MarsBars

MarsBars

Real estate continues to be a good way to accumulate wealth and income over the long run, and while owning commercial properties is out of reach and/or unrealistic for most retail investors, REITs offer a great alternative.

This brings me to Retail Opportunity Investments Corp. (NASDAQ:ROIC) which is a high quality U.S. West Coast-focused shopping center REIT that appears to be undervalued.

I last covered ROIC in November, highlighting its undervaluation and strong fundamentals, and it appears that the market has somewhat agreed, with the stock rising by 6.2% since my last piece

Nonetheless, ROIC is down by 8% since the start of the year and down by 9% over the past 12 months, as the brief market rally around income stocks has fizzled in favor of growth stocks.

In this article, I revisit ROIC including key updates on how the company is faring in the current environment as it relates to same-store portfolio growth, occupancy and tenant demand, and whether if it still fits my last 'Buy' thesis on the stock at the current valuation, so let's get started!

Retail Opportunity Investments Corp. is a shopping center REIT that focuses on owning properties in densely-populate metropolitan areas across the U.S. West Coast. It currently has 94 shopping center comprising 10.6 million square feet of gross leasable space. As shown below, ROIC has a presence in all major markets along the west coast in Washington, Oregon, and Norther/Southern California.

Investor Presentation

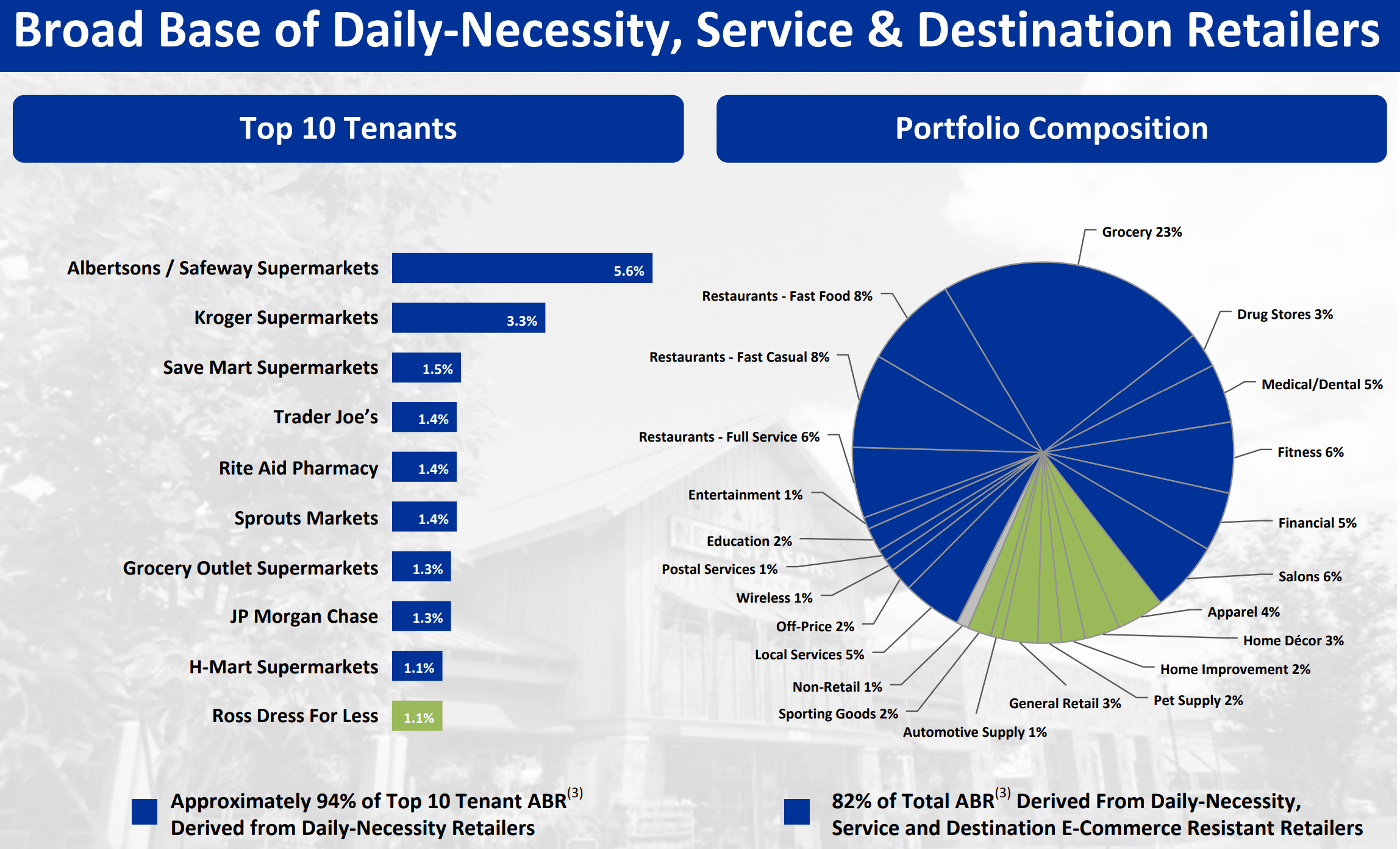

ROIC has one of the highest portfolio leased rates compared to peers, at a 97.7% rate and stands out for having the highest percentage of properties being grocery and/or drug-store anchored at 97%, making the vast majority of its centers being necessity based and thereby less resistant to e-commerce and/or recessions.

As shown below, ROIC’s top tenants represent a cross section of popular supermarkets including Safeway (ACI), Kroger (KR) and Sprouts Farmers Market (SFM), and 82% of annual base rent is derived from daily-necessity and/or service-based tenants that are e-commerce resistant.

Investor Presentation

Meanwhile, ROIC continues to demonstrate portfolio growth in its last fourth quarter earnings report released on February 14th. My key takeaways from the report include respectable same-store NOI growth combined with a strong portfolio occupancy rate and encouraging lease spreads, signaling strong tenant demand for ROIC's desirable locations, as described in more detail below.

This is reflected by same center cash NOI growing by 3.3% and 3.7% YoY for the fourth quarter and full-year 2023, respectively. While the portfolio leased rate dipped slightly by 50 basis points since the end of Q3 when I last visited the stock, it still remains healthy at 97.7%. Notably, ROIC has maintained a portfolio leased rate above 96% over the past 10 years.

While the broader commercial real estate market has seen plenty of headwinds over the past 12-18 months, driven primarily by higher vacancy rates in office properties, ROIC’s core focus on grocery-anchored properties remain sound. This is especially true for its West Coast focus, where properties are highly sought after and remain supply constrained, as reflected by record leasing activity in 2023 for 1.7 million square feet.

This enabled ROIC to achieve rent growth for the 11th consecutive year, including 7% increase in rents on renewal leases and 22% rental increase on new leases. As shown below, ROIC’s rent spreads on new leases in the 2022-2023 timeframe are at the highest level since 2018.

Investor Presentation

Looking ahead, ROIC may see additional acquisition opportunities materialize in 2024, as management is seeing more interest from private owners being willing to transact. This includes a property that was acquired in December in densely populated neighborhood in Los Angeles at a cap rate in the 6s for what management considers to be irreplaceable real estate.

One of the things that I would focus on for 2024 is to see if management is able to opportunistically transact in the current market, which may be tough as some private market owners may be unwilling to transact at higher cap rates in this high interest rate environment, opting instead to hold out for better pricing down the road.

As such, I would pay close attention to acquisition activity over the next few quarters to see if management is able to transact at cap rates above 6%, which would generally mean accretive growth for ROIC in this higher interest rate environment. While the absence of meaningful external growth opportunities in the near-term wouldn't necessarily derail my ending thesis on the stock, it is something worth monitoring for investors who prize a higher level of growth this year.

ROIC is supported by a strong balance sheet with a BBB- investment grade credit rating from S&P. It also has a safe debt-to-total assets ratio of 40%, which has declined every year since 2020, at which time it was 44%. Its net debt-to-EBITDA ratio has also declined every year since 2020 from 7.5x to 6.2x at present. Its debt maturities are well-laddered, with about $300 million in maturing debt each year through the next 5 years.

Risks to ROIC include tenant-specific risks such as its leases related to Rite Aid. 3 of ROIC’s 15 Rite Aid stores closed during the fourth quarter, which was the driver behind the sequential 50 bps drop in the leased rate to 97.7%. While this presents near-term risks, it also gives ROIC opportunities to re-lease the properties at a higher rate. Other risks include higher-than-expected interest rates which introduces refinancing risk, which could raise interest expense.

This could be mitigated by continued deleveraging of the balance sheet as ROIC has the potential to get down to a leverage ratio below 6x based on the aforementioned downward trend since 2020. This is supported by a 57% dividend payout ratio, leaving ROIC with plenty of retained capital to support debt paydown and/or opportunistic growth.

Turning to valuation, I continued to see value in ROIC at the current price of $12.93 with a 4.6% dividend yield and a forward P/FFO of 12.2, sitting far below its normal P/FFO of 16.5. ROIC saw a mid to high-single digit average annual FFO/share growth rate prior to the pandemic, and I would expect for ROIC to be able to achieve a mid-single digit FFO/share annual growth rate in the medium term driven by rental increases and external growth through acquisitions.

While sell side analysts who follow the company expect flat YoY FFO/share growth this year, they expect growth to resume in 2025-2026 with 4.4% to 7.8% annual FFO/share growth. With these data points in mind, I would expect for ROIC to trade at a forward P/FFO in the 14-16x range, which takes into consideration potential headwinds from the current higher interest rate environment as well as the strong demand trends from tenants and positive forward growth outlook.

As such, while I don't view ROIC as being as big of a bargain as it was since I last visited the stock when it was trading 6% lower, I continue to see value in it at the current price for the aforementioned reasons.

FAST Graphs

Lastly, ROIC also appears to be cheap compared to most of its shopping center peers, despite having a presence in desirable markets. For this exercise, I use EV/EBITDA since it includes both the value of equity and debt for an apples-to-apples comparison.

As shown below, ROIC's 15.3x EV/EBITDA sits below that of Kimco Realty's (KIM) 19.0x, Regency Centers' (REG) 19.1x, Kite Realty Group's (KRG) 17.4x, and sits just slightly above Brixmor Property Group's (BRX) 14.9x. For reference, KRG and BRX are more focused on secondary markets, unlike ROIC, KIM, and REG, which are more focused on Tier 1 markets.

ROIC vs. Peers EV/EBITDA (Seeking Alpha)

Overall, ROIC’s strong fundamentals and track record of high occupancy make it a solid choice for income investors seeking stability in their portfolio. ROIC remains a bargain at its current price and offers potential for solid total returns from its dividend yield, forward internal/external growth prospects and a reversion to its mean valuation in the long term. Moreover, ROIC has exercised balance sheet discipline with its deleveraging, which better positions the enterprise in the current higher interest rate environment. Considering all the above, I maintain a 'Buy' rating on ROIC stock.