JOHN AMIS/AFP via Getty Images

JOHN AMIS/AFP via Getty Images

It’s been about three months since I wrote my bullish piece on Byrna Technologies Inc. (NASDAQ:BYRN), and in that time, the shares are up about 119.5% against a gain of about 9.3% for the S&P 500. For those of you who took my advice and bought this name back then, you’re welcome. I’ll send you my Christmas wish list, because it’s never too early. Anyway, the company has recently announced earnings, and I think it’s fair to suggest that the market liked what it saw. Anyway, there’s a very obvious positive relationship between price and risk, so the higher the price, the higher the risk of the investment. Put another way, this might be a great investment at $5.50, but it may be time to take chips off the table at $12.05. I’ll decide whether or not to buy more, hold, or take my chips off the table by reviewing the financials, and going through some of the highlights of the recent earnings call. I also want to write briefly about the two significant challenges the company overcame in 2023.. Finally, I’ve covered the growth story, the so-called “tailwinds” here extensively in previous articles, so if you’re truly interested in such things, I’d recommend my earlier work on Byrna.

My writing has been described by some of my younger readers as “a bit extra”, and I understand that. It’s a challenge to concentrate on some element of an analysis when some goofy writer is going on about proper spelling or some similar inanity. For that reason, I put a thesis statement at the beginning of each of my articles, and these give you the opportunity to understand my thinking in a single paragraph. This gives you the opportunity to then flee before things just get too cheesy. You’re welcome. So, I’ll be adding to my position in Byrna over the next day or two. There are a few reasons for this. First, financial performance in 2023 was excellent in my view, in spite of two significant challenges. Second, the company is growing international sales. Third, the company is initiating a plan to increase production capacity, and will lead to production of 12,500 launchers per month, up from 10,000 at the moment. Finally, I was impressed by the way the company overcame two significant challenges in 2023. I don’t focus much on the quality of management, because, being a math nerd, I like the stuff that I can measure. That written, I must say that in this case management’s response to these two problems impressed me greatly. I’m comfortable tying up some of my capital with these guys. Thus ends my thesis statement. If you read on from here, that’s on you. I don’t want to read any complaints in the comments section about my bad jokes or correct non-American spelling, because you’ve been warned.

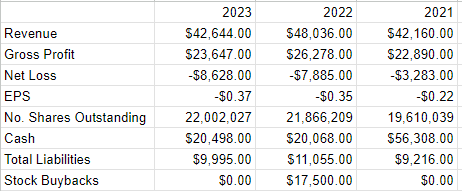

On the face of it, 2023 was not a great financial year for the firm, with revenue, gross profit down by 11.2% and 10% respectively, while the net loss has expanded by 9.4%. Digging a bit below the surface, though, reveals that comparisons to 2022 might not be entirely fair (more on this below) because of the effects of international sales. Specifically, there was a $7.6 million reduction in international sales from 2022 to 2023. This should be expected going forward with this business, because international sales, to police departments for instance, are large but infrequent. Additionally, starting in 2023, the company’s South American sales no longer show up in Byrna’s financial statements, but in those of BYRNA LATAM. See pp. F7 and Note 6 here for more details on this.

Given all of this, and given the challenges the company faced (more on this also below), I’d say that 2023 was actually a fairly good year for the firm, with the fourth quarter being a particular standout.

The thing that impresses me most about the financial results is the significant turnaround of the capital structure that happened in the final quarter of the year. When I last wrote about the business, the cash position had dropped to $13.65 million. One quarter later, and cash is sitting at about $20.498 million, and at the end of December, the cash position was $23 million. The company still has no long term debt, and total liabilities are a hair under $10 million, at $9.995 million. So, using the arithmetical skills not so lovingly beaten into me by the good Sisters at Holy Spirit School, I’m able to work out that as of the end of Q4, the company had 2.05 times more cash on hand than total liabilities, and as of the end of December, that figure had climbed to 2.3 times. This is a very strong balance sheet, especially for such an early growth business.

Taking all for all, I think the year has been a very good one, especially given the two significant challenges the company faced, and subsequently overcame, during the year.

Byrna Financials (Byrna investor relations)

Before getting into the highlights of the most recent earnings call I think it would be worthwhile to write briefly about two challenges the company faced in 2023, and how it overcame those problems. As an investor, I was happy that each of these problems were relatively short lived. In case you’re not familiar with the difficulties, I’ll go through them briefly. First, there were production problems with the very popular Byrna LE. This product was launched to wide acclaim in January of 2023, but the product was bedevilled by production problems and quality control issues. These were so severe that the company stopped taking orders, and this negatively impacted sales for obvious reasons. After “digging deep” with suppliers, these problems were overcome, and the company was able to relaunch the Byrna LE in May. Since then the production and demand for the product have remained strong.

The second, and much more serious problem was that the company was banned from advertising products on social media platforms, including Twitter, Facebook/Instagram, and Google. Coincidentally enough, these three giants decided to ban ads for the company’s product at the exact same time. That was a strange coincidence indeed. Anyway, this ban posed an existential threat, obviously. After a Herculean level of brainstorming, the company decided to settle on the celebrity endorsement model. The company signed Sean Hannity, and committed to a multi-million dollar advertising campaign on Hannity’s afternoon drive-time radio show. This propelled the company to a record breaking fourth quarter, as daily sales spiked to $120,000 a day on Byrna | Best Non Lethal Self-Defense Products and $35,000 a day on Amazon. If you want more on this, I wrote previously about how impressions have actually increased since the ban. Finally, the company is adding the likes of Judge Jeanine Pirro, Glenn Beck, and Bill O’Reilly to the list of celebrity endorsers.

As I suggested above, I think the fact that the company overcame these challenges speaks volumes about the quality of management here.

Reading an entire earnings call can be a pain, which is why I break down what I consider to be the most salient information in easily digested bullet points, so you won’t need to bother with all of this pesky reading business. You’re welcome.

Below are what I consider to be the most relevant points raised during Byrna’s year-end earnings call. Before getting into it, I’ll offer a bit of an acronym legend, as some of this can be tiresome if you don’t know what a particular TLA (“three letter acronym”) means. ROAS means “return on advertising spend”, AOV means “average order values.” You’re now equipped to sound like a marketing manager at your next social event, and I’m sure having people think you’re such a person will do wonders for your social life.

Anyway, here are the five key takeaways from the earnings call that I think are most interesting.

The new marketing approach has been a success. For example, in the fourth quarter, daily web sessions jumped to 32,500, up 174% from the 3rd quarter, and a 22% increase from the same period in 2022 before the social media ban.

The company’s ROAS reached 7.5x, and the company is seeing a continuation of this momentum with a 5.9x in the first two months of fiscal 2024. Significantly, these campaigns have been effective at attracting new customers, with first time customer rates soaring to 66.5% of daily orders, an uptick of 11% from the prior year. A new customer can be thought of as an increase in the annuity from future ammunition sales, and the like.

Because the Latin American, and South American sales are reported under LATAM, the company expects the reported international sales number in 2024 will remain depressed. That written, the company expects Byrna LATAM to do $8 million in sales.

Given the success of Byrna Toronto, the company expects to see excellent growth in the Canadian market. This expectation is reasonable given how quickly the product sold out. The company expects to see $1.5 million in sales in the Great White North in 2024, and, in my view, that figure is on the low side. For my part, I’m happy that I’ll finally be able to legally own one of these things.

Given that production bottlenecks have been a problem in the past, I was pleased to hear that the company has initiated a plan to scale up manufacturing facilities, including adding 25% more facility personnel, and opening a second assembly line. The second line is a bit of a head scratcher for me, as the company operates only one shift per day, but I have faith that there’s a logical reason for this move.

In conclusion, I think one of Byrna’s chief challenges is education. There are hundreds of millions of citizens around the world who are concerned about personal safety, but would never own a firearm even if we could. This is because of the myriad of legal, personal, and psychological risks of using one on an innocent bystander or, God forbid, a family member. Add to that the fact that most of us live under legal systems that deny us the right to use lethal force, so the point of whether or not to own firearms is moot. Though the need for personal protection is real, firearms are not an option for millions of people for reasons that are very understandable. The Byrna family of solutions solves this problem well in my view. The challenge is in educating people about the safer way to secure personal safety. Byrna’s solution is perfect, so the only challenge is in getting the word out. In my view, the company is doing a good job at that very thing. For that reason, I’m comfortable adding to my position at current prices.