BlackJack3D/E+ via Getty Images

BlackJack3D/E+ via Getty Images

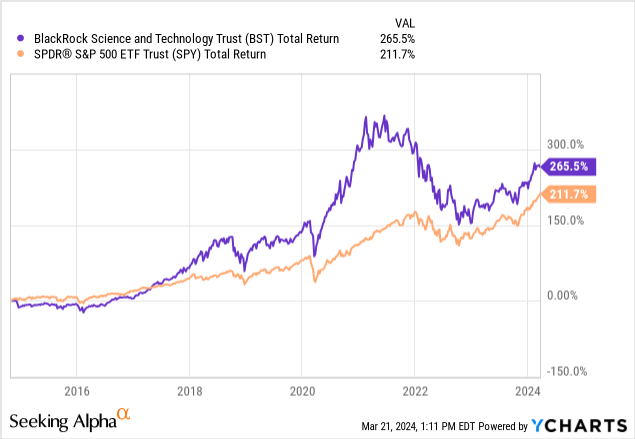

The BlackRock Science and Technology Trust (NYSE:BST) is an equity closed-end fund that invests in the technology sector. The fund has performed well since its inception in 2014, beating a variety of equity benchmarks along the way. Managed by BlackRock, the world's largest asset manager, BST has been a top performer in the technology closed-end fund sector.

BST's value proposition is simple, invest in the best technology companies around the globe and use a yield enhancement strategy to generate additional income-based returns. Adding to the mix, BlackRock (BLK) uses the vehicle to invest in private investments, which we will discuss. BST has delivered, paying a steady monthly dividend since the fund's inception. Given today's investment environment, a fund with a current yield above inflation supported by growth potential is a highly attractive opportunity.

We've previously discussed BST in-depth, reviewing its outperformance of equity benchmarks but cautioning around valuation concerns and the fund's use of private investments.

BST allocates its portfolio to market leaders throughout the global tech sector. BST further enhances returns with a covered call strategy. Covered calls generate additional income by selling options over owned positions. Despite capping upside, covered calls can provide additional returns during stagnant markets or down periods. Covered calls are a conservative options strategy and are frequently used as a yield enhancement technique for closed-end funds.

BST is large with over $1.3 billion in assets. BST is organized as a perpetual fund, meaning shares will continue to trade for the foreseeable future. The fund currently has 101 holdings as of the end of February 2024. The number of holdings has reduced from 134 to 101 since our initial coverage in 2021, meaning BST's portfolio has become more concentrated. BST is not a leveraged fund, but management notes approximately 33% of the portfolio is overwritten by call options.

BlackRock

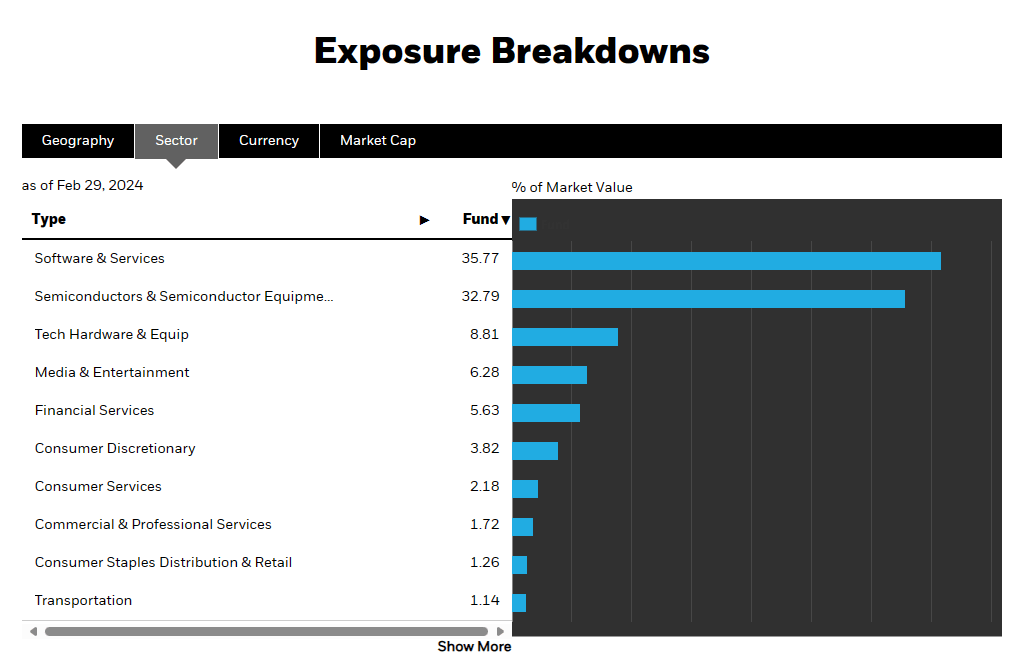

Sector allocations remain technology-oriented with software (36%) and semiconductors (33%) accounting for most of BST's holdings. Other notable sectors include hardware & equipment (9%) and media & entertainment (6%). The portfolio is split between publicly traded large capitalization companies and a sleeve of privately funded venture investments.

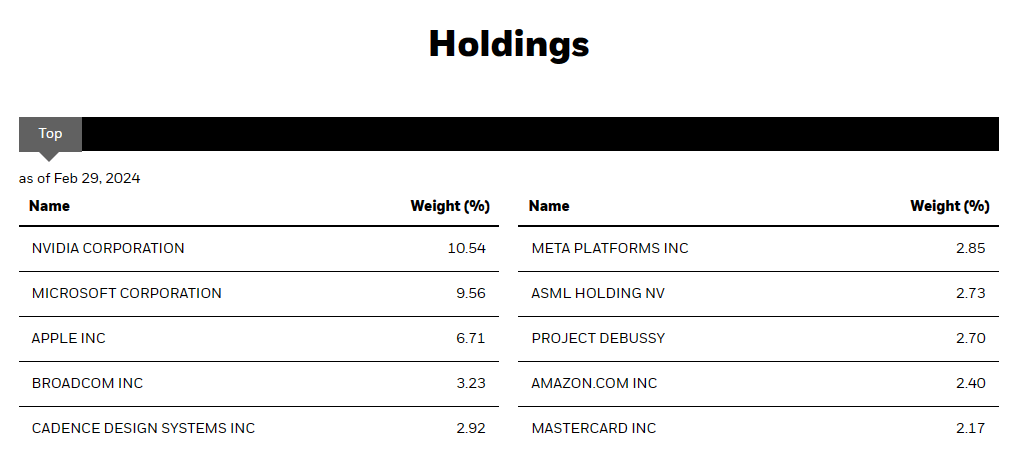

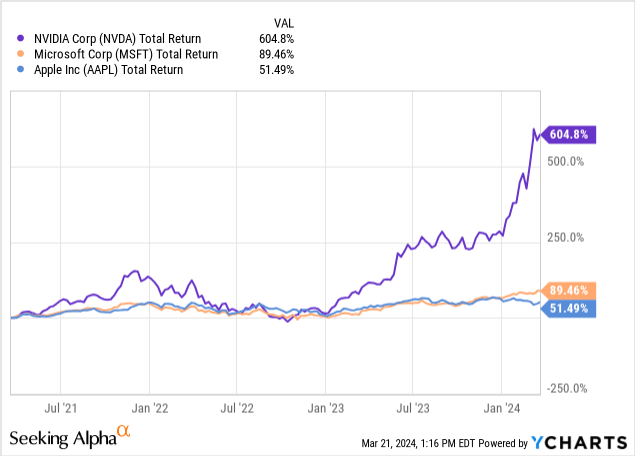

The fund's top ten holdings are recognizable names including Nvidia (NVDA), Microsoft (MSFT), Apple (AAPL), and Broadcom (AVGO). BST's portfolio has become increasingly concentrated towards the top holdings. Currently, BST has approximately 25% of its portfolio allocated to the top three holdings, including more than 10% to NVDA alone.

BlackRock

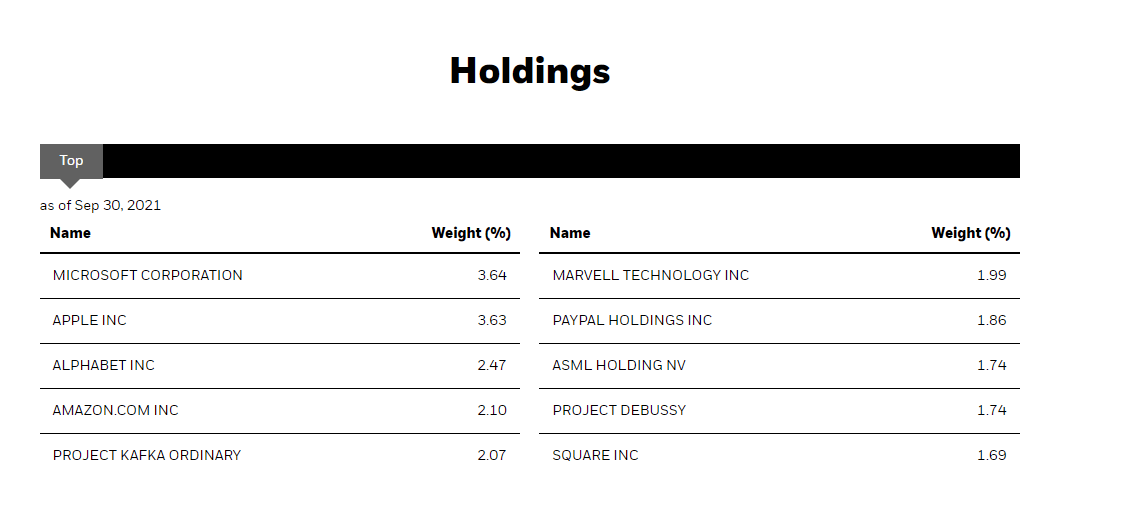

Compare this concentration to the portfolio before interest rates began to climb. In the third quarter of 2021, only 10% of the portfolio was allocated to the top three positions.

BlackRock

As we mentioned, BST also funds private, venture investments. BST's structure as a closed-end fund is a good match for illiquid investments like early-stage venture opportunities. In the top ten holdings is Private Debussy, representing 2.7% of the portfolio. Debussy and similar investments are opaque, but with some digging, we can uncover details. For example, according to the report of BST's sister fund, the BlackRock Science and Technology Term Trust (BSTZ), Project Debussy is an investment in a software company called Databricks. The report also provides information on other private investments in BST's portfolio, including updates on their valuations.

However, even considering this additional information, these private investments present unique risk factors. The chief risk factor is the unreliability of their net asset value calculations and their dependence on the availability of funding. The valuation of illiquid securities is complex and often reliant upon blending forecasts with historical data. Unfortunately, macroeconomics has changed so dramatically over the past several years that the accuracy of these early-stage valuations is unreliable.

The fund's lack of leverage is also critical given the use of private investments. Without leverage, BAST mitigates liquidity risk for the private sleeve, leaving the distribution as the primary risk to the fund's net asset value. This allows BST to continue holding a small portion of its portfolio in illiquid investments through volatile periods.

BST's allocation to illiquid private investments is much smaller than BSTZ's. Prospective investors may consider this important difference along with the difference in fund term and dividend distribution as key differentiators.

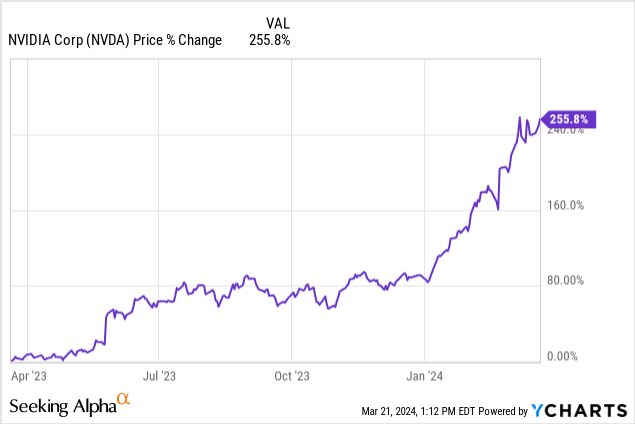

BST has seen incredible performance driven by the technology sectors run. Tailwinds stemming from AI combined with global semiconductor demand have propelled the sector to unforeseen highs. The portfolio's largest holding, NVDA, is one of the most successful stocks in the S&P 500.

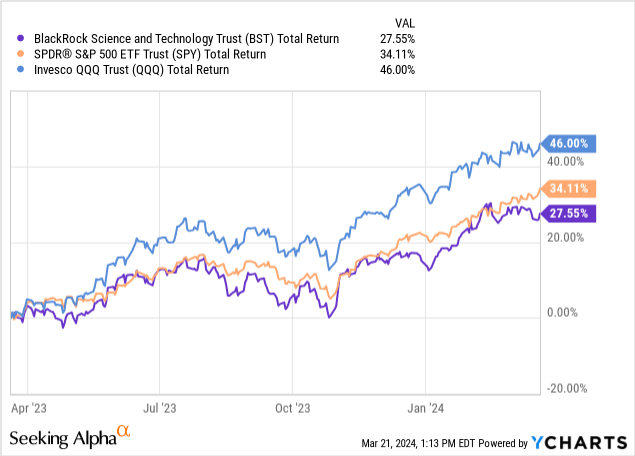

BST has also performed well as compared against the S&P 500, capitalizing largely on its tilt towards outperforming sectors. In contrast, BST has been unable to keep up with the Invesco QQQ Trust ETF (QQQ), which has outperformed significantly over the past twelve months.

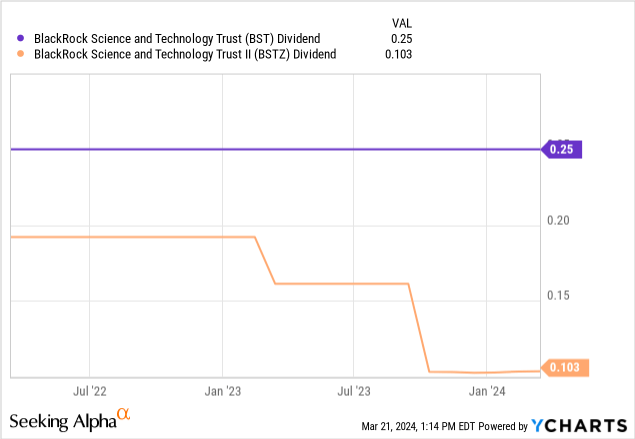

BST distributes a level monthly dividend sourced from dividends, capital gains, and proceeds from call options. BST delivers a level monthly dividend of $0.25 per share, which is different than BSTZ's variable dividend based on trailing NAV. Prospective investors may consider this as another key difference between the two funds.

Many income focused investors will look to BST as a superior choice given the stability of the dividend. BST has maintained the dividend distribution since inception, while BSTZ was forced to change the distribution policy. BSTZ reduced the distribution largely due to the slowing of private equity markets, allowing the distribution to move alongside NAV.

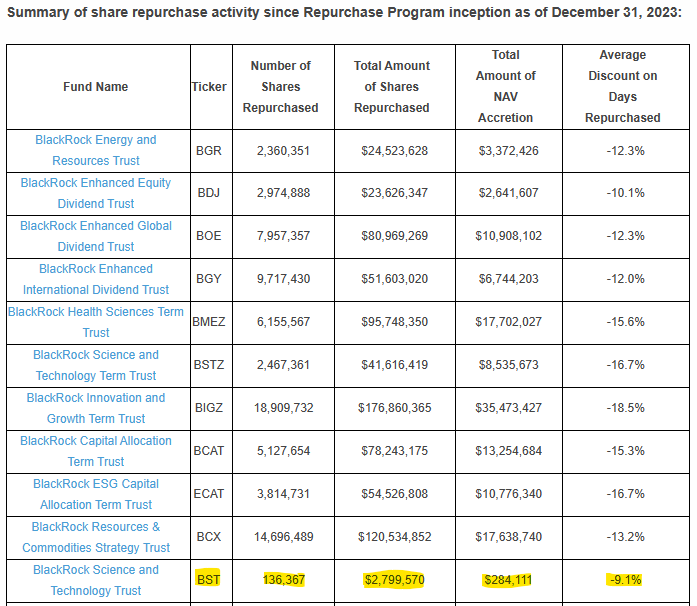

BLK has also employed a secret weapon in enhancing their closed-end fund lineup. The BlackRock lineup has a large share repurchase initiative which allows the funds to repurchase shares at a discount to net asset value. Repurchasing shares below net asset value is accretive to the fund, enhancing shareholding metrics in isolation.

Business Wire

Since the inception of the buyback program, BST has repurchased 136,367 shares, amounting to nearly $2.8 million dollars. The average daily discount was 9.1%. Note that BST has been successful even during the rising rate environment. As a result, the repurchase program is considerably smaller than other funds including BSTZ.

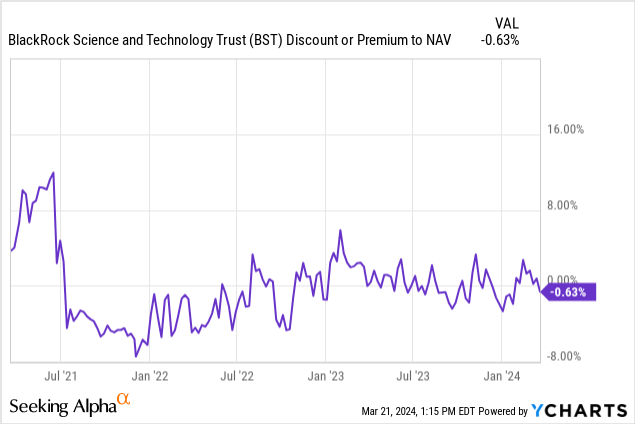

Based on current share prices, BST pays an 8.3% dividend distribution. The yield is compelling given the NAV growth coming from tailwinds in the technology sector. BST currently trades at a small discount to net asset value of approximately 1%. The fund's valuation varies so investors may find it more compelling to wait for a pricing discount to move. Even still, the fund's NAV is not entirely transparent given the allocation to private investments.

As with most funds from the manager, BST is inexpensive. The gross expense ratio of the fund is 1.00% and all in expenses are 9bps higher at 1.09%. The fund has no leverage expenses, reducing the shareholder burden.

BST has given shareholders a variety of reasons to be happy. As we mentioned, the trailing twelve months' performance of the fund's top holdings has powered a substantial amount of the total return.

With the portfolio heavily concentrated on these three names, investors may be left wondering how much room is left to run. These companies have fully priced valuations. The spotlight may now turn to BST's covered call strategy which can continue generating premiums by writing call options over positions that may stagnate. While the AI boom continues to rage, BST has a variety of levers to pull including options and buybacks to maximize the value for shareholders.

However, BST has an entirely different tailwind which remains locked up. The valuation and transactability of the fund's venture investments are largely dependent on the health of the IPO market. With financing costs increasing significantly over the past two years, many companies have shelved their plans to go public. Even worse, the increase in the cost of capital means many early-stage ventures have struggled to lock in the financing required to grow.

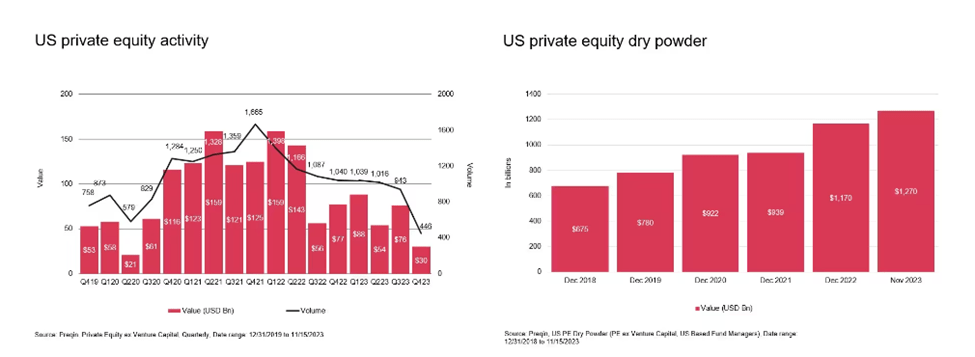

As interest rates appear to have peaked, there is optimism surrounding the health of the IPO market. PWC recently put out a report discussing the health of private equity.

In 2023, private equity (PE) activity remained sharply down from its pandemic peak, reflecting stubbornly high inflation and correspondingly elevated interest rates and capital costs. Despite sitting on unprecedented capital, investors remained cautious, awaiting reductions in asset valuations to reflect cooler demand and tighter financing. Vendors, for their part, are willing to wait for the right suitor, extending hold periods to maximize exit value.

We expect many of these factors to persist in 2024. In this context, value creation (both driving growth and expanding margins) will remain critical, both to justify cost-of-entry for new investors, and to achieve target internal rate of returns (IRRs) for owners on high-priced deals made during the frothy pandemic market. In addition, we see cash management and creative deal structuring coming into ever sharper focus, as elevated interest rates and costly credit become the new normal.

Putting this together, we see three key trends which will define private equity for 2024 and beyond:

- A blurring of the lines between investor and operator: The critical need to drive value creation - both top line and bottom line - will take many PEs beyond their traditional comfort zone, forcing a more hands-on approach with a corresponding need for greater operating capacity and capability.

- A relentless focus on cash and profitability: While continuing to drive growth, management teams will need to have an ever-closer eye on cash and operations, requiring CEOs to deliver margin expansion whilst continuing to drive growth, and further elevating the CFO role.

- An increased need for creativity and flexibility in dealmaking: With credit continuing to be expensive, investors will need to be creative, focusing on smaller deals or minority investments, and potentially increasing equity checks.

Despite the underlying headwinds, fund managers continued to amass capital. The decrease in activity over the past two years presents an opportunity to place new capital in new ventures which may prove profitable. Additionally, the dry powder could provide relief for existing ventures in later stages. Improvement in financing conditions will prove crucial for BST's private equity sleeve to deliver.

PWC

BST is a fund that largely speaks for itself. BST has delivered a reliable monthly distribution to shareholders with a portfolio of blue-chip technology companies combined with private investments. Those seeking exposure to the technology sector in an unconventional fashion may consider BST. Additionally, those looking for an investment to complement their value-oriented index funds which supplement with income may find BST's value proposition compelling. BST is attractive to investors of all shapes and sizes, hence why the fund has remained over $1 billion in assets.