monsitj

monsitj

“For greed all nature is too little.” - Lucius Annaeus Seneca

Watching with interest the dizzying heights reached out by TECH darling NVIDIA on the back of strong earnings and given the uninterrupted “risk-on” since the end of October, we decided to use as a title analogy “Animal spirits”. As we pointed out in our conversation “Springtime of Nations” published on the 24th of October, we indicated that we were looking at Bitcoin as a “liquidity” indicator. We told you at the time that the very jump in the price of Bitcoin in conjunction with President Xi Jinping’s recent surprise visit to the People’s Bank (PBoC) was probably tied to some sort of “unleashing” of a significant amount of additional stimulus. ETH and BTC jumped very significantly on the 23rd of October based on an ETF driven movement, on the anticipation surrounding ETF spot approval which propelled BTC around the $35K level, its highest level since May 2022 as a reminder. “Animal spirits” come from the Latin spiritus animalis: "the breath that awakens the human mind." It was coined by British economist, John Maynard Keynes in 1936. “Animal spirits” essentially account for market psychology and in particular the role of emotion and herd mentality in investing. “Animal spirits” are used to help explain why people behave irrationally, and are the forerunner to modern behavioral economics. In 2009, the term “Animal spirits” returned to popularity thanks to two economists: George A. Akerlof (Nobel laureate and professor of economics at University of California) and Robert J. Shiller (professor of economics at Yale University). They published their book, Animal Spirits: “How Human Psychology Drives the Economy, and Why it Matters for Global Capitalism”. The two authors argued in their book that although animal spirits are important, it is equally important that the government actively intervene to control them—via economic policymaking—when necessary. Otherwise, the authors postulate, the spirits might follow their own devices, that is, capitalism could get out of hand, and result in the kind of overindulgence that we saw in the 2008 financial crisis.

The 5 cognitive and psychological types of animal spirits identified by Akerlof and Shiller are as below:

These phenomena help economists consider answers to tricky questions such as "why do economies fall into depression" and why are financial prices and corporate investments so volatile?". “Animal spirits” often manifest as market psychology defined by either fear or greed. For the latter, the term "irrational exuberance" has been used to describe investor enthusiasm that drives asset prices far higher than those assets' fundamentals justify. Simply tacking on "dotcom" in 1999 and today “AI” to the name of a company increased its market value to extraordinary levels, with startups showing zero earnings commanding ever-higher share prices. Another example was the lead-up to the 2008-09 financial crisis and the Great Recession, when the markets were rife with financial innovations such as CDO (Collateralized Debt Obligations), CPDO (Constant Proportion Debt Obligation – ABN Amro “Surf” product made us chuckle at the time) and even CDO Squared. The “Animal spirits” thesis, like behavioral economics which we are fond of, essentially throws a monkey wrench into the assumptions of “efficiency” and “rationality”.

In this conversation we would like to muse on “NVIDIA” and Cocoa meteoric rise from an “Animal sprit” perspective and remind our readers on a few basic concept of “physics” such as the laws of “Thermodynamics”. As well we will look again at current issues of “Fiscal dominance” in the US following the astute comments made by Jeffrey Gundlach and reflexionate as well on why Jamie Dimon of JP Morgan decided to cash in for the first time since 2005.

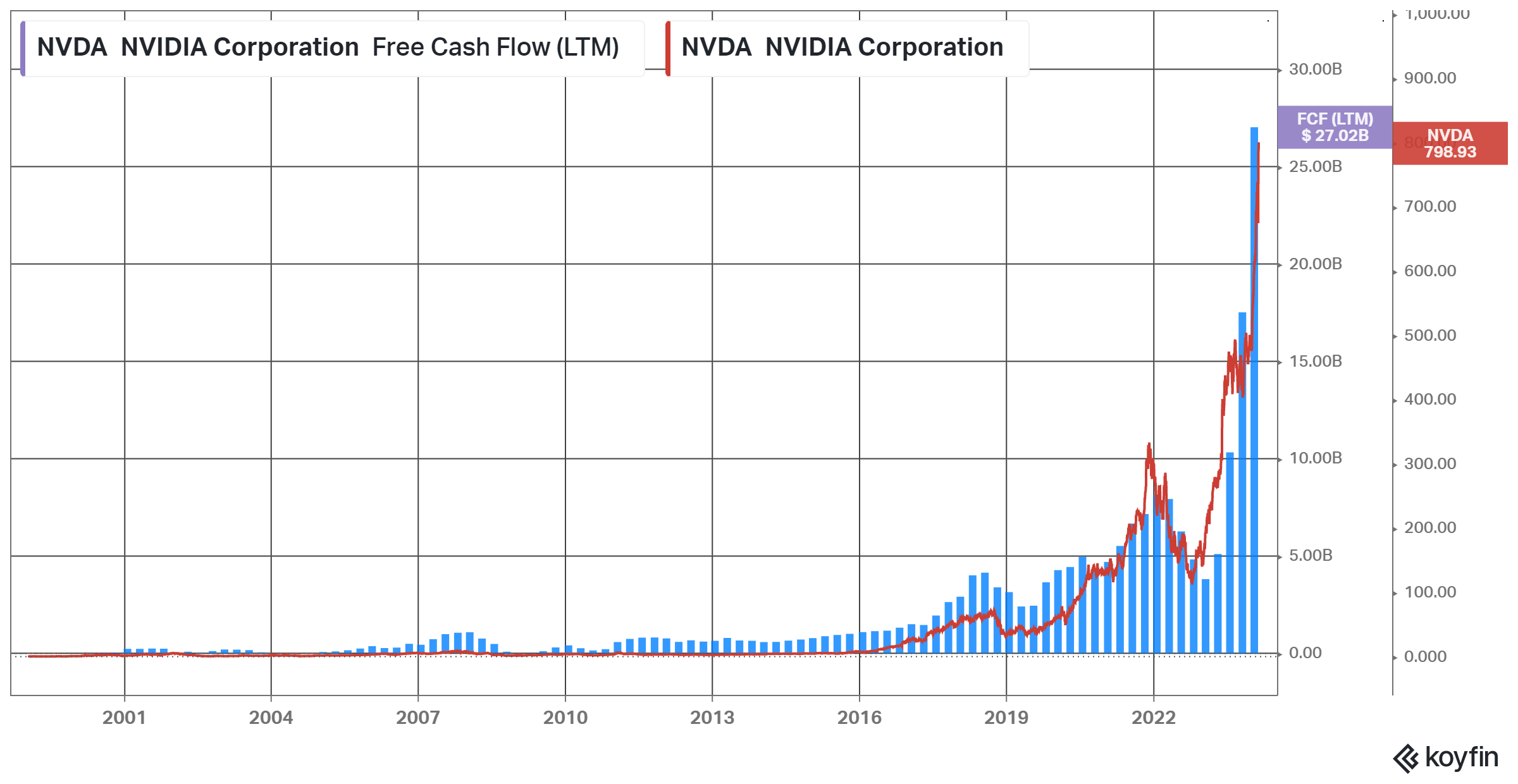

NVIDIA much anticipated earnings came out stellar with EPS at $5.16 vs. $4.64 expected and revenues at $22.1B vs. $20.62B expected:

NVIDIA and FCF (Macronomics - KOYFIN)

NVIDIA gained $1.200 billion in the last 12 months. NVIDIA net income jumped by a stunning $12 billion (+769%) YoY.

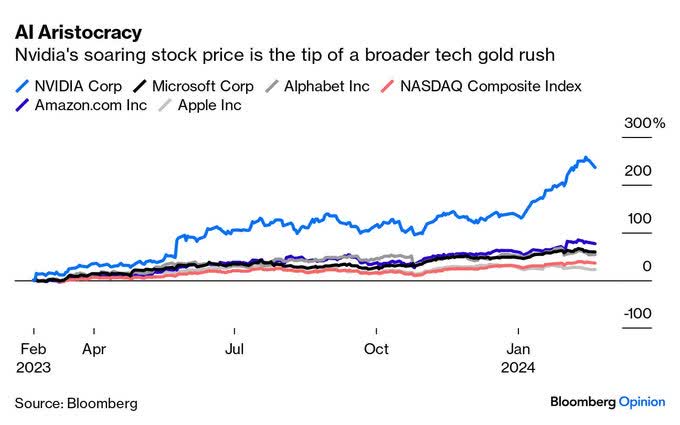

No wonder NVIDIA has seen a soaring stock price:

AI Aristocracy (Bloomberg - X/Twitter)

Here is the 1 year returns of the Magnificent 7, SPY, QQQ and equal weighted S&P 500 ETF, RSP:

1 year returns of the Magnificent 7, SPY, QQQ and equal weighted S&P 500 ETF, RSP (KOYFIN - X/Twitter)

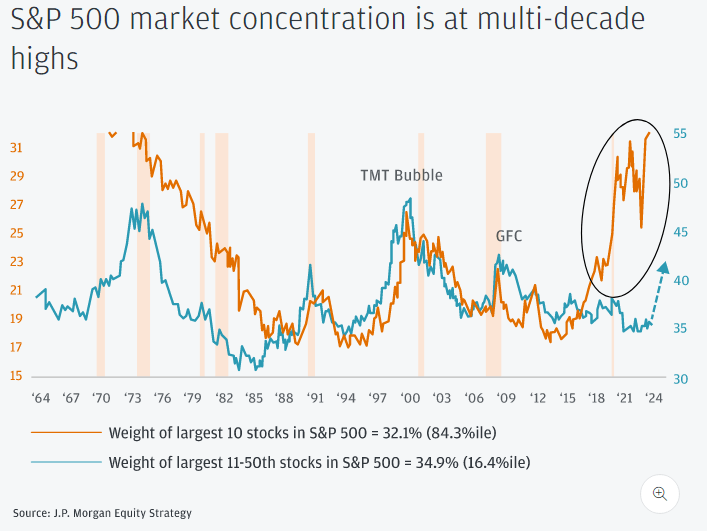

The S&P 500 is become highly concentrated. This is clearly shown in the below chart from JP Morgan:

S&P 500 Market concentration (JP Morgan)

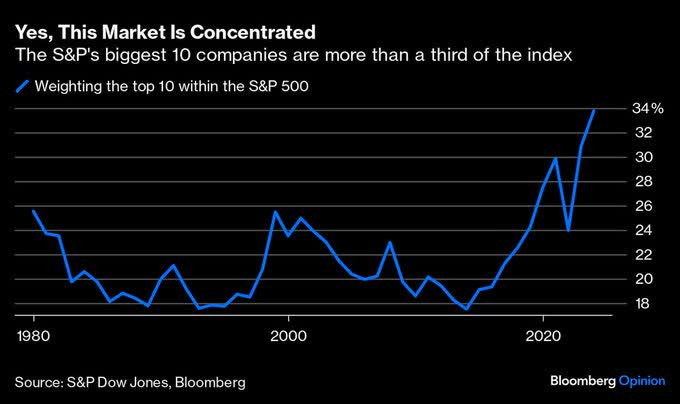

The US market does indeed display very high level of “concentration” in the TECH space:

Concentrated Market (Bloomberg - X/Twitter)

In recent years Emerging Markets (EM) performance has been a “winner-takes-all” environment, whereby a very short list of large growth-focused stocks have dominated performance. This why we have stated in our musings with rising “Fiscal Dominance” that Developed Markets (DM) such as the US are the new “Emerging Markets” (EM) behavioral wise. For instance, in Emerging Markets a very short list of large growth-focused stocks dominated performance also known as the “BANTS”, namely Baidu, Alibaba, Naspers, Tencent, and Samsung. Brazil’s IBOV index ended 2023 at 134.185 points, up 22.3% for the year (the fourth highest annual return in the last decade), nearing its all-time high. Brazil like the S&P500 is an “extreme version” of the Paretto Law: 10 companies accounted for almost 80% of Ibovespa returns in 2023. Heavyweights. Petrobras (common and preferred shares) and Itaú were the largest contributors to IBOV performance, accounting for 11.000 points (or 45.2%) out of the 24.450 IBOV gained in 2023, while Vale was the largest detractor of the index, with 470 points.

This is why we are saying DM is the new EM. We have discussed brushing the “Latam playbook” when it comes to “Fiscal dominance” and “Fixed Income” which we will return in our next bullet point.

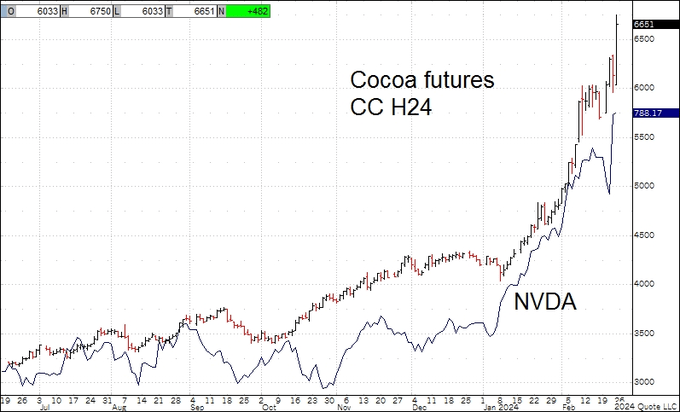

We find the below chart interesting from a “Scarcity principle” and valuation perspective:

“Here is March cocoa futures versus $NVDA. Scales are proportionate. Dance steps are pretty much the same too, which shows that the movements are really all just about liquidity flows” Tom McClellan

Cocoa futures and NVIDIA (Tom McClellan - X/Twitter)

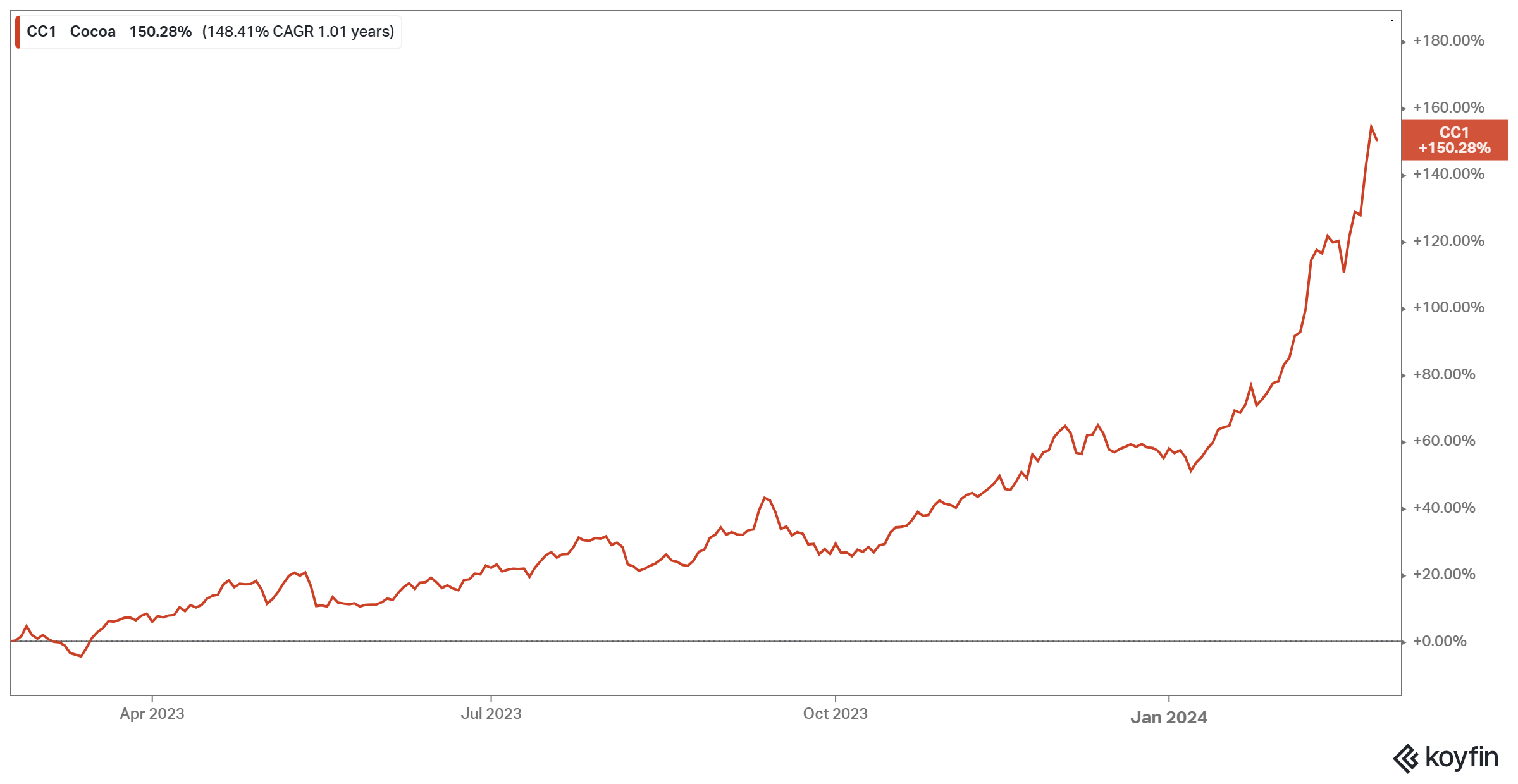

As a reminder, the “Scarcity Principle” is an economic theory that explains the price relationship between dynamic supply and demand. According to the scarcity principle, the price of a good, which has low supply and high demand, rises to meet the expected demand. According to the International Cocoa Organization, there was a deficit of 216kt in the global market during 2021/22 and 99kt in 2022/23. With a significant decline in West African output in the ongoing 2023/24 season, it is anticipated that the market will experience a substantial third deficit, nearing 400kt. The cocoa market was the strongest performing commodity of 2023, with London cocoa finishing 2023 up 70% (1 year chart below):

1 year Cocoa rise (Macronomics - KOYFIN)

Year to date, US cocoa futures are up a further 39%, while London cocoa has rallied by an additional 37%. Both contracts have hit new record highs.

The First Law of Thermodynamics states that energy can be converted from one form to another with the interaction of heat, work and internal energy, but it cannot be created nor destroyed, under any circumstances.

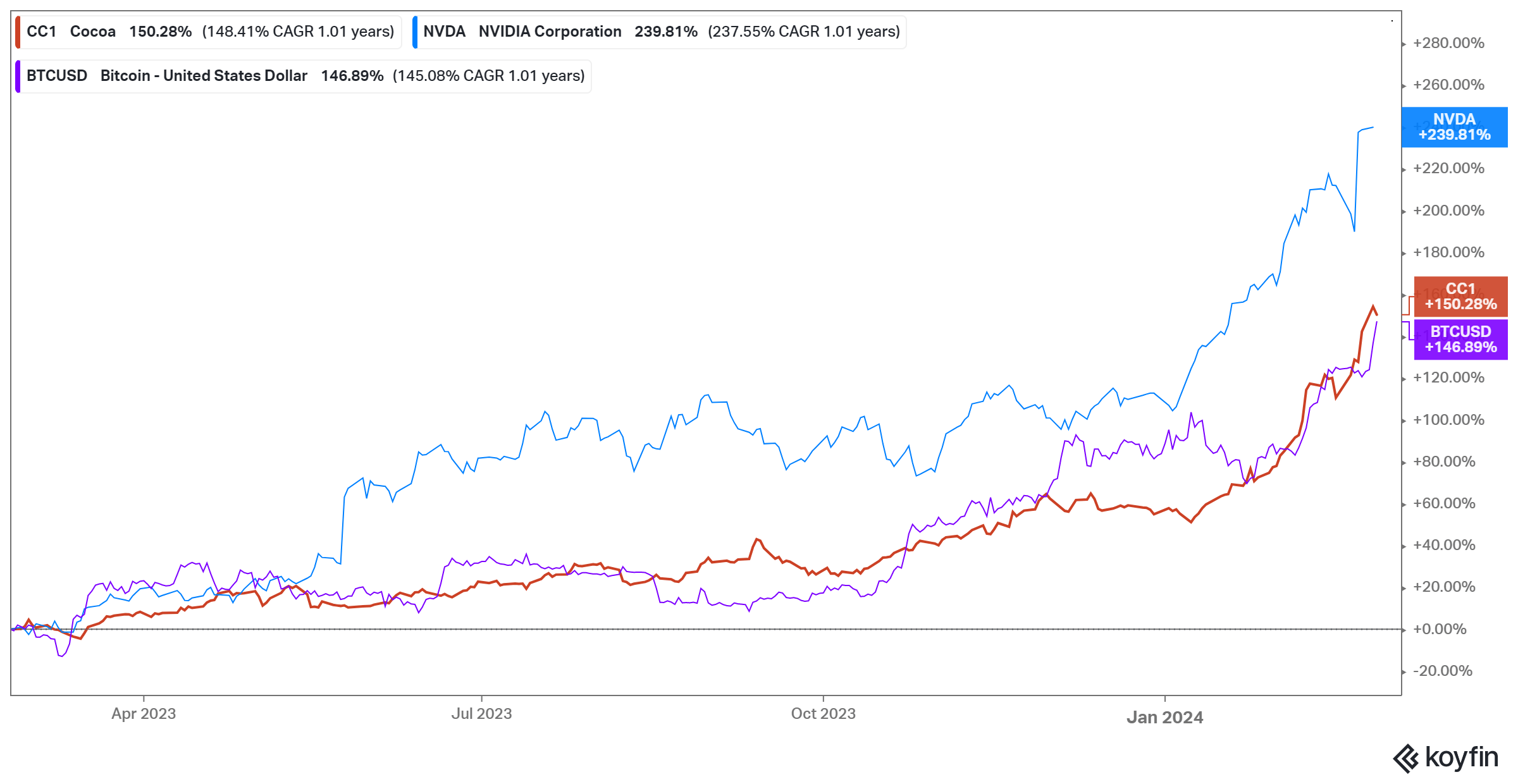

When it comes to “Animal spirits”, we think the below 1 year performance chart displaying NVIDIA, Cocoa and Bitcoin says it all:

NVIDIA, Cocoa and Bitcoin 1 year performance (Macronomics - KOYFIN)

On a side note, both AI and Bitcoin depend on a silver for hardware to operate and uranium to power it. Both metals are in a huge deficit. Draw your own conclusions.

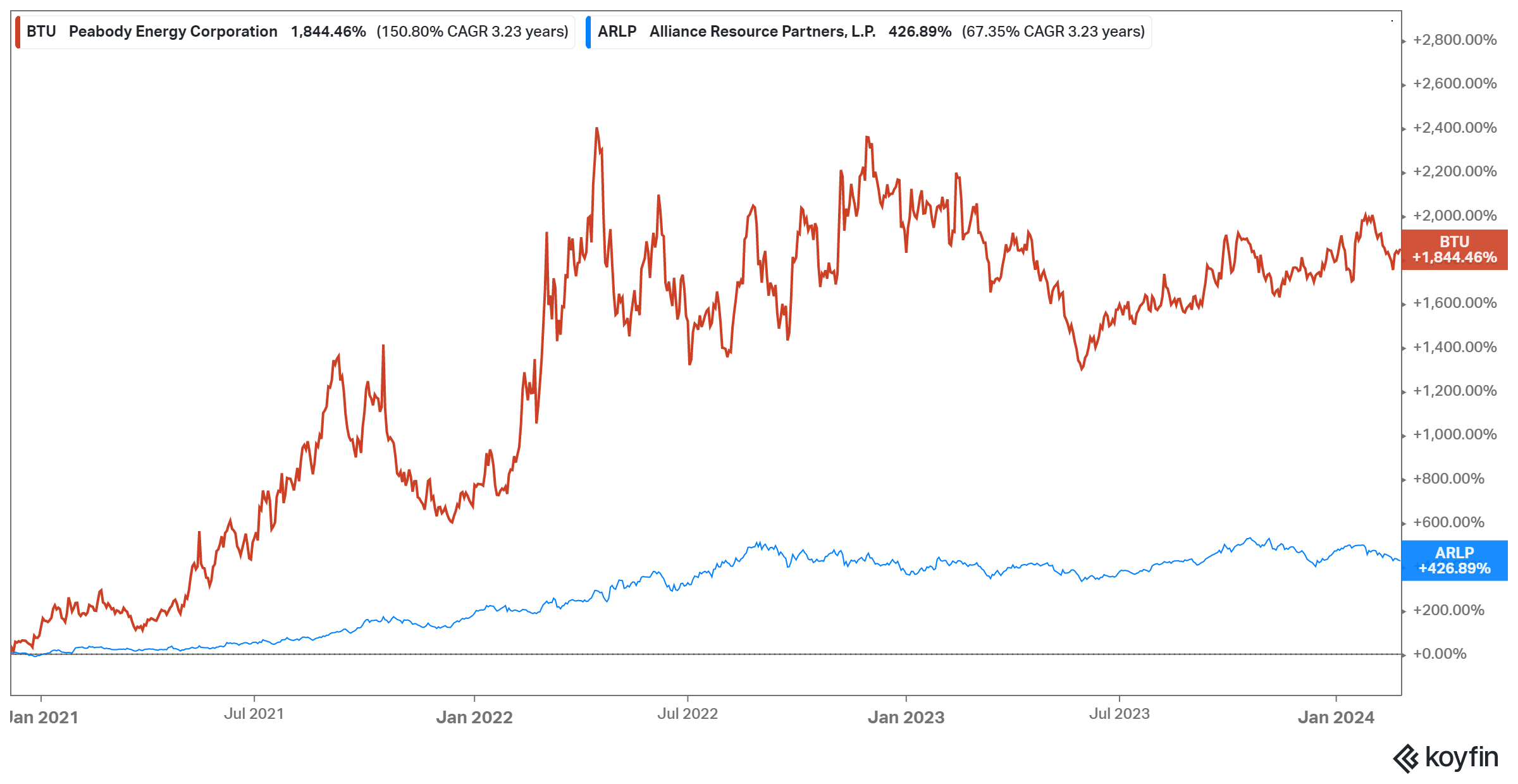

This is why we also told you that we have been riding the Uranium play via ETF URNM and via Kazatomprom because we like long-term value play (hence our “cheap” December 2020 recommendation to OHM Research clients on coal laggards BTU and ARLP at the time – performance chart below):

BTU and ARLP performance since 5th Dec 2020 (Macronomcis - KOYFIN)

Perpetual motion is motion that continues indefinitely without any external source of energy. This is impossible in practice because of friction and other sources of energy loss. A perpetual motion machine is a hypothetical machine that can do work indefinitely without an energy source. This kind of machine is impossible, as it would violate the first or second law of thermodynamics.

The current trajectory of the US Budget deficit has yet to be meaningfully addressed. As such, bond vigilantes are marauding. The most recent Treasury auction in the 20 years space was “ugly”. Tail was 3.3 bps which was the largest on record and foreign bidders dropped from 74% in November to under 60%. US dealers were saddled with 21% of the auction, which is double from November.

At the same time we had Jamie Dimon selling $150 million of $JPM shares for the first time since 2005.

Back in August 2023 in our conversation “The Decoy effect”, we mentioned the work of Charles W. Calomiris from the Federal Reserve Bank of Saint Louis entitled “Fiscal Dominance and the Return of Zero-Interest Bank Reserve Requirements”. We highlighted the part relating to the elimination of paying interest rates on reserves, a path already taken by the ECB. We indicated at the time that if the US government wishes to fund ever growing large real deficits, it needed to eliminate payment of interest on reserves and most likely increase capital requirements for the nation’s largest banks. This of course will directly impact the profitability of the US banks. In the aforementioned paper from Saint Louis Fed, imposing high reserve requirements for zero-interest paying reserves may seem quite “attractive for policymakers” interested in reducing inflationary consequences of “fiscal dominance” less so for the banking industry, as a reminder:

“The history of inflation taxation around the world has shown that when governments become strapped for resources, they often use zero-interest reserve requirements to tax banking systems and remove their spending constraints. For example, in Mexico during the 1970s and early 1980s, inflation taxation of banks became increasingly relied on as government expenditures rose; eventually, as fiscal problems mounted, the government expropriated first bank depositors and then bank equity holders by nationalizing the banks (Calomiris and Haber, 2014, Chapter 11). The general problem of impecunious governments taxing banks with the inflation tax, credit controls, or other means—which can have major adverse consequences for efficient capital allocation and growth—is the theme of a very large literature, which goes back at least as far as Gurley and Shaw (1960) and includes such landmark contributions as McKinnon (1973), Fry (1988), and Acharya (2020).

Taxing banks with reserve requirements and zero-interest reserves is convenient for two reasons. First, instead of new taxes enacted by legislation (which may be blocked in the legislature), reserve requirements are a regulatory decision that is generally determined by financial regulators. It can be implemented quickly, assuming that the regulator with the power to change the policy is subject to pressure from fiscal policy. In the case of the US, it is the decision of the Federal Reserve Board whether to require reserves to be held against deposits and whether to pay interest on them.

Second, because many people are unfamiliar with the concept of the inflation tax (especially in a society that has not lived under high inflation), they are not aware that they are actually paying it, which makes it very popular among politicians. If, as I argue below, a policy that would eliminate interest on reserves and require a substantial proportion of deposits to be held as reserves would substantially reduce inflation, then I believe it would be hard for the Federal Reserve Board to resist going along with that policy.” – Charles Calomiris

On that subject we read with interest Bloomberg article from the 14th of February entitled “UK refuses to publish QE indemnity due to ‘Market Sensitivities’”:

“In the last year and half, the indemnity has become highly expensive for UK taxpayers. The government has already transferred £38 billion ($47.7 billion) to the BOE to cover losses on the program and the bank itself is anticipating another £40 billion of losses this year. Under the indemnity, those are entirely covered by the state.

(…)

Charlie Bean, a former BOE deputy governor, has suggested changes should be made to QE because it is now exposing the BOE “to the charge that they have inflicted substantial costs on the taxpayer without adequate political legitimacy and accountability.”

Between 2009 and 2022, QE was profitable but the Treasury seized all £124 billion to reduce public debt. The BOE now expects the state to have to cover £200 billion of losses in the coming years, putting the lifetime cost of the program at £80 billion.

Bean’s proposal would see the BOE emulating the European Central Bank’s policy of “tiering” payments on reserves. Bailey said it would amount to a tax on the commercial banking system and “would be the wrong thing for us to do - we’d have to do that with the government.” – Bloomberg

For more on the Bank of England losses please read Chris Marsh analysis in his Money Inside and Out post entitled “How big are Bank of England QE losses”.

This is exactly what Bailey is hinting in the above Bloomberg article and most certainly the course which will be taken in both the United States and the United Kingdom. In that context bank “profitability” will take a “hit”.

Of course increasing “reserve requirements” is clearly a feature of the LATAM playbook as per the below chart displaying Argentina’s Reserve Requirements Ratio from April 1985 to November 2023:

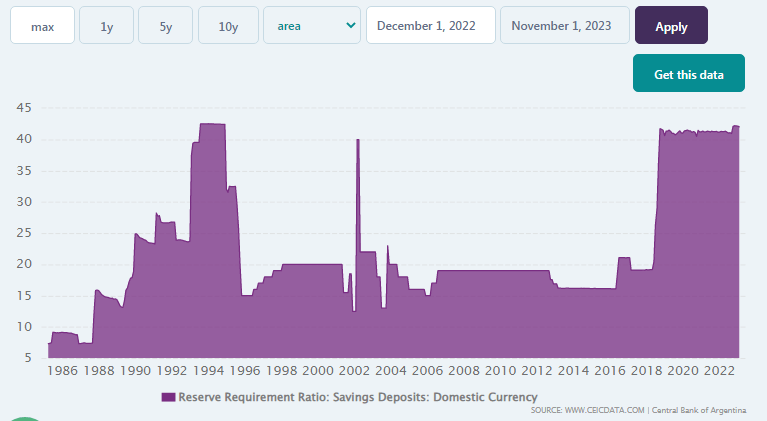

Argentina Reserve Requirements since 1985 (Macronomics - CBCDATA.COM)

Emerging markets tend to raise reserve requirement ratios and repress financial markets when interest rates in large economies decline to shield against volatile short-term capital inflows or to lean against inflationary pressure.

In August 2023 in our conversation “The Decoy effect”, we mentioned that the Federal Reserve’s top regulatory official laid out a sweeping plan to increase capital requirements for the nation’s largest banks in the wake of recent bank failures. Click the link for more on the Fed proposal.

As mentioned in the work of Charles W. Calomiris from the Federal Reserve Bank of Saint Louis entitled “Fiscal Dominance and the Return of Zero-Interest Bank Reserve Requirements”.

“It is quite possible that a fiscal dominance episode in the US would result in not only the end of the policy of paying interest on reserves, but also a return to requiring banks to hold a large fraction of their deposit liabilities as zero-interest reserves” – Charles Calomiris

As pointed out on X/Twitter by Luke Gromen, “bond stuffing” is nothing new, but looking at recent poor auctions and falling participation from foreign bidders, it looks to us that the path described by Charles Calomiris will go through an increase in “reserve requirements”. We highly recommend watching Jeff Gundlach’s thoughts on the trajectory of US budget deficit:

As summarized by Eric Yeung relating to Jeffrey Gundlach thoughts:

1) If interest rates is at 6% for the next 5 years. 50% of U.S. tax receipts would have to go to interest expense.

2) If interest rates is at 10% for the next 5 years. 100% of U.S. tax receipts would have to go to interest expense!

3) The Fed will probably only cut rates one time when inflation go down to 2.5% this year. This is what J Powell wants for his legacy as Fed Chairman.

4) Once recession hits this year or in 2025, the FED will aggressively cut rates, but it will fuel inflation. As well FFR only affects the short end of the yield curve. The long end yields might go significantly higher due to the U.S. debt problem.

U.S. banks have substantially higher risk-weighted assets relative to the accounting value of assets than similar European banks. This difference in risk-weighted assets relative to accounting assets means that large U.S. banks should be required to issue more capital than a European bank with similar assets and risks. The Fed is not the only one thinking about increasing reserve requirements. The ECB is a well thinking about it, after having stopped paying interest on reserves in September last year. Remuneration of bank reserves reduces the effectiveness of interest rate increases as indicated by Paul De Grauwe. QE has led to record losses for Central Banks while leading to record profits for commercial banks. These QE losses will have to be plugged by taxpayers. Some Central Banks are serious in their fight against inflation and therefore have stopped paying interest on reserves. Next step, we think is a hike in “reserve requirements” therefore more “bond stuffing” and more “financial repression” leading to less “profitability” in the banking sector overall and maybe this is the reason for Jamie Dimon divestiture we wonder…