Kyryl Gorlov/iStock via Getty Images

Kyryl Gorlov/iStock via Getty Images

I have previously discussed DMC Global (NASDAQ:BOOM), and you can read the latest article here. The company ended FY2023 as it headed into a few challenges. It faced margin headwinds due to changes in customer mix and lower absorption of overhead costs. The DynaEnergetics segment topline held steady, and the company can ramp up production of its new perforating system in 2024. However, in the Arcadia and NobelClad segments, the company's operating margins can decline in early 2024 as the residential end markets fail to exude confidence.

BOOM's cash flows have gathered momentum, and in 2024, it plans to deleverage its already robust balance sheet further from its free cash flow growth. I think the stock is reasonably valued, with a positive bias, versus its peers. Compared to my last analysis, the company currently operates in a more challenging environment. So, I think, investors would do well to "hold" the stock and restrict their returns expectations.

In my previous article, I pointed out BOOM's challenges and the pockets of growth. I discussed why the DynaStage perforating system was at the center stage of growth while the company developed the next-generation DynaStage systems and planned to commercialize them in 2023. Due to the recessionary fear, the company would sacrifice sales growth in Arcadia but look to expand its operating margin. I wrote:

The DynaStage perforating system sales grew in Q1, which reflects the company's manufacturing strength in Germany and Texas. Its NobelClad segment margin, however, can be adversely affected by a less favorable project mix. However, adverse outcomes on the two patent cases concerning DynaStage's perforating system can derail its outlook.

At the start of Q1, BOOM battles through many challenges as some battles appear to relent. The residential and construction markets are yet to recover after the lull in 2023. In the perforating market, pricing pressure continues following a consolidation in the end market. The company's operating margin will likely stay under pressure in the near term. However, production ramp-up in the perforating system and higher international sales in the DynaEnergetics segment can offset the headwinds in the Arcadia and NobelClad segments. Given the obstacles ahead, I downgrade from a "buy" to a "hold" position."

FRED data

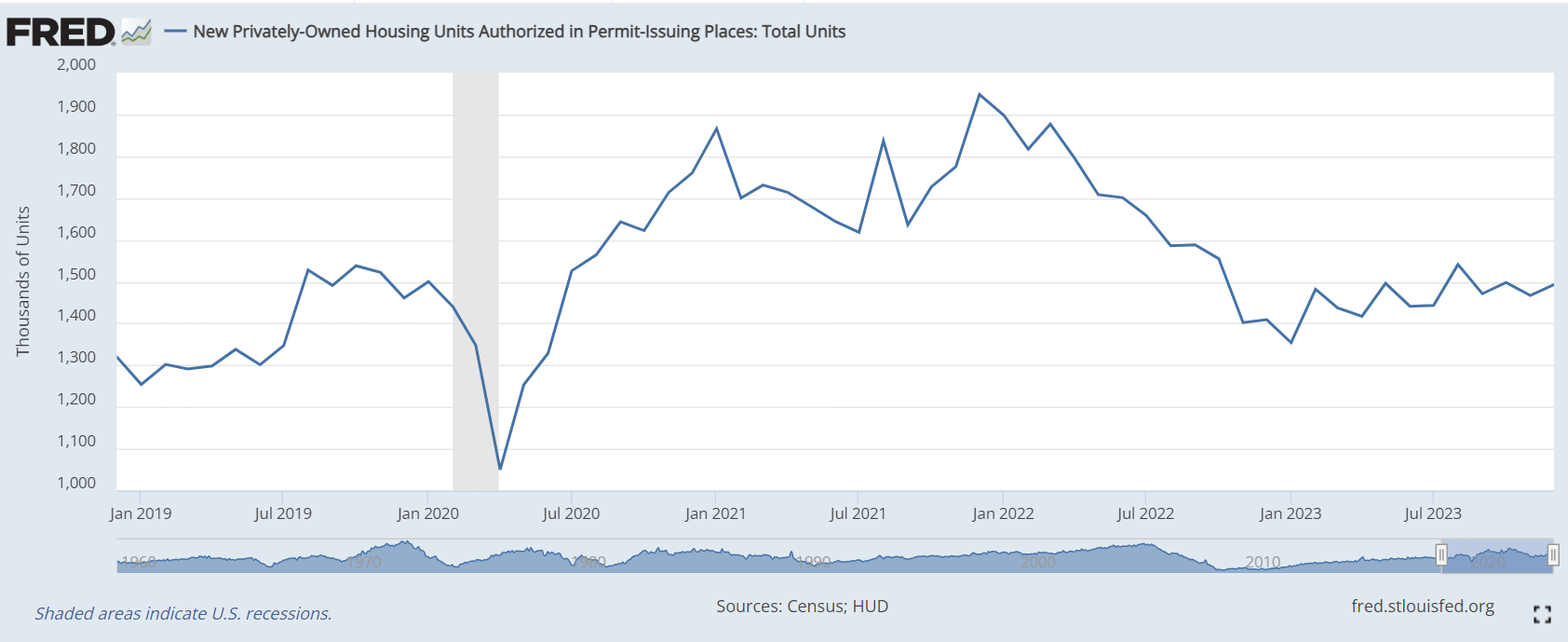

BOOM's Arcadia segment serves the building products market, particularly the commercial and high-end residential buildings. During Q4, it completed the first phase of a paint capacity expansion and planned a second expansion in 2H 2024. However, the residential and construction markets have not been steady. Over the past two years until December 2023, the new privately-owned housing unit permits declined by 23%. In Q4 (Sep-Dec), the market stabilized marginally. Nonetheless, the uncertainty over the US economy and a possible recession can make the market vulnerable in 2024. During Q4, the company's performance was negatively affected in the western and southwestern regions of the country.

Public construction spending far outpaced the dwindling residential market. It increased by 36% until December 2023 over the past two years, according to FRED data. On top of that, lower aluminum prices affected the sales adversely. In the perforating market, I see pricing pressure due to consolidation. To counter that, the company focuses on technology and automation that can yield results in Q1 and Q2. Introducing new tech in its gun systems has improved the product mix. Plus, the company's operational excellence initiatives can reduce costs and drive margins throughout 2024.

BOOM's Filings

In the DynaEnergetics segment, international sales propelled the company's performance after rising by 22% in 2023 over the previous year. In North America, DynaStage system sales increased by 4% in Q4. The segment margin, however, contracted due to margin pressure. In 2024, the company can introduce new products, e.g., ramp up production of its new Gravity 2.0 perforating system. The new product is a light, compact, self-orienting system that can improve the company's margins.

The company plans to simplify its portfolio to enhance shareholder value. Essentially, the company pursues separate strategic alternatives for DynaEnergetics and NobelClad. For Arcadia, it seeks a differentiated business model and a large addressable market. Currently, BOOM is looking to capitalize on the global market's strong demand for Cylindra Cryogenic Transition Joints (to join heat transfer equipment, liquified gas storage tanks, and other equipment).

Based on the expectations and critical drivers formed in Q4, BOOM's management expects its Q1 revenues to decrease by 11% (at the guidance mid-point). In the Arcadia and NobelClad segments, its EBITDA margins are expected to decline marginally. At the DynaEnergetics segment, however, the EBITDA margins can improve following lower bad debt expenses and higher sales volumes.

BOOM's Filings

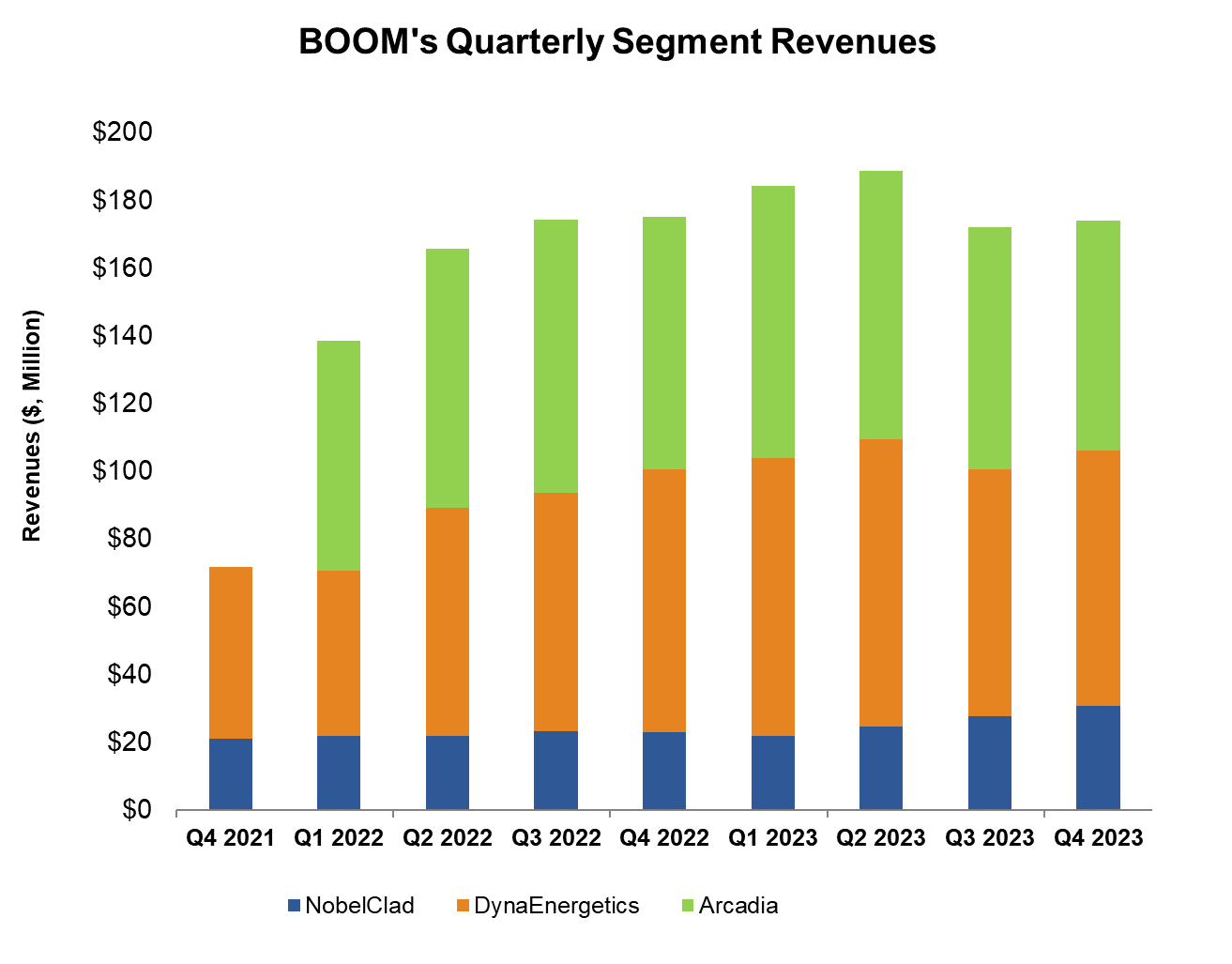

Higher international sales volumes in the DynaEnergetics oilfield products business kept the company's revenue steady (up by 1%) in Q4 2023 compared to a quarter earlier. However, BOOM'S gross margin and adjusted EBITDA margin contracted in Q4. Adverse changes in customer mix and lower absorption of manufacturing overhead costs led to margin contraction.

Although the adjusted margins improved in NobelClad and Arcadia, it took a hit in the DynaEnergetics segment. NobelClad witnessed a margin recovery through a better project mix and improved fixed-cost absorption.

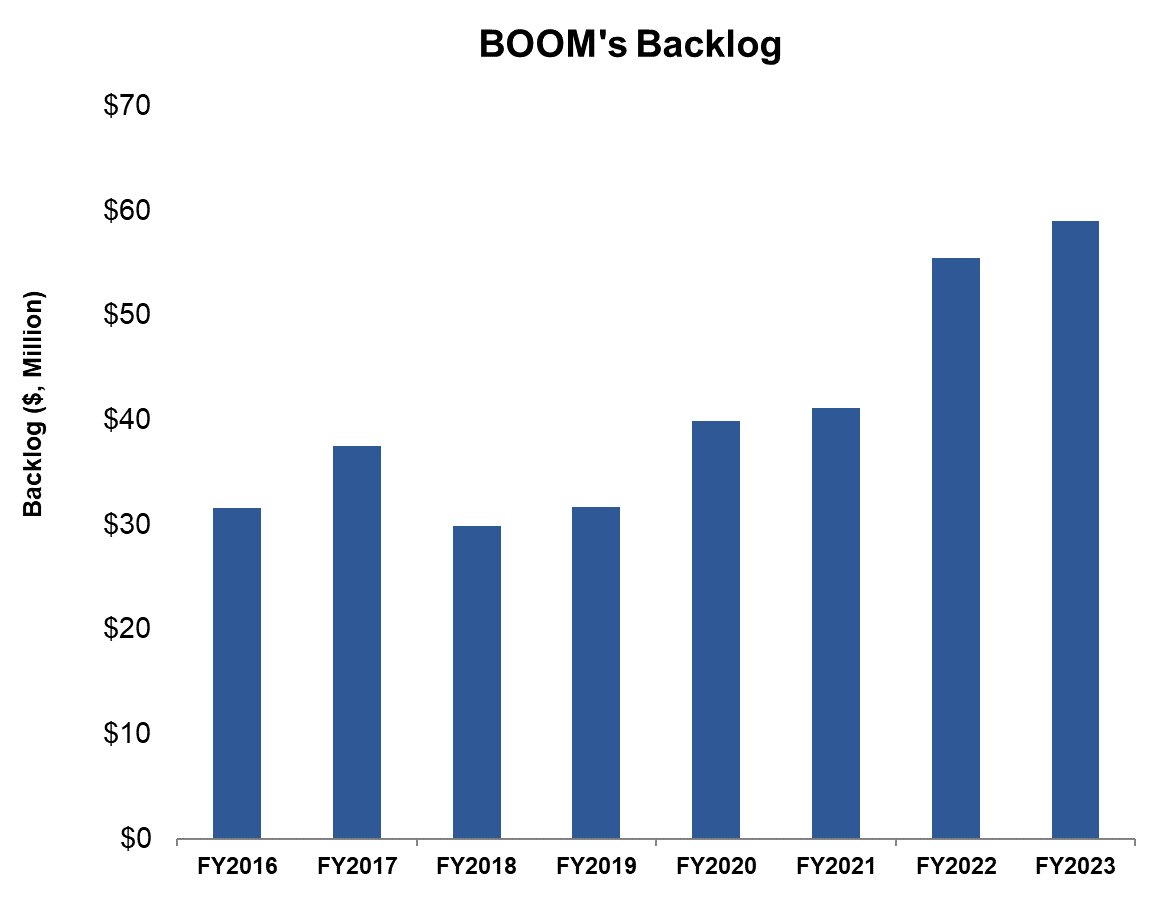

In FY2023, BOOM's cash flow from operations, led by higher revenues, increased by 47% compared to a year ago. Free cash flow nearly doubled in FY2023. The company uses its FCF for long-term debt repayment, distributions to its Arcadia joint venture partner, and investing in marketable securities.

BOOM's net debt of $72 million as of December 31, 2023. Its leverage (debt-to-equity) of 0.28x improved (from 0.31x) a year earlier. The current leverage is also lower than many of its peers. Its total liquidity is $94 million (cash plus revolving credit facility). So, its financial risks are limited.

Author Created and Seeking Alpha

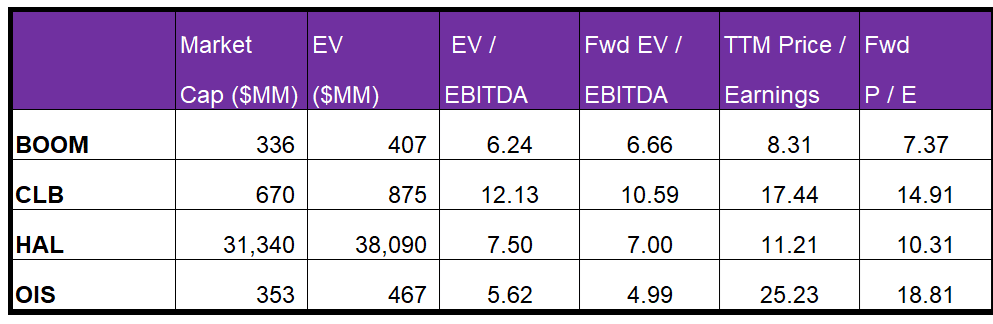

BOOM's EV/EBITDA multiple (6.2x) expansion to the forward EV/EBITDA (6.7x) contrasts its peers (CLB, HAL, and OIS), implying a fall in EBITDA compared to a rise in EBITDA for its peers. This typically results in a much lower EV/EBITDA multiple. The stock's current multiple is lower than its peers (11.2x). So, the stock is reasonably valued, with a negative bias, compared to its peers.

If the stock trades at the past average (~37x), it can increase significantly. However, the industry dynamics have changed over the past few years, and the stock is unlikely to respond to the factors as much as it used to. If the stock trades at the industry average, it can rally by 44%. Since my last publication in May 2023, the stock increased by 45% until September, validating my "buy" call. But it fell subsequently as lower fixed cost absorption hit the margin in Q4. Given the near-term pricing pressure in the residential construction market, I see the stock hovering close to its current price with a limited potential upside. So, I downgraded it to a "hold." Since it currently trades at ~$16.5, I reckon it should sell in the $16-$20 range.

Seeking Alpha

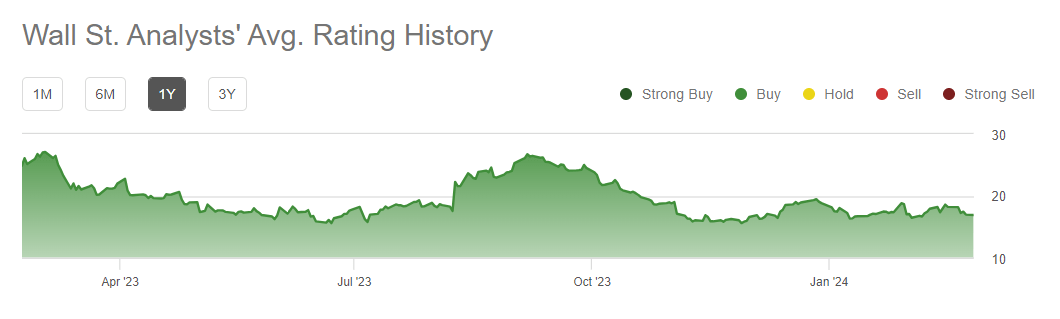

Two sell-street analysts rated BOOM a "Buy" (including "Strong Buy") over the past 90 days. One rated it a "Hold," and none rated it a "Sell." The consensus target price is $28, which implies a 66% upside at the current price. I think the sell-side analysts are overestimating the returns from the stock, although the stock price can rally marginally from here.

I see a nearly unanimous signal from the upstream operators spelling a cautious outlook on capex in FY2024. This, plus an expected decrease or uncertainty in oil and gas prices, threatens the oilfield services companies' financial results. Crude oil prices have declined significantly from their 2022 highs. As prices drop, the oil and gas exploration and production spending and projects get delayed or canceled.

US economic conditions and the commercial and residential construction industry influence BOOM's Arcadia segment financial results. The recent rise in inflation, interest rates, and construction costs can lead to lower product demand and adversely affect profitability. However, the residential construction market appears to head for stability in Q1 2024 as it moved up late in 2023.

Seeking Alpha

In 2024, BOOM will pursue separate strategic alternatives for DynaEnergetics and NobelClad, where it will simplify its portfolio to enhance shareholder value. It sees growth in the perforating gun market and can ramp up production of its new system. In Arcadia, it seeks a differentiated business model and a large addressable market.

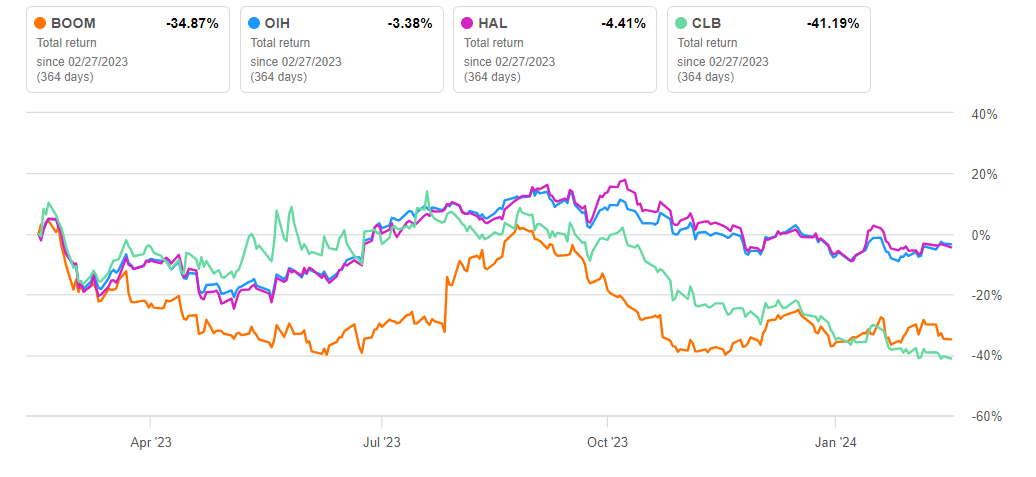

The commercial and high-end residential building end markets have not offered much growth over the past several quarters. This can lower its short-term outlook. Following the economic uncertainty, the stock price steeply underperformed the VanEck Vectors Oil Services ETF (OIH) in the past year. However, the company has the financial strength to withstand challenges for a long period, as reflected in its robust balance sheet. I expect returns from the stock to improve in the medium-to-long term.