Sundry Photography

Sundry Photography

I rate CBRE Group, Inc. (NYSE:CBRE) stock as a Buy.

Previously, I touched on CBRE's latest investment and the company's financial prospects in my September 27, 2023 update. With this latest article, I review CBRE's most recent quarterly financial performance and its management guidance. CBRE's Q4 2023 results exceeded expectations, and the company's guidance implies that a significant earnings turnaround is in the cards this year. New acquisitions could also boost the company's growth prospects. This explains why I continue to be bullish on CBRE as a potential investment.

CBRE published a press release disclosing its Q4 2023 financial results on February 15, 2024, before trading hours. The company's key financial metrics for the latest quarter surpassed expectations.

Revenue for CBRE expanded by +14% QoQ and +9% YoY to $8,950 million in the fourth quarter of 2023. Its actual Q4 2023 top line was +6% above the Wall Street analysts' consensus sales estimate of $8.44 billion.

The company's non-GAAP adjusted EBITDA and EPS for Q4 2023 turned out to be +14% and +17% better than the market's consensus forecasts, respectively, as per S&P Capital IQ data. CBRE's normalized EBITDA rose by +10% YoY to $737 million in Q4 2023, while its normalized EPS increased by +4% YoY for the most recent quarter.

The Change In CBRE's Operating Earnings Mix Over Time

CBRE's Q4 2023 Earnings Presentation Slides

The key factor that contributed to CBRE's Q4 2023 results beat was the company's success in optimizing its earnings mix for the past decade or so as detailed in the chart presented above. The company has successfully lowered its proportion of operating income generated by "transactional" businesses from 68% in 2011 to 40% for 2023.

At its Q4 2023 earnings briefing, CBRE emphasized that its:

"resilient businesses continued their strong growth" in Q4 2023, which "partly offset market-driven revenue declines in businesses that are sensitive to interest rates and debt availability."

CBRE's Global Workplace Solutions or GWS segment, which offers "resilient and non-transactional" facilities management and project management solutions, saw its net revenue grow by +13% YoY to $2,363 million in Q4 2023. In comparison, net revenue for the company's "transactional" Capital contracted by -12% YoY to $631 million for the latest quarter, as highlighted in its Q4 earnings presentation slides.

Investors had a positive view of CBRE's financial results for the latest quarter as evidenced by the company's post-results share price performance. CBRE's shares jumped by +8.5% to close at $94.30 on February 15. Apart from its Q4 2023 results beat, the market was likely to have been impressed by CBRE's fiscal 2024 guidance detailed in the next section.

The company issued its FY 2024 financial guidance in tandem with its Q4 2023 results release. Specifically, CBRE anticipates that it will turn around from a -33% drop in its FY 2023 normalized EPS to record a +16% growth in non-GAAP adjusted EPS this year as per the mid-point of its guidance. Its FY 2024 normalized EPS guidance was also better than the sell side's consensus bottom line projection of $4.39 per share.

The continued growth of the Global Workplace Solutions or GWS segment's and a recovery in the Capital Markets business are expected to be the main earnings expansion drivers for CBRE in FY 2024.

CBRE shared at the company's latest fourth quarter earnings call that it witnessed a "record pipeline conversion to new GWS (Global Workplace Solutions) contracts during Q4 (2023)" that will be largely recognized in 2H 2024 revenue. I have previously cited Jones Lang LaSalle's (JLL) management comments that "only three in 10 companies currently outsource their property management" in my February 2, 2023 article for JLL. As such, it is not surprising that CBRE's GWS segment is experiencing robust growth as the current level of property management services outsourcing is still low. In specific terms, CBRE is guiding for a "mid-teens" percentage increase in its operating income for the GWS segment for the current fiscal year.

On the other hand, CBRE expects its Capital Markets business to deliver a "mid-single digit" percentage growth in revenue this year as per its guidance. At its Q4 results briefing, the company noted that "investor sentiment has improved" thanks to a "better interest rate outlook" which is positive for its Capital Markets business' prospects. Goldman Sachs (GS) has also predicted in a February 2, 2024 research commentary that "capital markets activity will increase" this year on the basis that rate cuts "could boost IPO activity and corporate debt issuance." Notably, the YoY fall in net revenue for CBRE's Capital Markets business has already narrowed from -35% for Q3 2023 to -12% in Q4 2023, implying that the Capital Markets business is on the path of recovery.

To sum things up, I am of the opinion that it is realistic to expect CBRE to report strong bottom line growth in the current year, considering the outlook for its Capital Markets business and GWS segment.

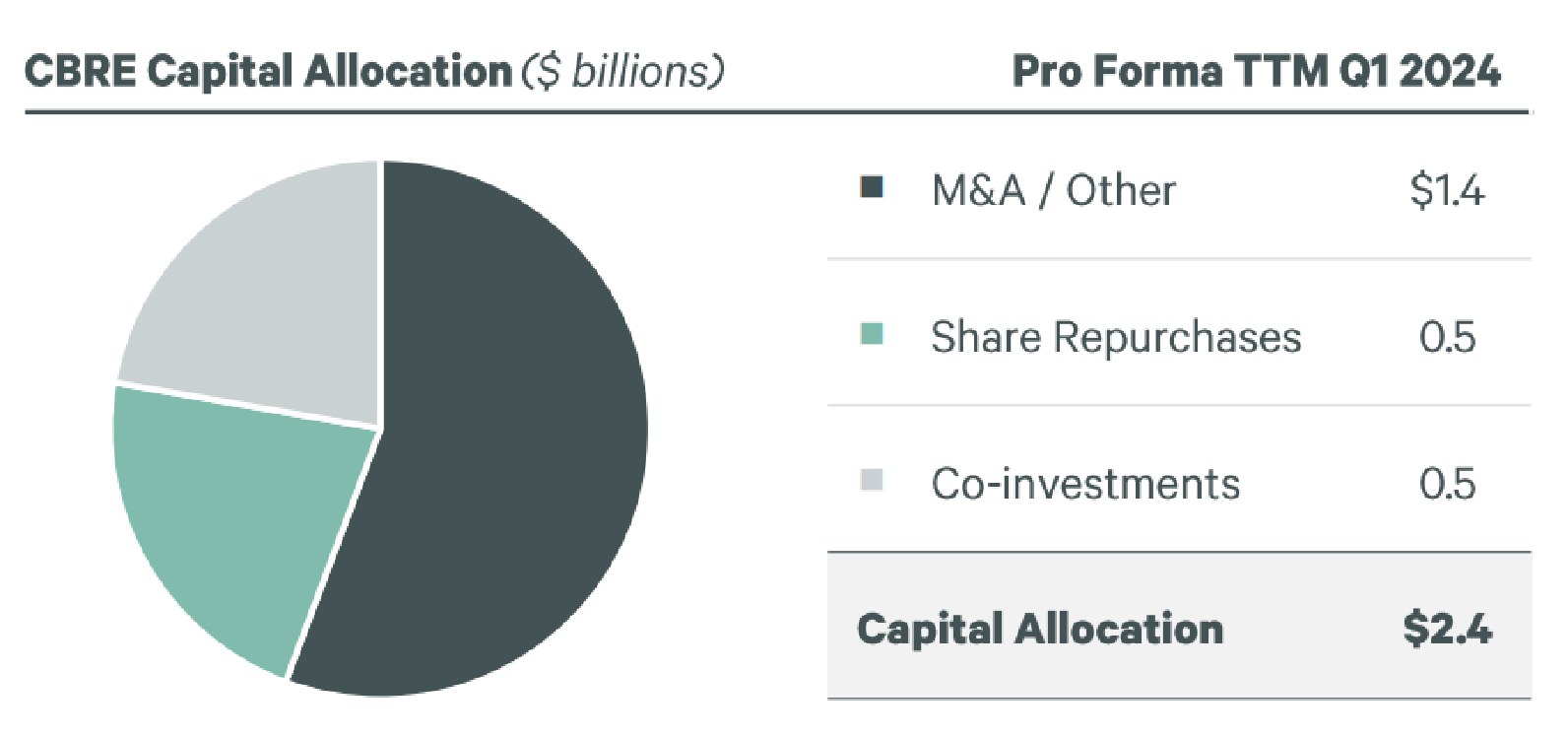

In the past 12 months, close to 60% of CBRE's excess capital has been allocated to Mergers & Acquisitions or M&A, as indicated in the company's Q4 2023 earnings presentation.

CBRE's Capital Allocation In The Last 12 Months

CBRE's Q4 2023 Earnings Presentation Slides

There is a good chance that CBRE's actual FY 2024 financial performance might even exceed expectations thanks to a boost from inorganic growth initiatives.

Firstly, CBRE highlighted at its Q4 2023 results call that the company's capital allocation this year is likely to be tilted "more towards M&A" just like last year because it is "seeing a greater ability to transact as sellers are more willing to meet our value expectations." This implies that the probability of the company executing on value-accretive M&A deals has increased, as the deal making environment becomes healthier.

Secondly, acquisitions could potentially drive a further optimization of the company's earnings mix. In its fourth quarter earnings presentation, CBRE revealed that the acquisitions that the company did in the last 12 months were "mostly in our resilient businesses." As such, CBRE's percentage of operating earnings derived from "resilient and non-transactional" businesses might continue to increase going forward on the back of new M&A deals.

Thirdly, CBRE is underleveraged at the moment, considering that its end-2023 net debt-to-EBITDA ratio of 0.7 times is substantially lower than the high-end of its net financial leverage target at 2.0 times. Therefore, CBRE has room to increase its financial leverage to a more optimal level by engaging in accretive acquisitions.

I am impressed with CBRE's better-than-expected Q4 2023 results, its positive financial guidance for FY 2024, and its inorganic growth potential. More importantly, the stock is still undervalued. CBRE's PEG or Price-to-Earnings Growth is calculated to be 0.75 times or below 1 based on a consensus next twelve months' normalized P/E of 23.8 times and a consensus FY 2025-2026 normalized EPS CAGR forecast of +31.6% as per S&P Capital IQ data. As such, I keep my Buy rating for CBRE intact.