pixdeluxe/E+ via Getty Images

pixdeluxe/E+ via Getty Images

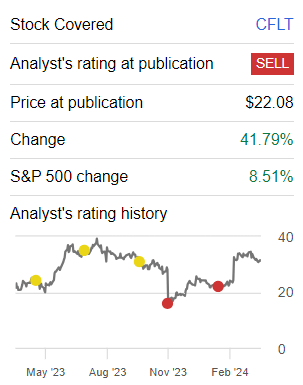

Confluent, Inc. (NASDAQ:CFLT) is a contentious stock. The business's growth rates are moderating. More specifically, despite management declaring that this business can grow at 30% CAGR, including the presumption of revenue beats each quarter of 2024, its growth rates will still be sub 30%.

However, Confluent's underlying profitability is expected to ramp up significantly in 2024, so that investors can see a path for Confluent to exit 2024 with 4% non-GAAP operating profits and climbing higher into 2025.

Therefore, I change my rating from a sell to a buy. And feel no scruples about admitting I was previously wrong and changing my mind, when new facts present themselves.

In my previous analysis back in January, I was bearish and stated that:

Concerns about the company's decelerating growth with the need to demonstrate meaningful profitability pose challenges. Even if Confluent achieves a 25% CAGR in 2024, I argue that the valuation may lack a sufficient margin of safety for investors.

Author's work on CFLT

With the benefit of hindsight, I called this wrong. While I was very much on the right path in terms of its growth rates, I was wrong in that I didn't factor in such a massive increase in profitability for 2024.

Confluent specializes in data streaming, providing tools and services for businesses to manage and analyze large amounts of data in real time. Their main product, built on the open-source technology Kafka, and their cloud-based service, Confluent Cloud, enable companies to process incoming data continuously, facilitating quick and informed decision-making based on real-time information.

Confluent competes directly against the large tech players, for example, Amazon's (AMZN) AWS' Amazon Kinesis and Microsoft's (MSFT) Azure Stream Analytics, but many other players too.

Confluent's near-term prospects appear promising as the company continues to capitalize on the growing demand for data streaming platforms.

Its transition to a fully consumption-oriented go-to-market model for Confluent Cloud indicates a strategic shift towards enhancing customer acquisition and maximizing revenue potential. Admittedly, I'm not a fan of consumption-based business models, but in the past few years, there's been a big move toward this sort of model being popularized. The drawback of this model is that the company puts itself at the opposite end of the table from the customer, in that the more the customer uses the service, the bigger the bill. It's essentially the opposite of Netflix (NFLX), which promotes binge-watching and maximum engagement.

By adapting sales compensation and product pricing to reduce friction and encourage expansion, Confluent aims to accelerate growth and capture more market share in data streaming opportunities. Furthermore, Confluent's recognition as a leader in the data streaming category by industry analysts like Forrester and InfoWorld underscores its position as a frontrunner in the market, instilling confidence among customers.

By offering a comprehensive platform that integrates stream processing seamlessly with its core Kafka infrastructure, Confluent aims to become the go-to solution for businesses seeking to harness the power of real-time data analytics.

Despite its promising outlook, Confluent faces several challenges too. For example, navigating the competitive landscape in the data streaming market, which has become increasingly crowded with both large tech players and new entrants.

Given this context, let's now discuss its financials.

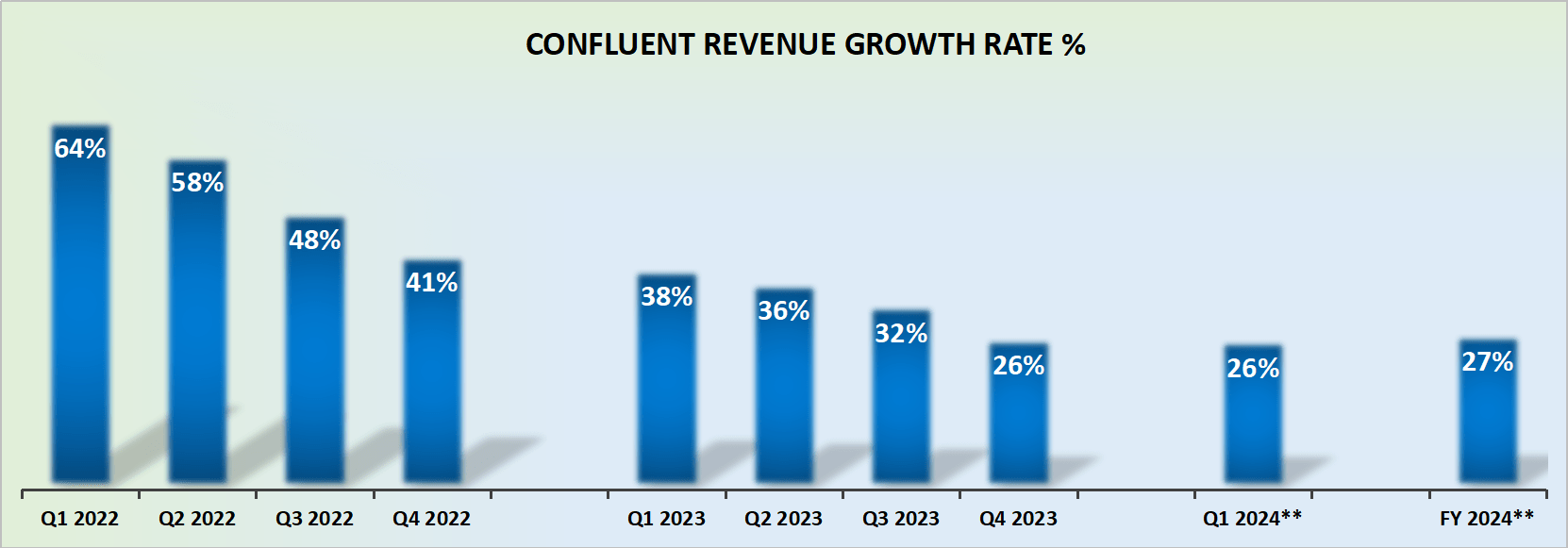

CFLT revenue growth rates

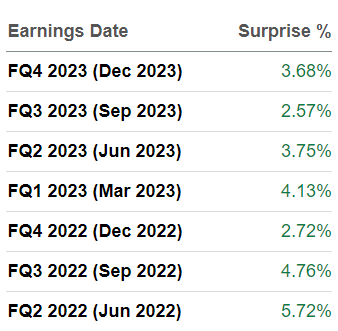

Confluent has provided guidance indicating a CAGR of approximately 25% for the upcoming year. However, considering that 2023 presents a somewhat less challenging hurdle for Confluent to surpass, coupled with the historical trend of Confluent's management exceeding revenue consensus by approximately 2% to 3% (see below), this strengthens my belief that there is a very high probability that Confluent will meet or slightly exceed its present guidance. Consequently, this could lead to achieving a 27% CAGR in 2024.

SA Premium

That's clearly a positive element. But the actual bull thesis is described next.

Confluent is rapidly making its way to profitability. According to my estimates, by the time Confluent exits 2024, it will be a on path toward sustainably delivering 4% non-GAAP operating margins or higher. To support this reasoning, consider that Q4 2023 just ended with 5% operating margins.

Furthermore, even though Confluent's guidance for 2024 points towards breakeven profitability, the fact that Q1 is expected to come in at negative 4% (or better), implies that the second half of 2024 should see Confluent's underlying profitability rapidly increasing.

This means that investors are today asked to pay 10x forward sales for Confluent, as an unprofitable business, but in the next twelve months, investors will be more than willing to pay 10x forward sales for a business that's growing at more than 25% CAGR, while delivering about 4% non-GAAP operating margins.

Along these lines, consider what management said on the earnings call,

[...] we are focused on sustaining efficient growth in 2024 by delivering our first breakeven year for both non-GAAP operating margin and free cash flow margin. Given our solid Q4 performance, we feel confident in delivering 22% total revenue growth for 2024 and eventually returning to our midterm target growth of 30%.

In conclusion, Confluent's near-term prospects exhibit a notable improvement in profitability.

While concerns regarding moderating growth rates persist, the anticipated ramp-up in underlying profitability throughout 2024 signals a compelling opportunity for investors.

With revenue growth rates projected to reach 27% CAGR in 2024 and a trajectory towards achieving 4% non-GAAP operating margins, Confluent, Inc. stock presents an attractive investment proposition, warranting a change in my rating from sell to buy.