kirilllutz/iStock via Getty Images

kirilllutz/iStock via Getty Images

PHINIA Inc. (NYSE:PHIN) is a company that manufactures integrated components and systems that aim to increase efficiency and reduce emissions in both combustion and hybrid vehicles. PHIN's historical financial results have shown consistent revenue growth over the past three years. However, for 2023, its margins contracted slightly due to high inflation affecting costs and a decrease in commercial vehicle [CV] volume in China. Looking ahead, its strong business win in 2023 is expected to bolster its long-term growth. Although S&P is expecting 2024 global light vehicle [LV] production volume to decline, PHIN's decision to focus more on CV and the aftermarket [AFM] segment is a good move to reduce its exposure to the LV segment. In the long run, this shift will ensure that its business remains robust even in times of volatility. On these factors as well as double-digit upside potential, I recommend a buy rating for PHIN.

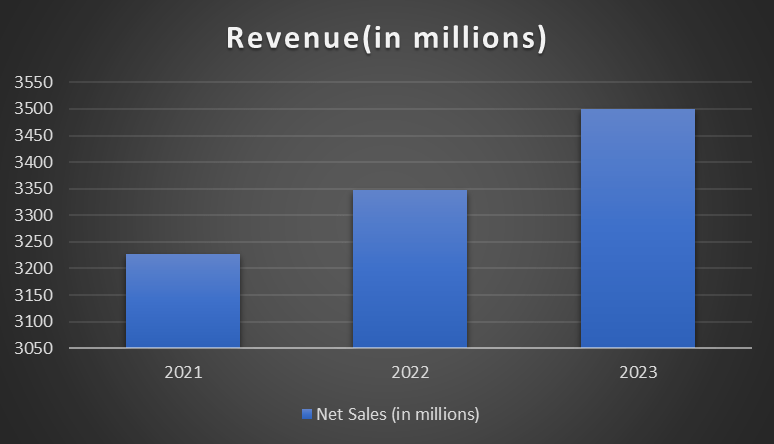

Over the last three years, PHIN's revenue has been growing annually. In 2021, it reported total revenue of $3.2 billion, while in 2022, it was $3.3 billion. This represents a year-over-year growth of ~4%. The growth was driven by increased volume, a better product mix, and new business wins, but was partially offset by fluctuations in foreign exchange.

For 2023, total revenue was $3.5 billion, which represents year-over-year growth of ~4.5%. This growth was attributed to higher pricing, increased volume, a better product mix, and new business wins. The growth drivers for 2023 were the same as those for 2022, and this shows the business's robustness, sustainability, and market positioning.

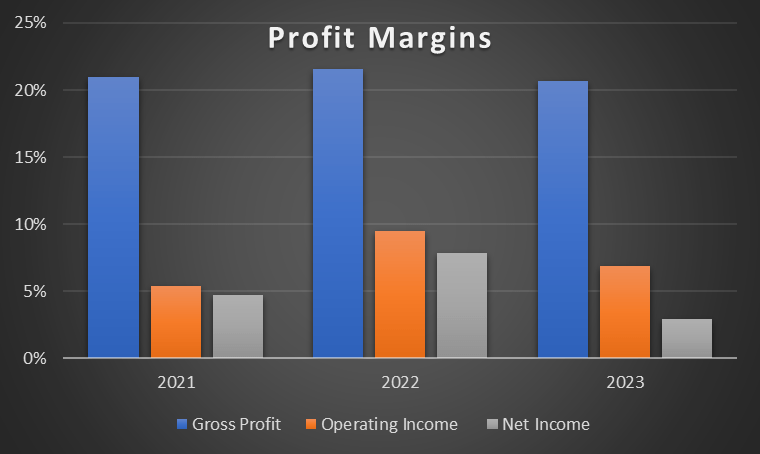

In terms of profit margins, 2023's figures showed slight contractions. Gross profit margin contracted from 21.5% to 20.7% due to higher supplier-related costs and inflation. Its operating income margin contracted from 2022's 9.5% to 6.9%. The decline was due to a decrease in CV volume in China and inflation costs that were not recovered from PHIN's customer base. As a result of the contraction in gross profit and operating income margin, the net income margin decreased from 7.8% to 2.9%.

Author's Chart Author's Chart

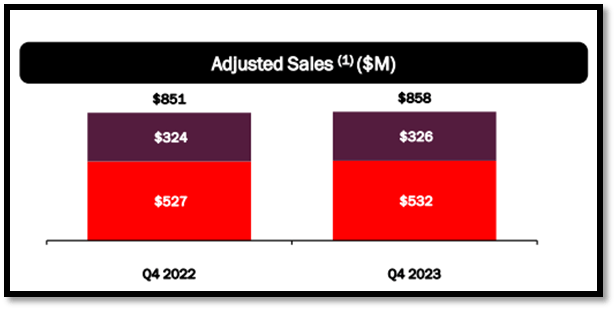

For 4Q23 results reported on February 21st, adjusted total revenue increased a modest 0.8% year-over-year. For context, adjusted revenue excludes some contract manufacturing agreements that PHINA has with BorgWarner Inc. (BWA). These contract manufacturing agreements are connected to the spin-off. The modest growth was due to lower CV original equipment sales in China offsetting gains from non-contractual commercial negotiations. Its revenue can be segmented into fuel systems and AFM. AFM was up ~0.6% while the fuel system increased ~0.9%.

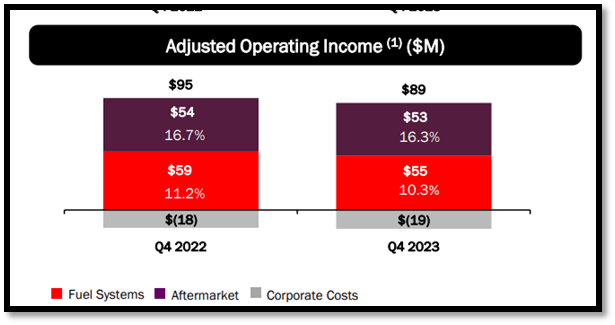

In terms of segment adjusted operating income margin, both AFM and fuel system margins fell year-over-year to 16.3% and 10.3%, respectively, but the decline was modest when compared to the previous period. The decrease in AFM and fuel system margins was caused by inflation increasing input costs. On the company level, PHIN's 4Q23 adjusted operating income margin fell from 11.2% to 10.4%, while adjusted EBITDA decreased from 15% to 14.8%.

Investor's Presentation Investor's Presentation

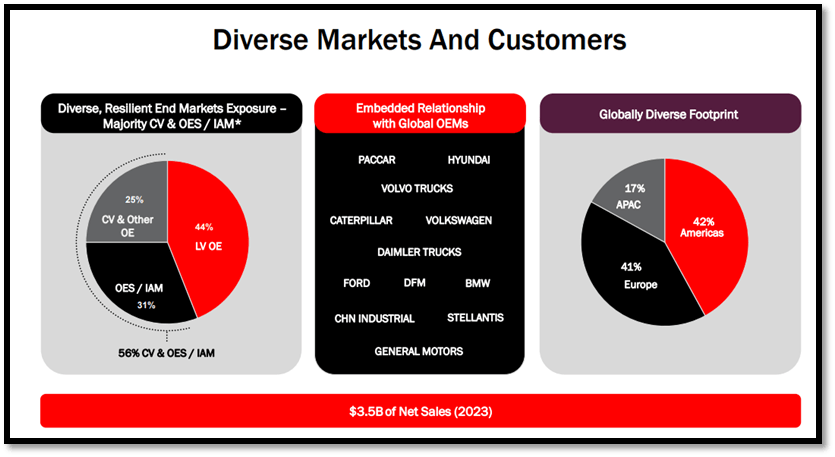

Firstly, PHIN has won a new conquest business to supply its gasoline direct injection [GDI] fuel system to a customer that is a leading original equipment manufacturer [OEM]. This OEM is well known for hybrid and low-emission powertrain technology, specifically within the LV segment. This new conquest business win demonstrates PHIN's ability to gain market share in the LV segment, especially in hybrid vehicles. In 2023, the LV segment accounted for ~44% of its total revenue, which forms the largest share of PHIN's revenue segments. With this win, it is set to bolster its LV segment's growth outlook.

In addition, PHIN also secured a contract extension to continue supplying its next-generation heavy-duty diesel fuel systems to a customer who is a leading global OEM. This business win demonstrates PHIN's strong and ongoing relationships with major players in the CV market. As of 2023, CV accounts for ~25% of total revenue, which is considered a part of PHIN's core segment. Therefore, this business win will continue to provide support for PHIN's core CV segment.

Lastly, PHIN also won a business to supply medium-duty diesel systems to another leading global OEM in the CV segment. This win reflects its product strength not just in heavy-duty diesel fuel systems but also in the medium-duty diesel systems segment. Therefore, this medium-duty diesel systems business win combined with the heavy-duty diesel fuel systems is set to bolster its CV segment, which is considered one of its core revenue segments.

Investor's Presentation

For 2024, S&P forecasted that production levels would be mainly driven by consumer demand. With vehicle inventory levels reaching equilibrium, S&P anticipates global LV production to decline modestly by 0.4% to ~89.4 million units. For mainland China, production levels are expected to be down 0.1% due to weak domestic demand. In Europe, it is expected to decline to low-single digit, driven by decreasing backlogs, weaker demand, and stabilizing inventory levels. Lastly, for North America, it is expected to increase by a modest 0.5%. In terms of semiconductor shortages for 2024, S&P does not expect a shortage as the automotive industry has taken steps, such as stockpiling of chips, to ensure that supply for 2024 is sufficient.

In terms of vehicle sales, it is expected to grow 2.8% year-over-year. The modest growth is attributed to high vehicle prices, high inflation, and high interest rates. For February 2024, inflation in the US surprised the market after it increased to 3.2% vs. January's 3.1%. With inflation still above the Fed's target rate, it's not a surprise that the market is feeling uncertain about the timing of the rate cut. This situation is creating headwinds for vehicle sales as the growth forecast incorporates interest rates and vehicle costs as the factors that drive demand.

Investor's Presentation Trading Economics

For 2024, global LV production is expected to decline modestly, with engine production declining ~4%. On the other hand, global CV production is expected to be flat year-over-year, while the AFM segment is anticipated to bolster 2024's growth outlook.

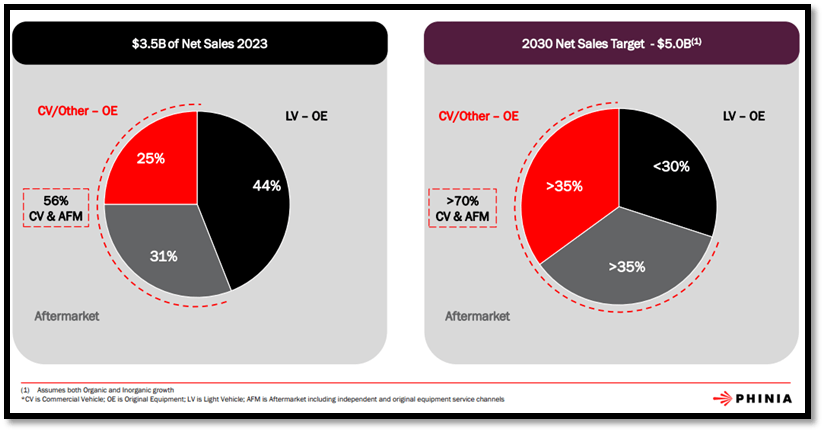

For the long term, management expects a positive outlook for PHIN driven by market share expansion in the CV market and an increase in vehicle population, which will support AFM demand. As a result of this positive long-term outlook, PHIN aims to have a portfolio that is more balanced, with CV and AFM owning at least 70% of total revenue. As of 2023, CV accounts for ~25% of total revenue, AFM accounts for ~31%, and LV has the largest share of ~44%. By 2030, it aims to have CV account for 35%, AFM to account for 35%, and LV to be less than 30%. One of the reasons for this strategic shift is that the AFM segment is more resilient to economic downturns. Therefore, PHIN's strategic decision to make its portfolio more balanced by focusing on CV and AFM is expected to bolster its growth outlook.

In July 2023, PHIN completed its spinoff from BWA. Looking into 2024, PHIN expects to exit all the low-margin contract manufacturing agreements [CMAs] by 2Q24, while the exit of transitional service agreements [TSA] is anticipated to be completed by 3Q24. As the CMAs have low to no margins, exiting them is expected to bolster PHIN's future margins. Apart from margins, management also stated that the CMA exit is also expected to improve future working capital.

Investor's Presentation

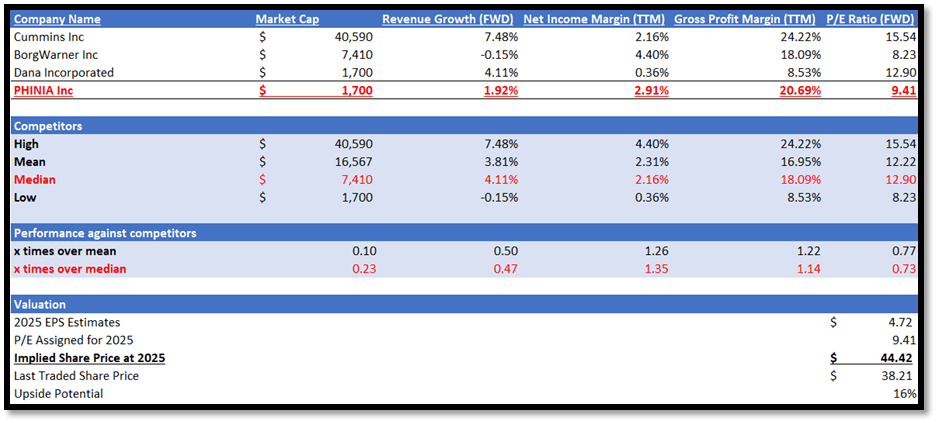

PHIN operates in the automotive parts and equipment sector. I will be comparing PHIN with industry peers in terms of growth outlook and TTM profitability margins. Firstly, in terms of growth outlook, PHIN significantly underperformed its peers. PHIN has a forward revenue growth rate of 1.92%, which is only 0.47x its peers' median of 4.11%. In terms of profitability margins, PHIN is mostly in line with its peers. PHIN has a gross profit margin TTM of 20.69%, which is modestly higher than its peers' median of 18.09%. Despite having a higher gross profit margin TTM, PHIN's net income TTM is even closer to its peers' median. PHIN reported a net income margin TTM of 2.91%, while its peers' median was 2.16%.

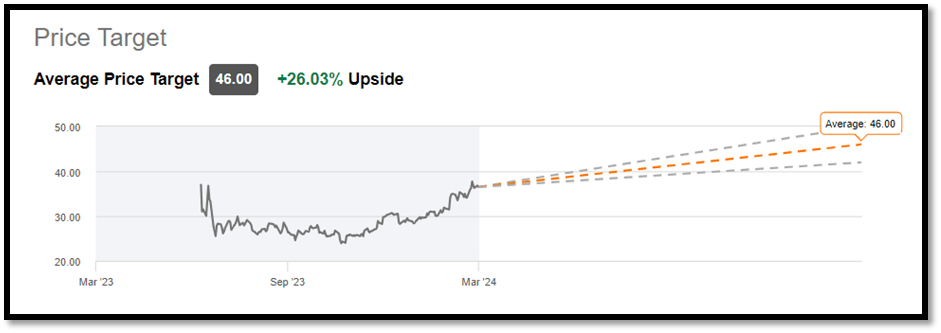

Currently, PHIN's forward P/E ratio is trading at 9.41x, which is lower than its peers' median that is trading at 12.90x. Given PHIN's underperformance in its forward revenue growth rate and inline profitability margins, it is fair for PHIN to be trading at a lower P/E ratio. The market 2025 revenue estimate for PHIN is $3.54 billion, while the 2025 EPS is $4.72. Given the growth catalysts discussed above, such as its strong wins in new and existing business across both LV and CV and its strategic shift towards CV and AFM, these estimates are reliable as they share the same sentiments. By applying 9.41x to its 2025 EPS estimate, my 2025 target price is $44.42. This represents an upside potential of ~16%, which is conservative compared to Wall Street's estimate that has a target price of $46.

Author's Valuation Model Seeking Alpha

The downside risk associated with PHIN is its large exposure to the LV industry. As of 2023, LV accounts for 44% of its total revenue. For 2024, S&P is expecting global LV production to decline modestly due to vehicle inventory levels reaching equilibrium. In addition, 2024 global vehicle sales growth is anticipated to be modest due to the high interest rate and vehicle price. Due to its large exposure in the LV segment, these expected weaknesses will create headwinds for PHIN in 2024.

PHIN has demonstrated robust revenue growth over the last three years. However, 2023's margins contracted modestly due to inflation and a decrease in China's CV volume. As we look ahead, PHIN's strong business win in 2023 shows the strength of its market positioning, and such wins are expected to bolster its growth outlook. However, global LV production is expected to decline in 2024 due to stubborn inflation, high interest rates, and high vehicle prices. In order to reduce its exposure to the LV segment, management is taking active steps by focusing its business more on AFM, which tends to perform well even in poor economic conditions. Therefore, for the long term, I expect this move to bolster its business's resilience. Combining this with double-digit upside potential, I am recommending a buy rating for PHIN.