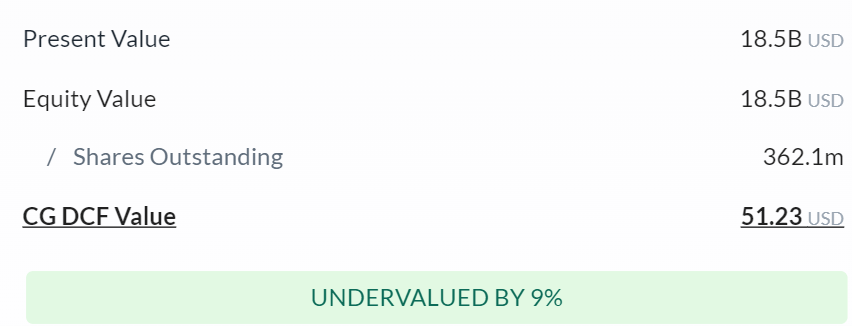

According to Alpha Spread's discounted cash flow analysis, at its base case, the net present value of Carlyle should be $51.23, representing a 9% undervaluation.

Alpha Spread Alpha Spread

The model, calculated over 5 years without perpetual growth built-in, calculates an increase in the value of Carlyle's shares over the previous model due to lower interest rate expectations going forward. I estimated and input a discount rate of ~8.5% due to the potential for lower rates.

Alpha Spread

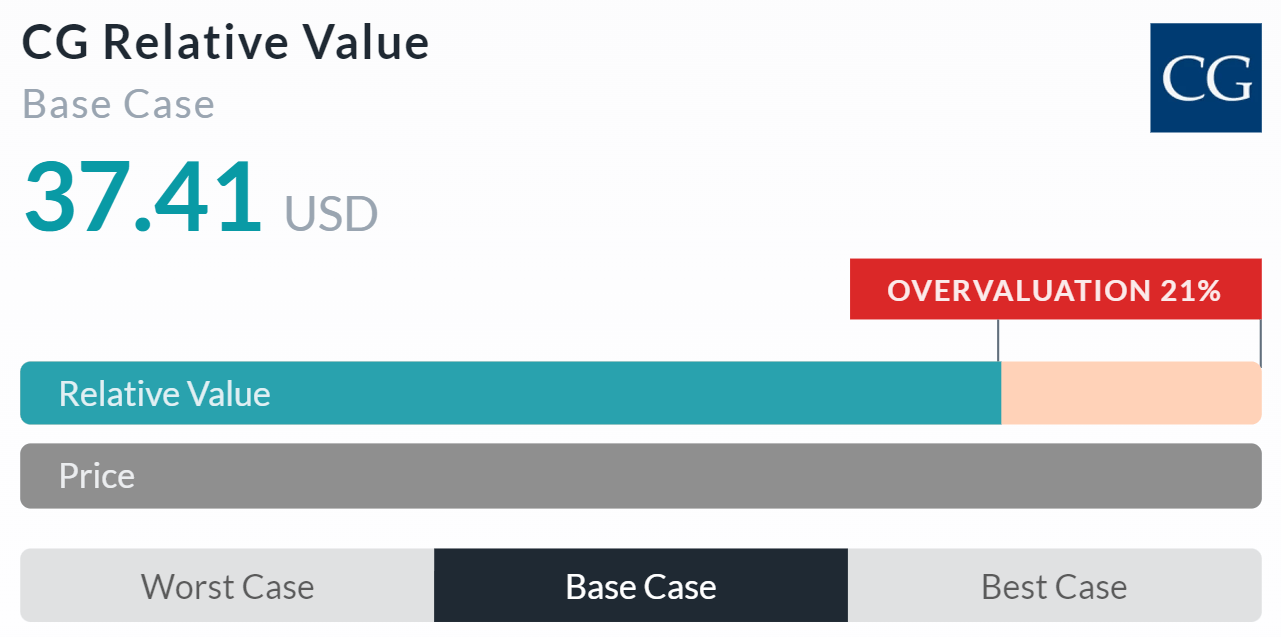

On the other hand, Alpha Spread's multiples-based relative valuation tool estimates an overvaluation of 21%, projecting a relative price of $37.41. While Alpha Spread's model is sometimes skewed by outlier comparators, I believe this to be an accurate representation of Carlyle's relative value.

Therefore, averaging out the NPV and relative value, the fair value of Carlyle should be ~$44.32, representing a ~6% overvaluation.

In terms of operational potential, my opinion is more bullish; Carlyle manifests strong asset diversification with low capital given >$76bn in available capital. Unlike other private equity firms- such as Apollo (APO) which has bet big on private credit or Blackstone's real estate focus- Carlyle has developed a sustainable and diversified model, spread between Global Private Equity, Global Credit, and Global Investment Solutions, with the latter two driving Carlyle's AUM growth.

Carlyle FY23 Presentation

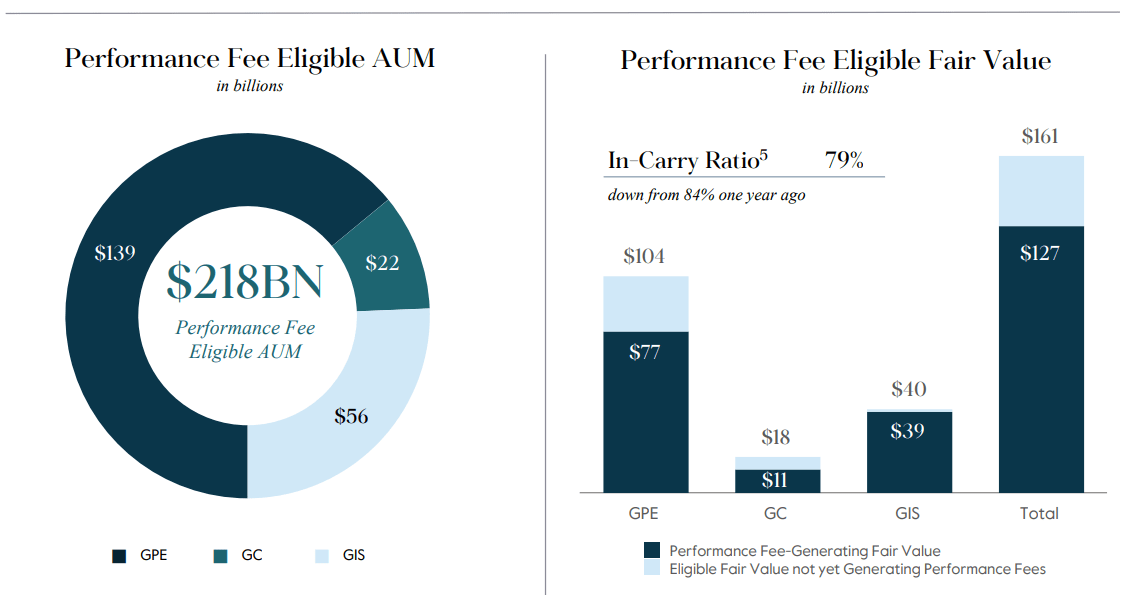

Despite this asset mix, Carlyle retains a large exploitable market in terms of FAUM, with Global Private Equity currently dominating fee earnings. As such, private credit and other investment solutions can lead to material margin expansion given continued scale growth. While Global Private Equity and Global Investment Services are highly dependent on rate swings, Global Credit may continue to grow secular of rates, though magnitudes may shift with rates.

Carlyle FY23 Presentation

Ultimately, through all its activities, Carlyle intends to fulfill its FY24 objectives, including targeting fee-related earnings of ~$1.1bn, expanding margins to 40-50%, supporting >$40bn of inflows through fundraising, and a share repurchase capacity of $1.4bn in addition to the extant dividend of 2.98%.

Carlyle FY23 Presentation

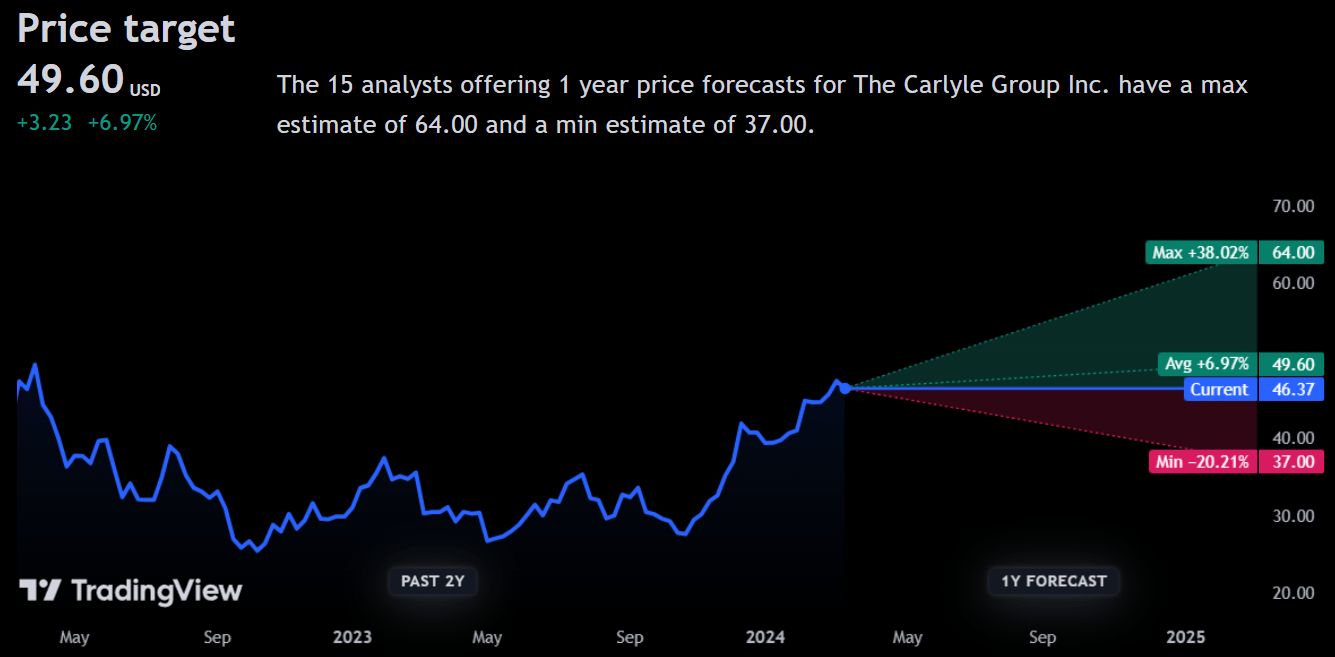

Analysts are slightly more optimistic than I am about the stock, estimating an average 1Y price target of 6.97% to a price of $49.60.

TradingView

Inversely, in the worst case, analysts project a minimum price target of $37.00, representing a decline of 20.21%.

This polarized attitude likely reflects differing analyst opinions of the significance of lower rates- or the likelihood of lower rates in 2024- for Carlyle and its earnings.

While most analysts expect rates will decline in 2024, the cost of capital will nonetheless remain heightened- with a large part of Carlyle's business still dependent on traditional private equity deal flow and holdings, this means the firm's revenues may be sensitive to rate swings. This also holds true for underlying asset values, which may inhibit the firm's operational flexibility, especially in terms of capital fundraising.

On the other hand, as asset managers, banks, and other private equity firms diversify, an increasing number of institutions are looking towards private markets for margin enhancement. In turn, competing for fundraised capital may mean lower margins for Carlyle, as more would be returned to investors. This may depress margins and reduce reinvestment or capital return capabilities for Carlyle.

Looking forward, although Carlyle maintains a solid, diversified operational model, the company trades at a small premium, which may inhibit medium-term growth prospects.