krblokhin

krblokhin

Burlington Stores (NYSE:BURL), which many will remember as the Burlington Coat Factory, has had a major rebound from its low point in the Fall but is about where it was a year ago.

Seeking Alpha

With Q4 and FY results recently out, it's worth taking a look at this well-known retailer and examining what kind of potential it has going forward.

The company was acquired by Bain Capital in 2006 and later spun off again in 2013. That conveniently gives us a full decade to examine the financial performance of the company and gauge what it can do going forward.

Author's display of 10K data

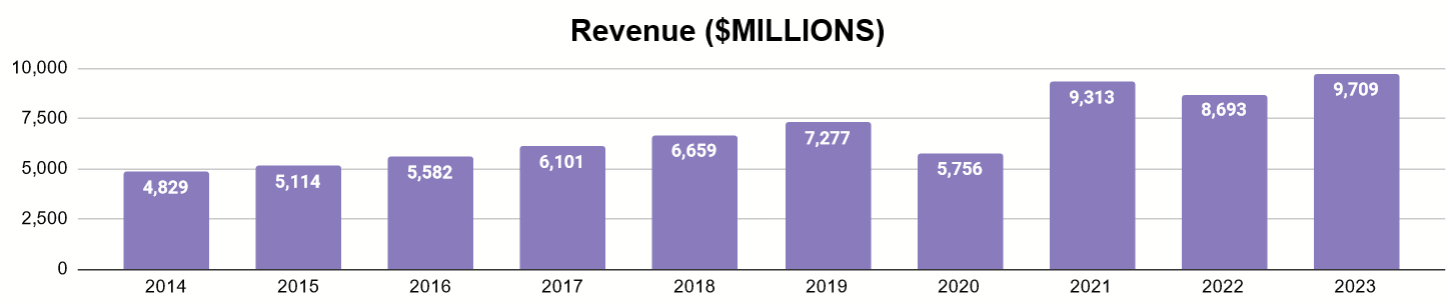

Revenues steady grew from about $4.8 billion in 2014 to about $9.7 billion today, representing a CAGR of about 8%. Operating expenses also grew at a similar rate. The result?

Author's display of 10K data

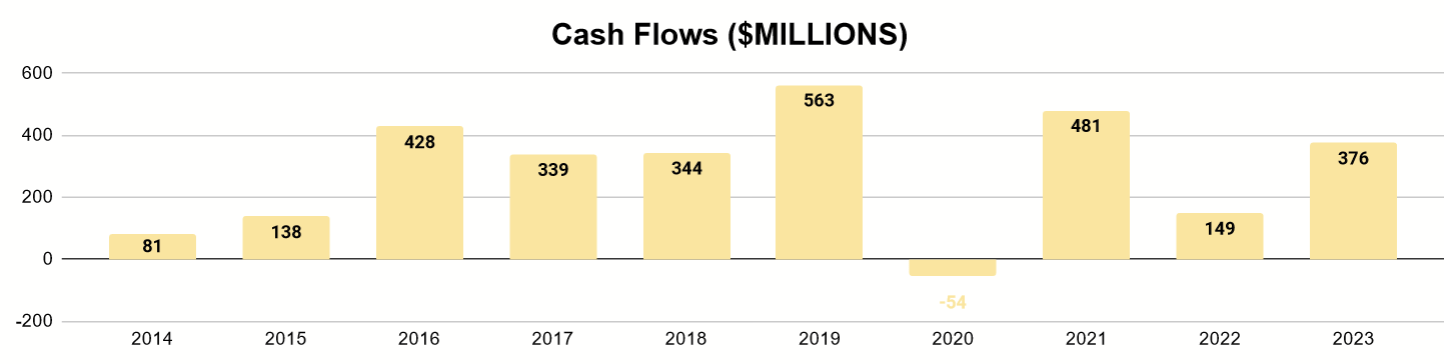

Free cash flow did not change much. With their margins typically being between 5% and 6%, FCF was more greatly affected by minor, year-over-year differences between the growth of revenues and expenses, being widened or squeezed depending on how one outpaced the other.

COVID was the one truly exceptional year, temporarily halting the compounding growth of revenues and with 2020 being the only year to show negative FCF.

This trend was a mixture of expanding their footprint and same-store sales growth, going from about 540 stores in 2014 to 1,007 today. In their Q4 2023 earnings call, management clarified:

In the years leading up to the pandemic, although we might have planned low-single-digit comp, the intent was always to chase above that. And measured over multiple years, our comp indeed averaged 3% to 4%.

Author's display of 10K data

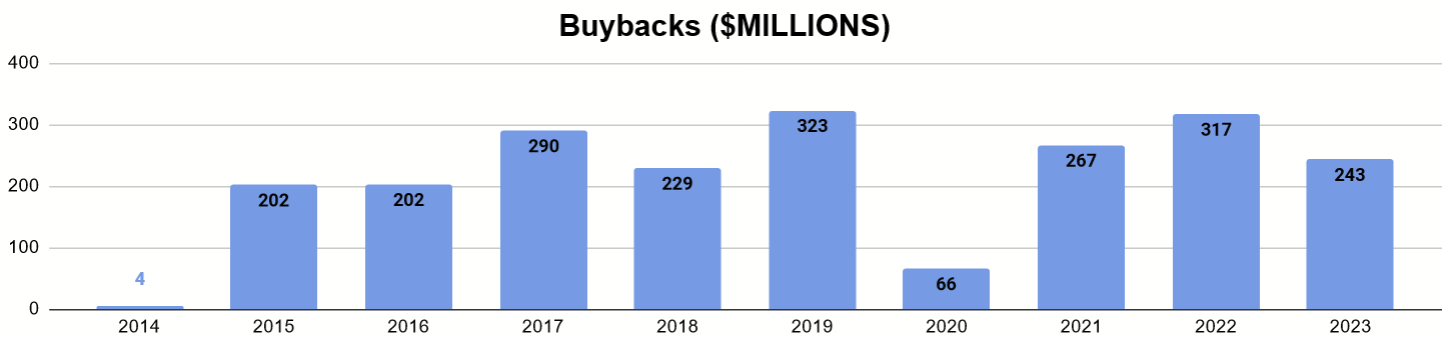

The company has not paid any dividends during this time. Instead, cash has been returned to shareholders primarily through buybacks, beginning in earnest in 2015 and typically accounting for a majority of a year's FCF.

Author's display of 10K data

Despite a prior trend of paying down its debt, the advent of COVID created a need for financing through an additional $1 billion of leverage, which has not yet returned to pre-pandemic levels.

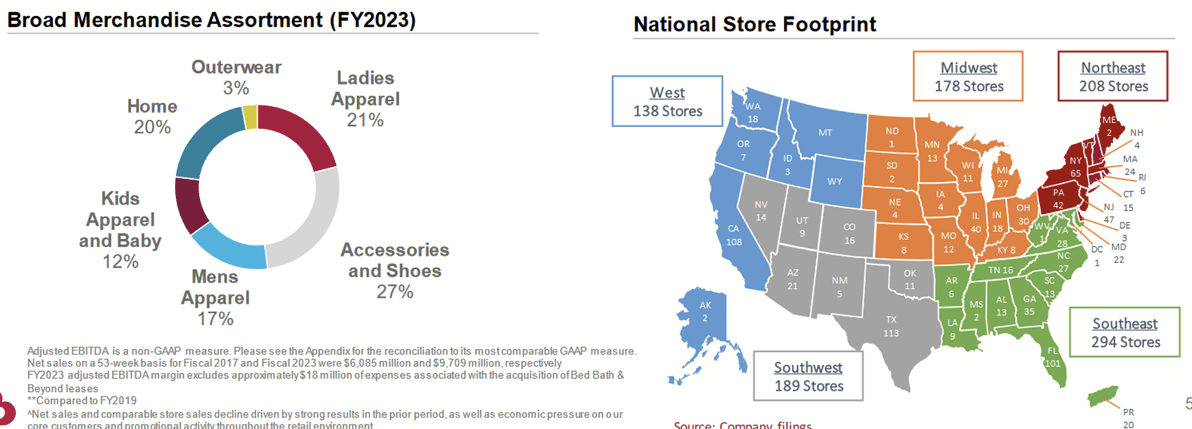

Burlington describes itself as an off-price retailer in clothing and apparel, giving customers a "treasure hunt" experience. Off-price means that it is able to buy more premium brands from vendors at a discount and offer them to consumers cheaply. According to the company, the discount is often up to 60% off of normal sticker prices.

Q4 2023 Investor Presentation

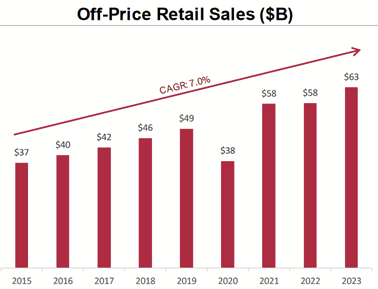

This model explains why, unlike many other brick-and-mortar retailers, Burlington has managed to experience growth and continues to do so. The trend has been similar for the wider market of off-price retail.

Q4 2023 Company Presentation

That company reports that sales growth of the off-price market overall has experienced a CAGR of about 7% (explaining much of Burlington's growth).

Q4 2023 Company Presentation

The company is spread across several U.S. geographies and offers a variety of product that appeals to multiple demographics and uses. As such, its operations are mainly affected by trends that impact large swaths of the country, such as seasonality. As they note in their 2023 Form 10K (pg. 6):

In the second half of the year, which includes the back-to-school and holiday seasons, we generally realize a higher level of sales and net income. Weather is also a contributing factor to the sale of our merchandise. Generally, our sales are higher if the weather is cold during the Fall and warm during the early Spring. Sales of cold weather clothing are increased by early cold weather during the Fall, while sales of warm weather clothing are improved by early warm weather conditions in the Spring.

These trends impact not only their sales but their staffing decisions (2023 Form 10K, pg.4):

As of February 3, 2024, we employed 71,049 associates, of which 76% were part-time or seasonal associates...We hire additional associates and increase the hours of part-time associates during seasonal peak selling periods.

As such, their ability to operate profitably depends on their ability to respond to these seasonal changes (which may occur faster or slower than expected), manage their price-sensitive inventory accordingly, and then also manage their manpower to accommodate these fluctuating customer needs.

2023 Form 10K

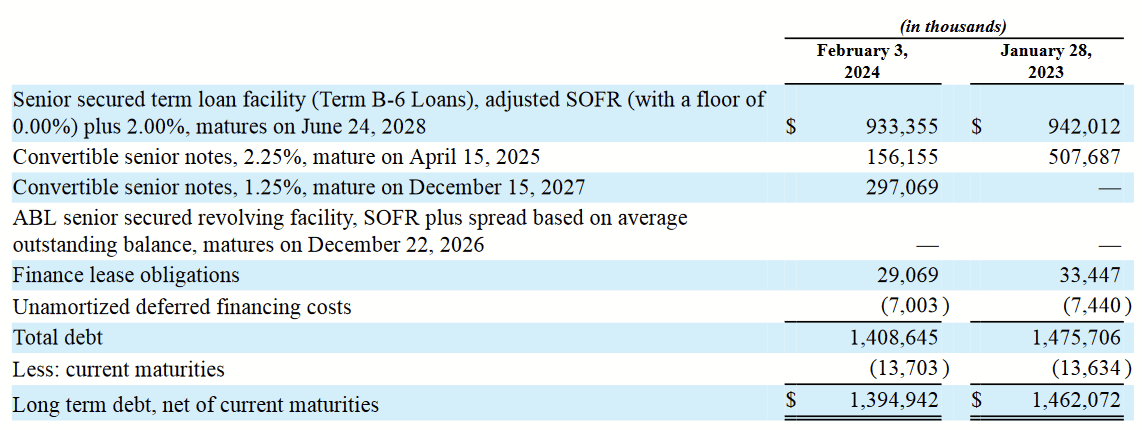

The company currently sits on about $1.4 billion of debt. A decent amount of this comes from low-interest, convertible notes. The majority of it comes from their loan facility.

2023 Form 10K

Not only does this bear higher, floating-rate interest, but it is backed by substantial collateral (2023 Form 10K, pg. 55):

The Term Loan Facility is collateralized by a first lien on the Company's favorable leases, real estate and property & equipment and a second lien on the Company's inventory and receivables.

These account for nearly all of the company's tangible assets.

There are a number of positives and negatives to weigh here. I want to start with the things that bode well for the company.

I previously showed the graph of the company's data on the rise of the broader market for off-price. I believe this is a trend that is likely to continue. It's important to be skeptical of brick-and-mortar stores as investments in my view, especially amid the rise of e-commerce. I made a similar point when I wrote about Kohl's (KSS) in December.

Yet, where department stores have suffered is from their full-price model. Online sales-whether it's a hub like Amazon (AMZN) or the rising shift of many brands to DTC sales-has been out-competing them over the past decade. With full-price goods, getting the product quickly and conveniently to the customer is what matters.

Goods that don't make it to customers are the fuel for these players in the off-price space, and they aren't threatened in the same way that a Kohl's is. Thus, as these legacy department stores and other full-price retailers continue to decline, this will be a growing market for off-price.

A lot happened over the last few years, starting with COVID, that complicated the company's ability to move forward with growth as it liked. CEO Michael O'Sullivan indicated this optimism, indicating that most of these issues are behind the company now in Q4 earnings:

So here we are, what to expect in 2024? I'm going to whisper this, but we think it's possible that 2024 could be the first full normal year since I joined Burlington in 2019. And that's kind of how we approached guidance for 2020.

Q4 2023 Company Presentation

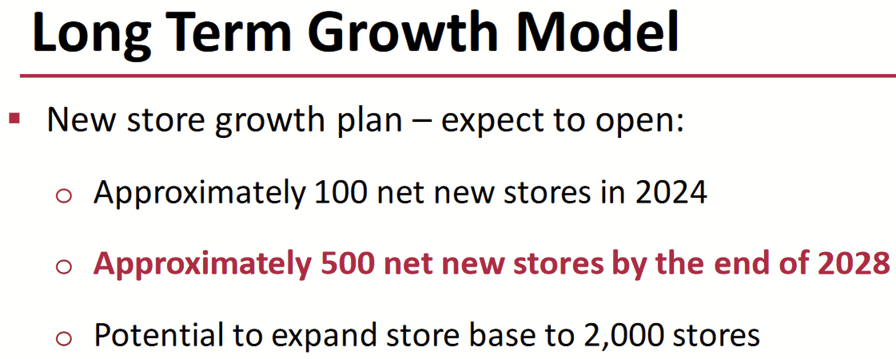

The company intends to keep growing stores and believes that 500 can be added by the end of 2028. They also believe that they can grow operating income to about $1.6 billion, which is roughly triple 2023's levels.

Q4 2023 Company Presentation

This tripling would be based on doubling their operating margins to about 10%, while continuing to increase sales at same stores and new.

That's the good news. What concerns might there be about the future?

The first that comes to mind is the fact that the company is continually vulnerable to external forces that it cannot control. COVID was an extreme example, but other forces like supply chain disruptions, freight rates, inflation, seasonality, and cost of labor are not. Burlington rides the wave of the growing off-price retail market. What if that wave subsides?

Q4 2023 Company Presentation

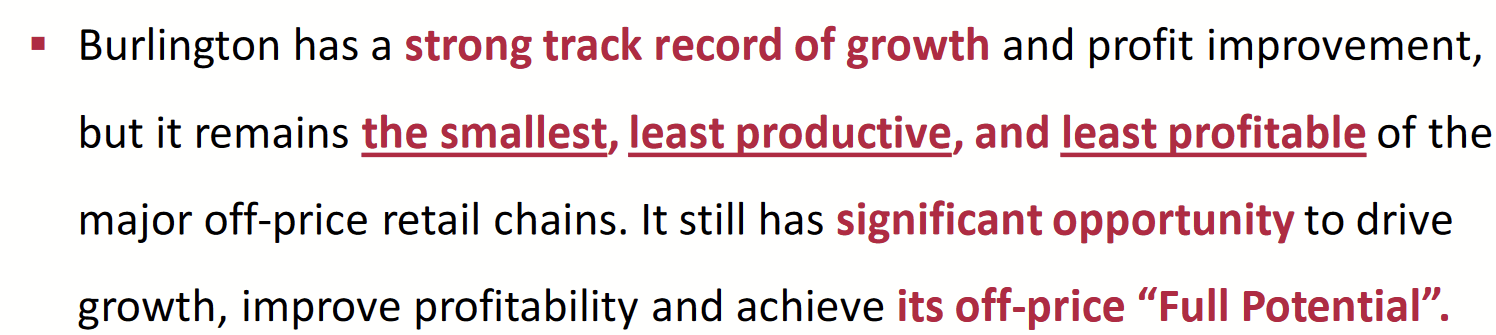

By its own description, the company is one of the less-accomplished of its peers. While these can be good businesses when conditions are favorable, industry leaders are the ones that continue to grow and consolidate, even when secular trends create shrinkage in their space. While I do not caution this on the assumption that such a reversal is likely, long-term investors are likely aware that this can and does occur. When that happens, I believe our long-term returns are safer with the players whose operations and capital allocation set the standard.

On that note...

As I showed before, the company has regularly spent $200M to $300M each year for most of the last decade. This it did even when it experienced negative cash flows during COVID.

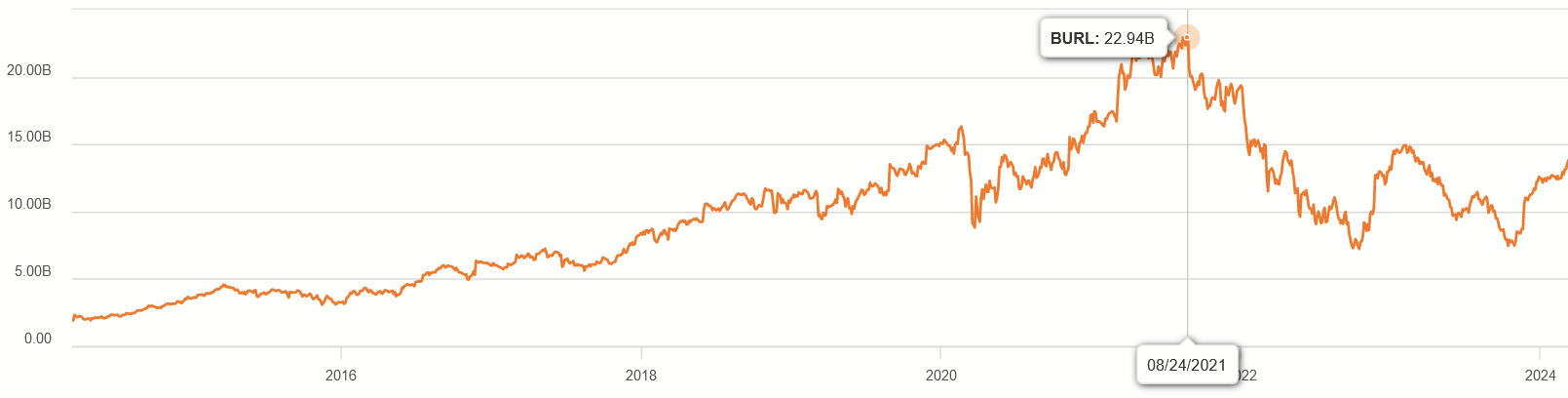

Market Cap History (Seeking Alpha)

With the market cap consistently at a double-digit multiple to FCF (from low to high) and the 8% CAGR of revenues over the decade, it appears these share repurchases have consistently been done at a premium and with an appetite that does not wait for better prices. Over time, I think this has an effect of minimizing long-term returns. In Q4 earnings, O'Sullivan noted:

We did, in fact, increase our buybacks to a little over $100 million last quarter, which was nearly double the previous quarter. So we were more opportunistic this past quarter, as we will from time to time, depending on valuation and liquidity. And we don't guide to buybacks, but I think you can see, looking at our balance sheet at the end of the quarter, we had over $900 million in cash and over $1.6 billion in liquidity, so we're in a really very strong liquidity position.

As we've said many times before, our first priority is to invest in our growth. And Kristin just, a few questions ago, walked through our larger CapEx investment in 2024. Nevertheless, despite that step up, we still expect to generate sufficient cash flow, free cash flow to return excess cash to shareholders.

I don't read this as a sign that buybacks will slow down or cease, particularly if they feel they have enough cash on hand. This brings me to another part of how they manage their cash flow.

I already discussed the level of debt that the company has. A majority of it is from their term loan facility, which is currently yielding over 7%. Realistically, it makes plenty of sense to pay this expensive debt down, since that's close to what their average growth rate has been anyway and eliminates the risk of default with it.

I am concerned that $1 billion in debt was raised in 2020 and that over $800M was spent in the years that followed on buybacks and not paying the loan facility down. While I did talk about the advantages of their off-price slice of retail and extra resilience it has against the domination of e-commerce, it's an operation that runs on tight margins. One tough year to create a liquidity pinch is all that's needed for a problem. That gets me to my last point.

Based on the points I saw raised by management in Q4 earnings and their 10K, they seem like they are trying to do too many things simultaneously: adding stores, increasing same-store sales, buying back shares at large volume, all while taking its time to de-leverage. I believe the company would become a much less risky investment if it dropped one of those things, and I worry that its attempts to multi-task will hurt its returns over time.

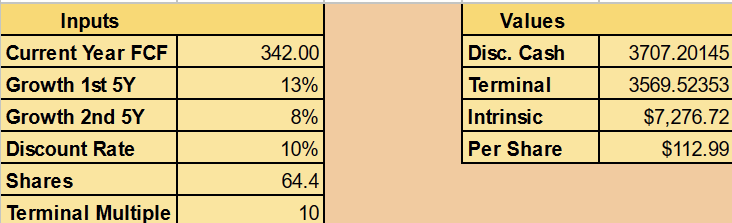

Even with all that I said, we have enough to do a valuation of this company. We'll do Discounted Cash Flow model with the following assumptions:

I use $342M because it's the median, annual FCF value for the last decade. I avoided an average because I think COVID was too unusual of an event to be indicative of the likely future. 13% growth allows them to continue their typical rate of store expansion, on top of margin improvement. Since they believe they can reach 1,500 stores in five years and have a potential for 2,000, that implies about a 6% growth rate from there, adding an additional 2% since they typically improve same-store sales as well. A terminal multiple of 10, meanwhile, is reasonably likely for a company with this level of growth.

Author's calculation

Those assumptions give us an intrinsic value for the business of about $7.3 billion, at $113 per share. With it currently standing close to $14B and $218 per share, there's nothing to suggest today's prices are a good entry.

Moreover, this is a valuation that works with the optimistic outlook provided by management and doesn't factor in the concerns I mentioned. As such, I would want to see not only a much steeper discount in the future but also something to alleviate these concerns.

Burlington Stores has managed to run a profitable business after Bain decided to let it go. Where many brick-and-mortar retailers stagnated or shrank in this time, Burlington continue to grow.

Yet, concerns remain. While off-price retail as a market has room to grow (and Burlington with it), it's easy to botch the execution when operating on tight margins. With expansion, same-store sales growth, buybacks, and good chunk of debt on their books, I'd prefer to invest in a company that keeps it simple and leaves less room for error.

Even if I didn't have those concerns, price still matters, and I feel the happy ending for the long-term investor is more than reflected in today's prices. As such, I am waiting for a better deal.