hirun

hirun

PowerSchool Holdings, Inc. (NYSE:PWSC) has reported its Q4 2023 financial results, missing both revenue and earnings estimates.

I previously wrote about PowerSchool in July 2023 with a Hold outlook on slower revenue growth and continued operating losses.

Software companies such as PowerSchool Holdings, Inc. may see reduced development costs with the aid of AI technologies over time, and its free cash flow has shown improvement.

However, revenue growth is moderate and operating results have proven uneven due to customer timing issues.

I’m Neutral [Hold] on PWSC for the near term.

With its education administration cloud software platform, PWSC pursues primarily K-12 school districts in North America and to a lesser extent, internationally.

It sells directly through its in-house sales team in its core markets and through resellers elsewhere and offers a modular approach to the various functions that can benefit from software automation.

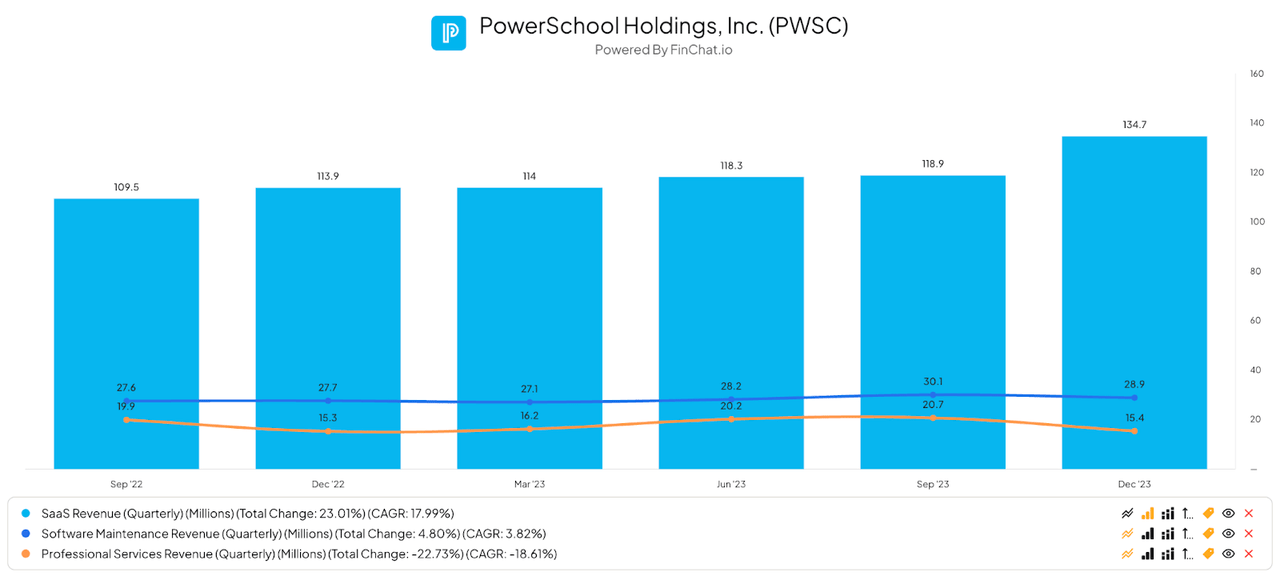

PWSC’s main revenue segments are SaaS Revenue, Software Maintenance and Professional Services, as shown in the chart here:

FinChat.io

Also, for the trailing twelve-month period by region, U.S.-sourced revenue accounted for $648.6 million (93%) and Canada / International revenue was $49.1 million (7%), with most of the growth coming from the U.S.

The company also licenses APIs (Application Programming Interfaces) for partners to develop their own plug-in options.

More recently, PWSC has been incorporating AI technologies to enable educators to personalize education content through its "PowerBuddy" assistant.

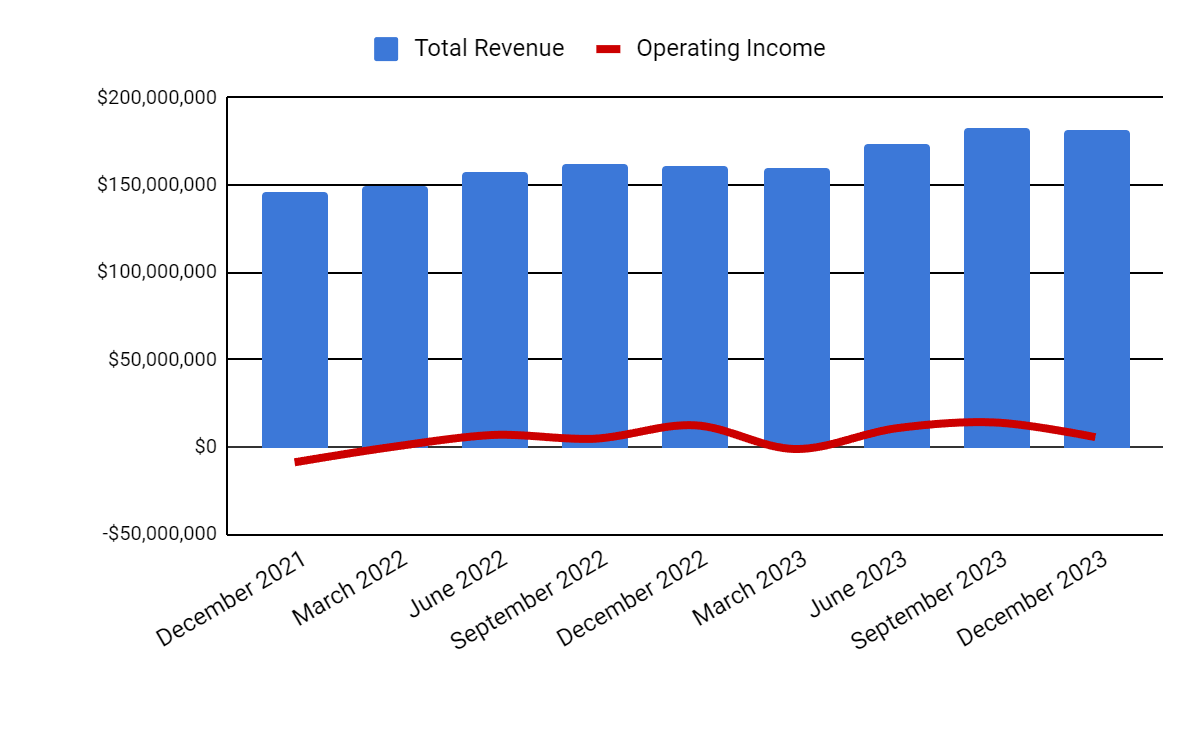

Total revenue by quarter (columns) has risen materially in recent quarters (YoY) due to improved cross selling results; Operating income by quarter (line) has dropped due to higher SG&A expenses and the timing of large deals being implemented.

Seeking Alpha

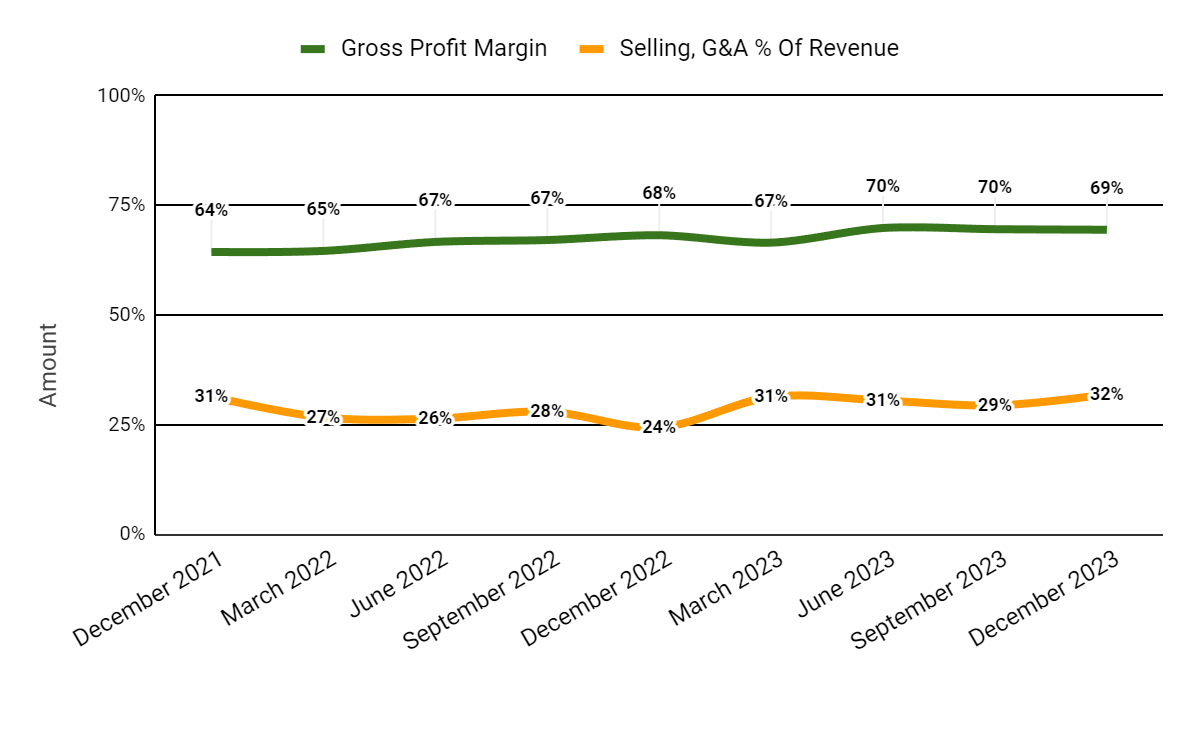

Gross profit margin by quarter (green line) has been trending higher as a result of greater operations scaling and process efficiencies; Selling and G&A expenses as a percentage of total revenue by quarter (orange line) have also moved up recently due to more sales and marketing investment in its international expansion efforts.

Seeking Alpha

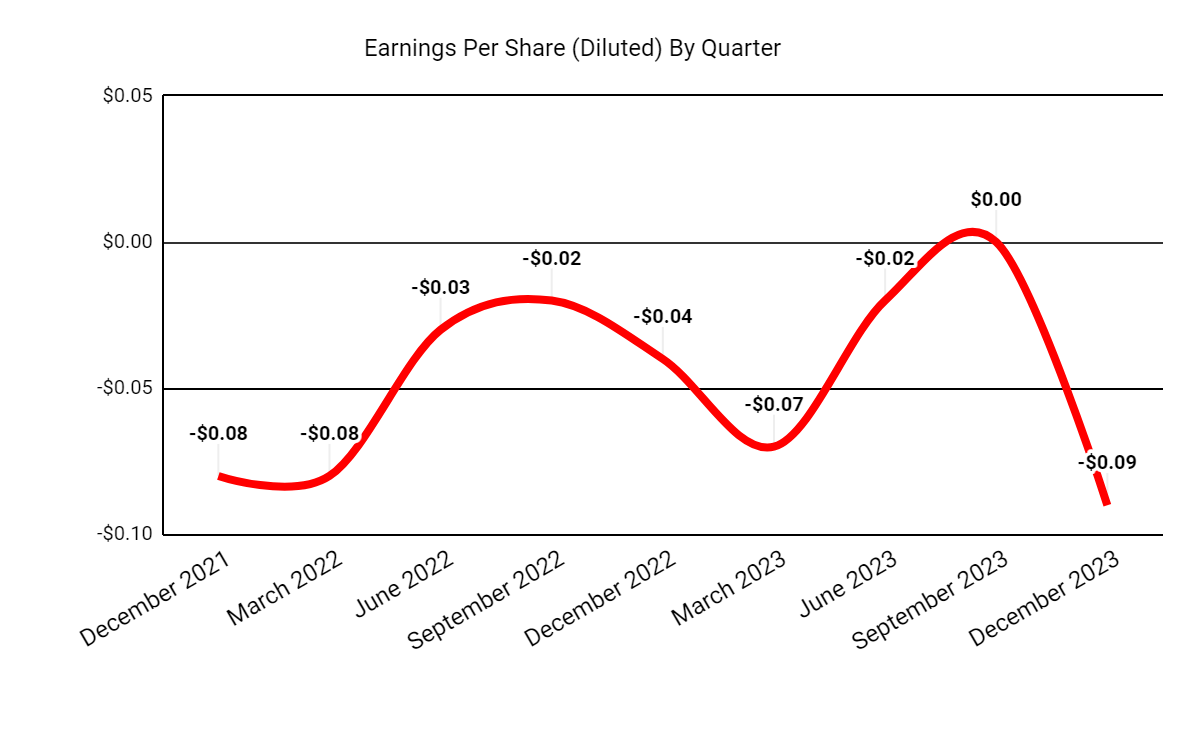

Earnings per share (Diluted) have dropped sharply into negative territory in the most recent quarter, beyond normal seasonality, due to higher SG&A expenses.

Seeking Alpha

(All data in the above charts is GAAP.)

The following table shows certain financial metrics for PowerSchool when compared to competitor Blackbaud, Inc. (BLKB):

Metric | Blackbaud | PowerSchool Holdings | Variance |

EV/Sales ("FWD") | 3.8 | 6.0 | 56.9% |

EV/EBITDA ("FWD") | 11.6 | 17.6 | 51.9% |

Rev. Growth Estimate ("FWD") | 6.4% | 11.5% | 80.1% |

Net Income Margin | 0.2% | -4.5% | --% |

Operating Cash Flow | $199,630,000 | $170,590,000 | -14.5% |

(Source: Seeking Alpha.)

PWSC is being valued at a significantly higher EV/Sales multiple due to its higher forward revenue growth estimate, which appears reasonable.

Below is a major metrics table that shows various forward or trailing twelve-month results for PWSC:

Metric | Amount |

EV/Sales ("FWD") | 6.0 |

EV/EBITDA ("FWD") | 17.6 |

Price/Sales ("TTM") | 4.9 |

Revenue Growth ("YoY") | 10.6% |

Net Income Margin | -4.5% |

EBITDA Margin | 18.6% |

Market Capitalization | $4,280,000,000 |

Enterprise Value | $4,740,000,000 |

Operating Cash Flow | $170,590,000 |

Earnings Per Share (Fully Diluted) | -$0.18 |

2024 FWD EPS Estimate | $0.99 |

Rev. Growth Estimate ("FWD") | 11.5% |

Free Cash Flow/Share ("TTM") | $0.80 |

Seeking Alpha Quant Score | Hold - 2.88 |

(Source: Seeking Alpha.)

The company's "Rule of 40" performance history is shown here, with the firm’s operating margin dropping materially in Q4 2023 vs. that of Q1 2023:

Rule of 40 Performance (Unadjusted) | Q1 2023 | Q4 2023 |

Revenue Growth % | 8.6% | 10.6% |

Operating Margin | 17.0% | 3.1% |

Total | 25.6% | 13.8% |

(Source: Seeking Alpha.)

PWSC’s success is based on its ability to cross-sell its product modules, in essence a true "land and expand" approach.

Management is also seeking to expand its footprint internationally through resellers and partnerships, notably in Latin America and Saudi Arabia.

With the recent launch of its personalized AI technology PowerBuddy, the sales team has seen solid demand for the new capability.

One thing we are starting to see with AI coding capabilities, is the potential for a lower COGS as software companies use AI to reduce support and development costs.

While these savings will play out over a longer time frame, AI technologies may serve to make software companies like PWSC more profitable as they are frequently the earliest adopters of these types of technologies.

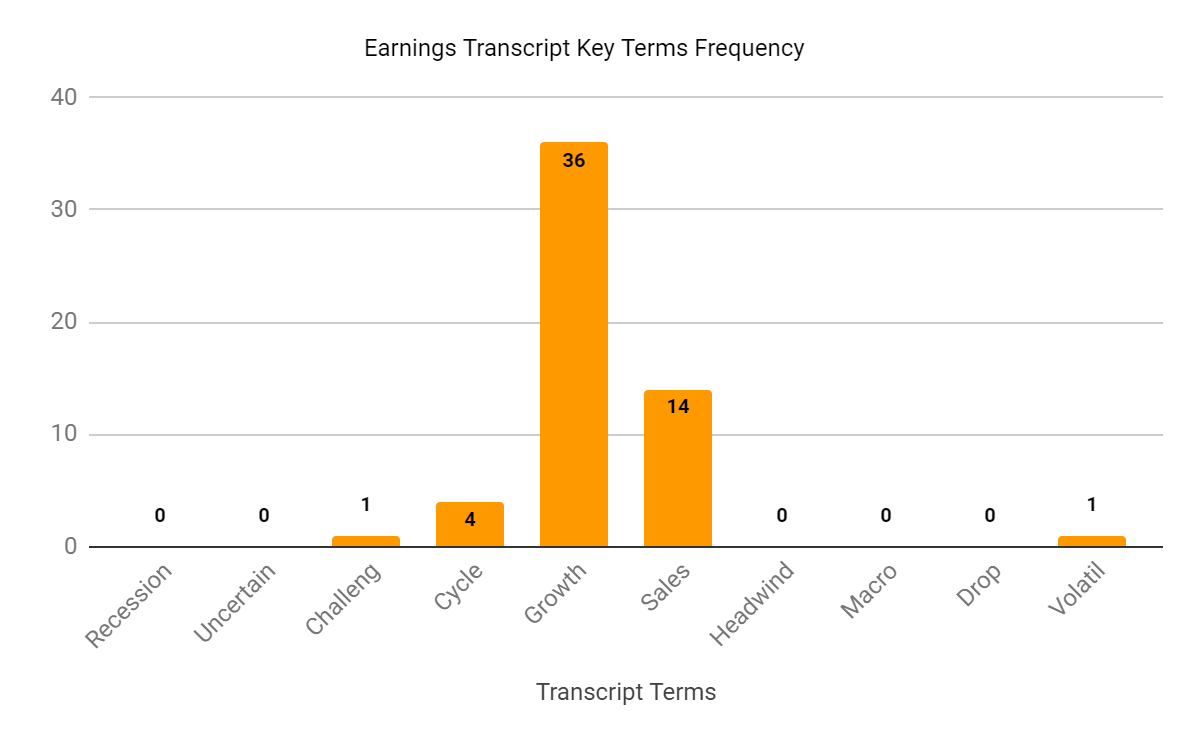

I prepared the following "sentiment indicator" chart which shows the frequency of certain keywords in the most recent analyst conference call with management:

Seeking Alpha

The chart shows that the firm is facing some volatility from large deal sizes, but otherwise there are few mentions of negative terms.

Notably, free cash flow grew by 25% in 2023 on "improved working capital and lower capitalized product development costs, which helped offset higher interest expenses."

Forward revenue growth expectations are around 11.5% vs 2023’s growth of 10.6%, so it appears the firm’s growth rate may increase nominally.

The question for investors is whether the firm’s growth rate and operating income profile will produce a meaningful catalyst for the stock.

With a "slower for longer" cost of capital reduction as inflation remains sticky, the valuation environment for moderately-growing companies with little or no earnings may be challenged.

While PWSC’s free cash flow growth is a real bright spot, it is likely already priced into the stock and I’m skeptical that the company will be able to continue to grow free cash flow by 25% on a regular basis going forward.

So, my outlook for PWSC remains Neutral [Hold], although the stock may be volatile on timing of large deals from quarter to quarter.