BrightView Q1: Divestitures And Lower Leverage Could Imply Undervaluation With Risks

Summary

BrightView Holdings recently reported divestitures at a double-digit EBITDA multiple, indicating potential profitability.

The company's business segments, development and maintenance, generate significant income and are supported by the growth of private non-residential construction.

Despite risks such as debt obligations and goodwill impairments, BV is undervalued and presents investment opportunities.

Thanasis/Moment via Getty Images

BrightView Holdings, Inc. (NYSE:BV) recently reported divestitures at double digit EBITDA multiple, and announced cash re-investments that may bring operating margin growth. Furthermore, recent decreases in the net debt/EBITDA ratio and new announcements with regard to new M&A growth make BV a buy. Even considering risks from the total amount of debt obligations, goodwill impairments, or changes in the environmental regulations, BV does trade undervalued.

BrightView’s Business Segments

According to the last annual report, there are 280 franchises that make up the network of BrightView Holdings throughout the United States, being the leading provider of landscaping services for commercial entities in the country.

In my last article about BrightView, I noted that the stock was undervalued. I still think that there is some undervaluation. The stock price did not increase much compared to the price mark reported in 2022.

"BrightView Holdings, Inc. is trading quite undervalued. In my opinion, with sufficient free cash flow reinvested in mergers and acquisitions, the current net debt leverage may not be that worrying." Source: Previous Article

Source: Seeking Alpha

BrightView's services are divided into two large branches, development and maintenance, the latter being the one that represents the largest portion of income for the company, which generates around 5 times more each year than its main competitor in the landscaping market worldwide.

Much of the company's growth goes hand in hand with the growth of private non-residential construction across the country, which is, according to the last 10-k, forecasted to grow at least 1.3% each year through 2027. This factor is seen accompanied by the fact that more and more companies, construction companies, or space managers are choosing to outsource this service to reduce the cost structure, just as BrightView has oriented its service toward the design and development of large campuses, supported by an integrated network, which allows the company to be the only supplier.

As mentioned, the business of this holding is organized into the maintenance and development segments. The first of these segments is made up of the company's franchises, operated entirely by its own means, and offers general maintenance services as well as tree care, irrigation, and snow control in some regions. This service reaches all 50 states in the country, and serves different markets such as hotels, private construction, hospitals, and education along with the maintenance of sports spaces, with Brightview being the first consultant for Major League Baseball.

Its clients currently include about 8,800 office parks and corporate campuses, 7,100 residential communities, and 550 educational institutions among others. Its integrated nationwide network allows it to offer services to companies that also maintain franchises or facilities extended throughout the country under the same contracting method.

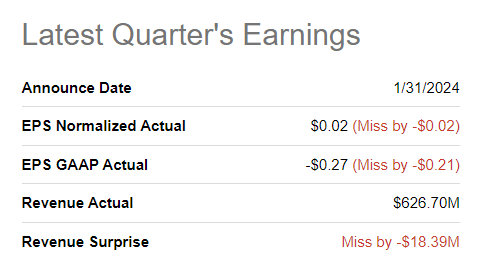

EPS Was Lower Than Expected, But Future FCF Growth Expectations In 2024 And 2025 Are Worth Having A Look

In the last quarterly report, BV reported lower earnings than expected. As a result, I believe that stockholders continued to sell shares of the company. Quarterly revenue stood at close to $626 million with EPS Normalized of close to $0.02.

Source: Seeking Alpha

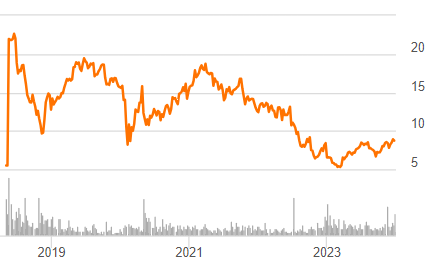

With that, BV is currently trading at multi year lows. In 2018, shareholders saw the company trading at close to $20 per share. Now, the stock price is raging between $5 and $10 per share. With these price dynamics, I think that having a look at the valuation of the BV makes sense.

Source: Seeking Alpha

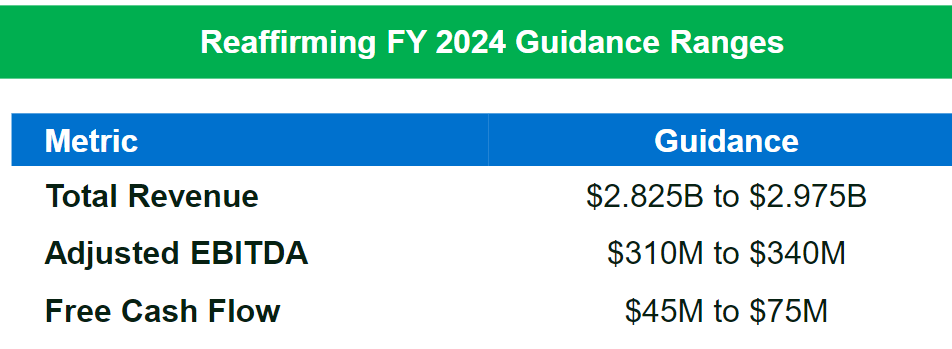

Given the recent guidance for the year 2024, I think that investors may soon pay more attention to BV. In the last quarterly presentation, BV reaffirmed its 2024 guidance. 2024 FCF is expected to be close to $45-$75 million with adjusted EBITDA of close to $310-$340 million.

Source: First Quarter Fiscal 2024

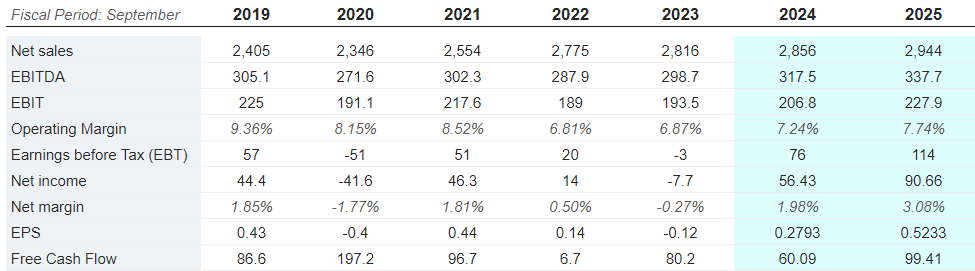

Market analysts out there are expecting significant increase in the operating margin, net income, and FCF growth. 2025 net sales is expected to be close to $2944 million, with 2025 EBITDA of $337 million, 2025 EBIT of close to $227 million, and 2025 net income of $90 million. Finally, 2025 free cash flow would stand at about $99 million.

Source: MarketScreener

Balance Sheet: Goodwill Accumulated Is Significant, But The Debt Is Not Small

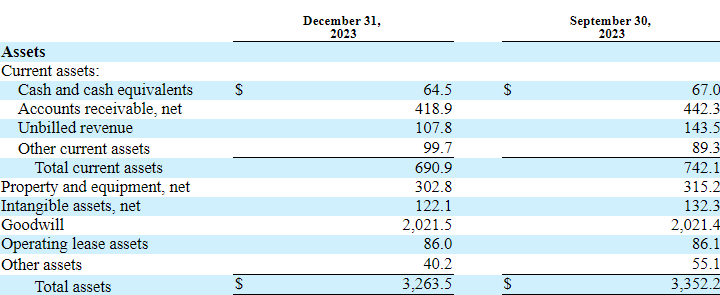

As of December 31, 2023, the company reported a large amount of goodwill and accounts receivable, which are financed with some debt. More in particular, the company reported cash and cash equivalents worth $64 million, accounts receivable of close to $418 million, and total current assets of about $690 million. Current assets/current liabilities ratio is larger than 1x, so I believe that liquidity is not an issue here.

Long term assets include property and equipment worth $302 million, with intangible assets of about $122 million, goodwill close to $2021 million, and total assets worth $3.263 billion. The asset/liability ratio is larger than 2x, so I think that BrightView’s balance sheet looks stable.

Source: 10-Q

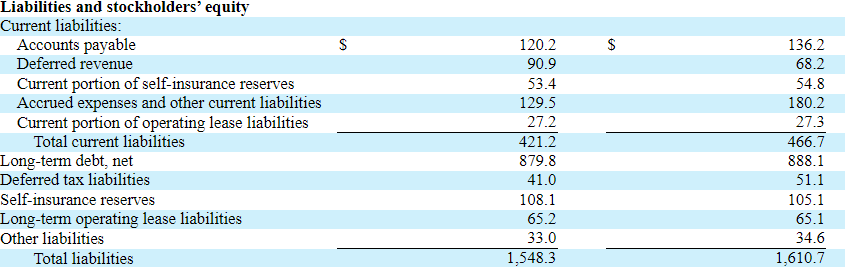

The list of liabilities includes accounts payable worth $120 million, deferred revenue of about $90 million, and total current liabilities worth $421 million. In addition, with long-term debt of close to $879 million and deferred tax liabilities of $41 million, total liabilities stand at $1.548 billion.

Source: 10-Q

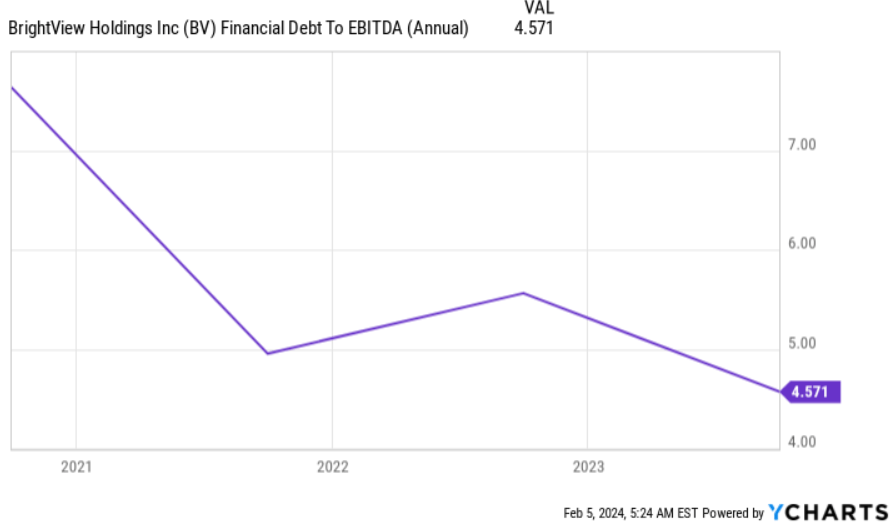

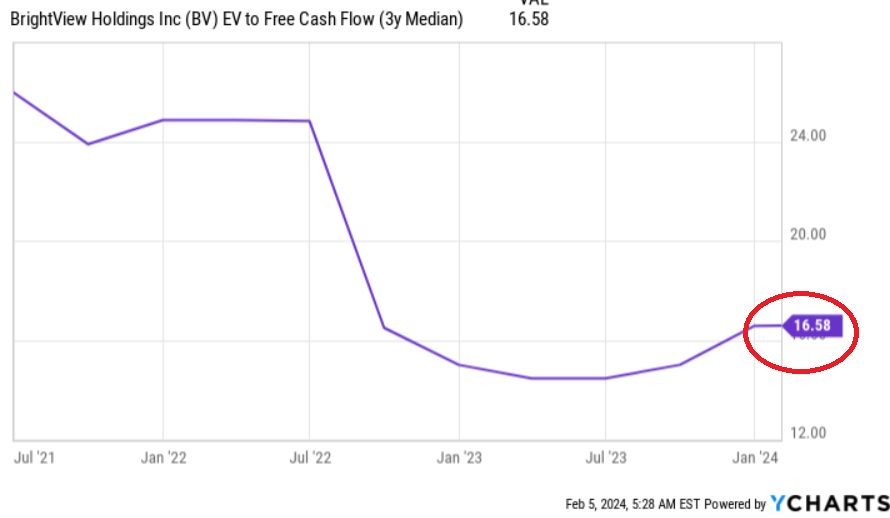

The total amount of debt is not small. BV’s financial debt/EBITDA ratio is close to 4.5x. With that, the company is making significant efforts. The net leverage decreased from more than 7x in 2021 to the current level. In my view, further decrease in the net leverage could lead to higher EV/EBITDA or EV/FCF figures.

Source: Ycharts

Source: Ycharts

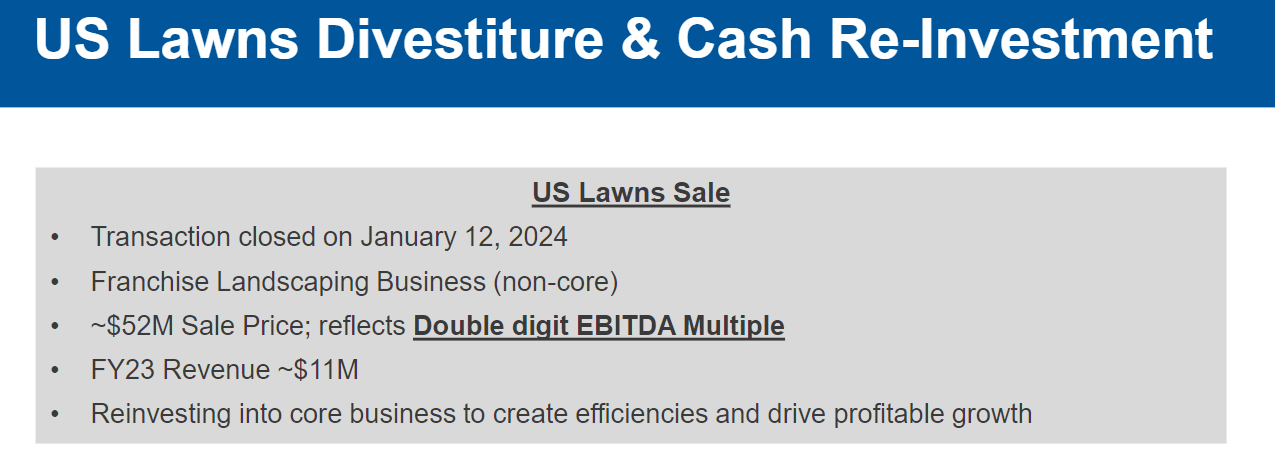

Recent Divestiture at Double Digit EBITDA Multiple And New Divestitures Could Bring Reinvestments in New Efficiencies and Profitable Growth.

In the last quarterly presentation, BrightView Holdings noted a transaction closed in January 2024, which included a double digit EBITDA multiple. In my view, if BrightView is selling assets or divisions at a double EBITDA multiple, it is fair using a double digit multiple for the assessment of the valuation of BV.

It is also worth noting that BrightView Holdings expects to reinvest the new cash in hand to create efficiencies and profitable growth. In my view, further cash re-investments could bring not only FCF margin growth, but also enhancement of expectations from investors.

Source: First Quarter Fiscal 2024

Acquisitions May Continue To Bring New Geographic Markets, Portfolio Expansion, And Economies Of Scale

Given the recent decrease in net debt/EBITDA, BrightView Holdings may propose new acquisitions in the coming years. In the last quarterly report, BV noted new expectations about inorganic growth to attract new customers.

"In addition to our organic growth, we have grown, and expect to continue to grow, our business through acquisitions in an effort to better service our existing customers and to attract new customers." Source: 10-Q

In my opinion, the new acquisitions could bring exposure to new markets and even enhancement of current services. As a result, if the portfolio of products increases, I believe that we may see net sales growth thanks to demand from existing clients. In this regard, the company also communicated that the commercial landscaping industry is highly fragmented. According to the last annual report, despite being the largest company in relation to these services, the company only comprises 2.7% of the market at the national level. More than 600 thousand suppliers seem to exist that are currently registered. Hence, BV will most likely find opportunities to scale the business model.

"As we continue to selectively pursue acquisitions that complement our “strong-on-strong” acquisition strategy, we believe we are the acquirer of choice in the highly fragmented commercial landscaping industry because we offer the ability to leverage our significant size and scale, as well as provide stable and potentially expanding career opportunities for employees of acquired businesses." Source: 10-Q

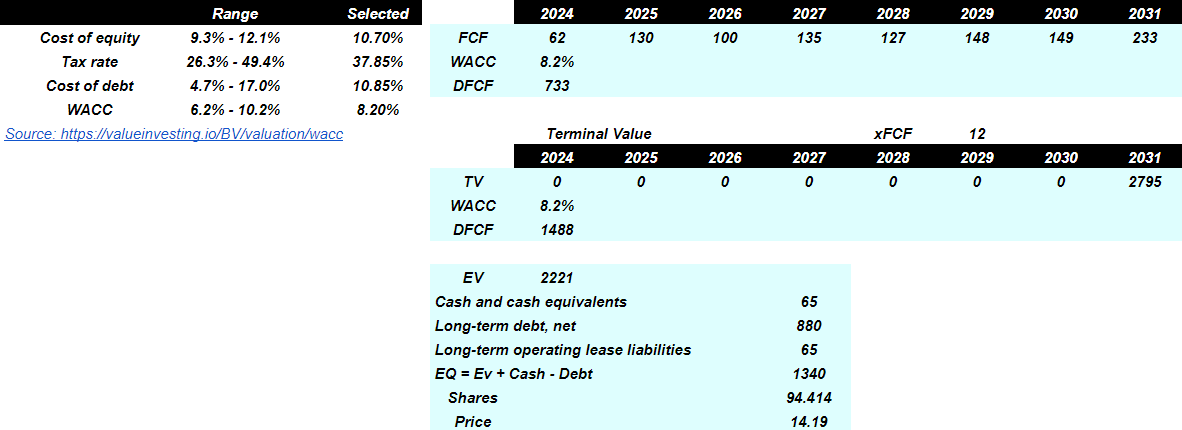

My Discounted Cash Flow Model Implied Upside Potential

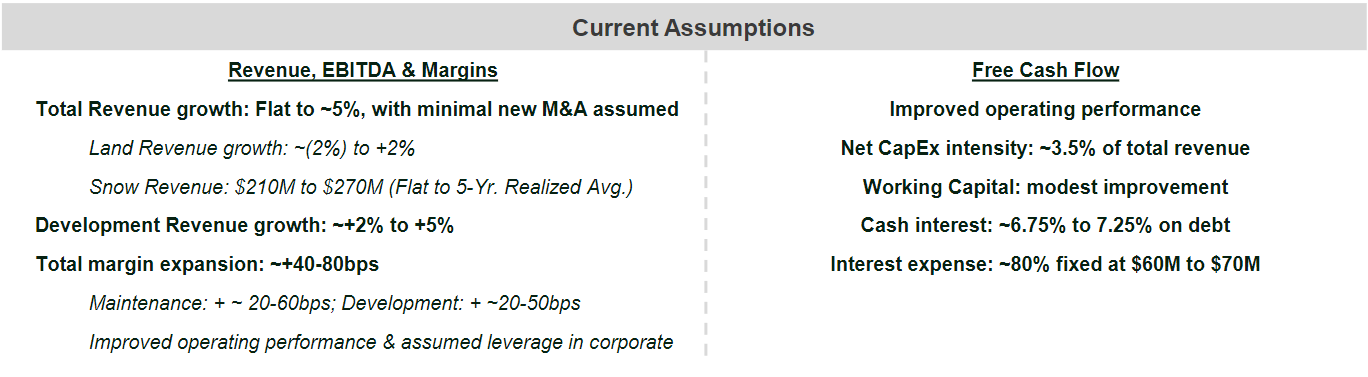

Given previous assumptions, I also paid attention to the expectations and assumptions given by BV in the last quarterly presentation. Note that BV is expecting revenue growth of about -2% and 2% along with margin expansion and operating margin performance improvements.

Source: First Quarter Fiscal 2024

Considering the guidance given by BV, I changed my expectations a bit. My numbers are a bit different from those shown in my previous article. The WACC used in this article is a bit higher than the cost of capital used in the base case scenario included in the last report. Besides, the exit multiple is a bit lower than my previous review. My numbers are based on earlier changes in working capital, capital expenditures, changes in inventories, changes in accounts payable, and D&A.

Source: Ycharts

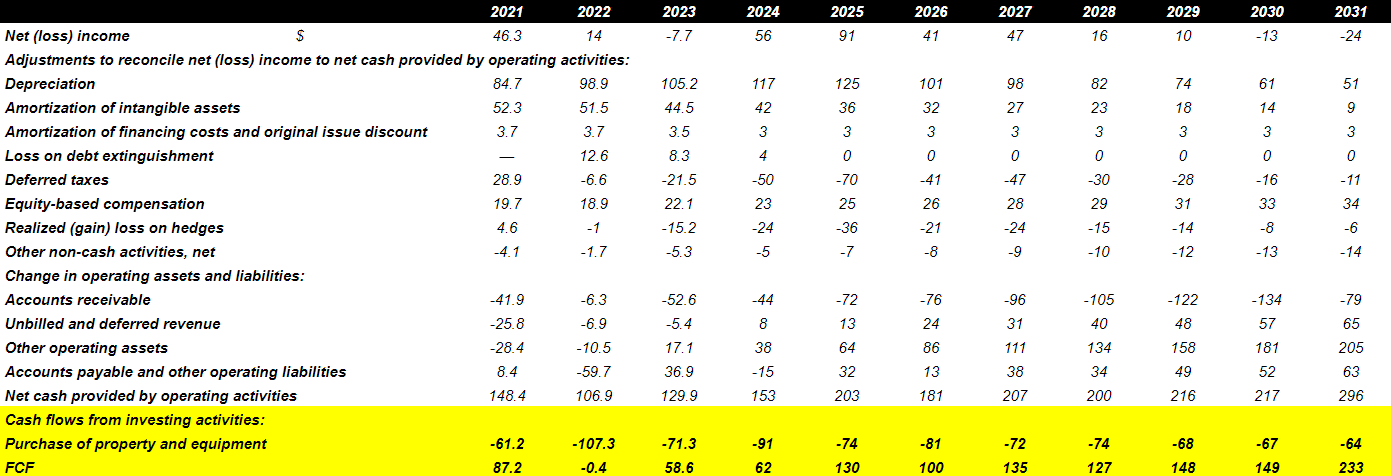

With previous assumptions and guidance given by management, my cash flow expectations include 2031 net income close to -$25 million, with the following adjustments to reconcile net income to net cash provided by operating activities. I assumed 2031 depreciation of close to $51 million, 2031 amortization of intangible assets of about $9 million, and amortization of financing costs worth $2 million.

In addition, with 2031 equity-based compensation of about $34 million, changes in accounts receivable of -$79 million, changes in unbilled and deferred revenue of about $64 million, and changes in accounts payable and other operating liabilities worth $62 million, 2031 CFO would be close to $296 million. Finally, taking into account purchase of property and equipment of about -$64 million, 2031 FCF would stand at $232 million.

Source: Author's Work

Assuming cost of capital of 8.2% and a terminal EV/FCF of 12x, the implied enterprise value would be close to $2.2 billion. Note that peers in the industry are trading at 12x EBITDA and 12.9x cash flow. Hence, I believe that my exit multiple appears reasonable.

Source: Seeking Alpha

Now adding cash and subtracting debt and operating lease liabilities, the implied equity valuation would be $1.3 billion. Finally, the fair price would be $14 per share.

Source: Author's Work

Competitors

As noted previously, the landscape care and snow removal services industry currently comprises approximately $96 billion in market value, and is highly fragmented with a large number of smaller players. Yellowstone Landscape, Bartlett Tree Experts, and HeartLand are the companies that, like BrightView, maintain an integrated network of services at the national level, while the rest of the landscape is made up of independent and regional participants, which is accentuated in the project development segment, in which there are almost no companies with national reach.

Risks

In a general context, any increase in the price of raw materials and sources of supply for the company, combined with a decrease in demand, or the possibility that some of its clients stop outsourcing such type of services are risk factors for the company.

On the other hand, the environmental factor is of vital importance, not only because of what may affect or change working conditions, but mainly because of the snow removal market, in which the company has experienced pronounced growth, which logically depends on the amount of snow that falls.

The company reports a significant amount of debt obligations. I believe that many investors may not be interested in BV because of this fact. In addition, increase in the interest rates could bring a significant increase in interest expenses and lead to lower net income growth.

Goodwill impairments also represent a risk for BV. Given the total amount of goodwill, changes in the valuation of targets acquired could lower future FCF expectations. As a result, I think that the implied valuation could lower. In this regard, BrightView Holdings offered the following lines in the last quarterly report.

"The principal assumptions utilized in the DCF methodology include long-term future growth rates, operating margins, and discount rates. There can be no assurance that our estimates and assumptions regarding forecasted cash flow, long-term future growth rates and operating margins made for purposes of the annual goodwill impairment test will prove to be accurate predictions of the future. We believe the current assumptions and estimates utilized under each approach are both reasonable and appropriate." Source: 10-Q

Conclusion

BrightView’s recent divestitures, cash re-investments, the guidance given for 2024, and more economies of scale driven by inorganic growth are good reasons to follow the company. In addition, in my view, further decreases in the net debt/EBITDA ratio driven by new FCF growth could lead to higher EV/EBITDA or EV/FCF multiples. As a result, I think that we may see new stock demand from investors. Yes, there are some risks from the total amount of debt, goodwill impairments, or changes in the environmental framework. However, at the current valuation, I think that BV is a buy.