eyegelb

eyegelb

The Q4 Earnings Season for the Gold Miners Index (GDX) is nearly over, and one of the most recent companies to report its results was Fortuna Silver Mines Inc. (NYSE:FSM). The company had a solid year overall, with its new Seguela Mine starting up on schedule and with production coming in above expectations with ~78,600 ounces produced at industry-leading all-in sustaining costs [AISC] of $760/oz. Unfortunately, this was offset by higher costs at its Lindero and San Jose mines, resulting in full-year all-in sustaining costs per gold-equivalent ounce [GEO] coming in above the industry average for another consecutive year. In this update, we'll dig into the Q4 and FY2023 results, recent developments, and see if the stock is attractive at current levels.

Ancien (Seguela) Mineralization - Company Website

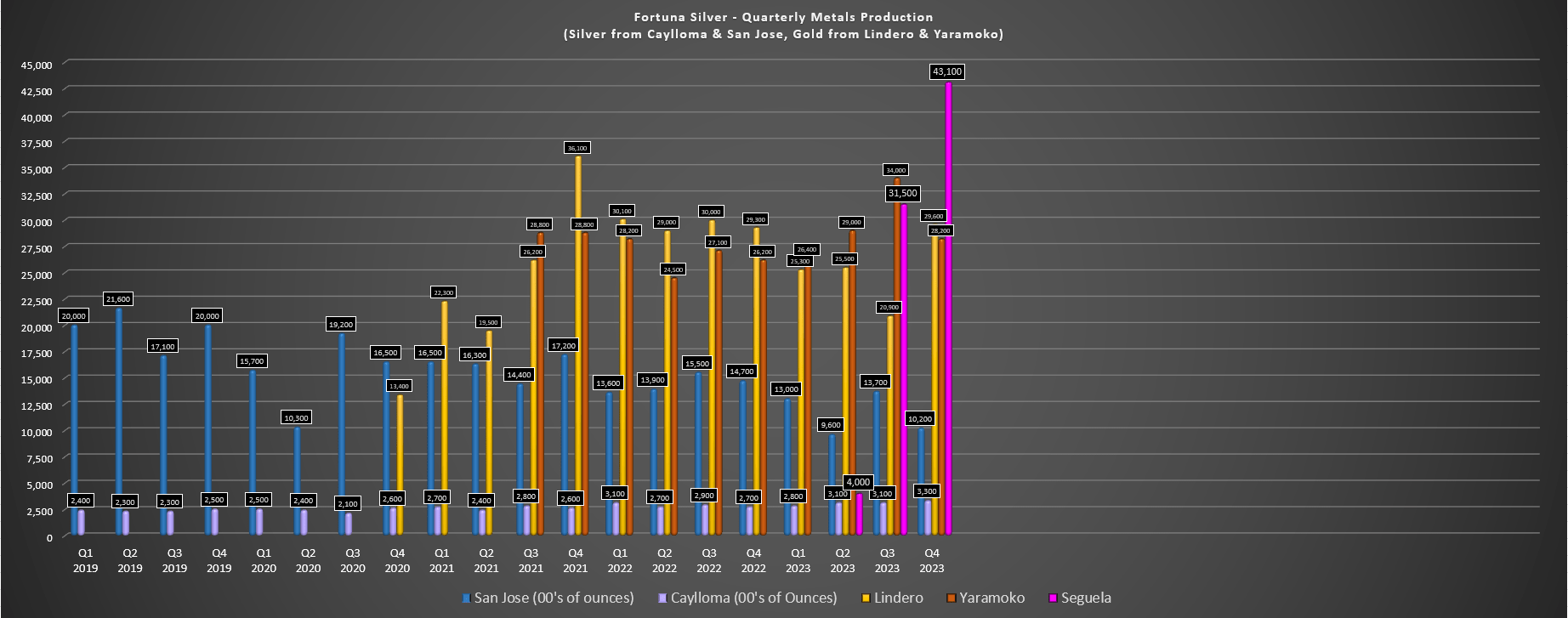

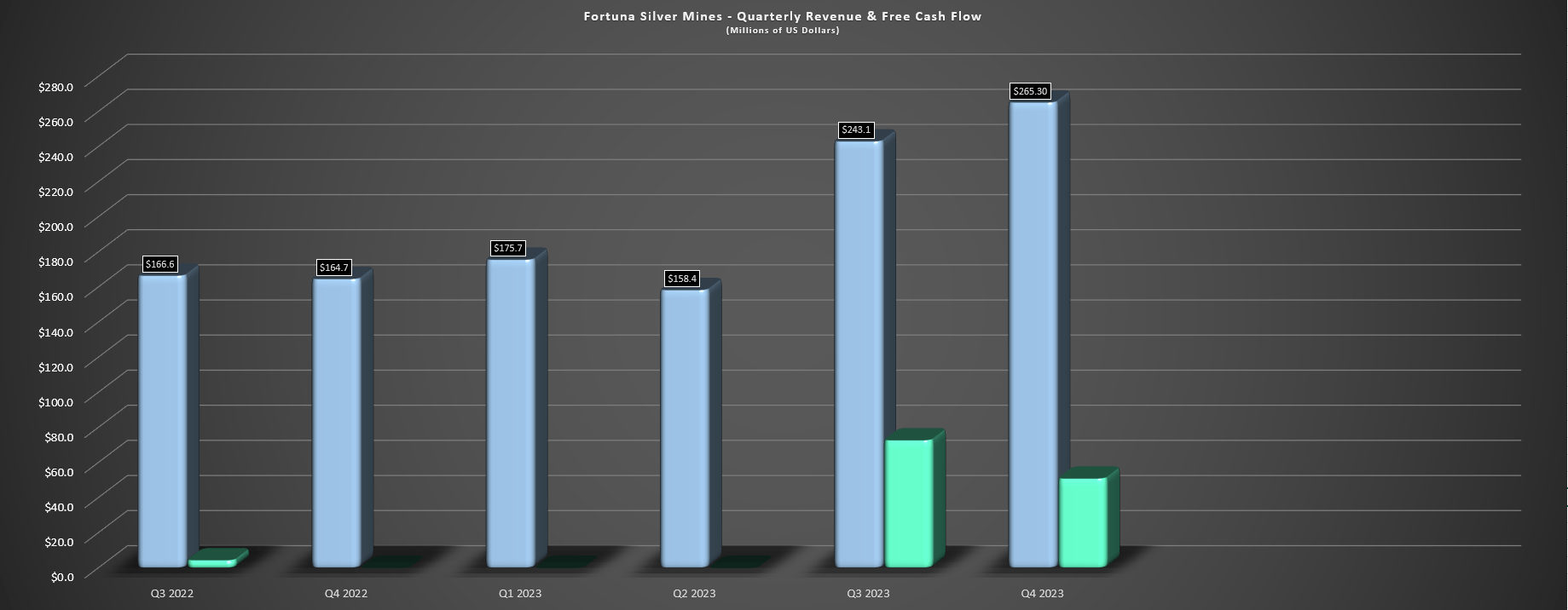

Fortuna Silver Mines ("Fortuna") released its Q4 and FY2023 results earlier this month reporting record quarterly production of ~136,200 GEOs, a 6% increase from the year-ago period. The higher production was helped by a huge quarter from the company's new Seguela Mine (~43,100 ounces of gold produced), another solid quarter from Yaramoko (~28,200 ounces produced), and a decent quarter from Lindero (~29,600 ounces). Unfortunately, the higher production from these three assets was offset by a much weaker quarter from its San Jose Mine, which produced just ~1.02 million ounces of silver (down 31% year-over-year) and ~6,300 ounces of gold (down 25% year-over-year), respectively, with production impacted by lower grades and throughput. The result of the weaker output was significantly higher costs at this asset, with all-in sustaining costs per silver-equivalent ounce coming in at $21.98/oz (Q4 2022: $15.53/oz).

Fortuna Quarterly Metals Production - Company Filings, Author's Chart Fortuna Silver Quarterly Revenue & Free Cash Flow - Company Filings, Author's Chart

Fortunately, the company still put up a solid quarter finally despite the softness at its previous flagship mine (San Jose), with quarterly revenue of ~$265 million and free cash flow of ~$51 million. This was a meaningful improvement over the year-ago period, benefiting from a fifth mine (Seguela) and a higher average realized gold price of $1,990/oz. And given that the gold price strength has continued into 2024, Fortuna is set up for another solid quarter in Q1 and should benefit from an average realized price at or above $2,050/oz.

Moving over to the full year results, Fortuna reported annual production of ~452,400 GEOs (+13% year-over-year), helped by a partial year of production from Seguela and the benefit of grades that well above the reserve grade from its Antenna deposit. The annual production figure included ~326,600 ounces of gold and ~5.88 million ounces of silver, translating to a 26% increase in gold production, offset by a 15% decline in silver production. This resulted in record revenue of $824.4 million (+24% year-over-year), ~$297 million in operating cash flow, free cash flow of ~$90 million and adjusted net earnings of ~$65 million ($0.22). The strong financial performance helped Fortuna to finish the year with ~$128 million in cash and ~$83 million in net debt after $41 million in debt repayments and its debt has been reduced further with a $25.0 million payment made post year-end.

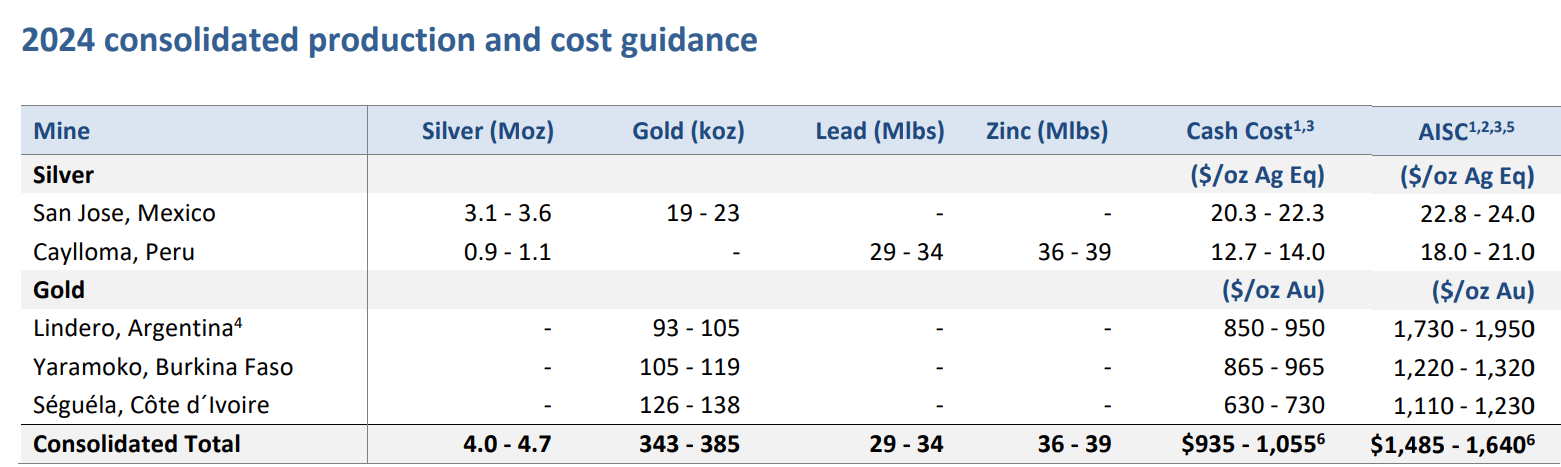

Digging into the results a little closer, Seguela was the star performer with ~78,600 ounces of gold produced at $760/oz all-in sustaining costs [AISC]. The strong performance at the mine was related to positive reconciliation (tonnes and grade) at the Antenna deposit, which led to bonus ounces and plant throughput, which was well above nameplate capacity. However, as noted in my previous update, 2024 will be a more normalized year for Seguela even with the benefit of higher throughput given the higher sustaining capital spend, a higher strip ratio (8.2 to 1) and more normalized grades. In fact, FY2024 AISC is expected to increase over 50% above FY2023 levels at the mid-point ($1,170/oz vs. $760/oz), meaning that Seguela won't have the same significant positive impact on AISC to help drag down costs this year.

2024 Production & Cost Guidance - Company Website

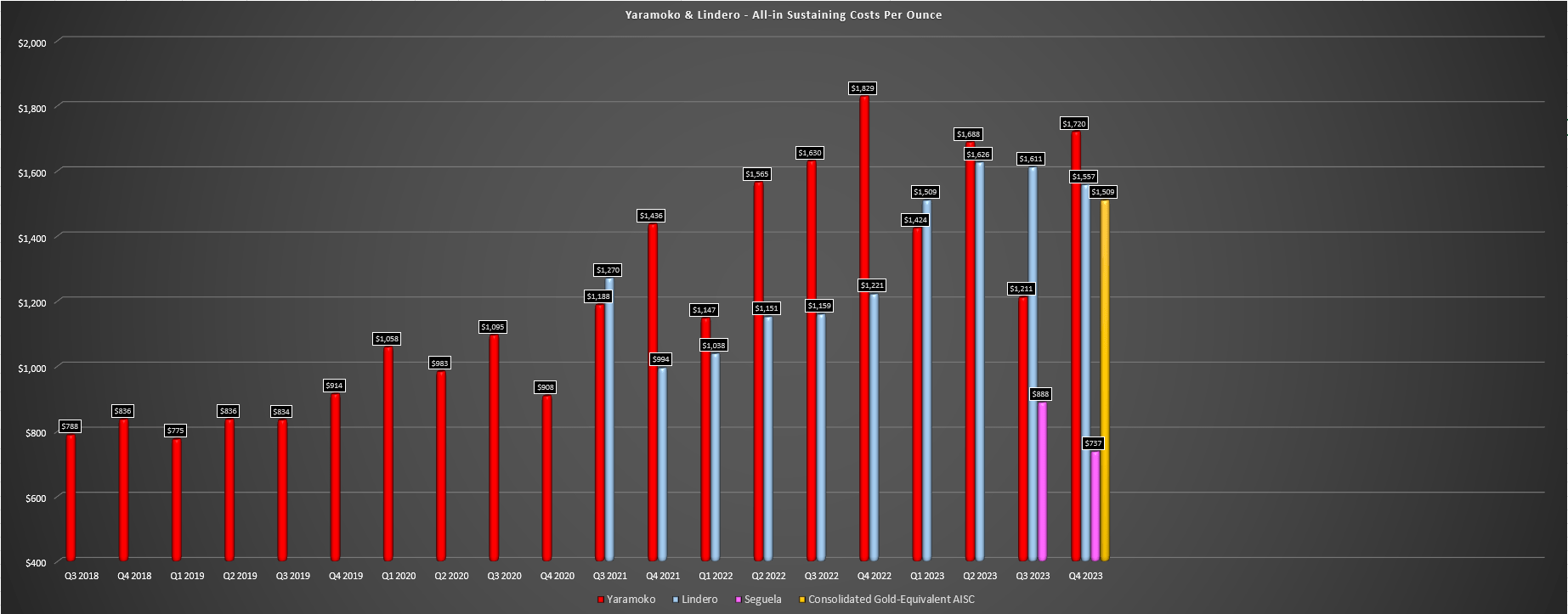

As for the company's Yaramoko Mine, production was higher at ~117,700 ounces of gold at slightly lower AISC of $1,499/oz (FY2022: ~106,100 ounces at $1,529/oz). The increased production was related to higher grades (6.81 vs. 6.37 grams per tonne of gold) year-over-year and annual AISC benefited from increased ounces sold, which offset higher sustaining capital in the period. The good news is that Yaramoko should have a better 2024 with higher grades and lower sustaining capital, with similar production expected at more competitive costs.

In Argentina, Lindero had a tough year with ~101,200 ounces of gold produced at $1,565/oz, which compared unfavorably to ~118,400 ounces at $1,140/oz last year. This was related to lower grades, inflationary pressures and higher sustaining capital, with sustaining capital elevated because of work on a heap leach expansion which is currently 23% complete. Given the elevated spending this year, Lindero's costs are expected to come in above $1,800/oz.

San Jose Mine - Company Website

Finally, San Jose had a disappointing year overall, with production of ~4.66 million ounces of silver and ~28,600 ounces of gold. This was significantly lower than the ~5.76 million ounces of silver and ~34,100 ounces of gold produced in 2022 and costs soared 28% to $19.40/oz vs. $15.11/oz in the year-ago period. Fortuna noted that the lower production was related to unfavorable reconciliation of silver/gold head grades to reserves and the impact of the 15-day illegal blockade.

However, the more disappointing news is that mineral reserves will be exhausted by year-end (mid-2025 previously), which shouldn't be a surprise to investors because, as I noted last year, there was going to be a significant hurdle to replace reserves at the mine given the impact of a stronger Peso, higher labor costs, and already high metals price assumptions. This resulted in an impairment charge of $90.6 million.

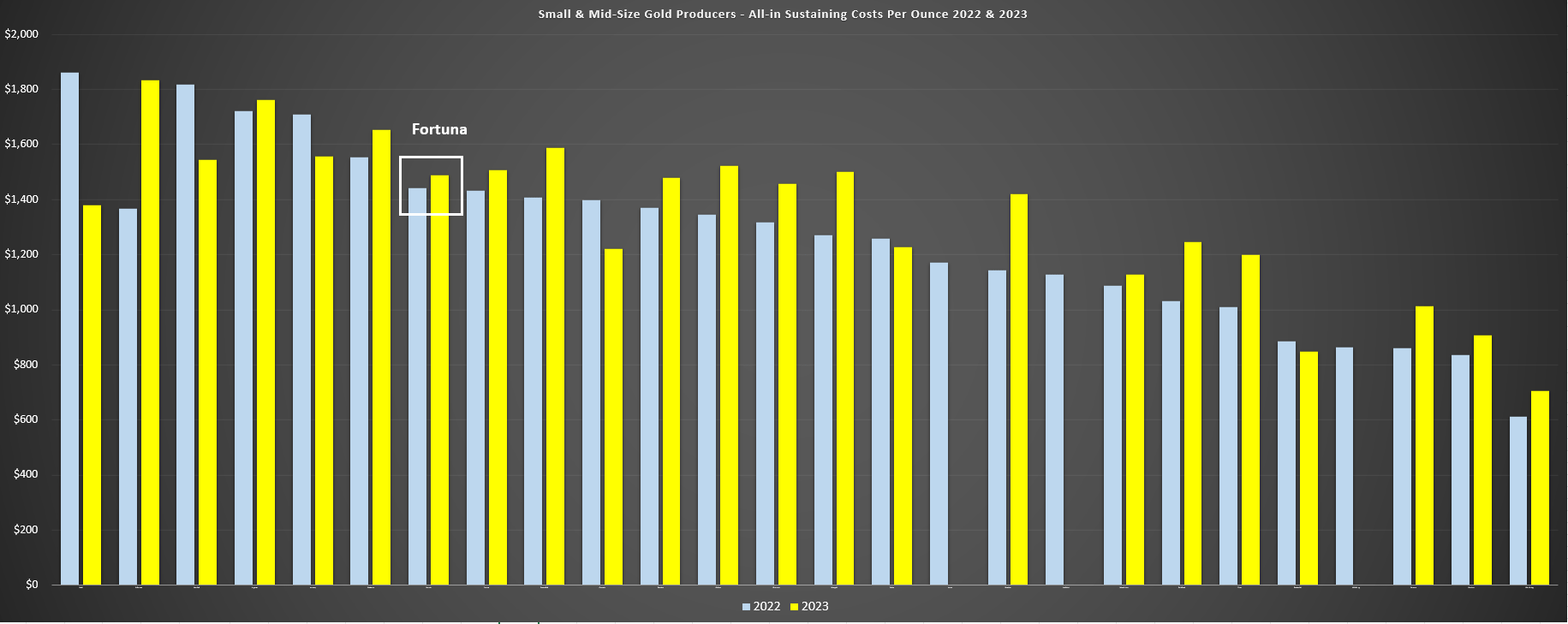

Looking at costs and margins, it wasn't a great year for Fortuna, even with the benefit of bringing a new high-margin mine online. This was evidenced by all-in sustaining costs increasing 5% year-over-year to $1,508/oz (FY2022: $1,431/oz) and coming in well above the industry average among the small and mid-size producer peer group. The higher costs were related to higher costs at its San Jose, Caylloma and Lindero mines, offset by lower-cost production from Seguela and Yaramoko. Fortunately, a higher average realized gold price allowed Fortuna to generate AISC margins of $440/oz (~23%) in 2023, an improvement from $371/oz in 2022 (~21%).

Fortuna Silver AISC vs. Peers - Company Filings, Author's Chart

Digging into the Q4 results, Fortuna's consolidated AISC came in at $1,509/oz (Q4 2022: $1,579/oz), translating to AISC margins of $481/oz (~24%). And while maintaining costs at these levels would have resulted in meaningful margin expansion this year, we will see higher costs in 2024 for reasons outlined previously, with AISC likely to come in closer to $1,600/oz this year.

On a positive note, gold and silver prices are making up for some of this weakness, setting Fortuna up to improve its AISC margins year-over-year if metals prices continue to cooperate. A look at Fortuna's all-in sustaining costs at each of its gold mines is shown below, with elevated at costs at Yaramoko and Lindero offsetting the ultra-low costs at Seguela in the most recent quarter.

Fortuna's Gold Mines Quarterly AISC - Company Filings, Author's Chart

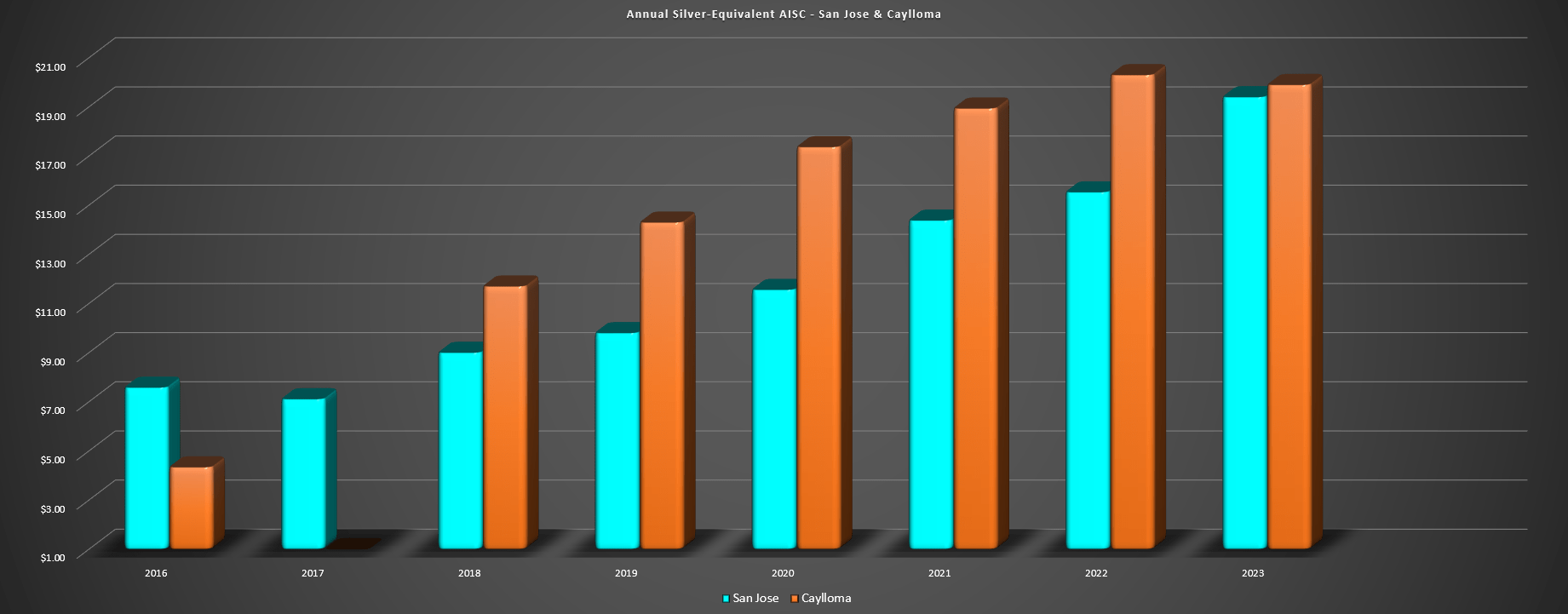

Finally, while many investors may have parked themselves in Fortuna given its title (Fortuna Silver Mines), it's important to note that the silver exposure here is de minimis, and the margins on the silver production are razor-thin if we do give the company credit for its relatively small silver production profile. This is shown below, with AISC rising to $19.40/oz and $19.90/oz per silver-equivalent ounce at its San Jose and Caylloma mines last year. And as noted previously, over 80% of this silver production is set to head offline within 12 months as operations wind down at San Jose.

And while this is certainly offset by bringing a high-margin gold mine online in Seguela, it is not ideal from a multiple standpoint given that Fortuna's former silver premium will not help the company in this cycle, suggesting that there's no reason the stock should trade in line with historical multiples given that it will now be an average cost primarily West African producer. We'll discuss this more in the valuation section later.

Annual Silver-Equivalent AISC - San Jose & Caylloma - Company Filings, Author's Chart

As for recent developments, Fortuna noted that it continues to focus on debt reduction and it's certainly make solid progress on this front over the past year. In fact, the improved balance sheet and higher gold prices should allow Fortuna to be net cash positive later this year, joining peers like Centerra Gold (CGAU), Alamos Gold (AGI) and several Australian producers. And as for capital expenditures, the company has another busy year of exploration planned across the portfolio, with 40,000+ meters planned at Diamba Sud with the hope to provide a PEA by year-end.

Meanwhile, the company plans to drill over 190,000 meters across the portfolio, with ~42,000 meters planned at Seguela to test underground targets at Sunbird, Ancien, and Koula, in addition to testing earlier stage targets like Barana, Badior and Kestrel. Overall, the focus on drilling at Seguela makes a lot of sense given the impressive hit rate here and the potential to maintain a ~150,000 ounce per annum operation longer-term here with higher throughput and a more optimized grade profile vs. average production of ~120,000 ounes envisioned in the 2021 FS.

“Our capital allocation priorities continue to be centered on providing maximum balance sheet flexibility through further debt reduction, and funding of aggressive organic growth programs with approximately 200,000 meters of exploration drilling planned across the portfolio. The Diamba Sud project in Senegal and the Séguéla Mine in Cote d'Ivoire are priorities for our exploration programs during the year.”

- Fortuna Silver Mines CEO, Jorge Ganoza.

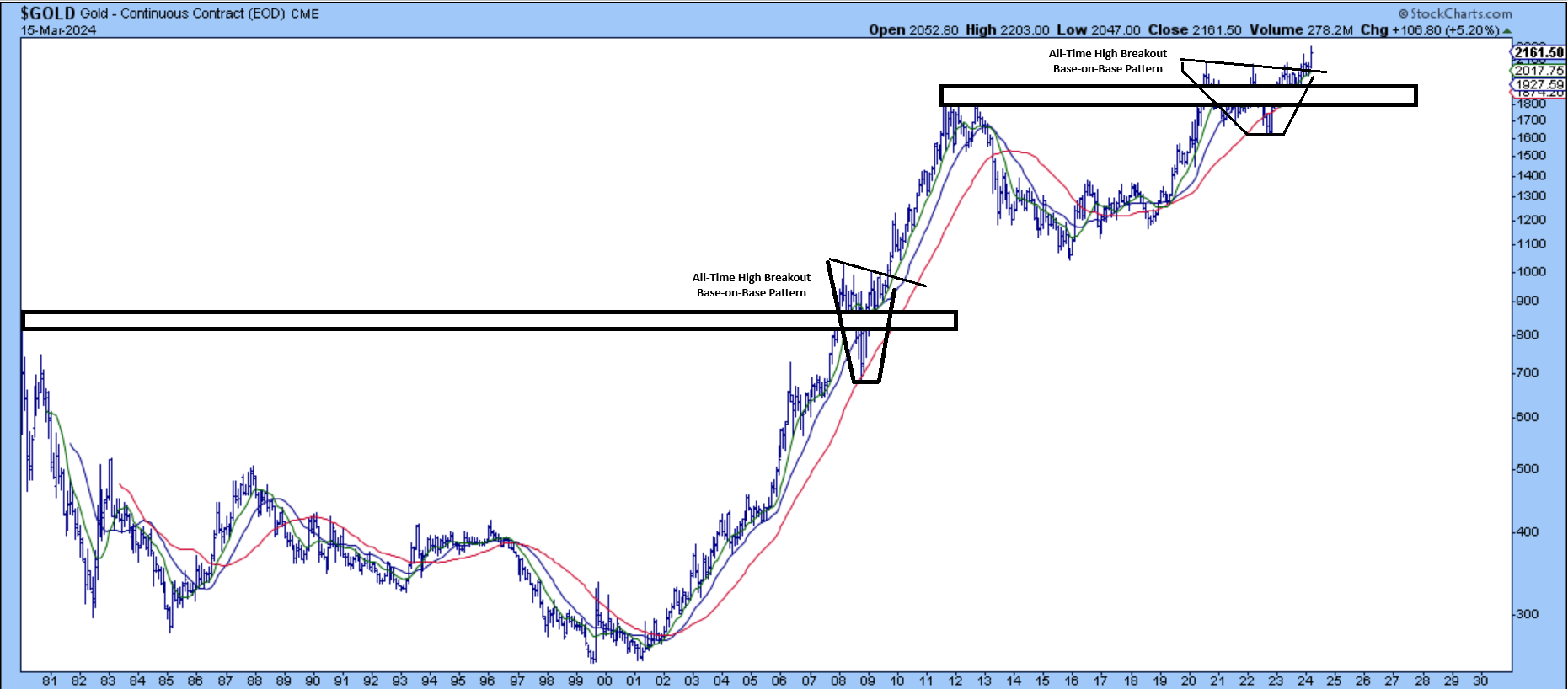

As for other recent developments, the major one is the gold price, which looks to be breaking out of a base-on-base pattern and has moved to new all-time highs. This is certainly a positive development for Fortuna given that it's transitioned into primarily a gold producer and the stronger gold price should help it to report another year of AISC margin expansion in 2024. So, while there were certainly some negatives this year like the earlier than planned cessation of mining at San Jose, these have been offset by continued exploration success at Seguela and the stronger gold price which has set Fortuna up to enjoy another year of significant free cash flow generation.

Let's look at the stock's valuation below:

Gold Price Long-Term View - StockCharts.com

Based on ~309 million fully diluted shares and a share price of US$3.40, Fortuna trades at a market cap of ~$1.05 billion and an enterprise value of ~$1.1 billion. This leaves it trading at ~4.0x FY2024 P/CF estimates and ~0.80x P/NAV based on an estimated net asset value of ~$1.33 billion. This would be a very attractive valuation if Fortuna was still a silver producer focused on Tier-2 ranked jurisdictions, but this is not the case today with the bulk of gold production coming from Tier-3 ranked jurisdictions (Cote d'Ivoire, Burkina Faso), and minimal silver contribution in its 2024 outlook with ~4.5 million ounces of silver production expected in 2024, representing less than 15% of 2024 revenue and with this figure set to decline to ~5% in 2025. Plus, while the previous outlook was for significant production growth, Fortuna will actually see production decline meaningfully in 2025 vs. 2024 levels, impacted by the cessation of mining at San Jose, lower production at Yaramoko and flat to lower production at Seguela.

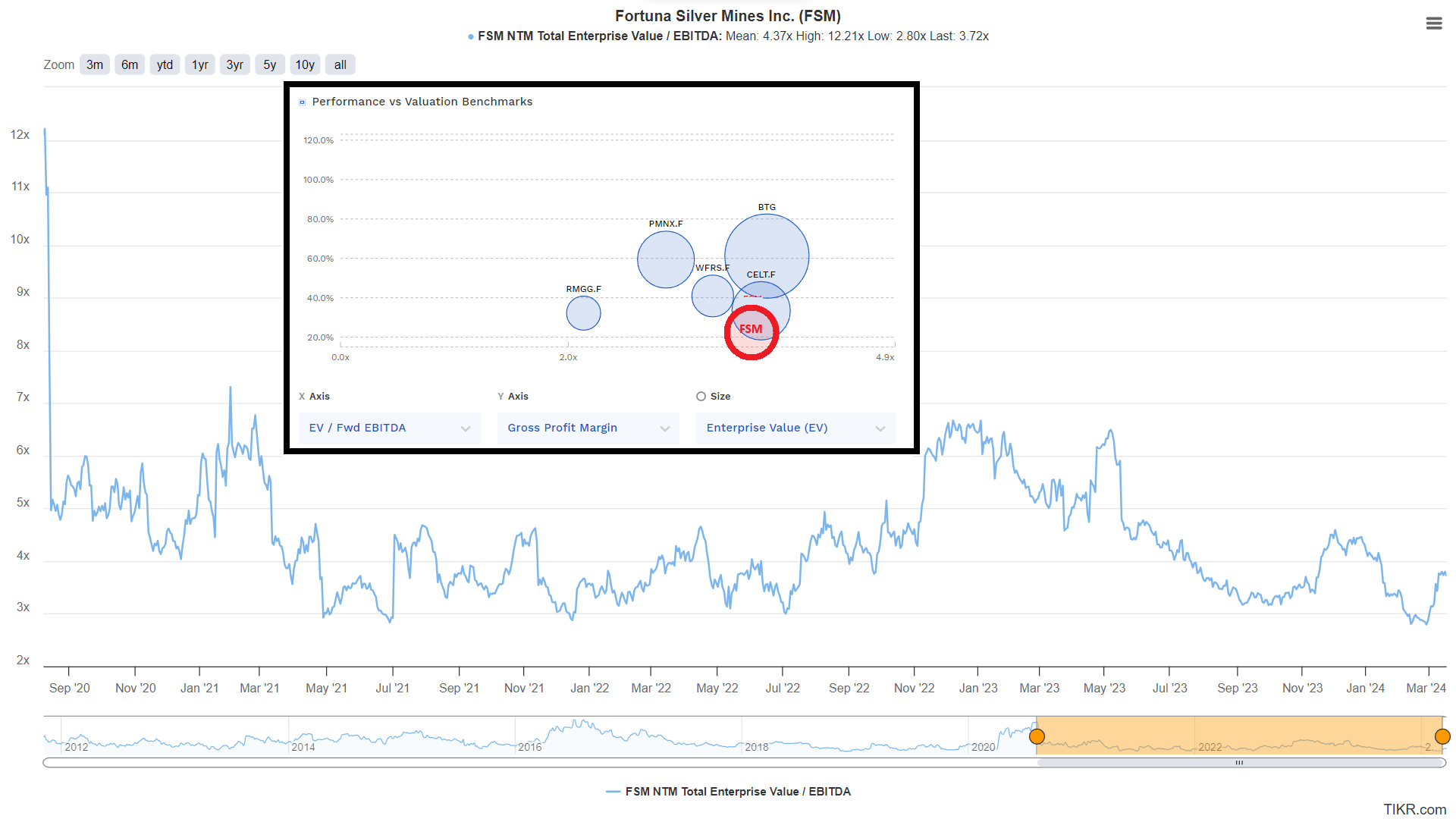

Fortuna Silver Valuation & Valuation/Margins vs. Peers - TIKR, FinBox

Using what I believe to be more conservative multiples of 5.5x forward cash flow given its significant exposure to West Africa and 0.90x P/NAV and a 65/35% weighting (P/NAV vs. P/CF), I see an updated fair value for Fortuna of US$3.95. This points to a 16% upside from current levels, making Fortuna one of the least attractively valued West African gold producers. And while Fortuna remains in the lower portion of its multi-year range from an EV/EBITDA standpoint, I believe much of this multiple compression is warranted given that is no longer a meaningful silver producer with San Jose set to head offline. In fact, if we look at where Fortuna trades relative to West African gold producer peers, it's actually one of the more expensive names when adjusting for margins, with it having the lowest AISC margins of the peer group (FY2023: ~23%). And as the chart above shows, Perseus Mining (OTCPK:PMNXF) and B2Gold (BTG) are far higher margin opportunities (40%+ AISC margins) with a track record of consistent per share growth available at lower/similar multiples than Fortuna.

I have lowered my P/NAV multiple to derive FSM's price target from 1.0x to 0.90x given the reduction in overall silver exposure and the fact that the company is largely a West African gold producer.

So, is the stock a buy?

While a rising tide will lift all boats and a higher gold price could easily push FSM back above US$4.00 per share, I prefer to buy at a deep discount to fair value or pass entirely. This is especially true when there are more attractive relative value opportunities, and B2Gold (BTG) certainly stands out as one of these opportunities with it trading at less than 5x FY2025 free cash flow estimates as a ~1.2 million ounce producer with an industry-leading cost profile.

In fact, B2Gold is set up to generate ~$1.3 billion in combined free cash flow in 2025 and 2026 combined, a massive figure when compared to its current enterprise value of ~$2.9 billion. So, with a ~6.3% dividend, a low single-digit free FY2025 free cash flow multiple and an impressive track record of creating value for shareholders, I think it's the far more attractive bet if I were looking to deploy new capital in the sector today.

Fortuna Silver had a satisfactory year overall, but the start of production at Seguela was partially offset by the reality that its time as a silver producer is coming to a close. This was evidenced by a shortened mine life than expected at San Jose and a significant impairment charge and I would expect this to impact the stock's multiple as it transitions into being a primarily West African gold producer.

And while there's absolutely nothing wrong with focusing on West Africa where the discovery costs are low, permitting is quick, and the ounces are plentiful, West African gold producers trade at a far lower multiple than their peer group, and Fortuna Silver Mines Inc. is not nearly as cheap as peers when adjusting for this transition. So, with a far greater margin of safety in names like B2Gold and i-80 Gold (IAUX) which are trading near multi-year lows, I much prefer these two names if I were putting new capital to work in the sector today.