d3sign/Moment via Getty Images

d3sign/Moment via Getty Images

The access to 50% of card swipe data in the United States is a valuable asset for Cardlytics, Inc. (NASDAQ:CDLX) and its relationship with major U.S. consumer banks offer it a strong customer base for targeted marketing campaigns. The increasing trend in the digital banking and payment sector is poised to provide boost to the company's growth prospects. CDLX offers a clear value proposition, access to bank channels and data, and has a scalable business model, with that being said, I am concerned about the impact of macroeconomic factors on consumer spending and advertising budgets in the short to medium timeframe, which may limit top-line growth. Therefore, at this time I am on the sidelines and assigning a hold rating to the stock.

CDLX has a powerful digital advertising platform that enables companies to develop and control targeted marketing campaigns based on consumer purchase data. The company's large network of bank partnerships, including four out of the five largest banks in the US, gives CDLX access to roughly 50% of all card swipe data in the country, covering over 168 million bank customers. With this purchase data, CDLX can create specific marketing campaigns that will allow consumers to save money while providing advertisers with extra sales/share gains and revenue for both the company itself as well as its FI partners. The company offers its FI partners access to the purchase data from revenue-sharing agreements. From my point of view, these agreements create a mutually beneficial relationship that drives robust growth for all parties involved. Along with the tremendous value provided by transaction data/analytics, I think that CDLX is only beginning to tap into a massive digital advertising market. As per Insider Intelligence, digital advertising spending in the US reached ~$263 billion in 2023 that implies CDLX share is less than 1% based on last 12 months revenue. Considering the immense collection of data that is available to CDLX and its low penetration in the digital advertising market I believe it will be able to drive healthy growth for many years.

Company Presentation

I am optimistic about CDLX's core platform, which is built on a lot of purchase data and bank partnerships. Dosh and Brig acquisitions have provided more diversification to its platform. Furthermore, Dosh has lots of partnerships with many FinTech players/neobanks such as Venmo, Betterment, and Ellevest which I consider a natural fit for CDLX, extending its reach to include firms that are closely related to its core banking customers. The scale of most of these companies is smaller than CDLX's top bank partners, but I think this will help CDLX serve more users in the underbanked category. Moreover, the Dosh acquisition has put CDLX in a prime position to continue its growth further as some of these FinTechs/neobanks are expected to grow very fast and eventually take a large portion of market share from the big banks.

After announcing its Q3 results, CDLX announced preliminary Q4 results and provided an outlook that is light on billings and revenue but brackets consensus on EBITDA. In 4Q, CDLX expects billings of $122-$133 million. The revenue is expected to be $82- $90 million. The guidance does not assume any unplanned holiday shopping/marketing budgets being released in 4Q, which could cause an upside to numbers if they materialize. EBITDA is expected to be $4-$8 million, bracketing the $6.6 million consensus. The company will report results on 29th February 2024.

While economic conditions remain choppy, the company's recent results have provided some optimism for investors. CDLX had the second consecutive quarter of positive operating cash flow at $1.2 million in Q3 2023 and first quarter of positive adjusted EBITDA of $3.9 million. I believe that liquidity concerns have been a major overhang for CDLX, as investors place more scrutiny on small-cap growth stocks. On the balance sheet, CDLX ended Q3 with $90.1 million in cash and cash equivalents and had $4 million of unused available borrowings underline of credit. CDLX's average cash burn over the past four quarters has been $12 million every quarter, but since the company has now posted positive cash flow from operations over the past two quarters, I am confident that CDLX has enough liquidity to execute on its core business.

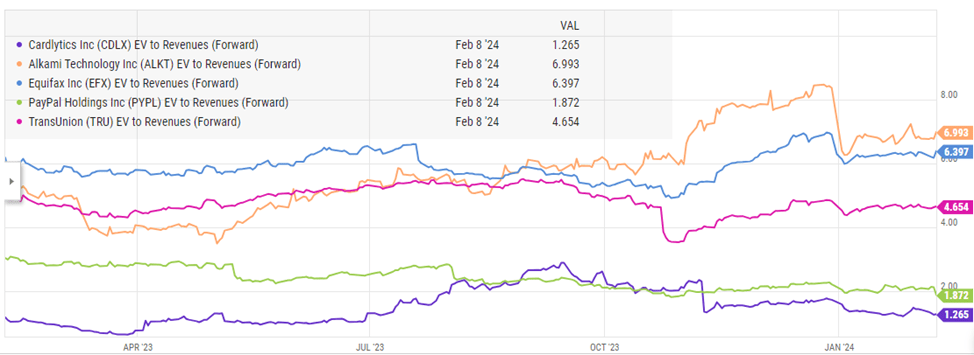

CDLX currently trades at an EV/revenue multiple of ~1.3x FY24 forward estimate, a discount to a peer group of FinTech peers that leverage data to create a competitive moat and/or have significant exposure to the positive trends in digital payments and banking. I believe it is appropriate that CDLX should trade at a modest discount to its comp group average, given its relatively smaller scale and experimental nature in addition to macro headwinds working against the company. That said, the company has diversified its business by expanding e-commerce relationships and acquiring Bridg and Dosh. In my view, this diversification created a more robust business that will be able to post robust growth as the economy recovers and consumer spending improves. However, in the near-term I believe macro uncertainty and high inflation will have an adverse effect on the advertising budgets as well as consumer spending in the next 6-9 months. If the multiple continues to trade down and goes below 1x forward EV/Revenue, similar to where the stock traded in first half of 2023, the stock might be attractive to buy just on a pure valuation basis. However, currently, I believe it is best to stay on the sidelines since there are no catalysts in place right now for the stock price to go up. I assign a hold rating to the stock.

YCharts

Cardlytics utilizes purchase data from more than 2,000 financial institutions to assist marketers in reaching their target audience effectively measure their advertising investments. Unique purchase data sets Cardlytics apart from its competitors and provides a comprehensive solution for advertisers. However, the company's billings and revenue figures have been light in the recent quarters, and it is clear that the macro pressures are currently weighing on the company, although the company has posted better margins after adjusting cost structures. I believe the top-line pressures due to macro headwinds would persist in the near-term, which is why I am staying on the sidelines for now. I would be keeping a close eye on the topline as macro conditions improve to make a change to my rating. Currently, I assign a hold rating to the stock.