The exterior and parking lot of a Scotiabank branch.

jewhyte/iStock Editorial via Getty Images

The exterior and parking lot of a Scotiabank branch. jewhyte/iStock Editorial via Getty Images

In investing, it's often said that the higher the risk, the higher the potential reward. There is an element of truth to this argument. Higher-risk asset classes like stocks and real estate have historically produced superior total returns to asset classes that are often touted as lower risk, including bonds and gold.

However, in equity investing specifically, a study released in 2022 with empirical data found this to be inaccurate. For this study, risk was measured by credit ratings awarded by the National Information and Credit Evaluation, Inc. or NICE Investor Service, Moody's-affiliated Korea Investor Service, and Korea Ratings.

The authors decided to examine South Korea because it provided a more complete data set than U.S. markets. The former's data was monthly data ranging from January 2001 to August 2015 while the latter was several years at most.

It was found that retail investors as a whole don't put enough consideration into an investment's bankruptcy risk and credit ratings. For this reason, retail investors tend to highly price underlying stocks despite their risks. This is what leads to underwhelming risk-adjusted returns.

As both an investor and an analyst, that's why one of my top priorities is to highlight companies with exceptional balance sheets.

Today, I'll be revisiting the Canadian banking giant, The Bank of Nova Scotia or Scotiabank (NYSE:BNS). When I initiated coverage in January, I appreciated the company's status as a leading North American financial company, its vigorous financial health, and its attractive valuation.

Since that time, shares have gained 5% as the S&P 500 (SP500) has rallied 10%. In this article, I will be examining Scotiabank's fiscal first quarter results, financial positioning, and valuation to explain why I'm maintaining my buy rating.

Dividend Kings Zen Research Terminal

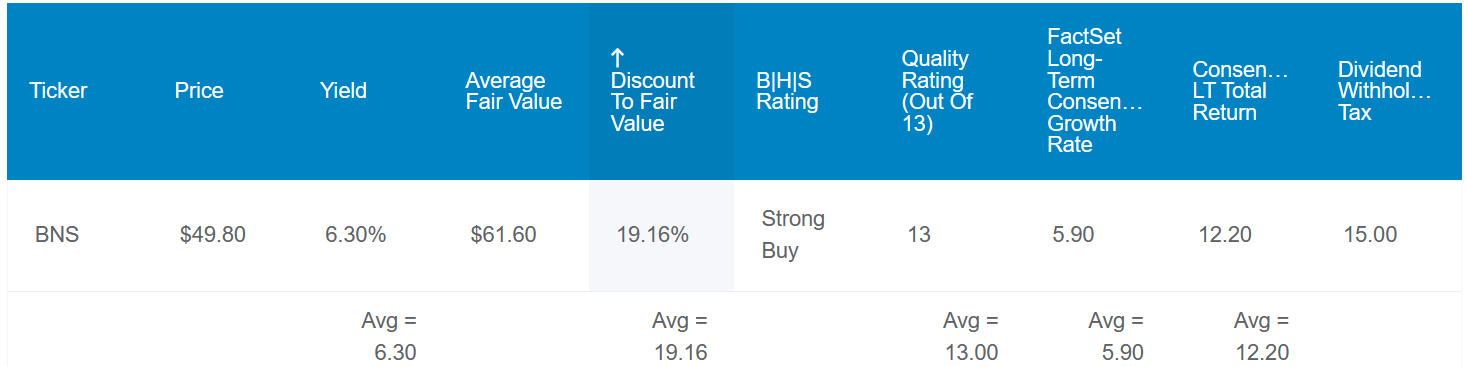

Scotiabank's 6.3% dividend yield compares favorably to the financial sector median of 3.6% according to Seeking Alpha's Quant System. This is enough to earn an A- grade from the Quant System on dividend yield. Yet, this dividend is also arguably safe.

The company's 65% EPS payout ratio is elevated moderately beyond the 50% EPS payout ratio that rating agencies prefer from financial institutions. However, as I'll discuss later in this article, that isn't as much of an issue as it initially seems.

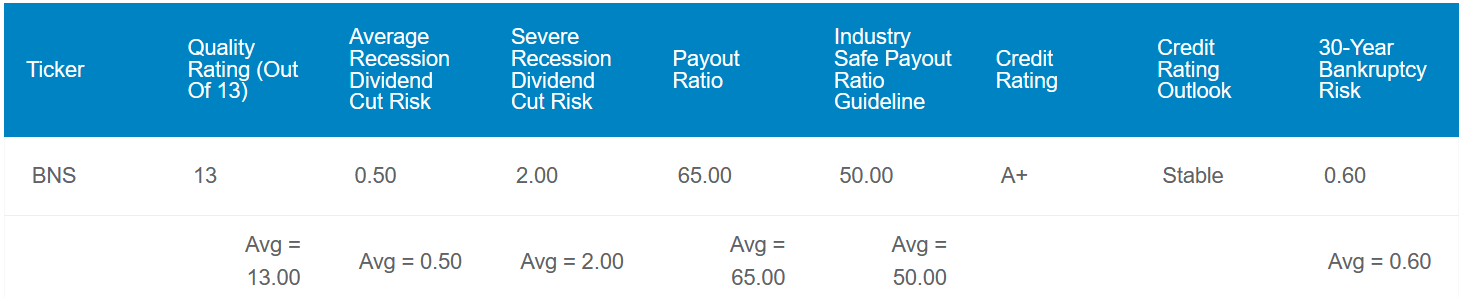

As I'll also elaborate on later, Scotiabank's balance sheet is secure enough that S&P awards an A+ credit rating to the company on a stable outlook. That suggests the risk of the Canadian banking giant going to zero in the next 30 years is merely 0.6%. Put another way, Scotiabank's credit rating implies that it would survive 166 out of 167 30-year simulations.

All of these elements together are why the Zen Research Terminal projects a 0.5% likelihood of a dividend cut from the company in the next average recession. In a severe recession, this risk is still relatively low at 2%. These are both the lowest possible dividend cut values for the Zen Research Terminal.

Dividend Kings Zen Research Terminal

Aside from its fundamentals, the valuation piece of the puzzle could also make shares of Scotiabank interesting here. Scotiabank's five-year average dividend yield of 4.9% could indicate its shares are worth $64 each.

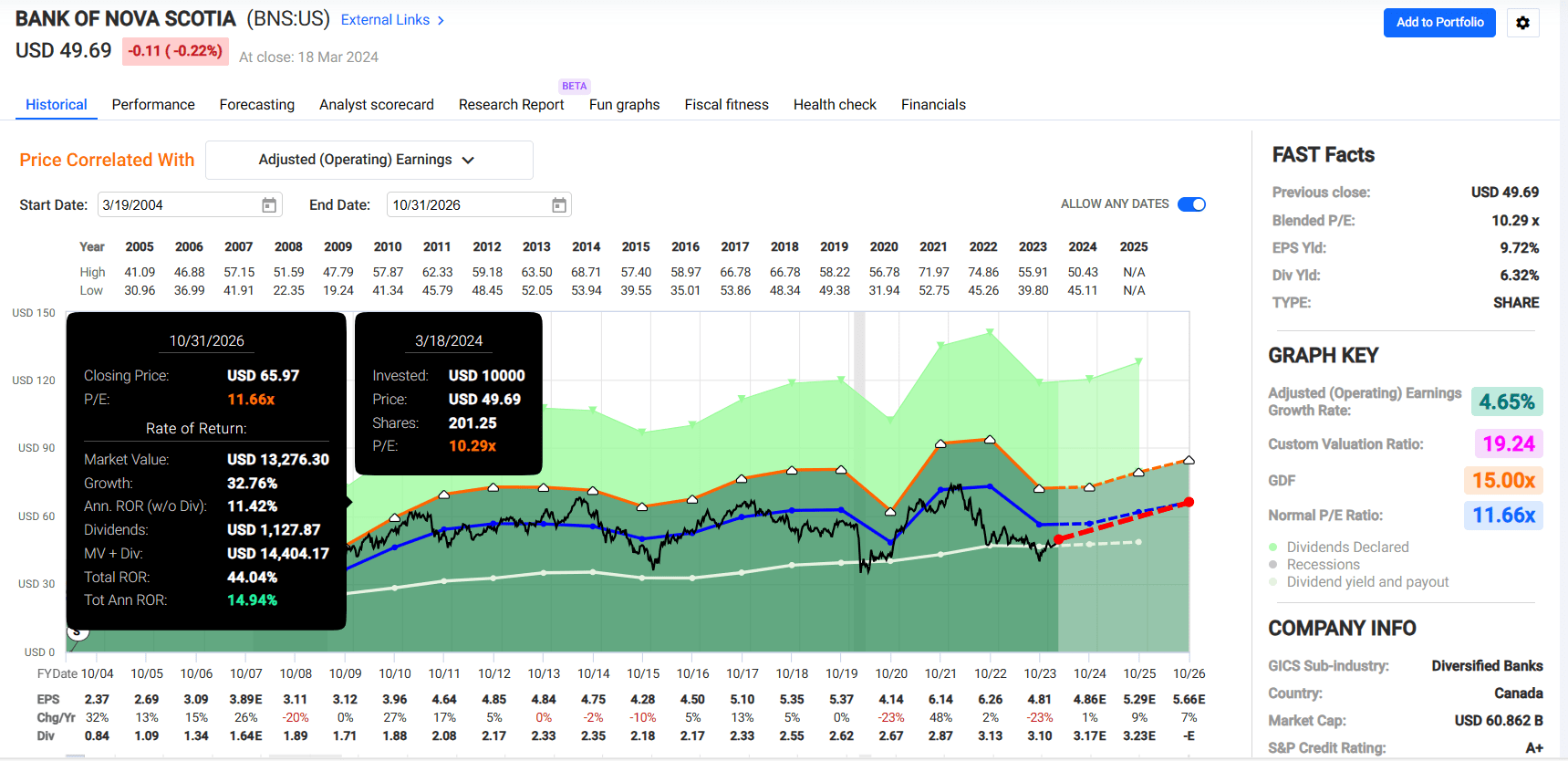

The bank's 20-year normal P/E ratio of 11.7 per FAST Graphs could translate into a fair value of approximately $58 a share. Given that Scotiabank's fundamentals appear to be intact relative to the past, I believe it's not unreasonable to expect an eventual reversion to this valuation multiple.

The following inputs into the dividend discount model show shares of Scotiabank to be worth $53 each as well: A $3.16 annualized dividend per share (annualizing the first half of dividends in US Dollars this calendar year), a 10% discount rate, and a 4% annual dividend growth rate.

Averaging out these values, I get a fair value of $58 a share. Relative to the $50 share price (as of March 19, 2024), that hints Scotiabank's shares could be trading at a 15% discount to fair value.

If the bank grows as anticipated and returns to fair value, here are the total returns that could be produced over the next 10 years:

Scotiabank Q1 2024 Investor Fact Sheet

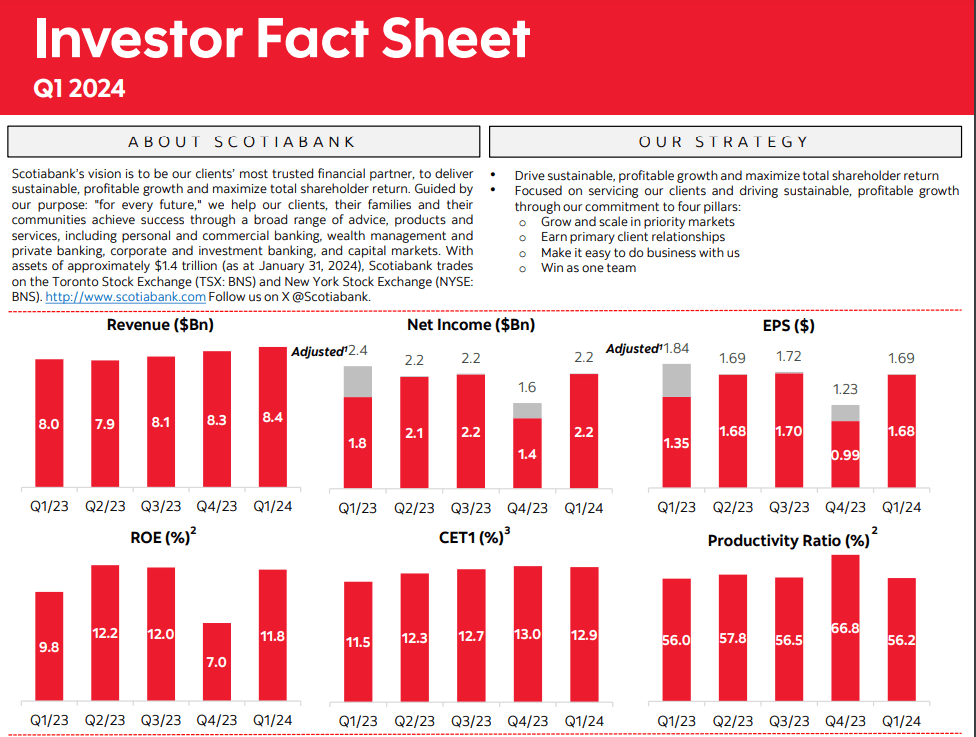

On Feb. 27, Scotiabank shared its financial results for the fiscal first quarter that ended Jan. 31. The company's total revenue grew by 5.9% year-over-year to $8.4 billion during the quarter (note that this amount and all to follow in this subhead are in Canadian Dollars). These results were powered by non-interest income growth, although net interest income contributed to growth as well.

Scotiabank's net interest income edged 4.6% higher over the year-ago period to $4.8 billion in the fiscal first quarter. According to CFO Raj Viswanathan's opening remarks during the Q4 2023 Earnings Call, that was due to an 8 basis point expansion in net interest margin. This is another way of saying the investment spread between a financial institution's interest received and interest paid to customers.

Non-interest income climbed by 7.7% year-over-year to $3.7 billion for the fiscal first quarter. This was driven by strength from Scotiabank's trading revenue, banking fees, and wealth management revenue.

Moving down the income statement, adjusted diluted EPS declined by 8.2% over the year-ago period to $1.69 during the fiscal first quarter. The company's adjusted net income declined because of a meaningful uptick in its provision for credit losses from $638 million in the year-ago period to $962 million in the fiscal first quarter.

The good news is that this suggests provisions for credit losses trended down from just shy of $1.3 billion for the fiscal fourth quarter. As a Canadian bank, Scotiabank has a reputation for being relatively conservative. So, it may end up recovering these credit losses. Backing out the $324 million year-over-year increase in these provisions, adjusted diluted EPS would have risen.

Scotiabank's financial prowess remained intact during the fiscal first quarter. The company's Common Equity Tier 1 or CET1 capital ratio of 12.9% was about as strong sequentially as the 13% posted in the prior quarter. Versus the year-ago period, Scotiabank's CET1 capital ratio was much better than the mark of 11.5%. This explains how besides its A+ rating from S&P, the company enjoys AA and Aa2 (AA equivalent) ratings from Fitch and Moody's on stable outlooks.

Looking forward, Chief Risk Officer Phil Thomas anticipates that PCL will likely peak next quarter or into the third quarter. But beyond that time, things should improve in the second half to the point that he thinks it will be a tale of two halves to the year.

This is why the analyst consensus is that adjusted diluted EPS will edge 0.6% higher to $6.58 this fiscal year per FAST Graphs. The improved macroeconomic outlook in 2025 and beyond has analysts forecasting an additional 8.8% growth to $7.16 in FY 2025 and another 6.6% in FY 2026 (unless otherwise sourced or hyperlinked, all details were from Scotiabank's Q1 2024 Earnings Press Release and Scotiabank's Q1 2024 Investor Fact Sheet).

In Canadian Dollars, Scotiabank's dividends paid cumulatively compounded by 27.4%. That's equivalent to a 5% compound annual growth rate. For the next few years, I would expect muted dividend growth.

That's because Scotiabank's payout ratio will come in around 64% to 65% this fiscal year. A few years of limited dividend growth could help this payout ratio to improve to the high-40% to low-50% range that is more typical of the company. In 2027 and beyond, I could envision dividend growth returning to the mid-single digits annually.

Scotiabank is a great business, but it still faces risks that are worth knowing and monitoring.

The finances of Canadian consumers are improving, but not yet ideal. The most recent data from Toronto-Dominion Bank (TD) found that household debt to disposable income was 178.7% to close out 2023. This remains near an all-time high. If the state of consumers can't keep improving, that could result in higher PCLs. This could harm Scotiabank's operating and financial results.

As a global financial institution, the company also has a treasure trove of data. Unsurprisingly, it consistently is the target of attempted cyber breaches. Scotiabank is adept at managing risk, but there are no guarantees it can stave off a major breach forever. If the company fell victim to a significant breach, this could have many negative consequences. Scotiabank's affected stakeholders could sue the company for sizable sums. Its reputation could also be hurt, resulting in a meaningful loss of business.

FAST Graphs, FactSet

In my view, Scotiabank is one of the better publicly traded banks in the world. The company's operating fundamentals look set to improve. Its balance sheet is a fortress. And the dividend hasn't been cut at any point throughout a nearly 200-year operating history.

The cherry on top is that shares are currently priced at a blended P/E ratio of 10.3. Against the 20-year normal P/E ratio of 11.7, this could be an appealing mean reversion play. If Scotiabank can match the growth consensus and revert to its valuation multiple of 11.7, 44% cumulative total returns could be in store through October 2026.