Joe Raedle

Joe Raedle

I have never been a fan of Beyond Meat, Inc. (NASDAQ:BYND) - the products or the stock. However, I always wanted the company to succeed as I believe Beyond Meat can play a crucial role in transforming the global food industry by finding solutions to long-term threats faced by humanity.

Last August, when Beyond Meat reported Q2 2023 earnings, I warned investors of more pain ahead. On cue, BYND stock has lost more than a third of its value since then. After digesting Q4 earnings, recent developments, and the industry outlook for alternative meat products, I still believe Beyond Meat is a poor investment choice. My bearish stance on BYND is based on three main reasons.

During the pandemic days, plant-based meat sales reached new highs amid a growing enthusiasm for alternative meat options. This enthusiasm has waned today, evident from the lackluster sales of plant-based meat products in recent times. According to research firm Circana, sales of plant-based meat products dropped 21% for the 52 weeks ending July 2, 2023, highlighting the struggles faced by this business sector. The waning demand for alternative meat is the first reason to be bearish on BYND.

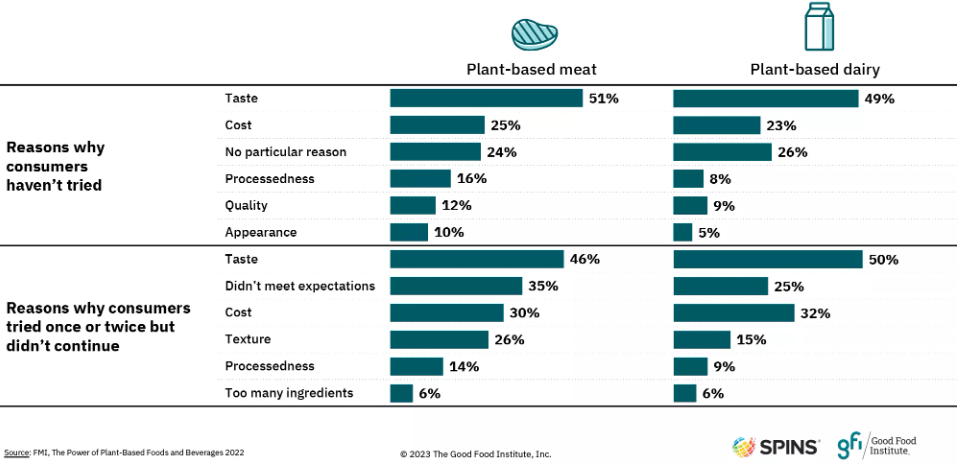

When plant-based meat products went mainstream a few years ago, the likes of Beyond Meat promised to offer products with a similar taste and texture as animal meat. This remains an unmet promise to date. The taste and texture factor is one of the leading reasons why many consumers still find plant-based meats less appealing compared to animal meat.

Exhibit 1: Top barriers to plant-based meat consumption

Good Food Institute

According to the Good Food Institute, more than 75% of U.S. consumers have either tried plant-based meat products or are willing to try them, which is encouraging. What is not so encouraging is that repeat sales of these products have failed to gain traction, which probably comes down to a few major factors including unmet taste and texture expectations. According to Statista, only 14% of consumers purchase meat substitutes regularly.

The high cost of plant-based meat products is another major barrier to the growth of the industry. Not so surprisingly, plant-based meat remains significantly more expensive than its traditional animal-based counterparts. Amid continued inflationary pressures, paying premium prices for alternative meat products that even fail to offer the same taste and texture as animal meat does not sound exciting.

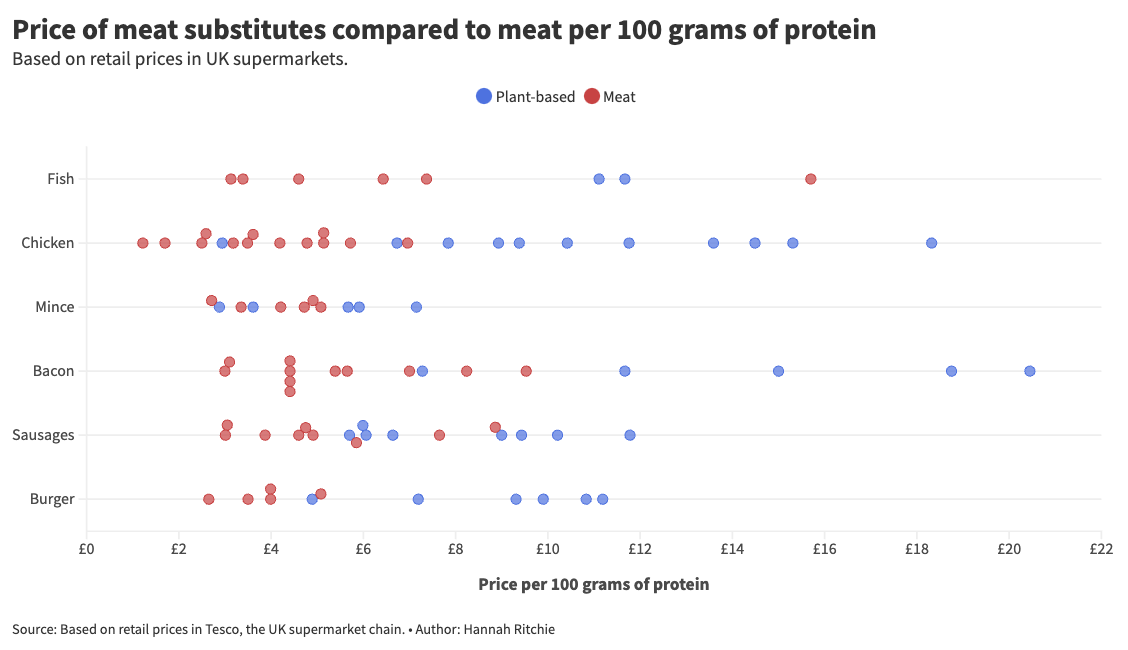

I found an interesting study conducted last year to compare the price differences of plant and animal-based meat in the United Kingdom. Interestingly, the author of the study compared the prices based on the required weight of meat per 100 grams of protein.

Exhibit 2: Price of meat substitutes compared to meat per 100 grams of protein

Sustainability by Numbers

It is crystal clear that animal meat is substantially cheaper than plant-based meat today. Even more interestingly, plant-based meat options that stood any chance of competing with conventional meat were Tesco's unbranded mince and sausages products - not the meat options from well-known brands such as Beyond Meat.

With inflationary pressures expected to persist in the foreseeable future, I do not see the demand for plant-based meat picking up meaningfully.

If we take a long-term perspective on the demand for alternative meat, I think we can all agree that demand will eventually pick up. However, that does not necessarily mean Beyond Meat will turn profitable - or even exist - when it happens. More on this in the next few segments.

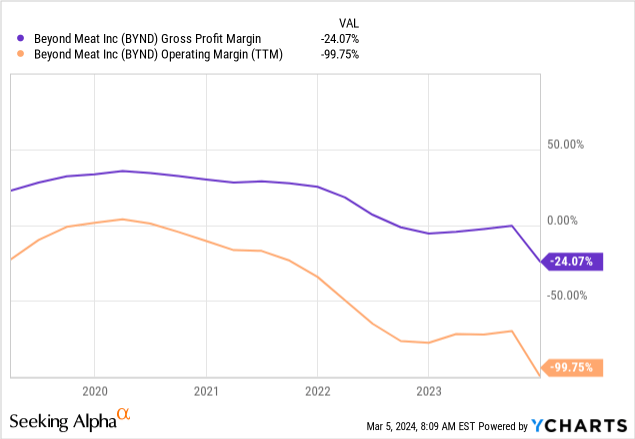

Beyond Meat's continued inability to make progress toward profitability is the second reason to be bearish on the company. The company, in the last couple of quarters, reported losses at the gross profit level itself, which suggests the business will have to grow exponentially - probably at unrealistic levels - for the company to ever turn a profit. The lack of a clear path toward profitability makes BYND an unreliable option to bet on the future of alternative meat, in my opinion. This is because I believe corporate earnings will dictate terms over the long-term stock market performance of a company.

Beyond Meat's products are expensive to produce, and the inflationary environment has added more burden on the company's cost structure. The unfavorable cost structure will continue to make it difficult for Beyond Meat to become profitable at the operating level for many years.

Exhibit 3: Profit margins

Beyond Meat has taken several measures to improve margins, including pricing changes that were rolled out in Q2 2023. The new tiered pricing strategy is a step in the right direction. Consolidating production and investing in more internal manufacturing capabilities could also lead to an expansion in margins in the future. However, I believe it is too early to incorporate such margin improvements into my model.

The increasing competition in the alternative meat industry may further impact Beyond Meat's earnings potential. New players are entering the market today while established brands are fighting for market share. Some large-scale brands entering this space include Nestle S.A. (OTCPK:NSRGF), Tyson Foods, Inc. (TSN), and Kellanova (K). This influx of well-funded companies is driving innovation and product availability - good news for consumers but not so much for current market leaders.

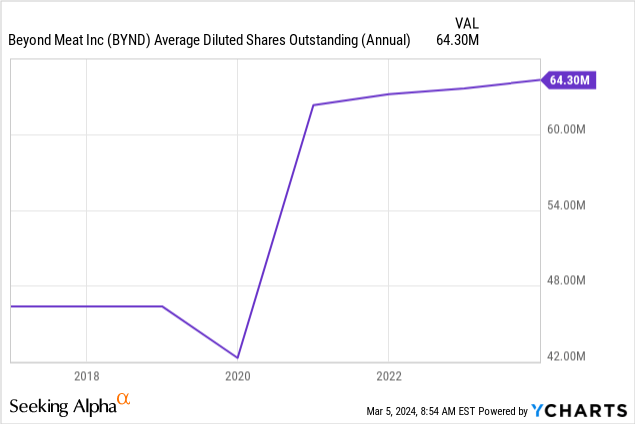

Beyond Meat's cash reserves have dwindled in recent times, which could be an early indication of more shareholder dilution in the long run. From over $1 billion in July 2021, cash and short-term investments have reduced to just below $200 million today while the company continues to experience operating cash outflows. Right on cue, Beyond Meat recently claimed that it may have to raise capital as soon as 2024.

Exhibit 4: Diluted shares outstanding

Ownership dilution is not uncommon in young, fast-growing companies. However, bearing the risk of dilution of a business that is still a long way away from profitability does not seem like an attractive bet to me.

In addition to the shrinking cash balance, Beyond's substantial operating losses and potential limitations in raising debt capital due to its considerable use of debt increase the risk of ownership dilution in the future.

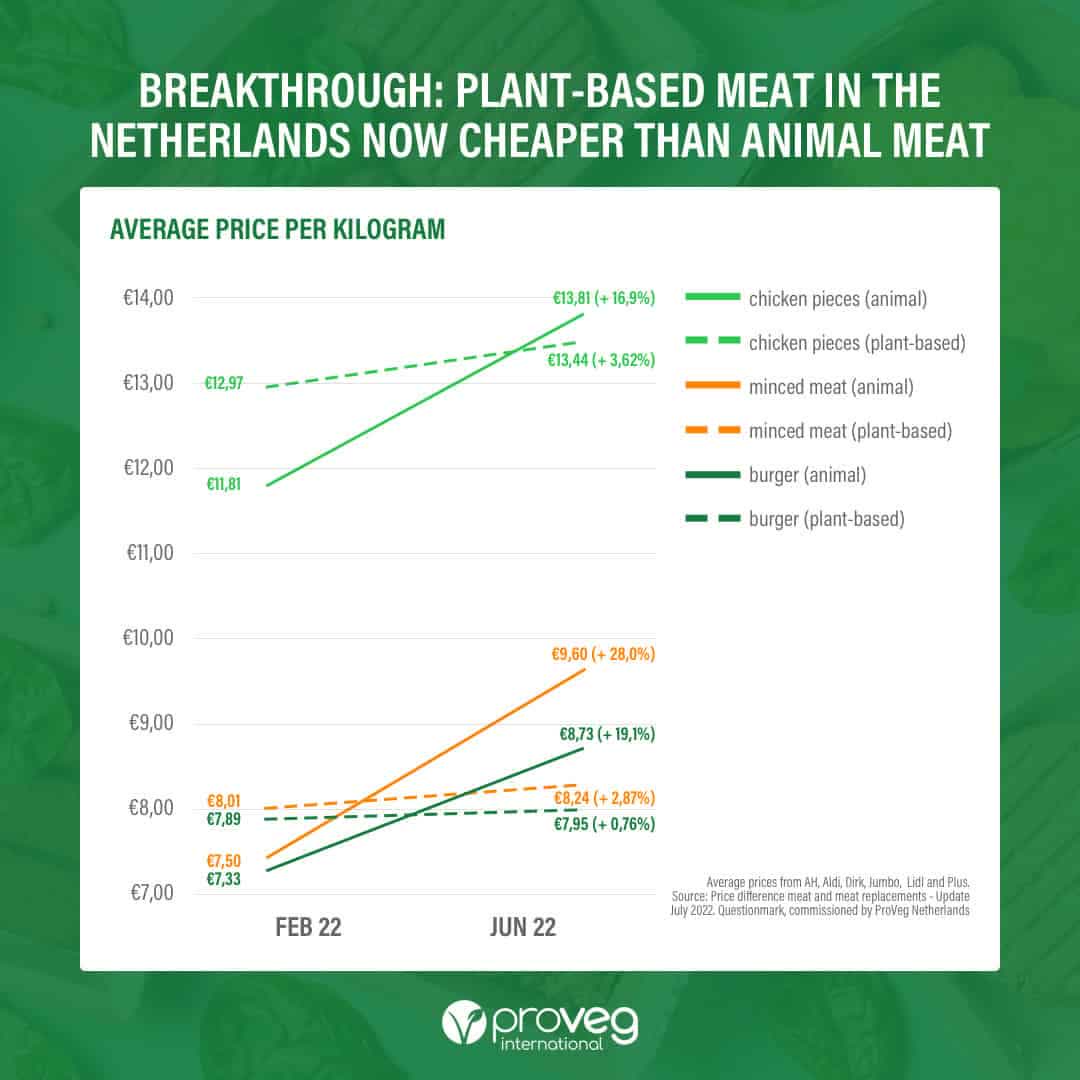

The one thing that could move BYND stock higher in the foreseeable future is the pricing parity between alternative meat options and conventional meat. Although this may sound decades away, in some countries, we are already seeing positive outcomes. For example, in the Netherlands, plant-based meat became cheaper than animal meat in 2022, which was a breakthrough development.

Exhibit 5: Average price per KG of plant-based and animal meat

Vegconomist

In a recent study, Questionmark found that some plant-based meat products are still cheaper than animal meat products in 6 of the 7 major supermarkets in the country.

If we start seeing similar trends in other parts of the world, I believe the market sentiment toward Beyond Meat will change dramatically, resulting in a major spike in BYND stock prices. Even if this happens, I do not believe Beyond Meat will reach profitability any time soon. However, this does make shorting BYND unacceptably risky.

Beyond Meat stock popped following the Q4 earnings release, only to lose ground when the company revealed more dilution may be on the cards. The alternative meat industry is likely to survive and thrive in the long run, but this does not guarantee Beyond Meat a place among the future elites of this business sector. I am reiterating my sell rating for BYND after digesting the recent earnings report.