simpson33/iStock via Getty Images

simpson33/iStock via Getty Images

Biomea Fusion, Inc. (NASDAQ:BMEA) is a promising clinical-stage company that discovers and develops covalent small molecules. BMEA is making strides in treating diabetes and several genetically defined cancers. BMEA highlighted positive phase 2 trial results for the BMF-219 program to treat diabetes, presenting significant HbA1C level reductions. In 2024, BMEA will expand its trials to solidify its findings in diabetes and oncology treatments. Yet, from a valuation perspective, I think BMEA doesn’t have a long cash runway and seems fairly valued. Given that we’re still far from seeing any meaningful cash flows, I lean towards a neutral rating on BMEA, balancing both the pros and cons of this stock. Hence, I rate it a “hold” for now.

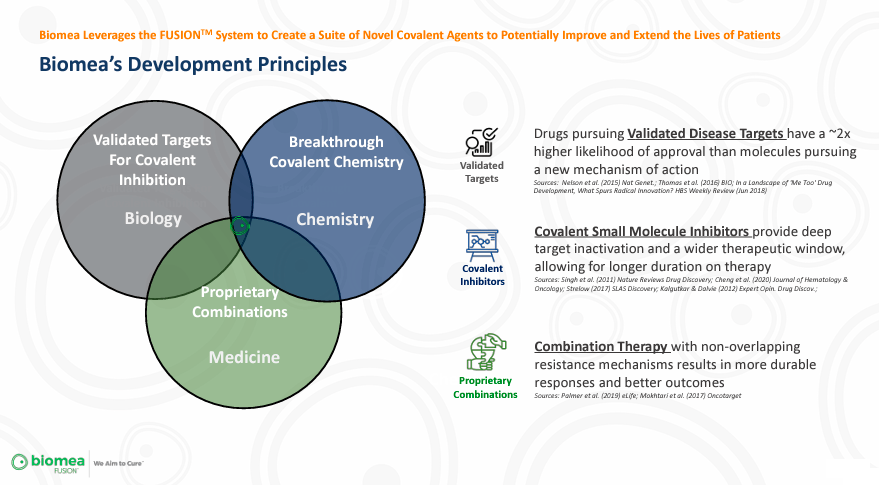

Biomea Fusion is a clinical-stage biopharmaceutical company founded in 2017 and headquartered in Redwood City, California. BMEA focuses on discovering and producing covalent inhibitor small molecules for genetically defined cancers and metabolic diseases. The company has built an R&D engine, the FUSION System discovery platform, to create synthetic compounds to form a permanent bond with target proteins that play a role in cancer and other diseases by causing oncogenic signals or impacting metabolic pathways.

This platform matters because BMEA has used it to create three covalent inhibitor programs that are in development: 1) BMF-219 menin inhibitor for treating diverse cancers and diabetes; 2) BMF-500, an FLT3 inhibitor for acute myeloid leukemia; 3) an additional oncology program for developing MYC and menin interaction inhibitors for therapies against large B-cell lymphoma, multiple myeloma, and KRAS solid tumors. The advantages of these drugs include greater target selectivity and maximization of the depth and durability of the clinical benefit for patients.

Source: Biomea Fusion, JP Morgan 2024 Corporate Presentation.

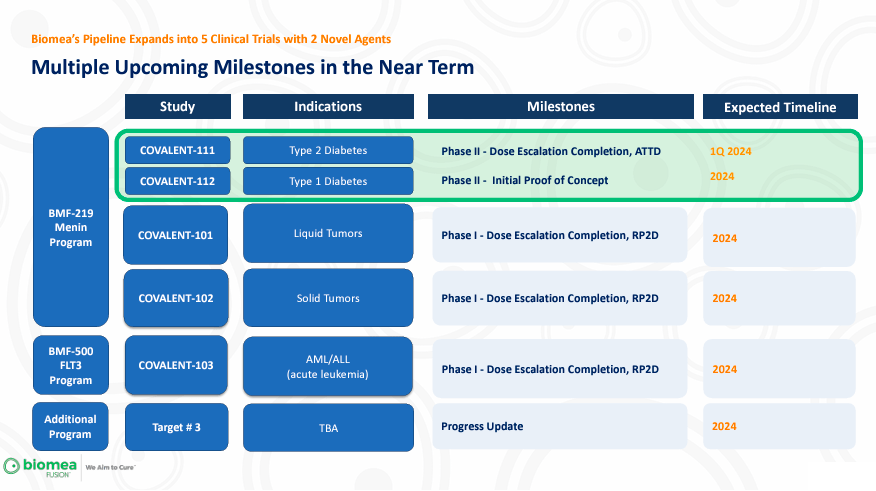

The BMF-219 program includes five covalent molecules: COVALENT-111 for type 2 diabetes in phase 2 of the clinical trials; COVALENT -112 for type 1 diabetes in phase 1; COVALENT -101 for Acute Myeloid Leukemia/Acute Lymphoblastic Leukemia [AML/ALL], Diffuse Large B-Cell Lymphoma [DLBCL], Multiple Myeloma [MM], Chronic Lymphocytic Leukemia [CLL], in phase 1; COVALENT-102 for Non-Small Cell Lung Cancer [NSCLC], Pancreatic Ductal Adenocarcinoma [PDAC], and Colorectal Cancer [CRC], in phase 1. On the other hand, BMEA’s BMF-500 program incorporates COVALENT-103 for AML/ALL leukemia in phase 1. Lastly, the company’s oncology program has a target for cancer treatments and is currently in the IND enabling phase.

Source: Biomea Fusion, JP Morgan 2024 Corporate Presentation.

Overall, the company’s portfolio mostly depends on the BMF-219-related pipeline. Particularly COVALENT-111 and COVALENT-112. However, its entire IP portfolio is relatively exciting, particularly because it focuses on oncology-related applications, which can be lucrative if successfully researched and commercialized.

Furthermore, on December 7, 2023, BMEA announced positive Phase 2 trial results for the BMF-219 program, with the COVALENT-111 molecule for treating type 2 diabetes. The data of the trial in 20 adults suffering uncontrolled type 2 diabetes who received the BMF-219 drug revealed significant reductions in HbA1C levels in 40% of participants with at least 0.5% reduction, 20% with a 1.0% or more decrease, including cuts up to 2.5%. The treatment aims to regenerate beta cells to produce insulin. The drug was well tolerated by the patients, without adverse events, corroborating BMEA’s prospects in oncology.

Despite the positive report, after a brief spike, BMEA's shares declined because the market seemed to misunderstand the data that presented residual HbA1c benefit over 22 weeks after cessation of dosing. The adjusted mean reduction in HbA1c was 0.8% at 22 weeks after their last dose of BMF-219, compared with a 0.7% placebo-adjusted mean reduction at Week 4. The market move was strange, and Citibank analysts suspected short sellers were targeting the stock.

Moreover, in BMEA’s data presented on December 9, the company indicated that at week 26, the 200mg dose of the drug in BMF-219 increased to 40% the percentage of patients with a 1% or more reduction of HbA1c levels, compared to the 20% in the 100 mg dose groups. After four weeks of treatment, patients saw meaningful HbA1c reductions and no serious adverse events for all dose groups. This means that BMEA’s treatment has statistically meaningful effects, making me think the initial market reaction was unjustified.

On January 9, 2024, BMEA highlighted results updates and anticipated 2024 milestones. At the Annual J.P. Morgan Healthcare Conference, the company presented positive results for type 2 and type 1 diabetes with the COVALENT-111 and -112 molecules. These achievements will be furthered in 2024 with the FDA and Health Canada clearing the initiation of the expansion of phase II study to evaluate the BMF-219 program in a minimum of 216 type 2 diabetes patients in a 12-week trial. They highlighted the potential of the BMF-219 program to address the cause of diabetes that could prevent disease progression. COVALENT-101 and -102 trials against liquid and solid tumors in AML and KRAS-mutant cancers are advancing in the oncology part of the BFM-219 program. Also, COVALENT-101 presented topline data in AML, achieving minimal residual disease negativity.

Source: Biomea Fusion, JP Morgan 2024 Corporate Presentation.

In 2024, BMEA expects to establish recommended phase 2 doses for COVALENT-101, -102, and COVALENT-103 of the BFM-500 program. The third molecule candidate for cancer treatment will be announced as a 2024 BMEA milestone. So these announcements show that BMEA is making important advancements in the research of diabetes and oncology treatments with positive data for its BFM-219 program for diabetes type 1 and 2, with the potential to cure the disease's root cause. Furthermore, the oncology programs also present progress, with AML and KRAS-mutant cancer treatments advancing steadily.

These are no small feats, and I believe the market is not fully pricing in the company’s potential if successful. Naturally, the expansion of phase 2 studies is a key milestone for the BFM-219 program. These results make me optimistic about BMEA’s research in 2024.

Lastly, from a valuation perspective, BMEA holds roughly $199.1 million in cash and equivalents. During the last quarter, I estimate the company burned through $23.9 million in cash, which annualized implies a burn rate of $95.6 million. I obtained these figures by adding the company’s CFOs and Net CAPEX. Overall, this means a cash runway of approximately 2.1 years. This is not a terrible amount of time, but I think it leaves the company with little room for mistakes. After all, if 2024 doesn’t deliver the expected results, they’ll likely be forced to tap into additional financing in unfavorable terms, and stock dilution is not out of the cards. Additionally, the company needs to produce meaningful revenues.

Moreover, BMEA currently trades at a P/B ratio of about 2.86, which, compared to the sector median of 2.36, signals a slight overvaluation from a balance sheet point of view. This, coupled with the company’s lack of concrete cash flow prospects in the near term and dwindling liquidity, leads me to temper my optimism on the stock in the near and medium term. However, I can’t be bearish on the company, as its research is quite promising. Hence, a “hold” rating captures this balance of bullish and bearish factors in my analysis.

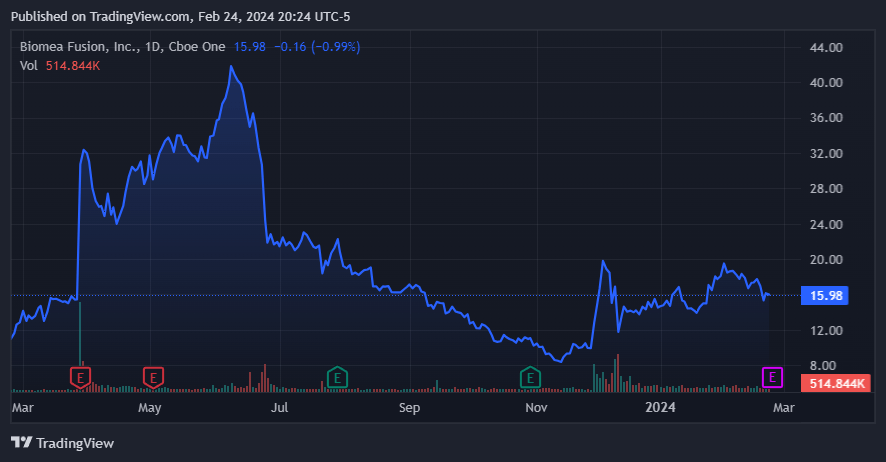

Trading sideways after a year of progress. Source: TradingView.

Indeed, the company's cash burn and lack of revenue catalysts in 2024 are concerning enough. However, it's also worth emphasizing that BMEA's main selling point is that it could be a viable alternative for treating diabetes and cancer caused by genetic reasons. The company's focus on covalent inhibitors opens previously undruggable genes and proteins as potential "druggable" targets. This effectively creates a substantial market opportunity for BMEA if it researches and commercializes BMEA. For instance, in diabetes type 2, BMEA's competitors could be Ozempic and Mounjaro, which have expected peak sales of over $10.0 billion. If BMEA were to do even just 5% of those figures, it'd represent roughly $500 million in yearly revenues. This hypothetical revenue justifies the stock's current market cap of $570.6 million. This is because it'd imply a forward P/S ratio of 1.14, which seems cheap compared to the sector median forward P/S multiple of 3.96.

Source: ACSH.org.

However, most of the company's pipelines are in diabetes and oncology, and oncology, in particular, has relatively low odds of approval. Since the company's oncology portion of its IP is still in Phase 1, there's still a long way to go before this research translates into meaningful revenue. But even the diabetes research itself is still in Phase 2, which doesn't quite change the company's outlook at this juncture either. These are key risks embedded in BMEA at this time, and even though the company's angle is innovative and potentially opens up treatment for previously unreachable proteins, the reality is that this IP is far away from having a positive impact on the company's financials.

Yet, in 2024, there are still some catalysts that investors have to look forward to, which could be well received by the market and give the shares some fuel for the upside. In particular, we'll get some updates about BMEA's COVALENT-111 in March at the Advanced Technologies and Treatments for Diabetes Meeting. Here, the company is expected to present additional data that could cause the market to upgrade its view on the stock. Likewise, in 2024, BMEA will finish enrolling three expansion cohorts for this drug. On the other hand, COVALENT-112 will complete its enrollment for the open-label portion, establishing the initial proof of concept for Type 1 diabetes patients.

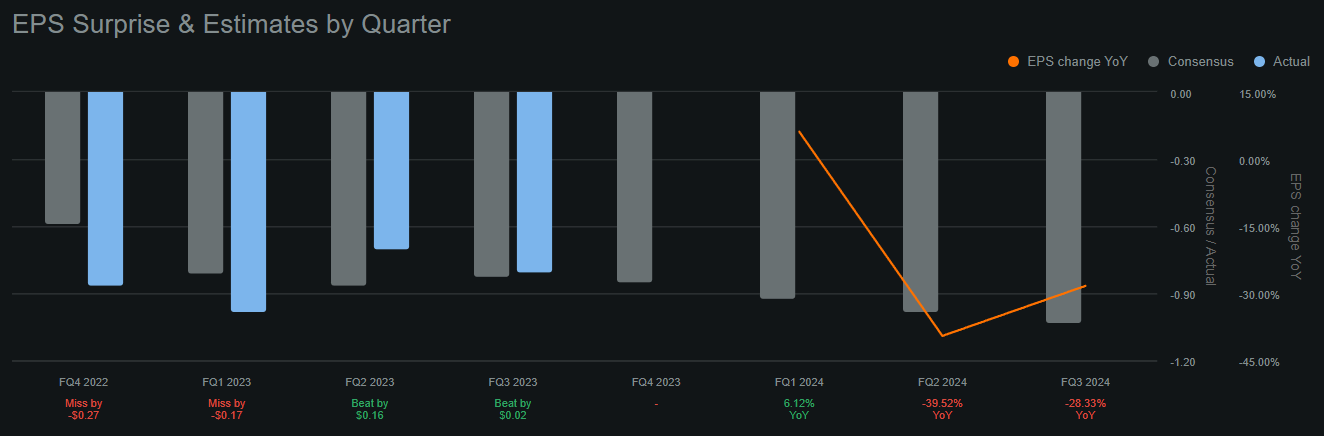

BMEA continues to accumulate losses despite promising research progress. (Source: Seeking Alpha.)

Unfortunately, the company is still projected to accrue losses in the future. Analysts expect BMEA to post a $0.85 loss per share in Q4 2023, which, compared to the current share price of $16.85, is indeed a significant hit. Moreover, these losses will likely persist into 2024, so holding the stock is not without risks, and shareholder value erosion over time is a real possibility. So I see that BMEA has ample upcoming catalysts in 2024 that could potentially uncover a pathway to revenue generation, licensing deals, or M&A to create shareholder value. But for now, I think the company's current valuation and prospects appear balanced, leading me towards a neutral stance on the stock.

I think BMEA’s research portfolio is promising, and I believe they’ll get positive results in 2024. Diabetes and oncology can be quite lucrative, and BMEA’s research is at the center of these fields, making good progress so far. However, from a financial perspective, I think the near-term lack of cash flows must be considered when evaluating the stock’s prospects. While I concede that they have enough cash runway to last into 2026, I also believe two years for a pre-revenue company is not that great. Thus, I lean towards a neutral rating for BMEA, giving it a “hold” for now.