Klaus Vedfelt

Klaus Vedfelt

Bonds are down but don't count them out for 2024 entirely. Following a spectacular end to 2023, bond performance has been stagnant as investors look to digest interest rate news. Over the past year, investors continued to push down yields and raise bond prices fueled by encouraging news from the Federal Reserve that interest rates may decline in the near term. Just recently, Jerome Powell testified before Congress that the Federal Reserve expects that rates will be cut "at some point" in 2024.

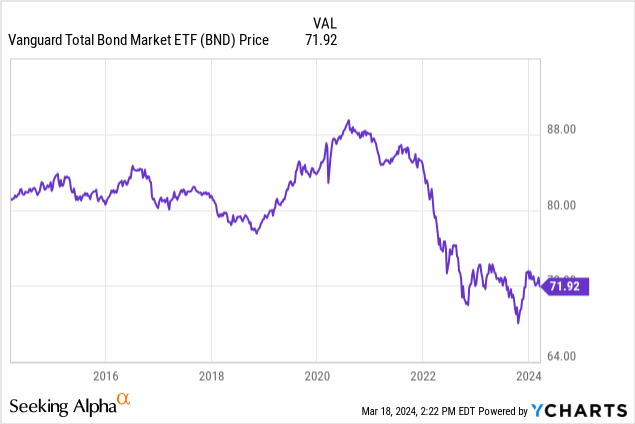

The bond market had a stellar year in 2023, capturing attention across the market as investors began to believe that the worst had come and gone. As the ten-year treasury priced a normalized level, the spotlight returned to income-producing assets which now carried healthy yields.

The long-anticipated bottom of the historic bear market for bonds came in the fourth quarter, and bond funds began to rally.

Bond prices climbed more than 20% as investors bet that the inflation was under control and rates had thus stabilized. Concurrently, the Federal Reserve's dot plot indicated expectations for coming rate cuts. However, the start of 2024 has been slow with the Federal Reserve indicating that rates may not be cut as quickly as anticipated.

For more comprehensive coverage of this scenario, I suggest reading my recent article. The bond market now forecasts an overwhelming consensus that the Federal Reserve will cut rates later this year. The next likely scenario will be at the May meeting.

In any event, it appears as though rates are destined to go lower, or at the very least, not climb higher in the near term. As the rally stagnates, it may be time to lock and load on bond funds. We will explore one of the best actively managed bond ETFs trading today, including thoughts on active management in today's market.

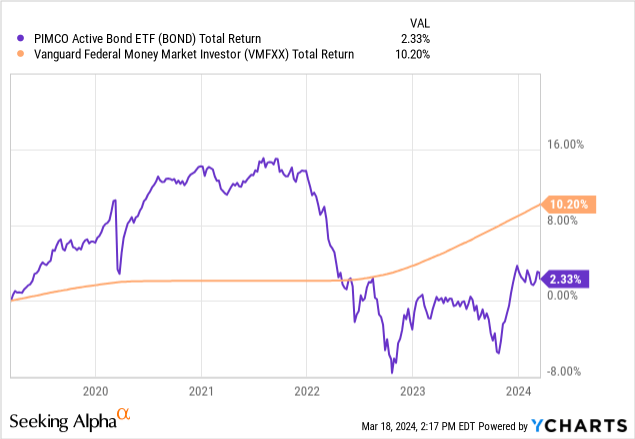

We covered the PIMCO Active Bond Exchange-Traded Fund (BOND) at the end of 2021. We described BOND as one of our favorite bond ETFs but cautioned around an investment given where interest rates were. Since then, BOND's price has declined by 17% and the total return has been in the red. Circumstances have changed and it's time to explore BOND once again.

BOND is an exchange-traded fund offering exposure to a diversified and actively managed portfolio of fixed-income investments. The fund has struggled significantly in the face of rising rates which have limited BOND's ability to perform. Following peaking inflation and rising interest rates, BOND faced a difficult outlook. Even with an active management strategy, BOND was unable to meaningfully outperform indexed competitors or even money market funds over the past five years.

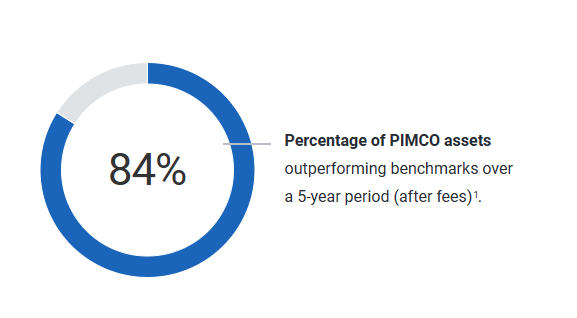

High expectations land on management for actively managed funds. PIMCO is a best-in-class manager of mutual funds, ETFs, and closed-end funds. PIMCO's management teams have produced reliable results, consistently beating their benchmarks in bull and bear markets. Their bottom line results are indeed impressive with 85% of PIMCO assets outperforming their respective benchmark, net of management fees over the past five years.

PIMCO

PIMCO's best-in-class management team utilizes a variety of vehicles for their funds. Most of PIMCO's assets are in mutual funds, closed-end funds, and private investment vehicles. Their ETF lineup is newer, and BOND is quickly becoming a flagship with nearly $4 billion under management. Let's explore the portfolio in depth.

The PIMCO Active Bond Exchange-Traded Fund (Ticker: BOND) is a diversified portfolio of high quality bonds that is actively managed, seeking current income and long-term capital appreciation, consistent with prudent investment management. BOND invests primarily in investment grade debt securities, and discloses all portfolio holdings on a daily basis. The Fund will seek to maintain a fairly consistent level of dividend income, and generally seeks to manage capital gain distributions. However, there can be no assurance that a change in market conditions or other factors will not result in a significant change in the Fund's distribution rate or that the rate will be sustainable in the future. With a primary benchmark of the Bloomberg U.S. Aggregate Index, the fund offers a core bond strategy that is designed to capitalize on opportunities across multiple sectors of the fixed income market.

Upon reviewing the prospectus, we will find that BOND is a highly diversified fund with an active management strategy. With an enormous portfolio of over 1,000 securities, BOND spreads risk effectively. BOND's structure as an exchange-traded fund allows for liquidity throughout the day and the manager to effectively trade in and out of the portfolio.

PIMCO

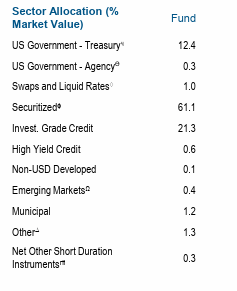

BOND is heavily diversified across sectors including securitized debt, investment grade debt, government securities, and a variety of others. As with nearly every PIMCO vehicle, BOND uses derivatives to speculate and hedge. In PIMCO's most recent semiannual report, management provides an update on performance including significant contributors and detractors.

For example, BOND's management notes that investments within securitized credit, such as collateralized loan obligations and ABS contributed positively to performance, as credit spreads tightened. Tactical positioning along the U.S. yield curve such as underweight exposure to the long end of the curve, helped protect net asset value as U.S. yields rose. Overweight exposure to high-yield corporate credit contributed as spreads tightened due to strong corporate performance as the economy remained healthy. PIMCO notes there were no material detractors from fund-level performance as fixed-income markets remain healthy.

The performance of bonds will continue to be inexorably tied to developments in monetary policy. As the Federal Reserve continues to craft its strategy to temper inflation, support the economy, and avert a hard landing scenario, investors are left polishing their crystal balls. When the Federal Reserve recently alluded to three 25-basis point rate cuts in 2024 through the dot plot, many investors became wildly optimistic.

In reality, inflation will continue to drive decision-making for the Federal Reserve. Policymakers will continue to look at inflation from different angles in an effort to determine whether cutting rates is prudent for the long-term health of the economy.

The cost of housing represents about one-third of the Consumer Price Index and about one-fifth of Personal Consumption Expenditures. Accordingly, "shelter costs" as they are known, remain a key indicator for the Federal Reserve's assessment of inflation. Shelter costs, such as rent, exhibit the slowest reaction to inflation given the time required for changes to reach the market. Rent is typically accounted for on a rolling basis meaning in-place leases that do not reflect current market conditions are included in the data.

The Federal Reserve is anticipating shelter cost inflation to temper in the near term. This scenario would be critical for those hoping that rates will come down. Should the Federal Reserve become comfortable with the status of its lagging indicators, it could instill confidence in a potential move around interest rates.

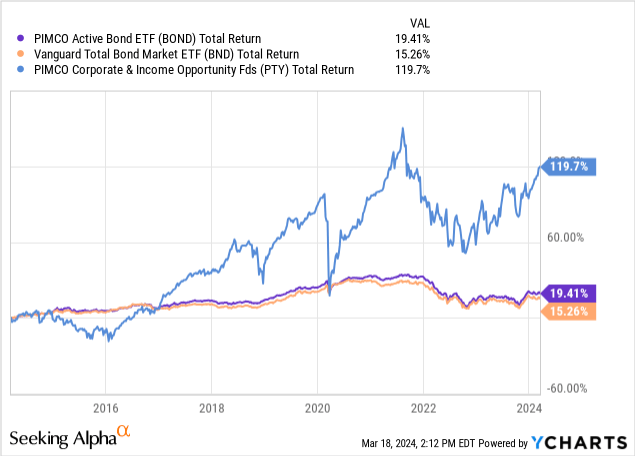

BOND's management team proposes that their skills and capabilities will lead to outperformance for shareholders. As we mentioned, PIMCO is a legendary manager with the vast majority of their managed assets outperforming their respective benchmarks. In fact, you don't have to look far to begin uncovering PIMCO investments which have outperformed passive bond funds. For example, the PIMCO Corporate and Income Opportunity Fund (PTY) has long outperformed its benchmark and is one of the oldest funds from the manager.

One critical contributing factor to this outperformance is the flexibility and freedom of the fund's investment mandates. PIMCO as a manager can use leverage, derivates, and all sorts of levers to deliver fund-level performance. Additionally, those funds can participate in special situations such as bankruptcies which may benefit from the liquidity structure of a closed-end fund as opposed to an ETF. As a result, BOND is more limited in its options for investments and new opportunities. Performance over the long and short term has been very close to indexed counterparts. I would argue that BOND takes additional risk as opposed to traditional fixed-income funds.

BOND is an effective fund that has delivered value to shareholders for more than a decade. More recently, the fund has felt the burn from rising interest rates which has pressured net asset value. The outlook has now changed after the federal funds rate increased significantly over the past few years.

However, BOND fails to deliver the outperformance it seeks. With long-term performance sticking close to more conservative, indexed counterparts, BOND lacks a compelling value proposition. In fact, a better option may be to complement a conservative, traditional bond fund like Vanguard Total Bond Market Index Fund (BND) with a closed-end fund like PTY. An 80/20 allocation to BND and PTY, respectively, would result in a higher blended yield and a higher overall return. Additionally, the risk profile would be comparable on a combined basis.

Typically, fixed income is a space where active management can reliably deliver outperformance. However, the structure of the fund and the limitations imposed on management often dictate how that outperformance can be delivered.