Bet_Noire

Bet_Noire

Badger Meter, Inc. (NYSE:BMI), a provider of water monitoring solutions, is benefitting from the adoption of more advanced technologies and an infrastructure spending boom. While growth is currently strong, and the company's margins improving, current strength does not appear to be sustainable. Badger Meter's backlog should ensure robust growth in the near term, but a normalization of sales will eventually come. Given this situation, I don't believe it makes sense to pay an exorbitantly high multiple for Badger Meter's stock, despite the quality of the business.

There are a number of secular trends supporting Badger Meter's business, including:

As a result, there is increasing demand for water monitoring solutions that provide real-time data and reduce labor requirements. Smart water meters are an important part of this as they are more efficient and help to address resiliency and sustainability issues.

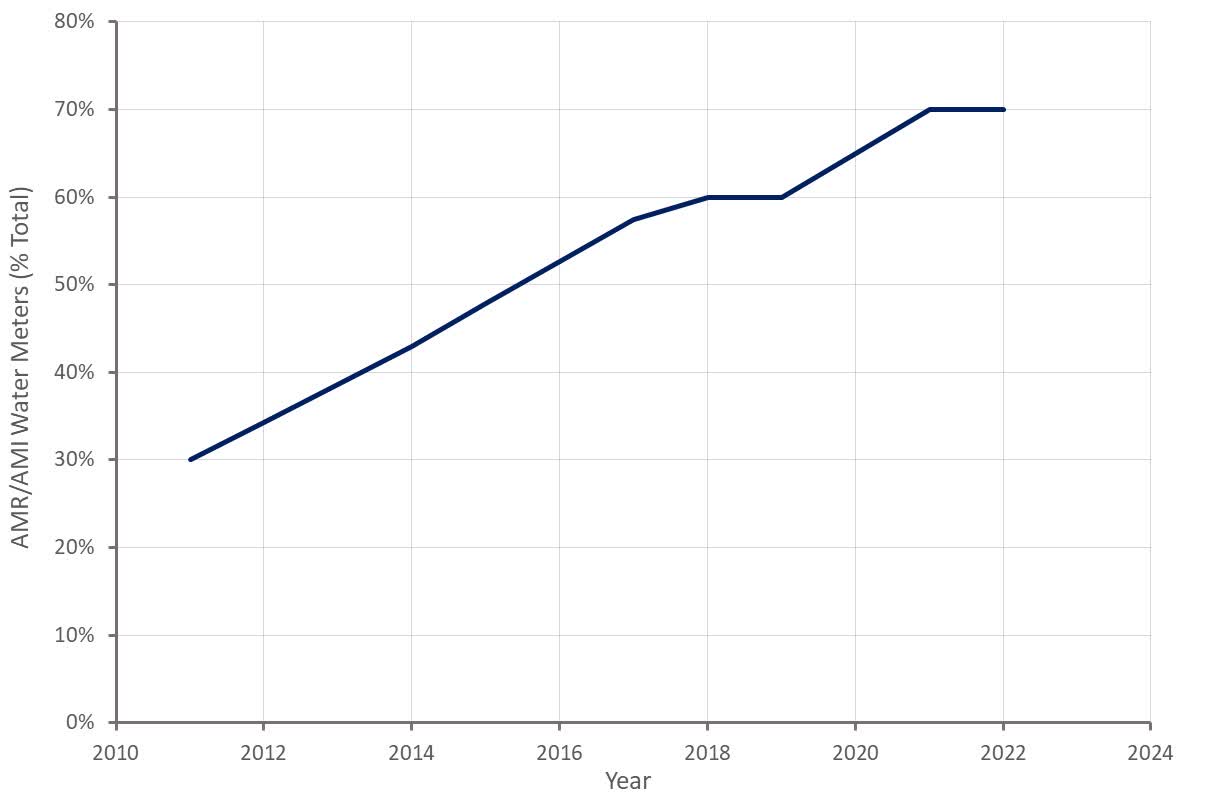

While adoption continues to increase, the penetration of meters that can transmit data remotely is now fairly high. The industry continues to move from AMR systems to digital AMI solutions though, and the importance of software and solutions like ultrasonic water meters continues to increase.

Figure 1: Penetration of AMI/AMR Water Meters (source: Created by author using data from Badger Meter)

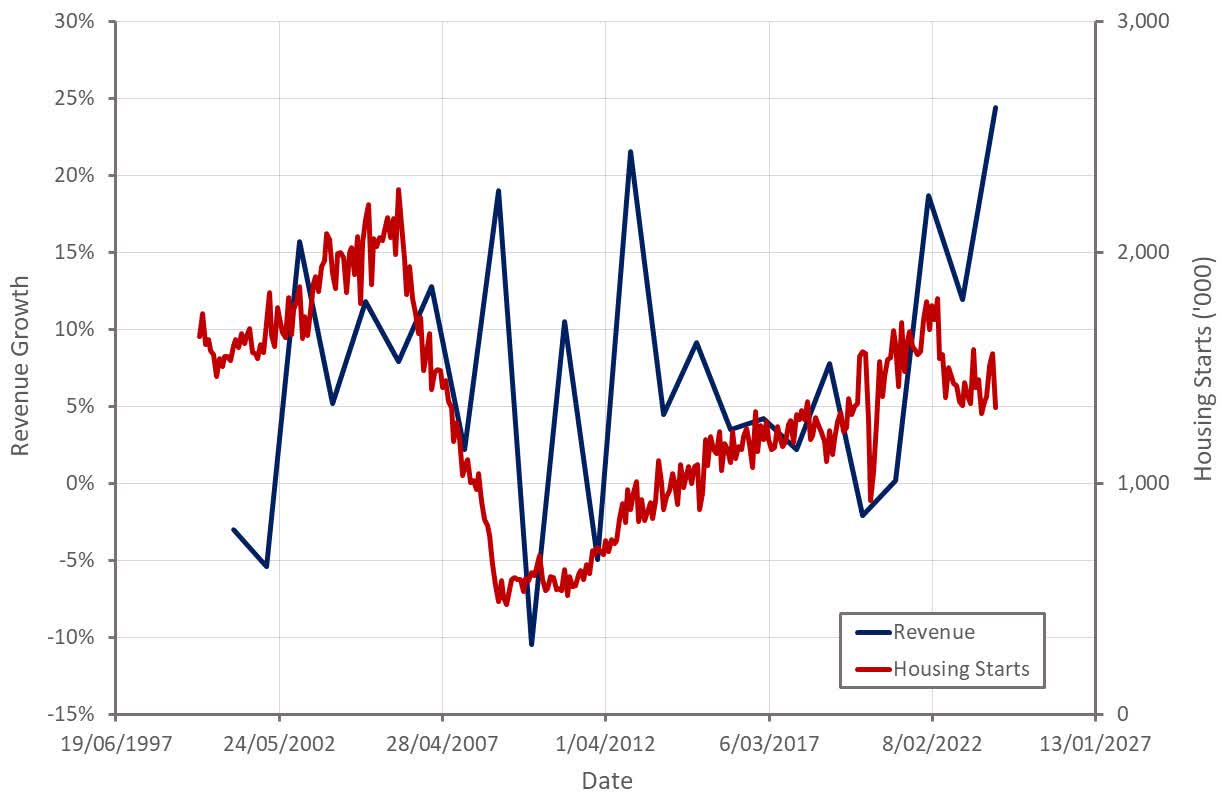

The transition to more advanced technologies is important for Badger Meter as replacement-driven demand and adoption of AMI is driving its business (~85% of sales), rather than new build housing. While less important, the recent housing boom has also contributed to the recent strength of Badger Meter's business.

Figure 2: US Housing Starts and Badger Meter Revenue Growth (source: Created by author using data from Badger Meter and The Federal Reserve)

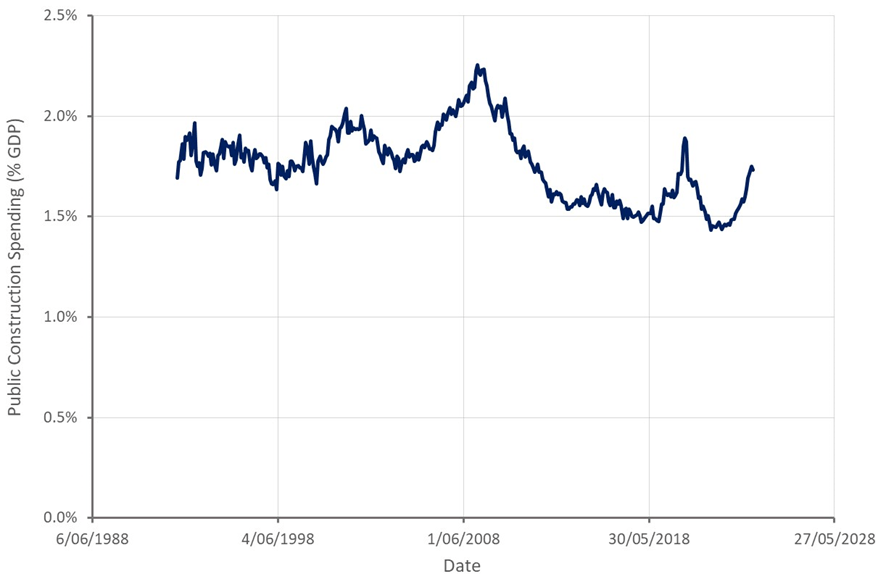

The recent strength of Badger Meter's business is not surprising given the amount of fiscal stimulus being poured into infrastructure. The Bipartisan Infrastructure Law has made over 850 billion USD in total funding available, which is being directed toward areas like water, road, rail, airports, and power infrastructure. The law has an authorizing period of five years, but spending is likely to last beyond this.

Autodesk, Inc.'s (ADSK) AEC business continues to perform extremely well, particularly in transportation, water infrastructure and construction. Water is a focus area for Autodesk, with the company acquiring Innovyze in support of this. Bentley Systems, Incorporated (BSY) has also highlighted the importance of government infrastructure spending, with funding now flowing into areas like water, broadband and the electricity grid.

While the demand environment remains robust, Badger Meter is now beginning to reduce its order backlog. The company's order backlog, along with strong demand, should support the business in the near term but there is the prospect of normalized infrastructure spending to consider.

Figure 3: Public Construction Spending (source: Created by author using data from The Federal Reserve)

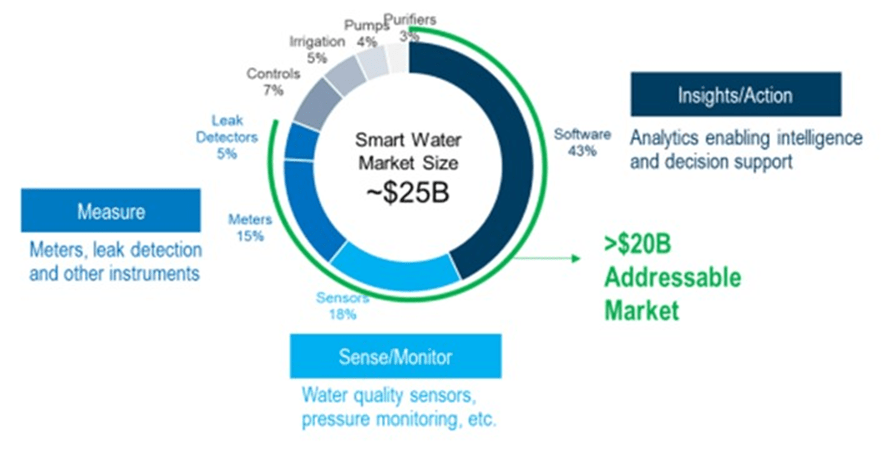

Badger Meter primarily targets the US but also has operations in select regional markets globally. This provides a large addressable market, with growth driven by population expansion, aging infrastructure and improved technology.

Figure 4: Badger Meter's Addressable Market (source: Badger Meter)

Utility water meter competitors include:

Badger Meter, Roper and Xylem have an estimated 85% market share between them.

Utility water radio product competitors include:

The water quality monitoring market is more fragmented, with Badger Meter often competing against smaller, specialized firms.

Competitors struggled with supply chain issues through the pandemic, allowing Badger Meter to outperform the market. With supply chains now normalizing, competition could be expected to increase going forward.

Badger Meter offers water solutions across areas like flow measurement, quality and other system parameters. These solutions provide customers with the data and analytics necessary to optimize their operations. The company's product portfolio includes:

Badger Meter segments its business into Utilities and Flow Instrumentation, with approximately 85% of net sales coming from the Utility Water product line.

Most water meters sold are mechanical, although the adoption of ultrasonic meters is increasing. Meters are generally classified as manually read or remotely read via radio technology. Remotely read systems can be either automatic meter reading (AMR) systems, where a vehicle must collect the data, or advanced meter infrastructure (AMI) systems, where data is transmitted utilizing a network. Badger Meter's ORION Cellular network powers its AMI solution. It can be rapidly deployed and avoids the need to install or maintain infrastructure.

Badger Meter's cloud-hosted BEACON software provides customers with a customizable dashboard, helping with customer service, infrastructure management and compliance reporting.

Water quality monitoring solutions utilize optical sensors and electrochemical instruments to measure a range of parameters (turbidity, pH, chlorine, nitrates, etc.).

Ultrasonic meters, meters equipped with radio technology, water quality monitoring and software are all supportive of ASPs and margins. The transition to more advanced technologies has therefore provided Badger Meter's business with a substantial tailwind over the past 15-20 years. This transition is maturing though, and as a result, it is reasonable to expect that Badger Meter's margins will plateau in coming years and growth will begin to taper off.

Badger Meter's flow instrumentation product line serves the industrial market, with both standard and customized solutions. Products include meters, valves and sensing instruments to measure and control a broad range of fluids. Primary use cases include water/wastewater and heating, ventilation and air conditioning.

Badger Meter continues to invest in innovation, software, production capacity and acquisitions. Badger Meter acquired the Telog/Unity network monitoring assets in early 2024. Telog provides remote telemetry units and Unity provides monitoring software. This supports Bader Meter's remote monitoring capabilities across utility, wastewater, storm water and source water applications.

Badger Meter completed the acquisition of Syrinix in January 2023 for 15 million pounds. Syrinix specializes in high-frequency pressure monitoring and leak detection with remote monitoring.

Badger Meter plans on pursuing further acquisitions to enhance its portfolio of solutions and drive growth.

Badger Meter's revenue was 182.4 million USD in Q4, up 24% YoY. Utility water sales increased 28% YoY in Q4, driven by robust AMI, software and ultrasonic meter demand. While the adoption of ultrasonic meters is increasing, mechanical meters continue to dominate Badger Meter's sales. International utility revenue increased more than 30% YoY, although this was off a small base. SaaS revenue was over 42 million USD in 2023, a 27% increase YoY. Flow instrumentation sales were only up modestly YoY in the fourth quarter though.

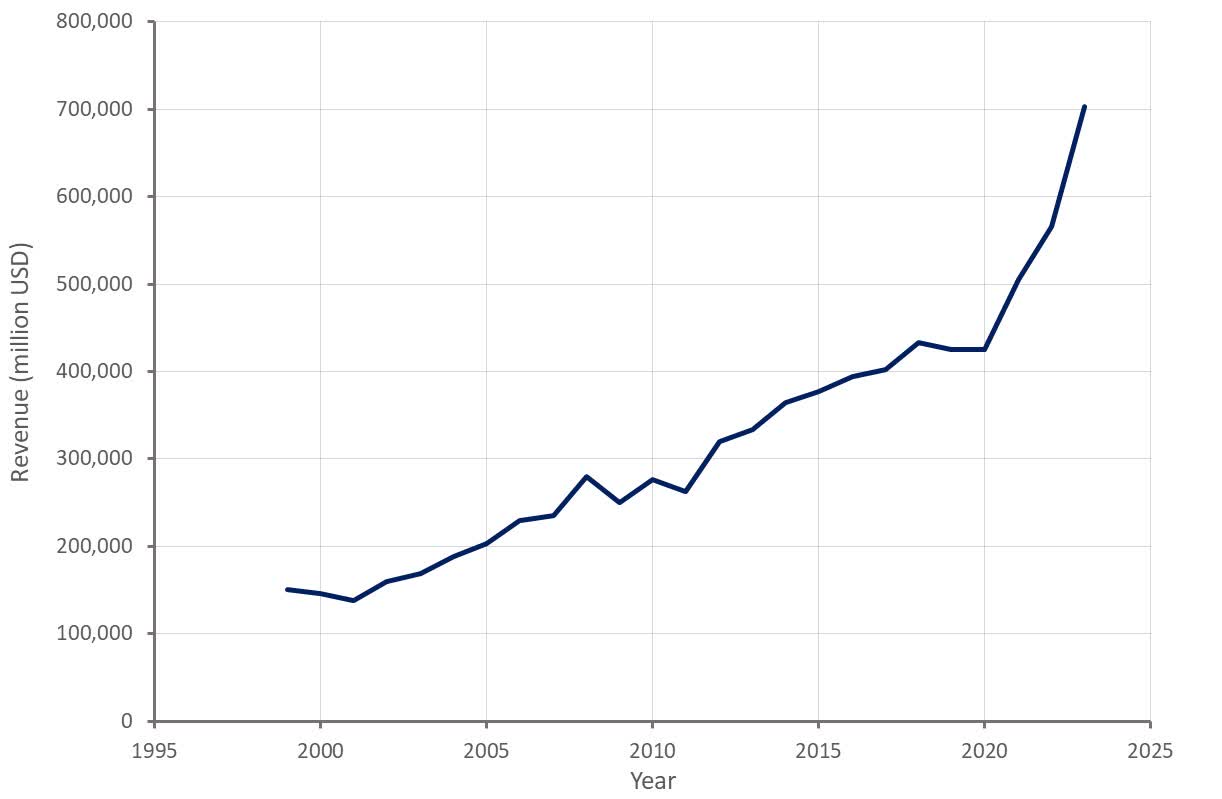

Growth is expected to moderate going forward, which is unsurprising given the recent infrastructure splurge that has occurred. Badger Meter's backlog remains elevated though, which should continue to support growth in the near term. Long-term organic growth is likely to be in the mid to high-single digit range.

Figure 5: Badger Meter Revenue (source: Created by author using data from Badger Meter)

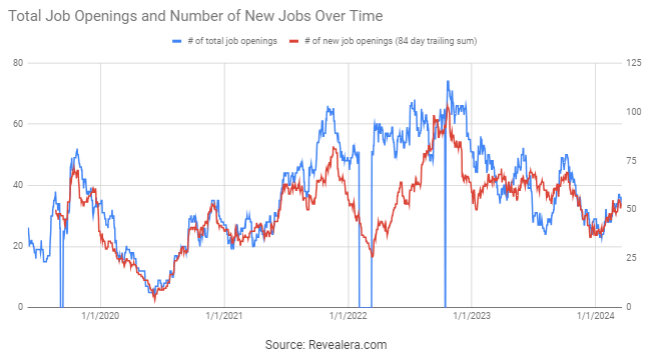

Job opening data seems to support a normalization of growth following the past few years of strength.

Figure 6: Badger Meter Job Openings (source: Revealera.com)

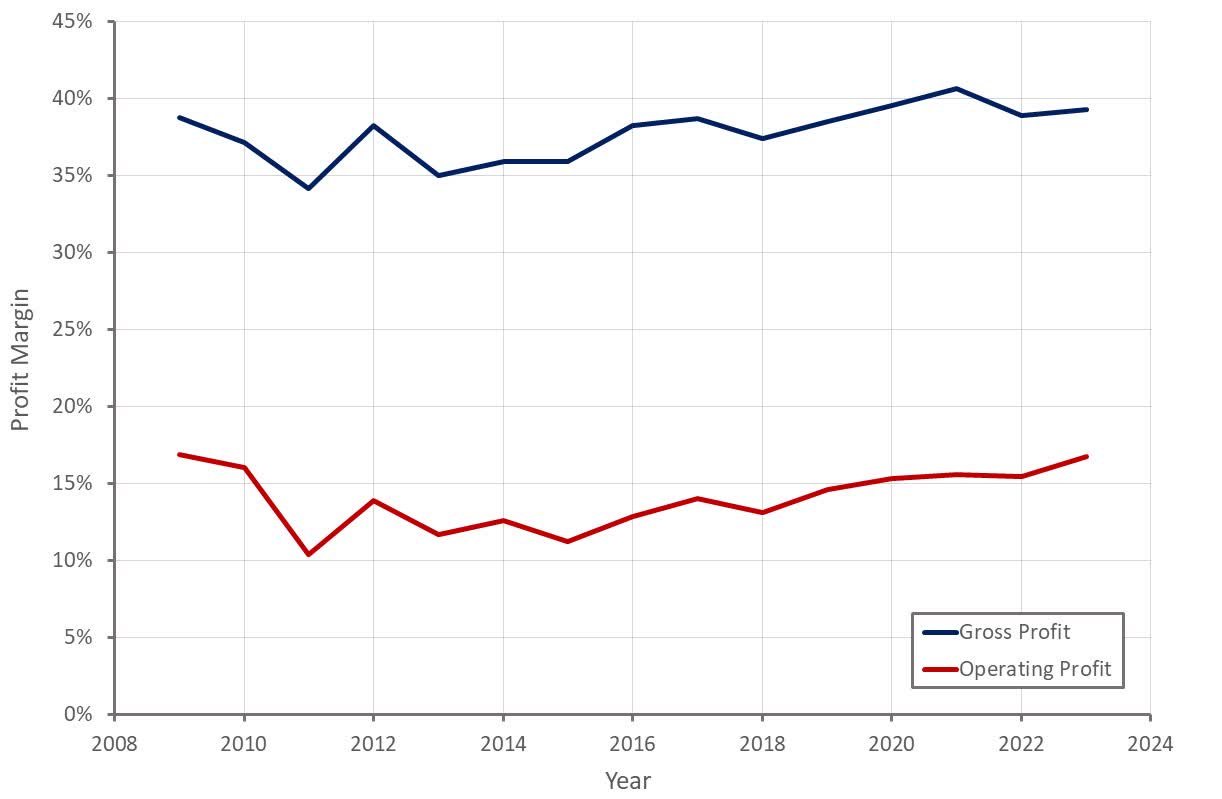

Badger Meter's margins have trended upward over the past 5-10 years, driven by economies of scale and an evolving product portfolio. Product mix, volumes, pricing and operating leverage contributed to higher margins in 2023. I would expect margins to continue trending higher but given the relative maturity of the transition to AMI, further gains may be modest.

Figure 7: Badger Meter Profit Margins (source: Created by author using data from Badger Meter)

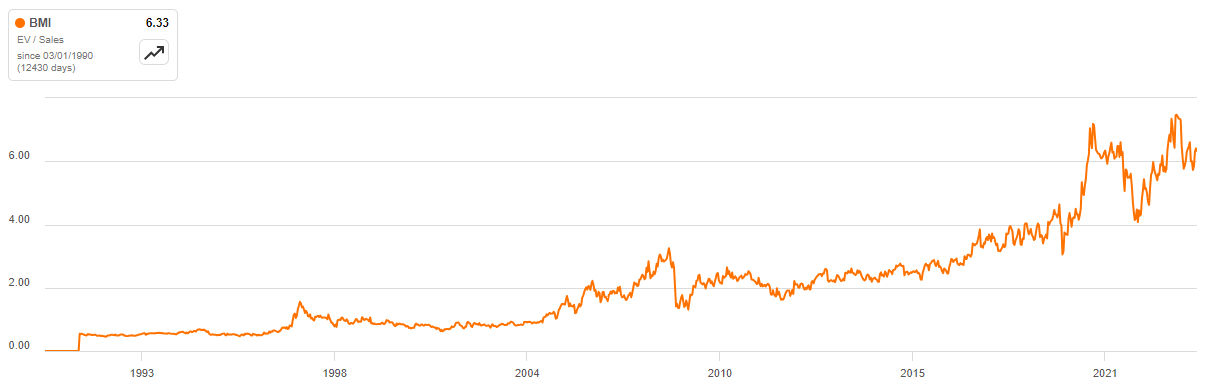

Over the past 20 years, Badger Meter's revenue multiple has expanded significantly (~6x) driving much of the stock's gains over that period. Badger Meter's performance has greatly exceeded analyst expectations in recent years, contributing to positive sentiment and a higher valuation. Badger Meter has also been able to expand its margins and has increased its annual dividend for the past 31 years consecutively. Multiple compression is far more likely than further multiple expansion going forward though.

The shift towards AMI meters and the growing importance of software are both supportive of margins and Badger Meter's competitive positioning. The transition towards AMI meters is rapidly maturing though, which will likely begin to weigh on growth at some point.

Badger Meter could also face a decline in revenue and lower margins once its backlog is gone and infrastructure spending normalizes, which could result in significant multiple compression. This situation could still be 1-2 years away though.

Figure 8: Badger Meter EV/S Multiple (source: Seeking Alpha)