JHVEPhoto/iStock Editorial via Getty Images

JHVEPhoto/iStock Editorial via Getty Images

Whether from a dividend or distribution, when a 9% yielder surfaces from research, it requires more investigation. Further scrutiny into CrossAmerica Partners LP (NYSE:CAPL) resulted in the verdict this relatively unknown, small MLP is a candidate for income seeking investors. As a distributor of fuel to gas stations, demand for CAPL's service is relatively inelastic. Still, management is key to profitably distributing that fuel, given oil's inherent volatility. With CAPL, management's vested interest in success underlies this recommendation. The MLP currently yields 9.6%, having generated the same quarterly distribution amount for the past 5 years. Growth of that distribution, as well as unit price appreciation, will be muted. However, if generating income is a priority, CAPL's robust and reliable distribution is worth consideration. Building incremental positions is recommended: Seasonality suggests initiating a position now will benefit from summer driving; on the other hand, a slowing economy and/or gas prices gyrating could impact the MLP's unit price and offer cheaper buying opportunities. Timing aside, CAPL is underappreciated for its high but consistent distribution yield that is backed by ample cash flow.

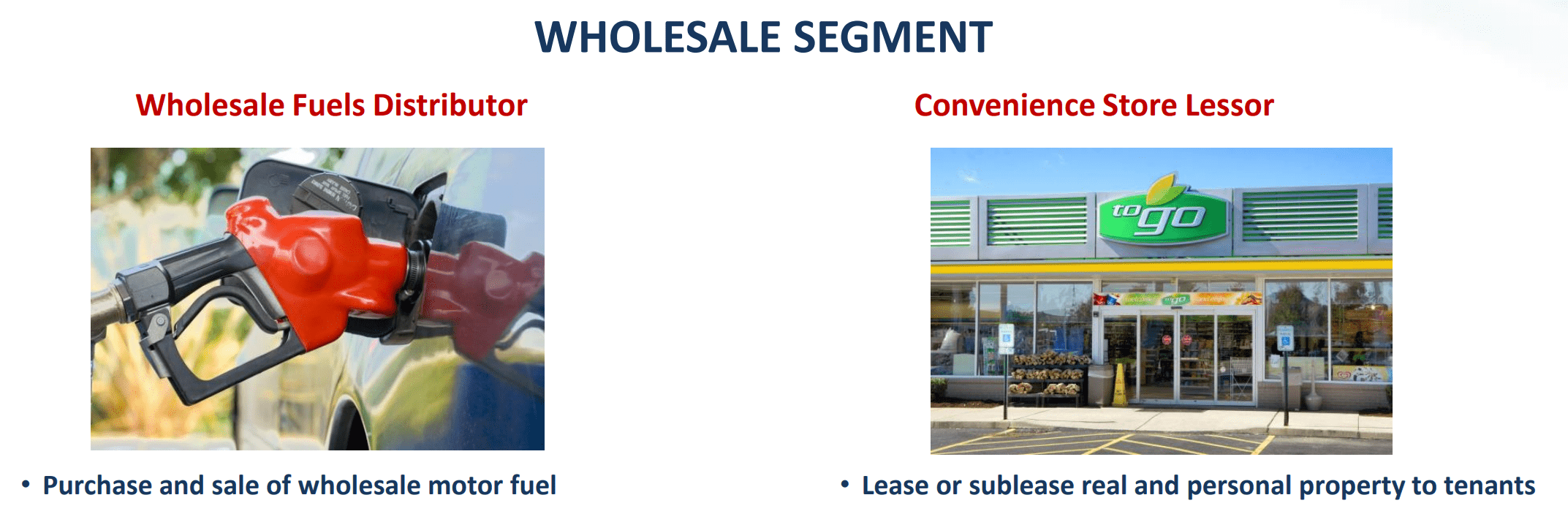

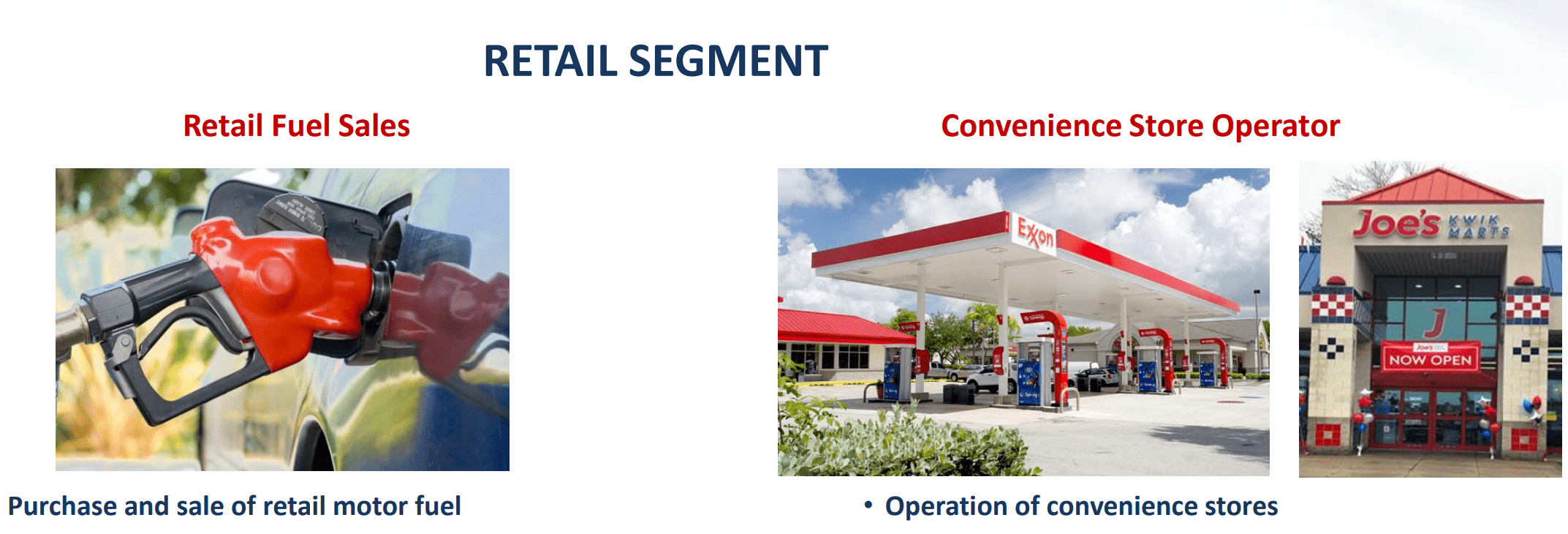

CrossAmerica Partners LP is the middleman between "Big Oil's" production and the millions of customers filling their cars and trucks at gas stations. The partnership makes its money by distributing the motor vehicle fuel produced by Exxon Mobil (XOM), BP (BP), Chevron (CVX), Sunoco (SUN), Valero (VLO), Gulf (owned by CVX), Marathon (MRO), Phillips 66 (PSX) and Citgo (owned by the Venezuela government). The fuel is supplied to independent dealers, tenants/dealers who lease their property from the partnership, and locations owned or controlled by the company. Below is an overview of CAPL's operations:

CAPL Investor Presentation

CAPL's Investor Presentation

CAPL distributes fuel to over 1700 locations across 34 states, primarily in the east and mid-west. Long-term and exclusive distribution contracts characterize the relationship with 643 independent dealers and the 451 lessees, who also pay rent to the partnership. Company sites, numbering around 675 (as of last March) are a focus for future growth, as CAPL works to convert lessee dealers to more profitable company operated sites. In addition to making a profit on the fuel it distributes and rent received, the 250+ convenience stores owned by CAPL contribute lucratively to the partnership's bottom line.

Any deliberation of CrossAmerica requires understanding the role of founder, Joseph V. Topper, Jr. An analogy to Michael Dell's return to Dell Computer (DELL) after stepping away as the #1 decision maker would be a stretch, but, the importance of Mr. Topper's role to CAPL cannot be overstated. As a young 30-something, Topper bought his family's retail fuel business in 1987. Five years later, he founded what was then called Lehigh Gas Corporation, the seed company to the IPO that became CrossAmerica Partners in October of 2012. CAPL's initial years trading on the NYSE, when Topper was the CEO and Chairman of the Board, saw the unit price double. Two years later, Topper resigned from the Chairman position and in 2015, stepped down as President and CEO (ringing the closing bell of the NYSE on the final day of his tenure). The announcement of Topper's departure is in synch with the MLP's price descendent downward. A year after his exit, CAPL had given up all of its initial gains by the end of 2016. Four years later, after further floundering by CAPL unit price and a distribution cut, Topper returned to the Chairman's role, immediately ending the drain of incentive distribution rights ((IDRs)) and stating the following:

At this time, we anticipate maintaining our current distribution policy, distribution coverage and leverage ratio targets that have been outlined over the past few quarters.”

CAPL has honored these comments made in November of 2019. A good test came during the Covid-impacted time period: Despite historic lows in the price of oil and CAPL's unit price, as well negligible demand from reduced driving, the partnership maintained its distribution. Topper's 30+ years of experience navigating gas price fluctuations as a fuel distributor, as well as managing the underlying real estate required by a gas station, have been crucial to CAPL's success.

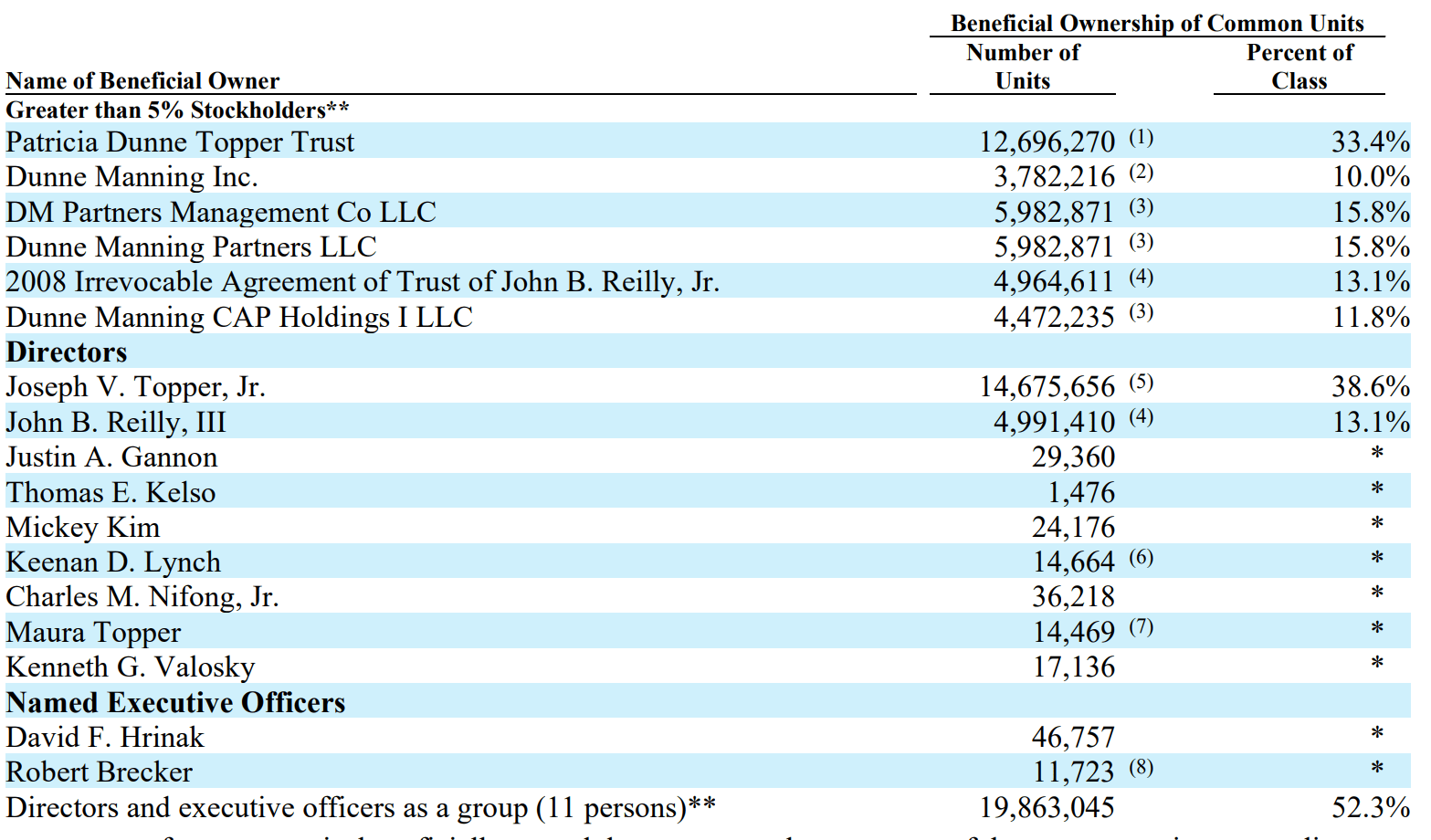

In addition to Joe Topper, who owns ~39% of the partnership's units, other insiders have significant stakes in CAPL. Vice-Chairman (John B. Reilly) owns 13% of the partnership's common units and the involvement of other Topper-related entities are listed below:

gurufocus.com

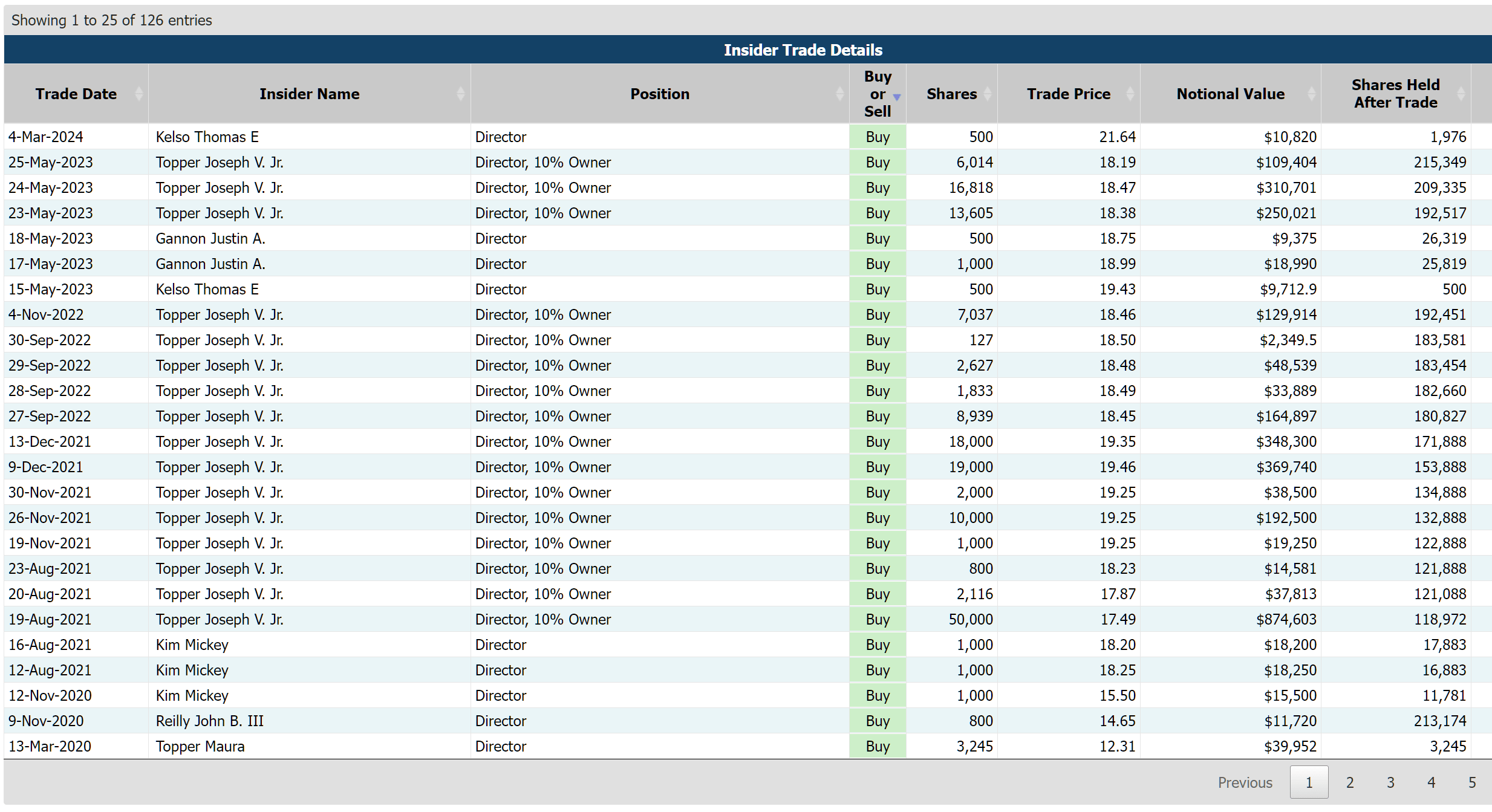

Some see these 'beneficial' owners subjugating unitholders to their decisions. Alternatively, CAPL unitholders know management shares a vested interest in the partnership's distribution policy continuing, along with a satisfactory unit price. Importantly, SEC Form 4 filings detail Topper's buying when CAPL's unit price drops. Last year, significant insider buying by Topper took place twice when CAPL was trading around $18/share price, a pattern seen in 2022 and prior years. The Form 4 filings shown below suggest other CAPL board members and executives are confident in the MLP's future, as well.

gurufocus.com

For investors concerned if Joe Topper isn't involved with the day-to-day decisions, Topper's daughter Maura Topper was appointed as the company's CFO in August 2021. Deeply familiar with the organization and possessing a strong accounting/business background, CAPL's financing approach has improved since taking on the role. Most likely, she's the #1 candidate to lead the MLP when Joe Topper decides to lessen his involvement.

Having 51.6% of the outstanding units controlled by decision makers vested in the partnership's success, aligns their interests with public unitholders. In addition to significant insider buying, the 2020 decision to eliminate IDR's (after Joe Topper returned) offers further evidence of an alignment with unitholders. CAPL's $830M market cap is small compared to better known energy MLPs, such as $51B Energy Transfer LP (ET) and $62B Enterprise Products Partners LP (EPD). This size, along with its ownership structure, offers investors a tighter 'partnership' with those in control. Stakes by Citadel and Blackstone's Steve Schwarzman suggest confidence in the Toppers and CAPL's other beneficial owners

Variations in CAPL's reported revenues and earnings reflect crude oil's price changes. Last year is a good example: The average WTI spot price went from $94.90/barrel in 2022 to $77.58/barrel in 2023, a decrease of 18%. In turn, CAPL's revenues were down 12% and its operating income declined 8% in 2023. However, the MLP's 2% increase in gross profit reflects management's ability to navigate oil's volatility.

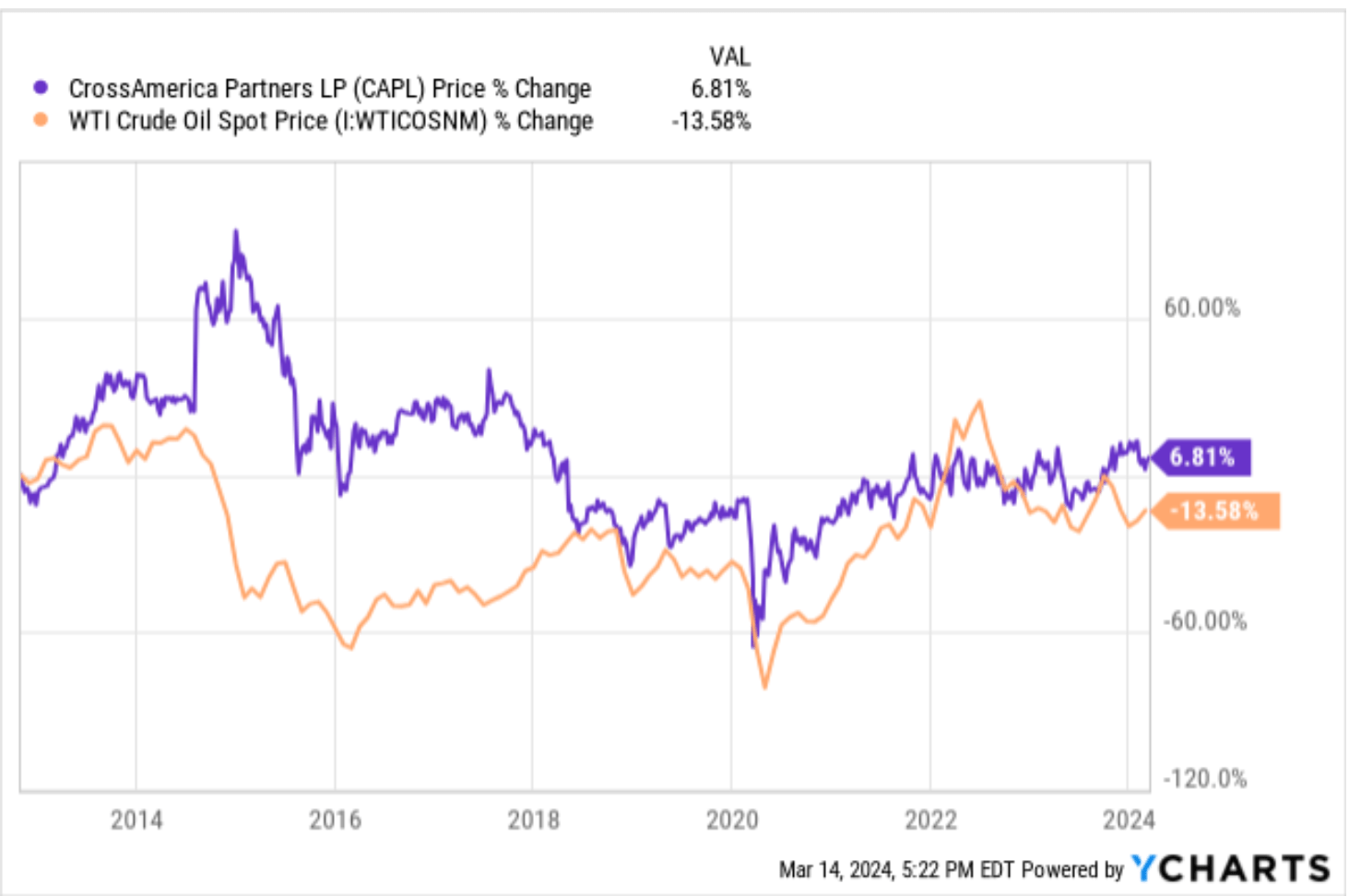

Oil's fluctuations can be reflected in CAPL's trading on the NYSE, as well. The graph below shows how CAPL's unit price has changed versus WTI spot price. Despite, the challenge of oil's price swings, CAPL has annualized a total return of 8.6% since its IPO in 2012.

YCharts.com

CAPL's performance, at times, has reflected acquisitions and distributions that were too aggressive. However, CAPL seems to have learned from its years when this aggressive approach resulted in too much debt and a 16% distribution cut in 2018. Last year, CAPL did not close on any major acquisitions. Instead, the partnership paid down debt ($9M) and reworked its revolving credit agreement in April, getting the green light from Citizens for $925M. As the year ended, it's leverage ratio was inline with this credit agreement--a key to sustaining the distribution--and amended terms extended its maturity to 2028. Strategic use of interest rate swaps helped the effective interest rate be a manageable 4.9% as of 12/31/23.

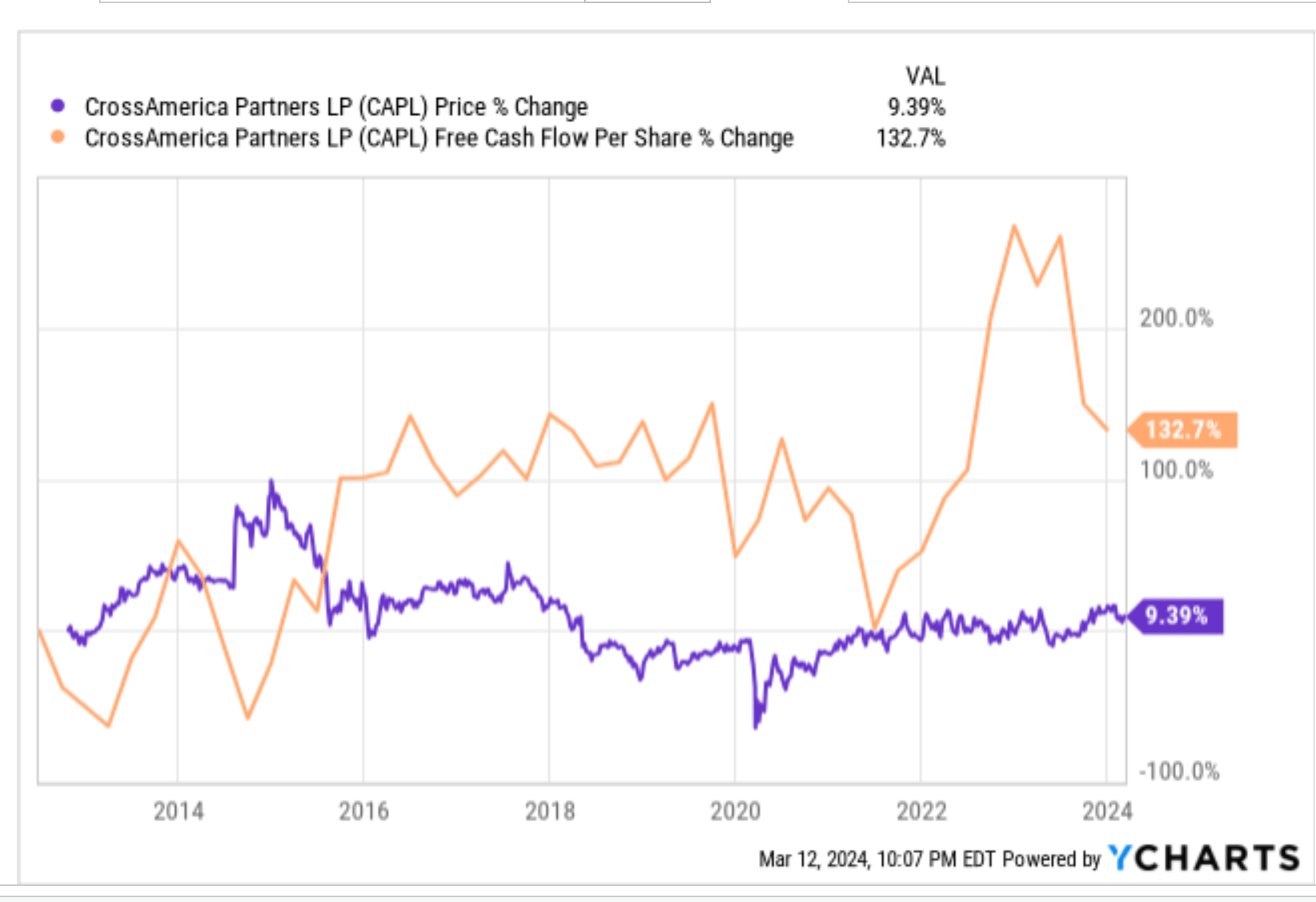

With financing solidified, a margin of safety exists that facilitates management's priority to cash flow generation, regardless of fluctuations in revenues and earnings. Given cash flow is key to the current distribution remaining intact, the financing arrangement is supportive cushion. The graph below shows CAPL's cash flow is ample to maintain the current distribution, an amount that has been sustained since Joe Topper's took back control.

YCharts

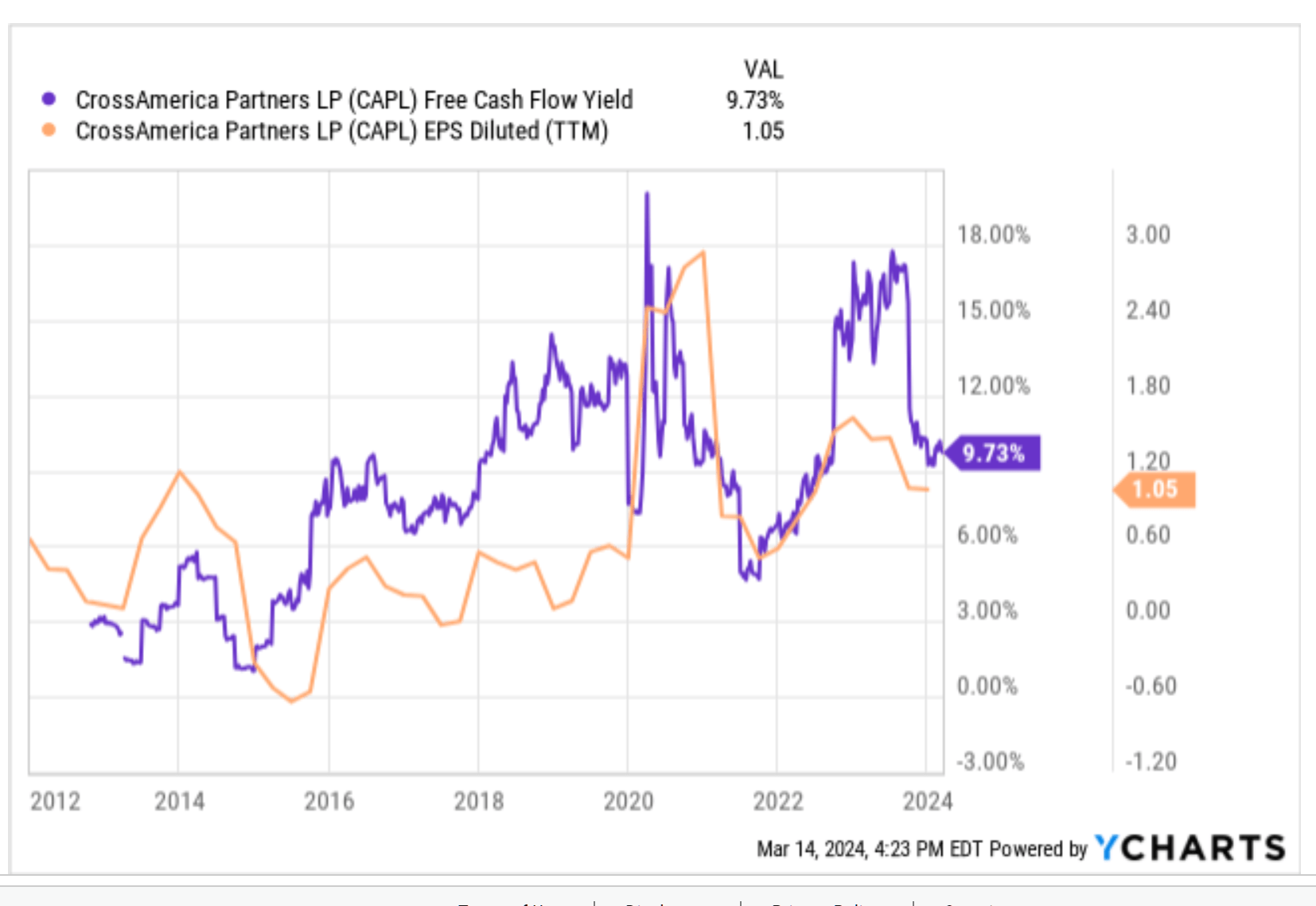

With $82M in free cash flow on a trailing 12-month basis and a market cap of $843M, CAPL's FCF yield is 9.8% and above is 13-year median of 8. From an earnings perspective, the partnership's 12-month trailing earnings-per-share (as of 12/31/23) was $1.05, which translates to an earnings yield of 4.7% (using CAPL's price on March 14th). Both measures are pictured below and suggest a sustainable distribution. Additionally, CAPL's distribution coverage (distributable cash flow/distributions paid) of 1.46 is in line with what's required by its revolving credit agreement and fits its historical pattern.

YCharts

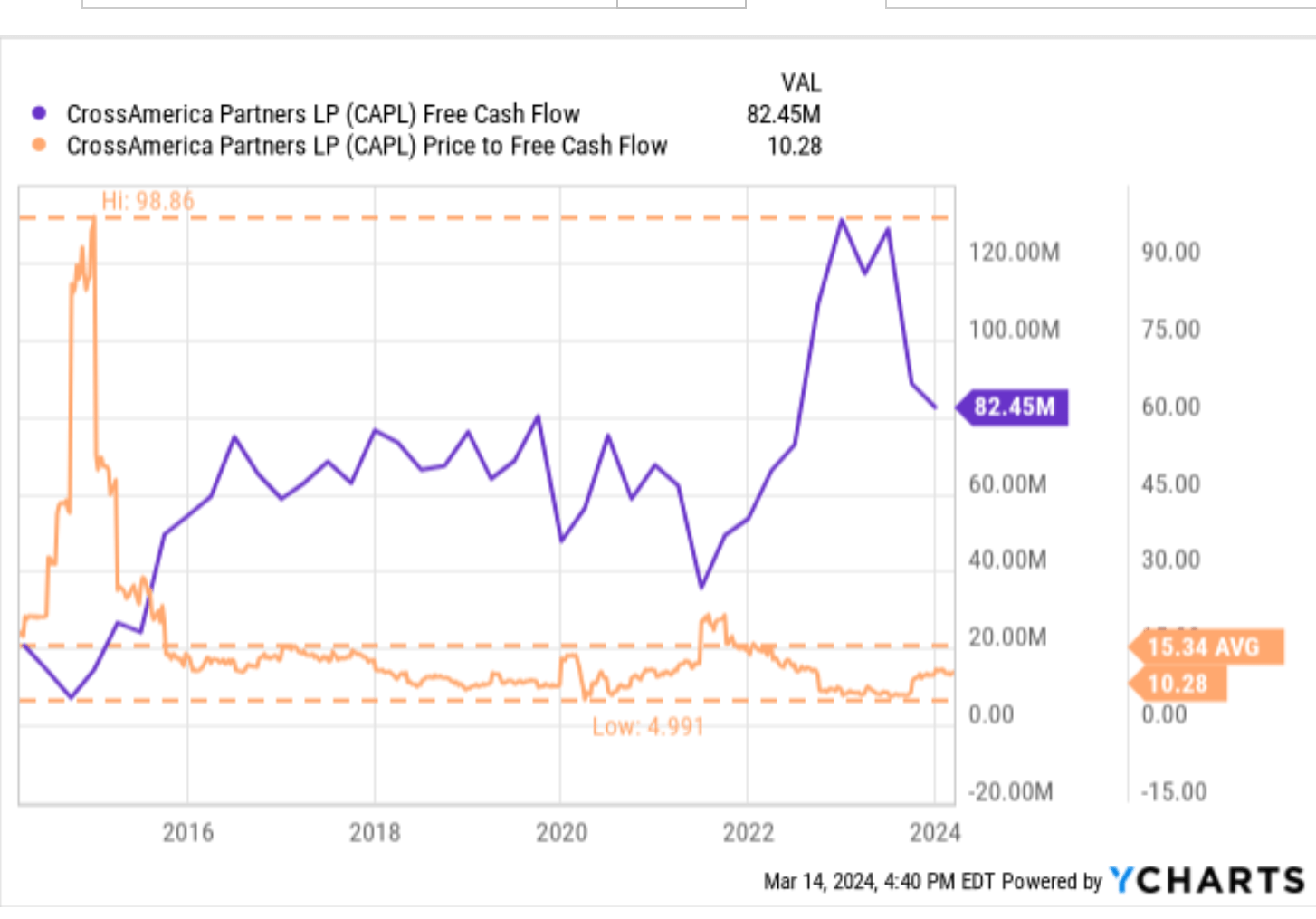

To understand CAPL's current price in relation to its cash generation, the graph portrays what investors have paid for a dollar of cash flow over time. The price to free cash flow, or P/FCF ratio, is a more relevant metric than the P/E ratio for gauging the CAPL's unit price in relation to its distribution. Currently, CAPL sits below its 13 year average of 15x. Based on its past trading pattern, investors aren't overpaying for CAPL's distribution at the current level of 10x P/FCF.

YCharts

CrossAmerica isn't right for someone wanting strong total return potential; it is right for someone seeking income. Price appreciation is possible, especially when gas prices climb higher, but volatility from changing prices at the pump needs to be expected. If that is tolerable, CAPL's 9.6% distribution yield can be a reliable source of income thanks to the company's cash flow. Insiders control over 50% of the outstanding shares, making their interests aligned with unitholders. A deep dive into CAPL's history and future plans, confirms the power of that alignment. Finally, if worried about the impact of electric vehicles, know that CAPL's capex plans include adding charging stations to their company owned sites, especially those with convenience stores whose sales could benefit while cars get charged. In sum, superior total return is an unrealistic expectation; but, a reliable, robust distribution is a reasonable assumption.