ngkaki/iStock Editorial via Getty Images

ngkaki/iStock Editorial via Getty Images

We're now well through the Q4 earnings season, and so far, it has proven to be quite a volatile one, with many growth stocks sliding or jumping sharply on quarterly releases. Notably, there have been upside surprises in many stocks that have been thought to be "dead money," including Box (NYSE:BOX).

Box, the cloud storage software company, has been in a growth rut for years. With file storage being a saturated market plus the omnipresent competition from Dropbox (DBX) and Google Drive, the common sentiment is that Box has nowhere to go: but Q4 results, which demonstrated a re-acceleration in billings growth rates, have proven the mainstream thinking wrong.

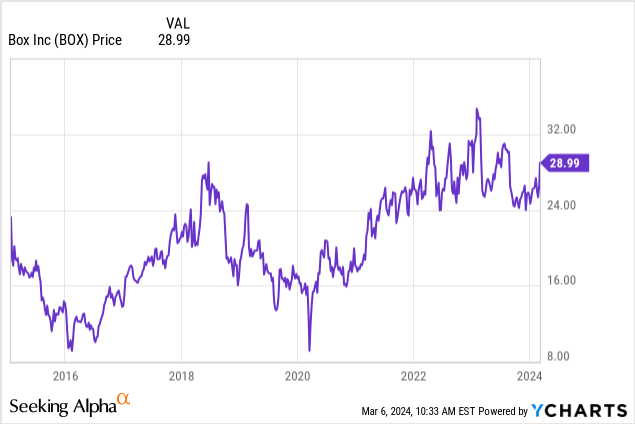

I last wrote a bullish article on Box in December, when the stock was trading in the low $20s. Though the stock has advanced more than 20% since then, with gains picking up after Box's Q4 earnings release, I remain stoutly bullish on Box's prospects for the remainder of the year. Box is the exact kind of stock I want to fit into my portfolio eat this exact moment: with a very expensive S&P 500 and many tech stocks that, in my view, are ripe for a correction, Box offers downside protection in its very modest valuations plus its ever-expanding profit margins.

We also have to remember that for Box, AI is not just a buzzword, but a capability it has been instilling into its product stack for years. Box's AI goal is to help customers "unlock the power of enterprise content" - its tools can help users quickly search across thousands of documents, summarize them, and even generate new content.

Here is a refresher for investors as to the core tenets of the bull case for Box:

The core risk to Box, of course, is saturation in the storage market. The need to upload and store files online and in the cloud has been omnipresent for years, and the market is already cornered by the three incumbents: Box, Dropbox, and Google Drive.

There are two opportunities and offsets to this, however. The first is the fact that Box has always maintained its best-in-class reputation for enterprise customers (though both of its competitors offer business packages, Box has long maintained its credential for being the most secure and advanced). As file storage becomes more commoditized and buyers select vendors based on AI and value-added feature sets, Box is set to gain market share, in my view. The second is growing data needs overall, which should continue to emphasize the importance of a robust and scalable storage strategy.

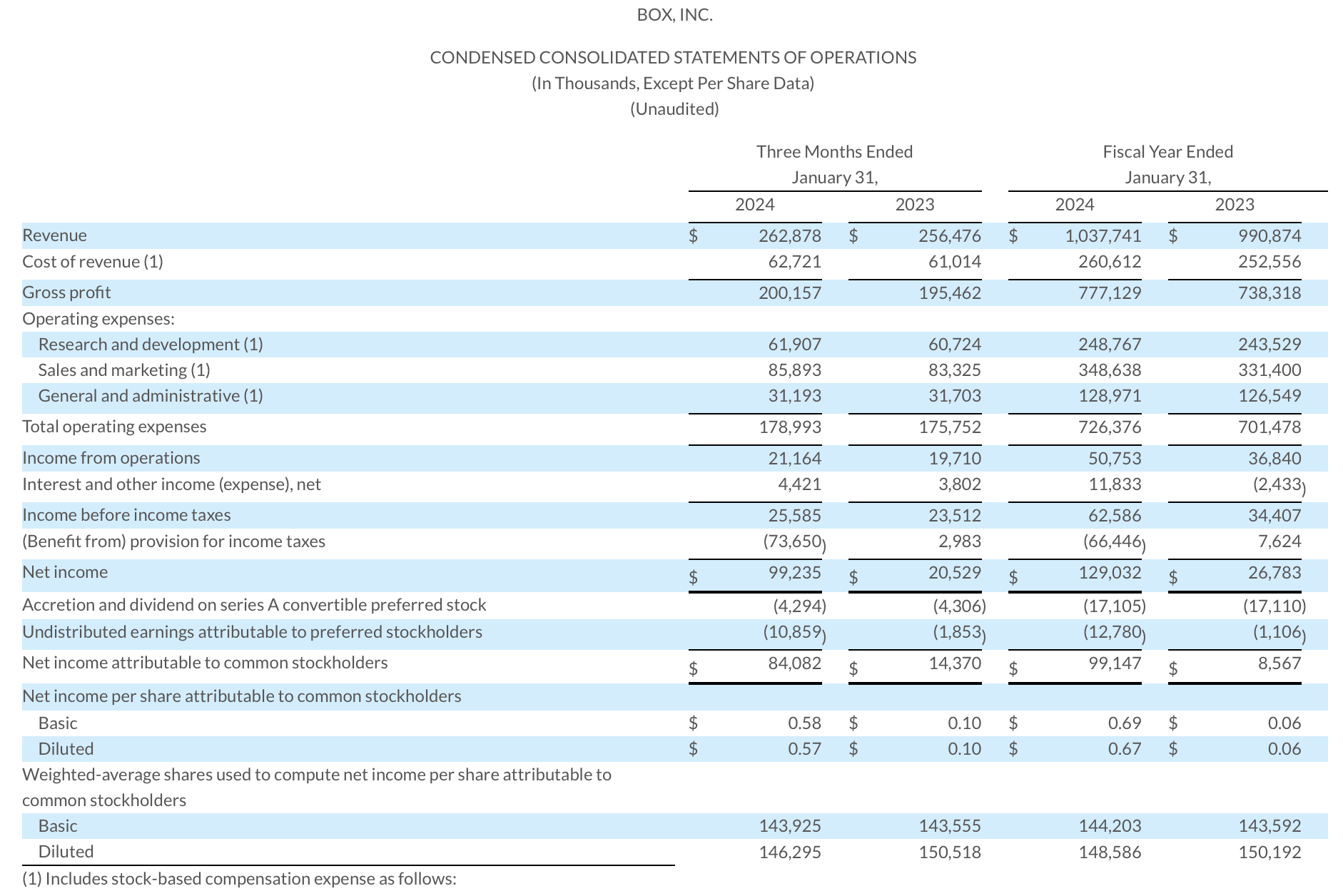

Let's now go through Box's latest quarterly results in greater detail. The Q4 earnings summary is shown below:

Box Q4 results (Box Q4 earnings deck)

Box's revenue grew 2.5% y/y to $262.9 million, ahead of Wall Street's expectations by a hair. Note that FX continues to be a headwind for Box, which notes that revenue growth on a constant-currency basis would have been 4% y/y.

The company notes that macro conditions have started to stabilize, helping to remove pressure from limited IT budgets being the cause of deal slippage. Also within the quarter, Box announced a new integration with Microsoft Azure's OpenAI, further burnishing Box's credentials as the most enterprise-grade and AI-ready storage offering on the market.

Here is helpful commentary from founder and CEO Aaron Levie's prepared remarks on the Q4 earnings call on the company's sales priorities for the current year:

As we look ahead to FY'25 and beyond, and as we enter this new chapter as a platform to power intelligent workflows around content, we will leverage our go-to-market motion to bring new solutions to customers, add new pricing models and packages to drive further upsell and extend our platform to a deeper set of partners and system integrators to deliver our more advanced solutions to customers and drive further growth.

Further, we plan to ignite more demand gen and pipeline development programs to reach even more customers and prospects, doubling down in key verticals, such as financial services, life sciences, healthcare, and the public sector, honing our focus on key international markets and more.

We are focused on taking advantage of the market opportunity in front of us and these focused go-to-market investments and initiatives are being made to accelerate the future revenue growth of Box.

As you can tell, we are incredibly excited about the innovation we will be delivering to our category-defining content cloud platform in FY'25. Our robust product roadmap combined with our investments in strategic go-to-market initiatives positions us well for the megatrends that are driving IT decisions and for when a more normalized IT spending environment returns."

We note that Q4 billings returned to growth, accelerating to 6% y/y or 10% y/y growth on a constant-currency basis as shown in the chart below. Note that investors panned box last quarter for seeing billings fall to -2% y/y.

Box billings trends (Box Q4 earnings deck)

Multi-product attach continues to be a driver for large deals, with the company noting that 81% of new deals featured Box Suites, up from 72% last year. The multi-product customers on Box Suites plans now represent 55% of Box's revenue. The company has also flexed its pricing power, noting that price per seat is up since last year.

The company also notched a 26.7% pro forma operating margin, up 70bps y/y. Savings have come from the company's strategic decision to relocate many teams to cheaper locations: for example, the company notes that the bulk of its R&D hiring going forward will be in Poland, where it already has 300 engineering employees.

Despite its strengths, Box still remains modestly valued. At current share prices near $29, the company trades at a $4.16 billion market cap. After we net off the $480.6 million of cash and $370.8 million of debt on the company's most recent balance sheet, the company's resulting enterprise value is $4.05 billion.

Meanwhile, for the current fiscal year, Box has guided to $1.08-$1.085 billion in revenue, representing 5% y/y growth (6% in constant currency), and pro forma EPS of $1.53-$1.57.

Box outlook (Box Q4 earnings release)

This puts Box's valuation multiples at:

Note as well that there are $0.16 of "non business" headwinds embedded in Box's EPS forecast for next year, with $0.10 coming from currency headwinds and $0.06 from recognition of international deferred tax expenses. If we normalize for these items, Box's P/E is closer to ~17x.

All in all, Box remains quite a compelling buy, especially after Q4 results showcased a re-ignition of billings momentum and continued margin gains. Stay long here.