koto_feja

koto_feja

BrainsWay (NASDAQ:BWAY) is going from strength to strength as market headwinds ease, reporting another quarter of strong growth and reaching profitability. The company also gave strong guidance for 2024, providing further justification for the stock to continue rerating higher. None of this should be surprising for people who have followed my coverage of the stock, but the market and analysts continue to underestimate BrainsWay and the progress it is making.

Coverage of BrainsWay has increased in recent months as the stock price has ballooned, but the stock still seems to be poorly understood.

Treatment Durability

It has been suggested that TMS will not be more broadly adopted as the treatment effects are not durable. While data is relatively limited, TMS has generally demonstrated sustained efficacy over at least a 12-month period post-treatment. This is important as TMS is expensive, meaning the durability of treatments is an important determinant of insurance coverage.

Recurring Revenue

While BrainsWay’s business is selling relatively expensive capital equipment, the company actually has a reasonably large amount of recurring revenue, as close to half of its systems are leased. BrainsWay has stopped giving the figure but in the past, close to 50% of the company’s revenue came from leases.

BrainsWay has historically targeted smaller customers and its systems are a relatively large purchase for them. As a result, BrainsWay’s revenue can be volatile, depending on economic conditions. In particular, BrainsWay was hard hit by COVID and the rapid rise in interest rates in 2022. This situation was exacerbated by an inability to recognize 1 million USD of lease revenue in the fourth quarter of 2022 due to the deteriorating financial condition of one of its largest customers. A situation that was expected to persist in 2023.

Business Model

Some investors have suggested that BrainsWay’s decision not to pursue a pay-per use business model is a disadvantage, but this is unclear, as demonstrated by Neuronetics (STIM). Neuronetics is forced to dedicate significant resources to supporting system utilization, resulting in large losses that are not decreasing with scale. Neuronetics has also failed to innovate, likely because it has been overly focused on generating end market demand. This has allowed companies like BrainsWay and MagVenture to gain market share.

The TMS market is reasonably small though, and it is fair to question whether BrainsWay (and other TMS vendors) are capturing enough of the value they create to reward shareholders.

Market Saturation

While the TMS market is currently small, it has the potential to grow significantly. TMS is chronically underused as a treatment for MDD considering its pros and cons relative to other treatment methods. The number of medication failures required before TMS is eligible for insurance coverage continues to decline though, lowering the barrier for consumers to attempt TMS. Adoption could also be aided by protocol innovations that continue to reduce the time and effort required to receive treatment.

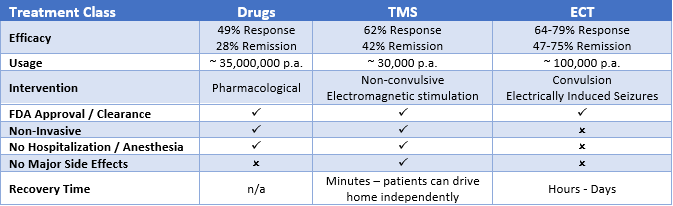

Table 1: Comparison of MDD Treatments (source: Created by author using data from Greenbrook)

TMS is still used almost exclusively for MDD, although usage is growing in OCD. BrainsWay has demonstrated efficacy in helping people to quit smoking, but insurance coverage is needed before this use case becomes meaningful. BrainsWay also continues to trial the technology in new areas, like Parkinson's Disease and post-stroke rehabilitation.

Competition

Investors generally seem concerned about increasing competition, but I wouldn’t rate this as one of BrainsWay’s top challenges at the moment. BrainsWay’s solution is differentiated, both in terms of core technology and indications. It is difficult to maintain differentiation based on just treatment protocol and in many cases, indications. For example, most TMS providers, including BrainsWay, have been quick to offer theta burst. BrainsWay was able to quickly introduce TBS as there was no real barrier to prevent it from doing so. Companies like MagVenture and Neuronetics were also hot on the heels of BrainsWay in OCD.

If anything, recent market headwinds have likely reduced the ability of most companies to aggressively compete for customers. BrainsWay still has a large cash balance though and is now profitable. Neuronetics for one has stated that it is happy to only place around 200 systems a year and is not trying to drive further growth.

There is also a range of competing stimulation technologies, which are often more effective, but also far more invasive. TMS continues to establish itself as an effective alternative for treatment resistant depression and OCD. The bigger threat long-term could be from alternative treatments like ketamine and psilocybin. Progress in this area appears to be slow though.

Share Count

BrainsWay only has around 16.5 million ADRs outstanding, although the fully diluted share count is slightly higher.

The TMS market was hard hit by both COVID and the rapid rise in interest rates in 2022. While the market is beginning to recover, some companies are still struggling. In particular, Greenbrook is one of the biggest providers in the US and it is fighting for survival. This includes reducing headcount, rationalizing marketing spend and the extinguishment of lease liabilities. Actions taken so far are expected to save the company an estimated 23 million USD annually.

Greenbrook's revenue has been stagnant over the past 15 months, the company’s operating profit margin is around -30% and Greenbrook has a large and growing interest burden (over 20% of revenue). Things aren’t quite as grim from a cash flow perspective though. Greenbrook’s total active treatment center count is down 29% over the past 12 months, although the number of treatments performed is only down 16%. This situation is unlikely to impact BrainsWay significantly though, unlike Neuronetics, who has a close relationship with Greenbrook.

Neuronetics continues to focus on system utilization, which is paying dividends, with utilization up 20% YoY in the fourth quarter. Initiatives include trying to increase patient awareness and helping customers implement best practices. System revenue was fairly flat though, coming in at 4.5 million USD. Neuronetics shipped 59 systems, slightly above its plan of 45 to 50 systems per quarter. Neuronetics expects 78-80 million USD revenue in 2024, up around 11% YoY at the midpoint, and 16.7-17.7 million USD revenue in the first quarter, up around 11% YoY.

Figure 1: BrainsWay Units Shipped (source: Created by author using data from company reports and The Federal Reserve)

BrainsWay's fourth quarter results were unsurprisingly strong and are a result of continued momentum internationally and amongst larger customers. BrainsWay shipped a net total of 60 Deep TMS systems, bringing the company's installed base to 1,101 systems, a 25% increase YoY. BrainsWay also shipped 64 OCD coils in the fourth quarter, representing OCD treatment capability on more than 50% of the installed base.

BrainsWay is still looking for the right distribution partner for its smoking cessation coils. Given the strength in the rest of BrainsWay's business and the company's low valuation, success in this area is not necessary.

In December BrainsWay announced a collaboration with a treatment provider based in the western part of the US. The most recent order brought the provider’s installed base up to seven systems, with further expansion planned.

BrainsWay also announced its expansion in South Korea in December. After recent sales the company now has an installed base of over 20 systems in the country.

The SAINT protocol is another accelerated TMS protocol, which could offer higher efficacy and compress treatment times from weeks into a matter of days. A small study by Stanford researchers found that high doses delivered on an accelerated timeline to a targeted area of the brain was highly effective for treating depression. In the trial, patients received treatment 10 times a day for five days, with 79% entering remission by the end of the trial. Electroconvulsive therapy is considered the gold standard for treatment resistant depression, and it only averages a 48% remission rate.

The SAINT protocol was licensed exclusively to Magnus Medical by Stanford University. Magnus Medical raised 25 million USD in 2021 to try and commercialize this treatment. To do this, they licensed technology from Nexstim, which pairs TMS with digital imaging to effectively target the region of interest. The estimated total value of the license agreement was approximately 19 million USD, with an upfront payment of 4 million USD. The remainder was anticipated to come from royalties over a period of five years. Magnus Medical received FDA clearance for the SAINT protocol in 2022. It is unclear how much progress the company has made though and 25 million USD will likely not go far in trying to establish a foothold in the market.

BrainsWay released peer reviewed results for its own accelerated TMS treatment in October. This study showed a 51% remission rate and there was no statistical difference in outcomes between dosing schedules, which varied between 2 and 10 sessions a day. Subjects typically responded within 3-5 days and the durability of treatment was substantial.

While BrainsWay’s technology is already differentiated, the company could further distinguish itself with its rotational field Deep TMS. In standard TMS, only neurons aligned with the coil’s electric field are effectively stimulated. Rotational field TMS aims to stimulate a far greater number of neurons by rotating the electric field. While this could enhance efficacy and reduce variability in treatment outcomes, the method still needs to be validated. It is also possible that this method could lead to more side effects or lower efficacy if inhibitory networks are activated.

Rotational field TMS has already been demonstrated to induce a significantly lower resting motor threshold in both the hand and leg motor cortices. BrainsWay also recently initiated 2 feasibility trials to evaluate Deep TMS 360. One study will test the safety and efficacy of Deep TMS 360 in the rehabilitation of stroke patients. The other study will assess the technology using an accelerated protocol in patients suffering from OCD.

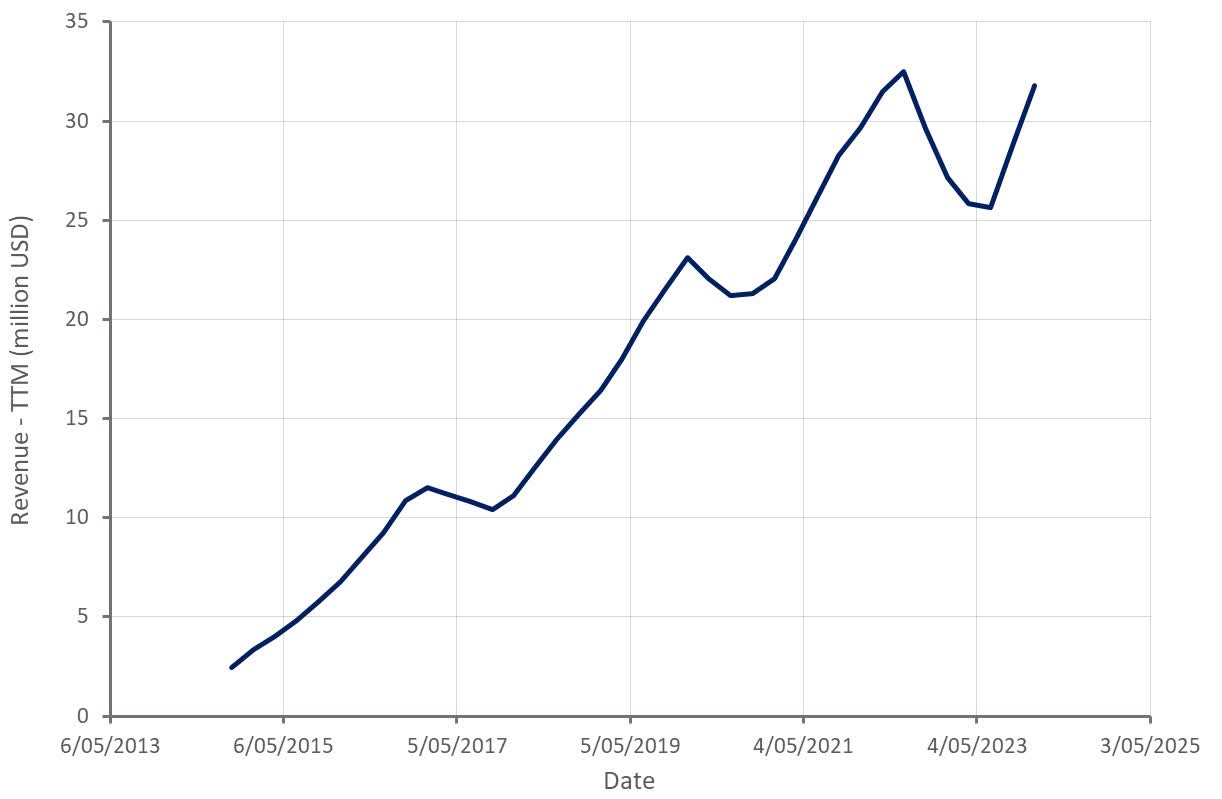

BrainsWay generated 9 million USD revenue in the fourth quarter of 2023, a 50% increase YoY. This strength comes as BrainsWay recovers from the lease issue in 2022 and the demand environment normalizes.

BrainsWay also guided to 37-40 million USD revenue in 2024, representing 16-26% YoY growth. This is noteworthy as BrainsWay has not been providing full year guidance. This suggests a more stable operating environment and growing confidence in the prospects of the business.

Figure 2: BrainsWay Revenue (source: Created by author using data from BrainsWay)

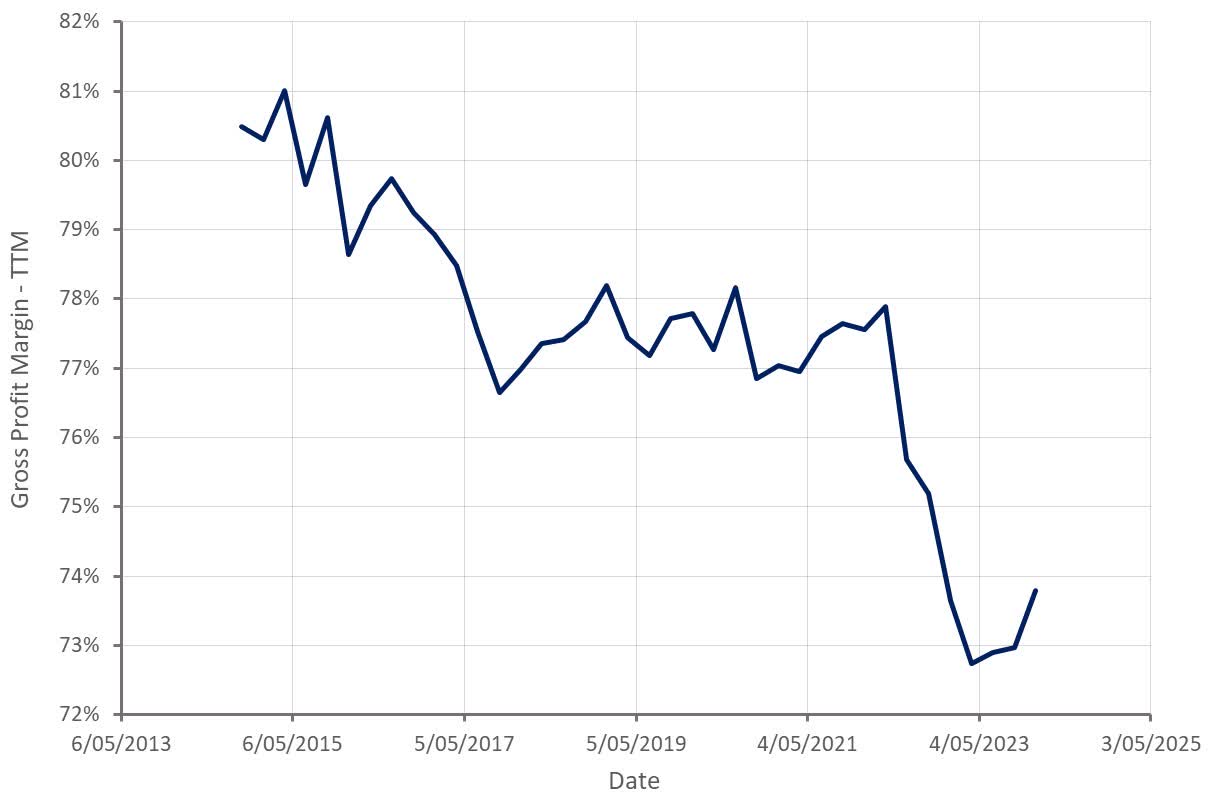

BrainsWay's gross profit margin was 75% in the fourth quarter, a 4% increase YoY. While BrainsWay's margins remain below pre-COVID levels, the result is impressive giving the growing importance of larger customers and the international business.

Figure 3: BrainsWay Gross Profit Margin (source: Created by author using data from BrainsWay)

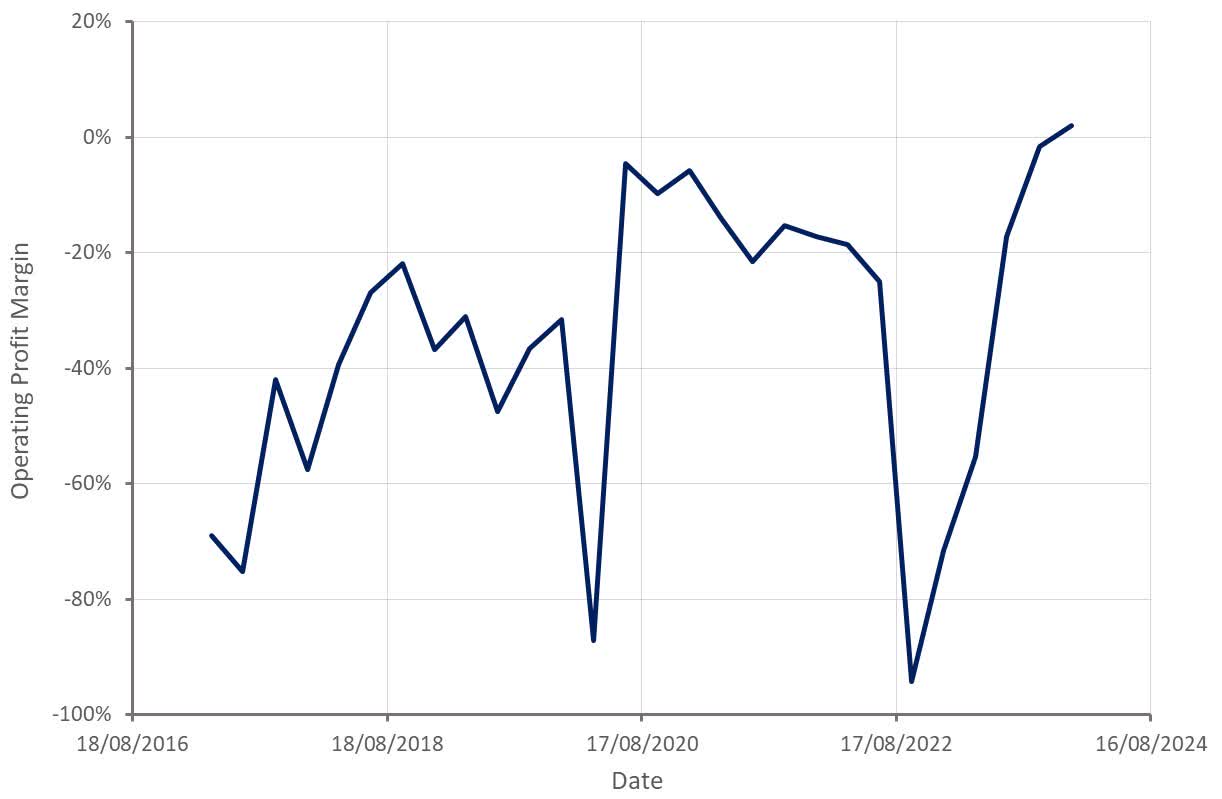

BrainsWay recorded a small profit in the fourth quarter, which comes on the back of ongoing cost discipline and operating leverage. While it is unclear how BrainsWay will choose to prioritize growth versus profitability going forward, the company's profits will likely continue to increase based on revenue guidance.

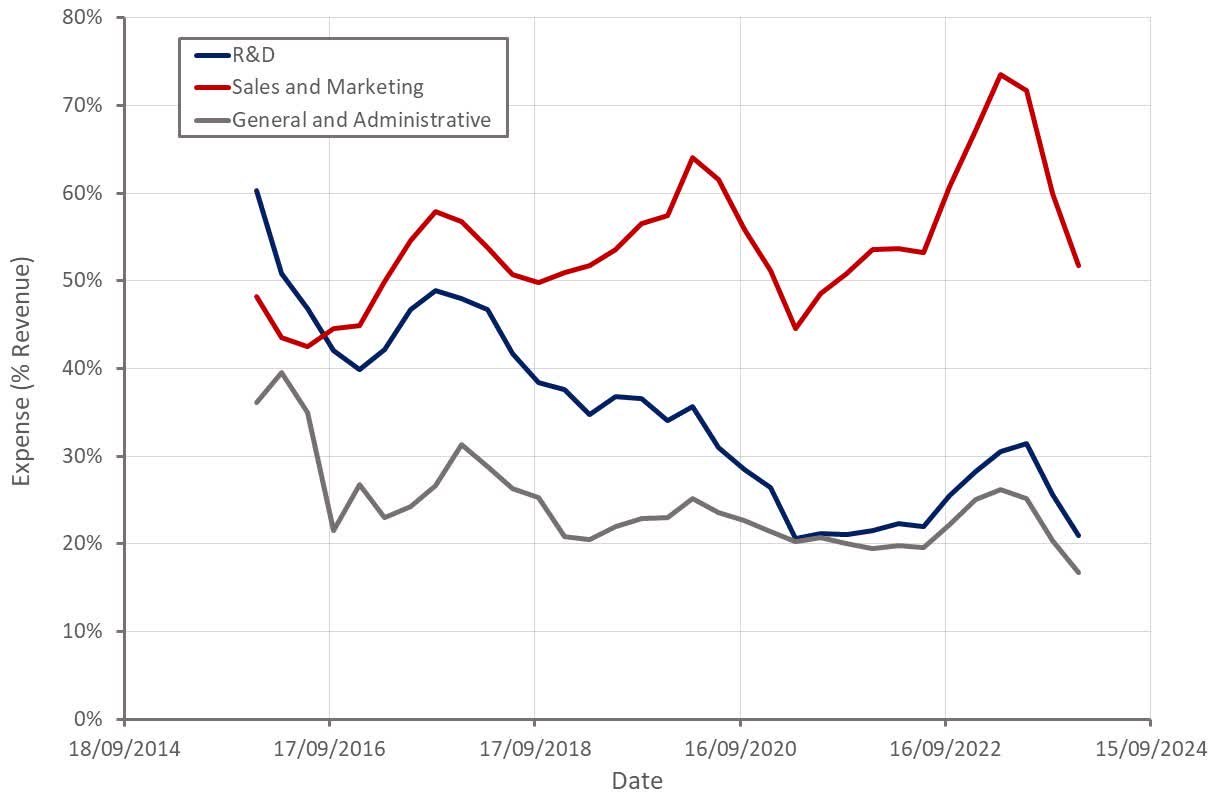

Figure 4: Operating Profit Margin (source: Created by author using data from BrainsWay) Figure 5: BrainsWay Operating Expenses (source: Created by author using data from BrainsWay)

BrainsWay currently has around 46 million USD of cash, cash equivalents and short-term deposits, putting the company in a position to begin returning capital to shareholders as it becomes profitable on a consistent basis.

While BrainsWay’s stock is up significantly over the past 12 months, the company’s valuation is still modest. Much of the share price move over the past 12 months was reversing an absurd overreaction to temporary headwinds in 2022.

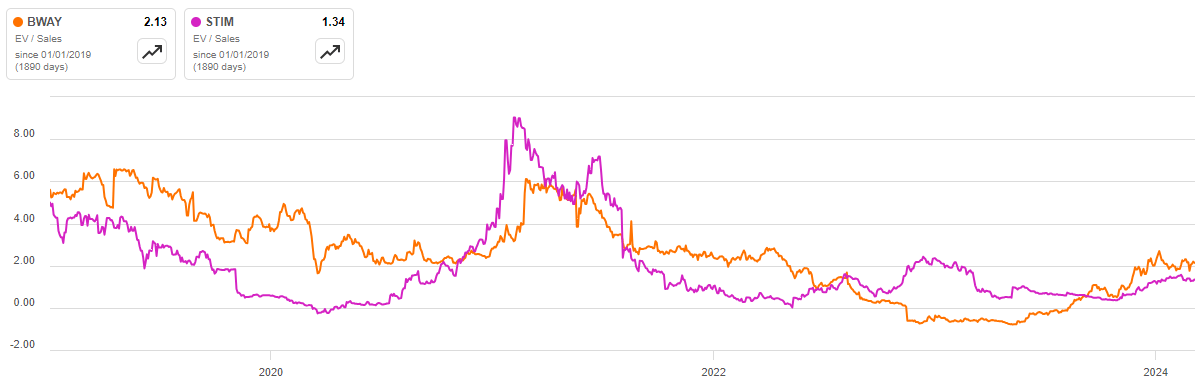

BrainsWay's forward EV/S multiple is still only around 1.5, which is too low given the company's prospects. This is obvious when comparing BrainsWay's valuation with Neuronetics. BrainsWay should trade on a higher multiple than Neuronetics as it is growing faster and has a better margin profile. There is currently little difference between the forward valuation of the two companies at the moment though.

Figure 6: BrainsWay EV/S Multiple (source: Seeking Alpha)