VeselovaElena/iStock via Getty Images

VeselovaElena/iStock via Getty Images

Readers may find my previous coverage published on 15 December 2023 via this link. My previous rating was a buy, as I believed Dutch Bros (NYSE:BROS) could continue to grow at a high pace and that the previous concern regarding its balance sheet was not going to be a hurdle to its growth. My previous thesis has played out pretty well, in that BROS continues to show strong growth in 4Q23, and that management is taking a serious approach towards its digital strategy. I am reiterating my buy rating for BROS as I am positive that it can continue to grow as guided and that there are positive catalysts that could drive acceleration in SSS growth.

BROS reported a strong 4Q23 quarter on 22 February 2024, growing revenue by ~26% to $227 million. Growth was driven by strong unit growth (23.8%), stemming from 37% growth in company units and 5.1% in franchise units. This strong growth performance was accompanied by improving profit margins, where the EBIT margin improved 300bps to 1.2% and the reported segment EBITDA margin expanded 250bps to ~9%. My key takeaway was that growth units growth continued to show strong traction, indicating that there is still room to grow. Also, importantly, BROS has shown that it is moving in the right direction in terms of profitability. Another noteworthy point is that BROS's balance sheet strength remained relatively stable vs. 3Q23, where it exited 4Q23 with a cash balance of $133.5, and gross debt only increased by ~$20 million.

Based on author's own math

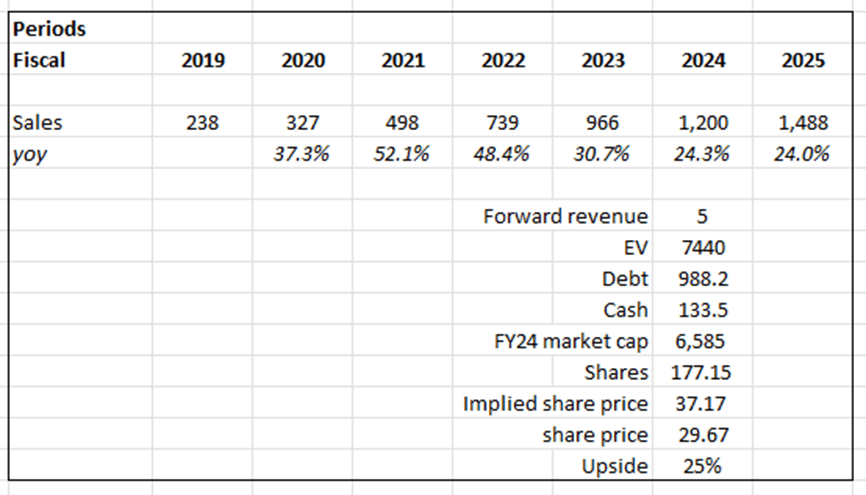

Based on my view of the stock, BROS still has 25% upside. BROS should have no issues printing strong growth ahead as the momentum in opening units (24% total unit growth in 4Q23) continues to be strong. SSS growth should also gradually improve from here, as 4Q23 showed a very positive improvement in traffic. The upside catalysts from ramp-up in digital strategy and roll-out of food products could further drive acceleration in SSS growth as well. Putting it together, I model BROS to grow 24% for the next 2 years (FY24 as per guidance and FY25 to continue with the same strength). I am not changing my valuation expectations, assuming BROS will continue trading at 5x forward revenue.

BROS's execution and performance were solid, and I expect this momentum to continue for the foreseeable future. For one, the business continues to show strong same-store sales [SSS] performance with improvements in traffic. In 4Q23, BROS reported SSS growth of 5%, driven mainly by company-owned store performance of 4.6%. While pricing was the main contributor (5% contribution), traffic has improved to flattish vs. last year, a 400bps improvement sequentially. I believe this was a strong sign of execution capabilities by the new CEO (Christine Barone).

Secondly, in the medium to long term, BROS's digital initiatives, such as mobile ordering and in-store payment, should provide a positive contribution to SSS growth. As I mentioned previously, major players like Starbucks (SBUX) have shown that mobile orders have a positive impact on growth. The announcement of a pilot test and the anticipated start of beta testing in the Arizona market indicate that management has taken the first significant step toward implementing this. I think the test will be an incredible success because BROS stores are perfect for mobile order-and-pickups because they have drive-through lanes in every store and these cool walk-up pickup windows that go well with covered outdoor seating. From a growth perspective, this would not only improve store utilization; it should also help to capture more orders as it is now much easier and more convenient for consumers to purchase (i.e., the friction to order or collect the drink is lower now). Data gathered from these mobile orders, where clients are required to create a profile, will complement BROS's new data-centric strategy for expanding their business. For reference, this strategy involves evaluating consumer demand and the factors that contribute to its growth using new datasets that consider demographics, proximity to other chains, proximity to existing shops, and AUV factors.

Lastly, the upside to SSS growth is when BROS starts to introduce food products. I believe this is a natural move for BROS, as there are successful precedents to show that it drives SSS. Using SBUX as the best competitor here, nearly 40% of beverages at Starbucks include food that is attached (SBUX 3Q23 earnings call transcript). However, in the case of BROS, this figure is 0%, which means there is a lot of space to expand. Adding food options should increase beverage sales even more, in my opinion because customers will have more of an incentive to visit the establishment if they know they can buy food to go with their drink. Given the new CEO's background at SBUX, where she oversaw the food division, there shouldn't be any issues with execution when launching food products. The problem with food is that it might take longer to prepare than drinks; hence, this is why the BROS roll-out of mobile-ordering digital functions is important. Ordering in advance allows BROS to prepare food and drinks in advance; hence, there is now a slowdown in productivity. This is particularly true for breakfast, where consumers are generally in a rush and want their order collected as soon as possible. As such, I think the priority for BROS is going to ramp up its digital strategy first, and once that is done, next is likely food. Both of these are key drivers for SSS growth acceleration.

New management carries risk, no matter how strong their pedigree is. In this case, execution is the key risk, as BROS needs to successfully ramp up its digital strategy before it can further leverage it to accelerate SSS. Another business risk is related to changes in consumer preferences. Given the brand image of BROS, it might not be so easy to change its product offerings to fit what a consumer wants. For instance, changing its main product offerings to fruit juice.

To conclude, I reiterate my buy rating for Dutch Bros, confident in its continued growth and potential for acceleration. BROS delivered a strong 4Q23, exceeding expectations with 26% revenue growth driven by robust unit expansion and positive SSS performance. Notably, the company maintained a healthy balance sheet with a stable cash position and minimal debt increase. The positive signs in traffic, improving from negative to flat year-over-year in 4Q23; the upcoming launch of mobile ordering; and potential introduction of food products make me feel more optimistic about BROS's growth outlook as well. Hence, I believe BROS is well-positioned to deliver on its guidance and achieve long-term growth.