TW Farlow

TW Farlow

If you have difficulty admitting that you are wrong, you absolutely will not make for a good investor. The fact of the matter is that investment decisions made by even the best of us are not always correct. Over the past couple of years, I have worked hard to make sure that I am more open with myself so that I can learn from my mistakes. One company that I have been dead wrong about, for instance, is Blue Bird Corporation (NASDAQ:BLBD), a firm that's focused on the electrification of buses. Back in March 2022, very close to two years ago from the current date, I talked about how the company had a rough couple of years. The worst at that time appeared to be over, and I even acknowledged that shares could be undervalued. But at the end of the day, a lot was riding on whether or not management's expectations would come to fruition. Because of the uncertainty associated with that, I ended up rating the business a 'hold'.

Since then, things have gone far better than anticipated. The company has seen rapid growth and cash flows are looking robust. Net debt remains low and management's forecasts are now believable. Unfortunately, my skepticism caused me to miss out on some attractive gains. Because while shares of the S&P 500 are up 15.8% since I last wrote about Blue Bird, its stock is up a whopping 53.5%. Given the data now, I don't plan to make that same mistake again. While shares are not the cheapest on the market, they do look attractively priced and the growth outlook for the company is rather robust. Because of these factors, I have decided to upgrade the stock to a 'buy' to reflect my view that shares are likely to continue outperforming the broader market for the foreseeable future.

Author - SEC EDGAR Data

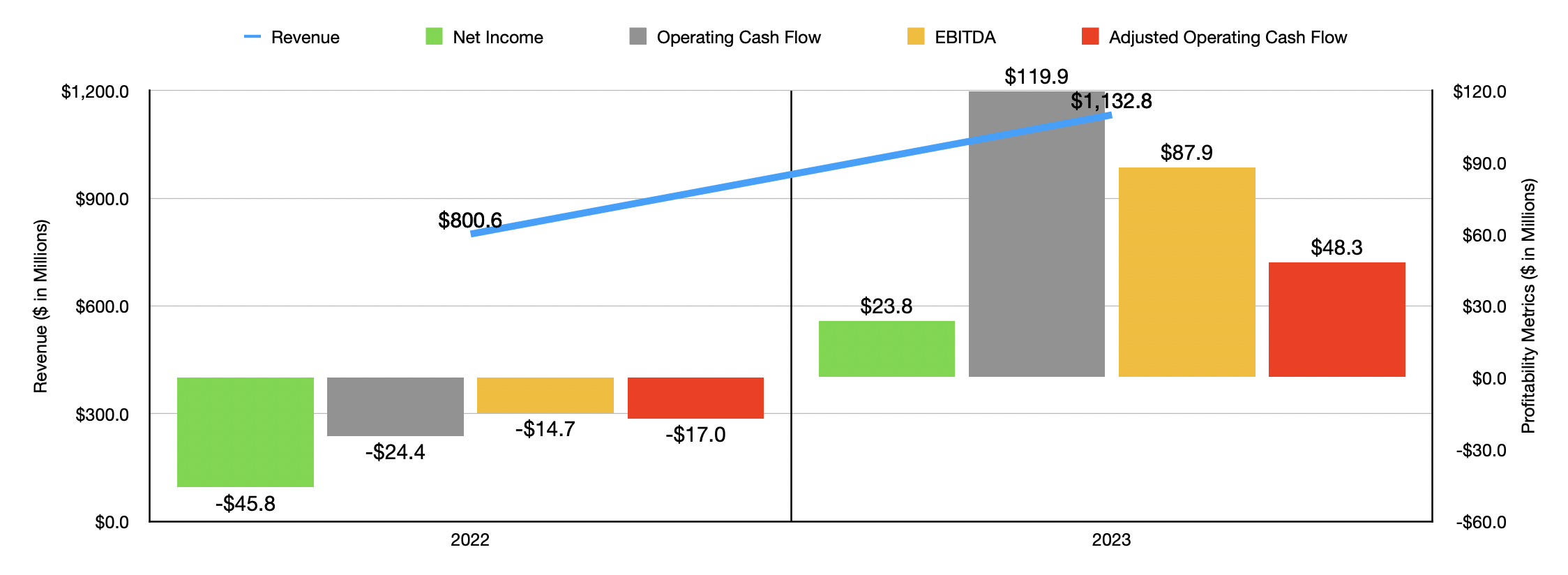

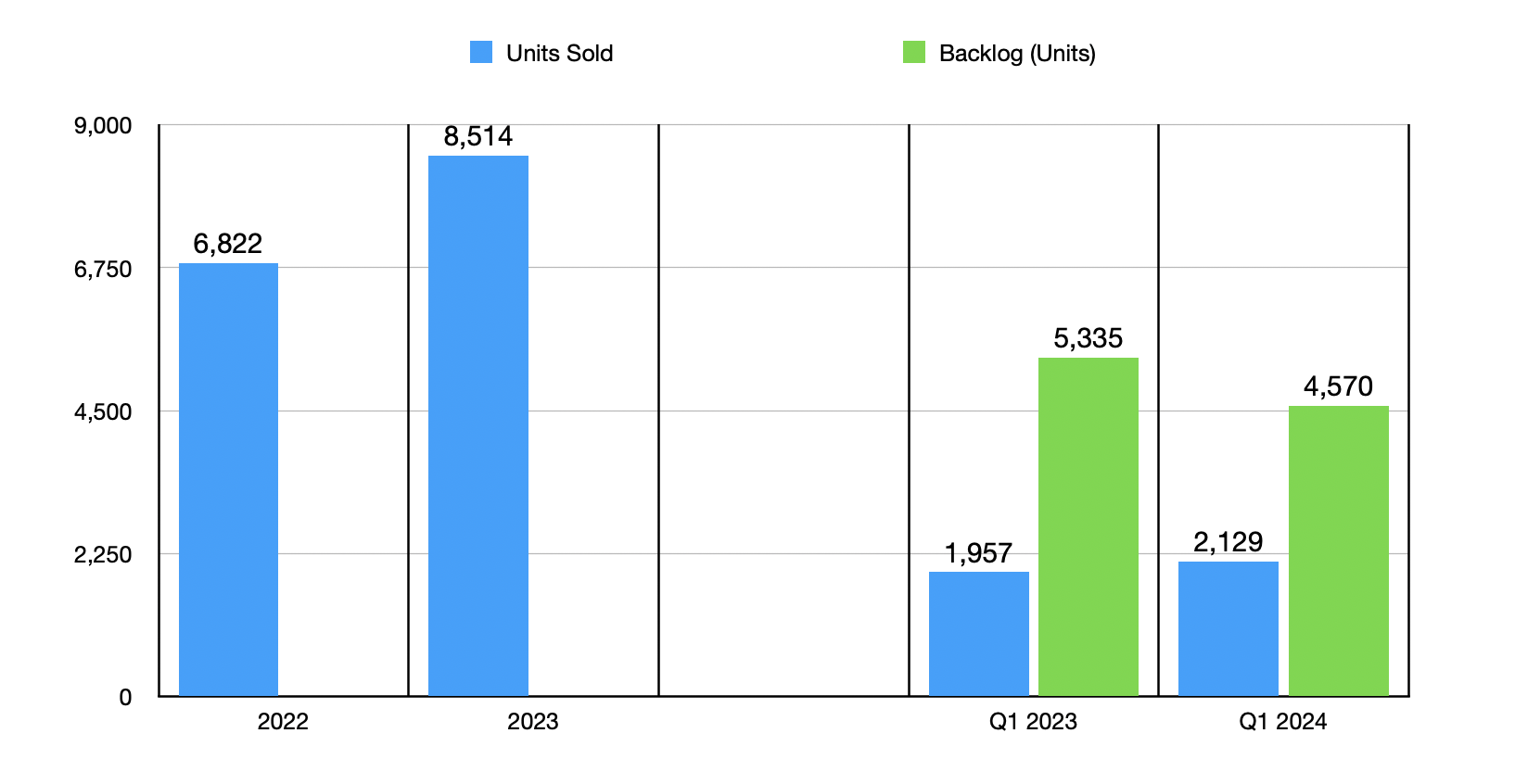

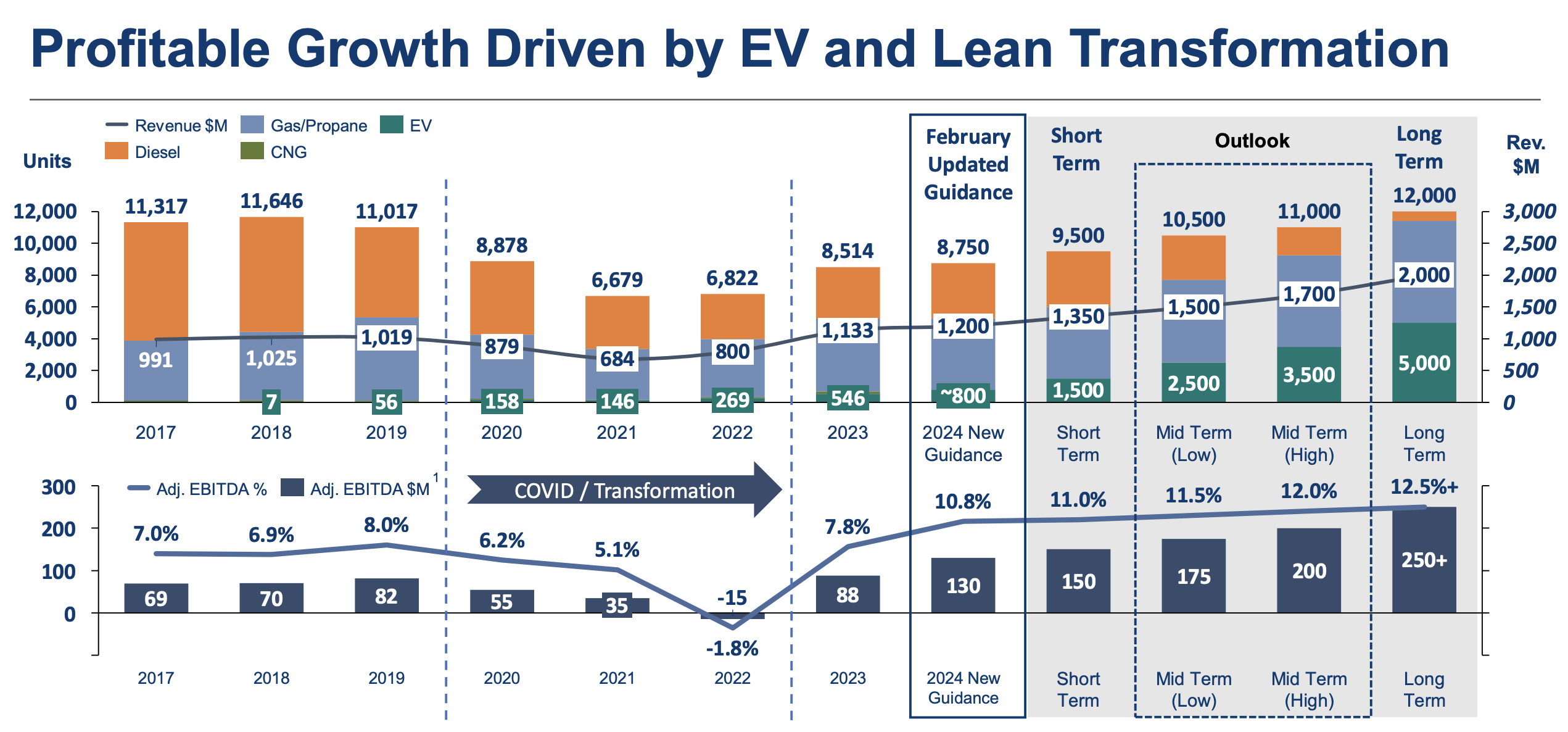

Fundamentally speaking, things are going really well for Blue Bird at this time. At a time when the electric vehicle space has seen the share prices of the companies in it suffer, Blue Bird has bucked the trend. Take revenue for instance. In 2023, sales came in at $1.13 billion. That represents an increase of 41.5% compared to the $800.6 million generated one year earlier. While the company did experience a nice increase in revenue associated with its Parts segment, with sales climbing from $77.1 million to $98.2 million, most of the increase came from a much larger Bus segment. Sales spiked 43%, or $311.1 million as the company enjoyed an increase in the number of units booked and a 14.6% increase in the average sales price per unit. The company booked 8,514 units in 2023. That's a sizable increase over the 6,822 units booked in 2022.

Author - SEC EDGAR Data

The increase in volume, combined with higher pricing, worked wonders for the firm's bottom line. The company went from a net loss of $45.8 million in 2022 to a net profit of $23.8 million in 2023. Other profitability metrics followed suit. Operating cash flow went from negative $24.4 million to positive $119.9 million. If we adjust for changes in working capital, we get a rise from negative $17 million to positive $48.3 million. Meanwhile, EBITDA turned from negative $14.7 million to positive $87.9 million.

Author - SEC EDGAR Data

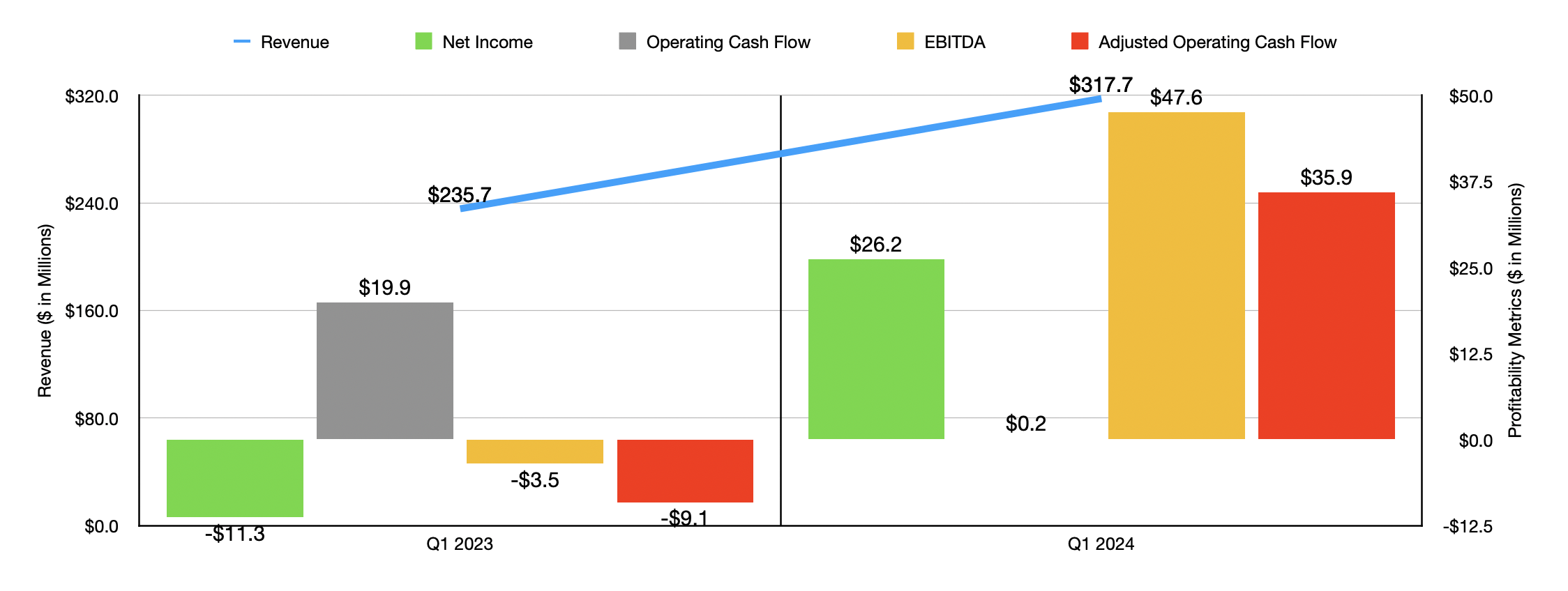

Attractive performance has continued into the 2024 fiscal year. During the first quarter of the year, management reported sales of $317.7 million. That's an increase of 34.8% over the $235.7 million reported at the same time in 2023. Once again, the vast majority of the increase came from the Bus segment, with revenue spiking 37.6% as the company enjoyed an 8.8% rise in units booked, taking that number from 1,957 to 2,129, and as it benefited from a 26.5% increase in average sales price per unit. Naturally, this combination worked wonders again on the bottom line. As you can see in the chart above, net profits and two of the three cash flow metrics for the company, all improved year over year. If there is any downside to this, it's that the backlog did manage to fall year over year, declining from 5,335 units to 4,570. But it's necessary to keep in mind that the company had faced a couple of years of supply chain constraints when it came to certain components that ended up causing an inflated backlog. So I don't see this as an issue at this time. Obviously, if it continues to fall, my mindset on the matter could change. But for now, the backlog looks just fine.

Author - SEC EDGAR Data

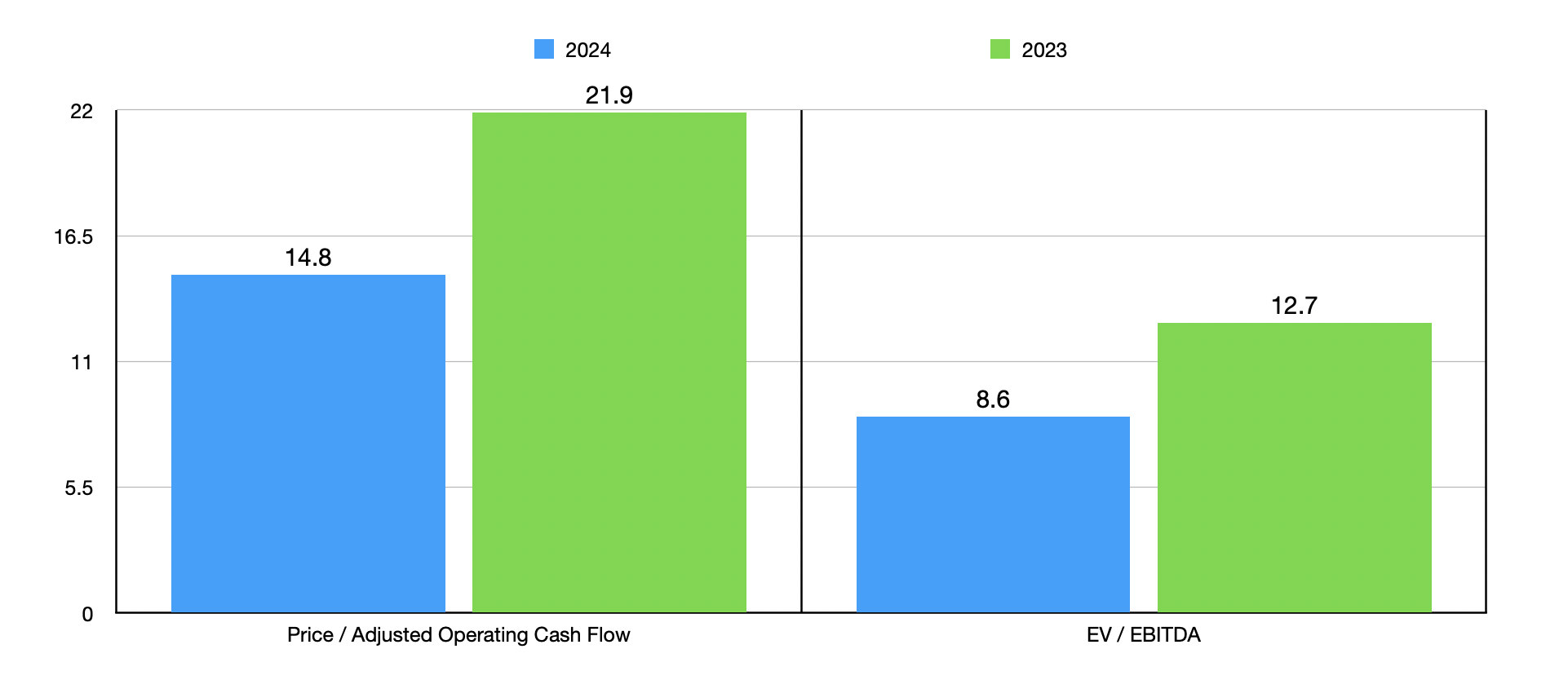

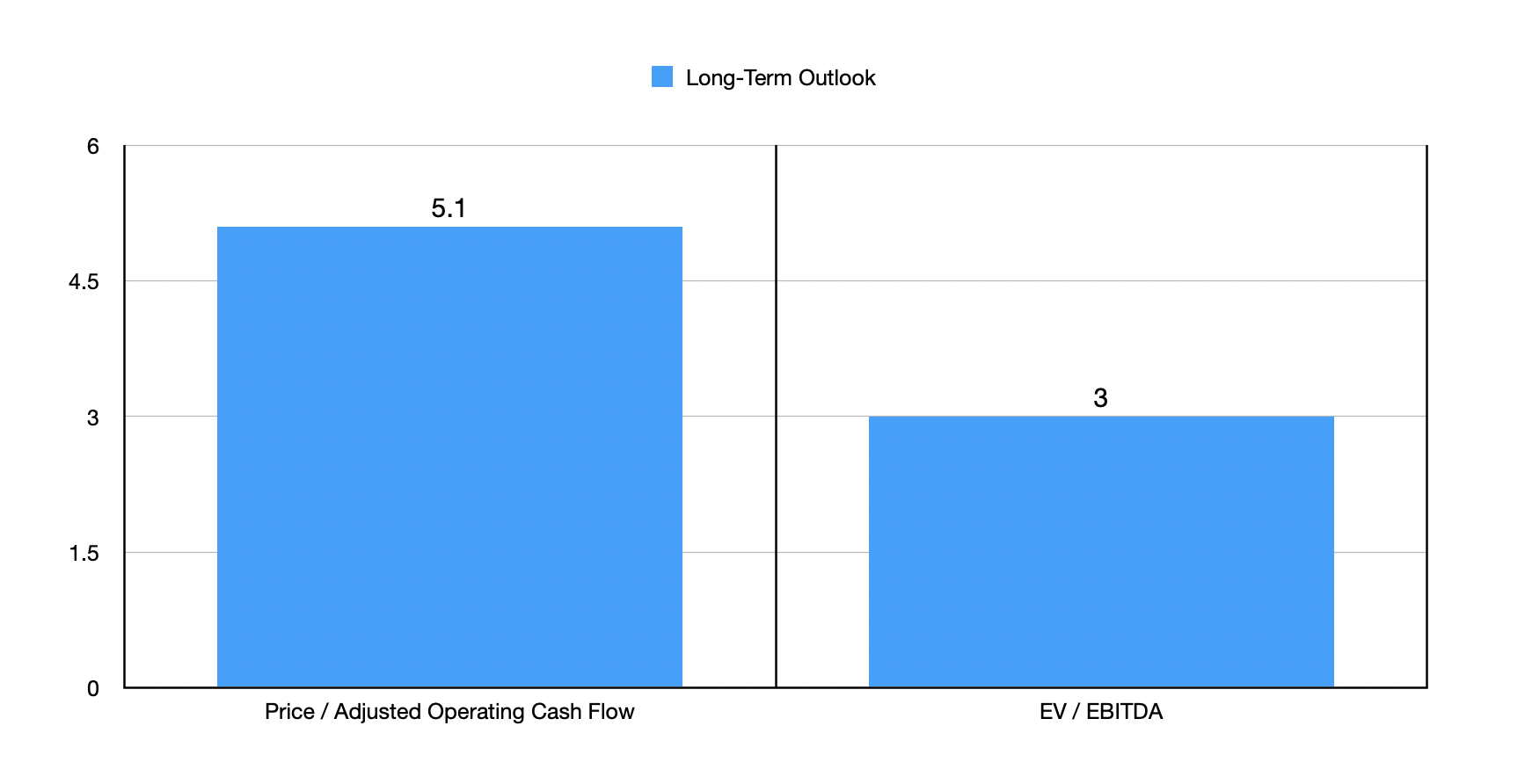

When it comes to the 2024 fiscal year in its entirety, management expects revenue of between $1.15 billion and $1.25 billion. While this is not terribly large compared to the $1.13 billion generated in 2023, management believes that the bottom line will improve markedly. They anticipate EBITDA, for instance, of between $120 million and $140 million. If this comes to fruition, it should translate to an adjusted operating cash flow of at least $71.4 million. Using these figures, valuing the company becomes quite easy. As you can see in the chart above, the stock looks quite cheap when it comes to the EV-to-EBITDA approach. But relative to operating cash flow, shares look much closer to being fairly valued.

The meaningful improvement in profitability expected for this year has also prompted management to make a big bet on the future of the business. On February 1, the firm announced a $60 million share buyback program. For companies that are this small and that are at this stage of their expected life cycle, I am highly critical of share buybacks. But given how positive cash flows are, this is an interesting bet that the share price would be substantially higher than it is today at some point in the distant future. Based on the available data, I would say that bet has a pretty good chance of paying off.

Blue Bird

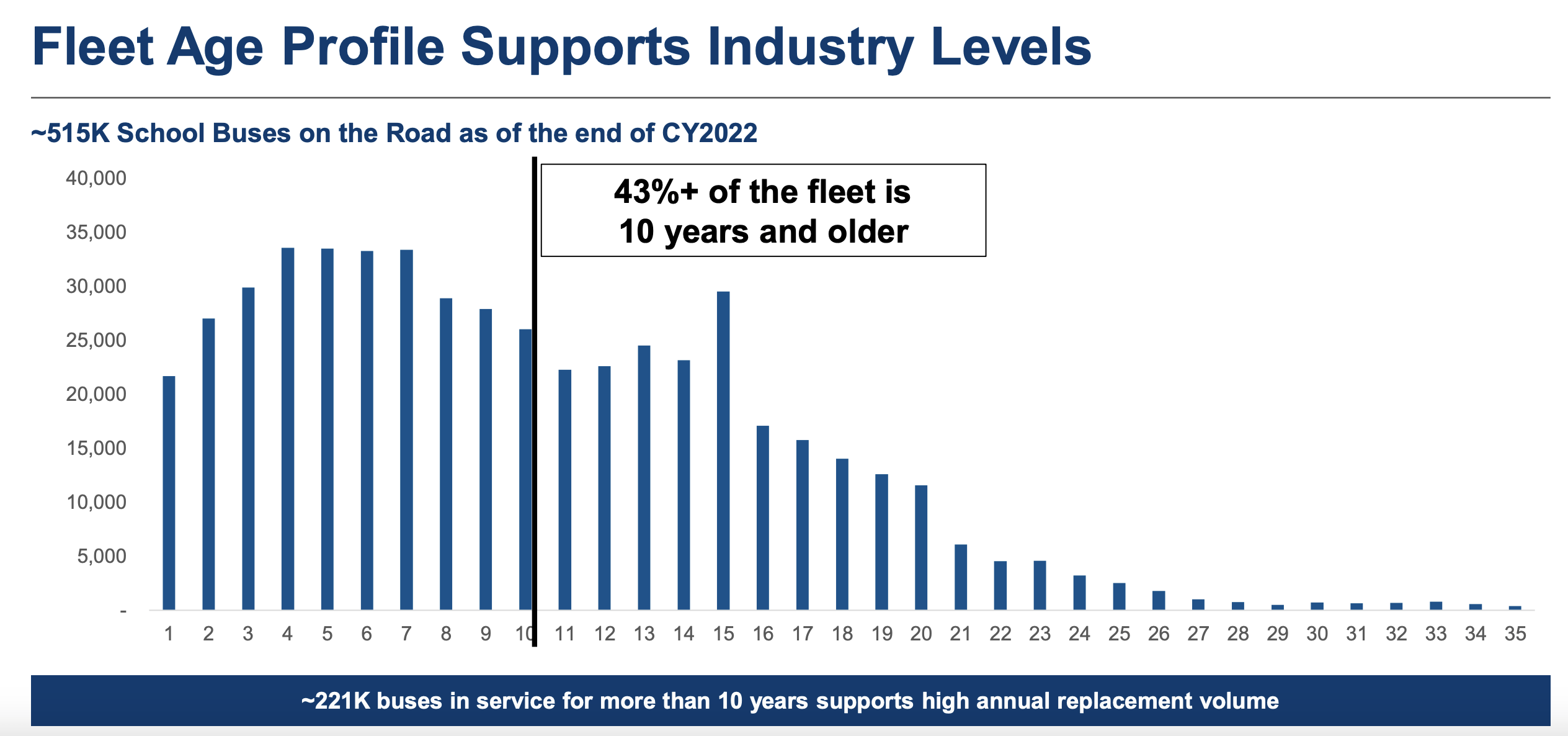

According to management, school buses are America's largest mass transit system. There are about 515,000 of them in operation across the US and Canada alone. And every school day, they are responsible for transporting around 26 million children. Every year an average of about 30,500 new units are ordered to replace those that are older. This works quite well from a timing perspective because, in most states at least, 15 years is set as the replacement target for school buses. As of this writing, about 43% of the fleet and the markets in which the firm operates are 10 years of age or older.

To encourage more environmental practices, governments have invested heavily in various initiatives. One grant program back in 2023 that was passed by the EPA saw $965 million in funds allocated for the purchase of 2,737 'clean' buses. Round three of that program will be at least $500 million and will be awarded between April and May of this year. It is possible that those funds could be increased. I say this because the second round of that grant, which was allocated last year, was originally planned to be only $400 million. Of course, this only helps with some pictures. But what's really exciting are the expectations that management has for the next few years.

Blue Bird

For this year, management is forecasting around 8,750 units being ordered. But over the next several years, this should grow to around 12,000 units per annum. As revenue increases, profit margins are also expected to rise. Based on current estimates, achieving an EBITDA margin of 12.5% on the long-term target for the company would result in an EBITDA of $375 million annually based on revenue of around $3 billion. If we assume that adjusted operating cash flow should rise at the same rate, we should expect a reading of about $206 million there. As you can see in the chart below, this would bring the trading multiple of the company down rather substantially.

Author - SEC EDGAR Data

At this time, I see no reason to be pessimistic when it comes to Blue Bird. Personally, I would prefer that the share buyback funds be allocated to additional growth. That or the company could use it to pay off the $58.8 million in net debt that it has on its books. Regardless, there are some improvements I would make if I were running the show. But at the end of the day, those improvements are just fine-tuning adjustments. The company as a whole seems to be doing really well and the upside for investors over the next few years should be attractive. Given these factors, I've decided to upgrade the stock from a 'hold' to a 'buy'.