d3sign/Moment via Getty Images

d3sign/Moment via Getty Images

Broadridge Financial Solutions, Inc. (NYSE:BR) is a leading financial technology company headquartered in Lake Success, New York. In this thesis, I will analyze its second-quarter results along with its future growth prospects. I will also be analyzing its valuation at the current price level and the upside potential in the stock price. BR has been experiencing consistent revenue growth along with continuous investment in technological advancement, giving it an edge over the competition. However, its valuation doesn’t leave significant room for an upside in stock price, and hence, I assign a hold rating for BR.

BR is a leading fintech company that provides technology-driven solutions for financial institutions, corporations, and mutual funds. Broadridge specializes in investor communication, securities processing, and data and analytics solutions. It assists companies in managing and distributing proxy statements, annual reports, and other shareholder communications. This includes services related to proxy voting, document processing, and shareholder outreach. It also offers solutions for trade processing, clearance, and settlement services to financial institutions. These services help streamline and automate various aspects of the securities lifecycle. Its data and analytics business provides data management and analytics solutions to help financial institutions make informed decisions. This includes tools for risk management, compliance, and business intelligence.

BR recently reported strong second quarterly results, with EPS beating the market estimates by 3.2% and revenues being in line with the market estimates. Revenues across business segments grew substantially, but the Capital Markets Solutions segment proved to be the outperformer, witnessing a 12% increase in revenues. As per my analysis, the company continues to experience strong demand, especially from the North American market. One point I would like to highlight is that it managed to improve its operating margins while growing its revenues at a solid rate, which I believe was difficult, especially in current high inflationary market conditions.

Investor Relations BR

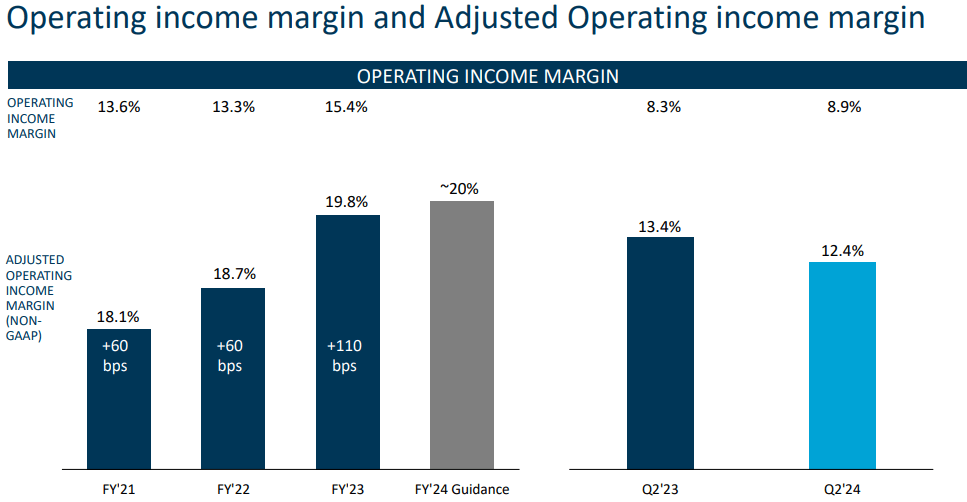

It reported total revenues of $1.4 billion, up 9% compared to $1.29 billion in the same quarter last year. I believe a 9% increase in recurring revenues was the primary revenue driver for the company. The most important thing is that the growth in revenues was largely organic, and the majority of it was from internal clientele portfolio growth, which also helped with cost savings. The operating income for the quarter stood at $124 million, a significant increase of 15% compared to $108 million in the corresponding quarter last year. This brings the operating margin to 8.9%, up from 8.3% y-o-y. A strong increase in the revenues complemented by controlled operating expenses resulted in this increase. The net income was reported at $70.3 million, a 22% increase compared to $57.5 million in the same quarter last year, reflecting diluted EPS of $0.59, compared to $0.48.

Now let us have a look at its balance sheet. As of December 2023, it reported cash and cash equivalent of $277 million against long-term debt of $3.65 billion. Here is where the real problem lies. Its long-term debt obligation skyrocketed from $2.2 billion in June 2023 to $3.65 billion in December 2023. High debt obligation could make future fundraising really difficult without putting significant stress on its balance sheet. High debt also results in increased interest expenses, putting a dent in its profit margin. For six months ending 31 December, it incurred $69.7 million in interest expenses, compared to $61 million in the same period the previous year, an increase of 14%. I would recommend investors consider this risk before investing in the company.

Investor Presentation BR

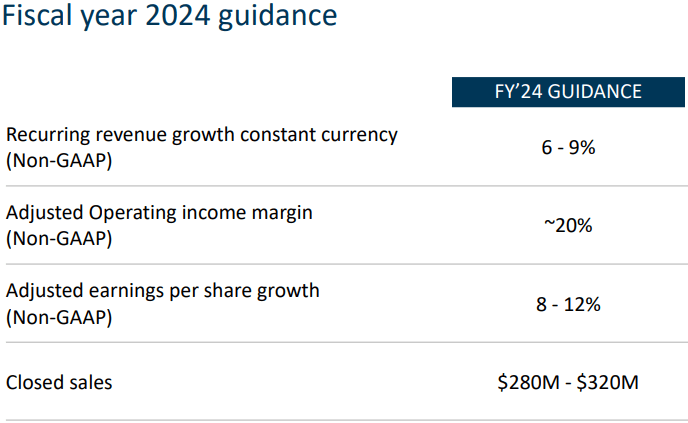

Overall, the company managed to outperform on multiple parameters, including revenue and profit growth. The management has not changed the guidance for FY24, with recurring revenue growth expected to be in the range of 6%-9%. The adjusted EPS is estimated to grow at 8%-12% in FY24. I think the company will be able to achieve these targets given its performance in the first half of FY24, and traditionally, it experiences a stronger second half.

BR is currently trading at a share price of $201.4, a YTD decline of 2%. It has a market cap of $23.76 billion. It is trading at a forward GAAP P/E multiple of 32x compared to the industry standard of 21.5x. BR is a market leader in the fintech technology space and commands a higher valuation. However, the current valuation doesn’t provide a favorable risk-reward profile. Investors can wait for a correction in the share price and utilize it to initiate a buying position. I believe $160-$165 would be an optimum entry point.

The company is experiencing strong demand despite a global slowdown, which is a big positive for investors. It has been growing its revenues at a considerable pace while improving profit margins. It faces the risk of high debt obligation, but it has been able to manage it with strong financial performance. It is trading at a considerable premium compared to the industry standards, resulting in an unfavorable risk-reward profile. Considering all these factors, I assign a Hold recommendation for BR.