Vertigo3d/iStock via Getty Images

Vertigo3d/iStock via Getty Images

Some people who don't want to buy Bitcoin USD (BTC-USD) or other cryptocurrencies have considered investing in an ETF focused on that sector. One such fund is Bitwise Crypto Industry Innovators ETF (NYSEARCA:BITQ). I was curious to see how exactly how it allocates its capital, so I gave it a look.

While I have been skeptical of crypto for a long time, there are risks worth observing with this fund, even if you feel good about crypto as an asset. I'll talk about its main holdings and why I think folks would be better-served selling and not endangering their capital.

BITQ is passively invested to track the results of the Bitwise Crypto Innovators 30 Index, a crypto index also developed by Bitwise. In their description of the Index, they note:

The index is divided into two tiers: not less than 80% of the index comprises a pure-play tier ("Tier 1"), composed of companies that are primarily focused on the crypto market, and a not more than 20% of the index comprises a supporting tier ("Tier 2"), composed of large-cap companies with diversified business interests that include at least one significant public business line focused on the crypto market

Through a fund based on this, it provides investors "exposure to the crypto economy" through more traditional means of investment and with none of the requirements that come with trading and holding crypto directly. As such, both the fund and the Index will be impacted by the fluctuations in the prices of cryptocurrencies and the shares of the companies.

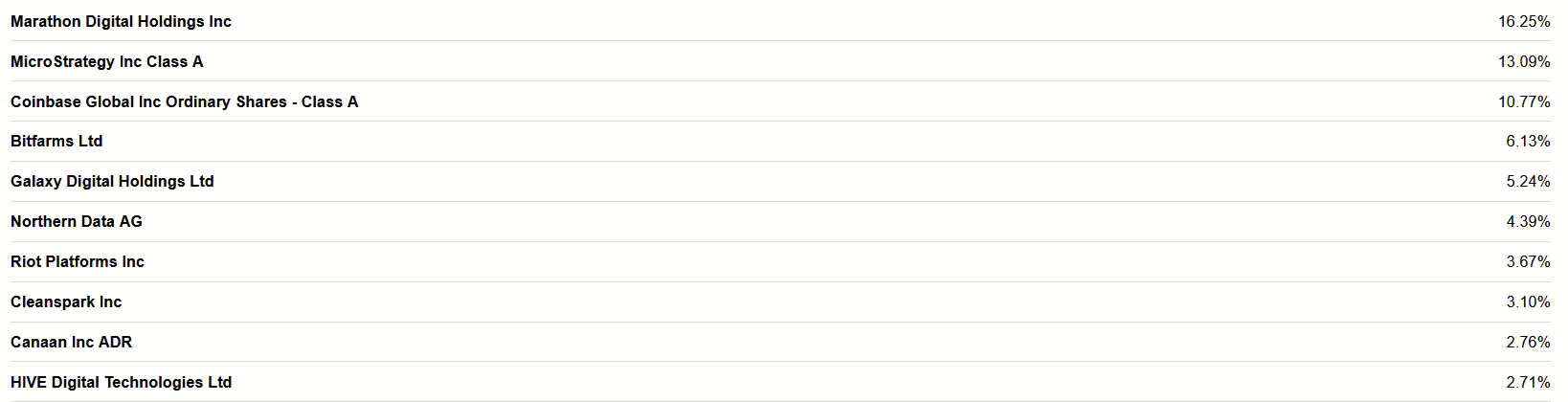

Seeking Alpha

These companies account for just over two-thirds of the fund. It's worth noting that this composition does shift a bit, as these investments have very volatile price movements, but overall, I think an analysis of this group should give us an idea of the kind of returns BITQ can deliver. Let's hop into that.

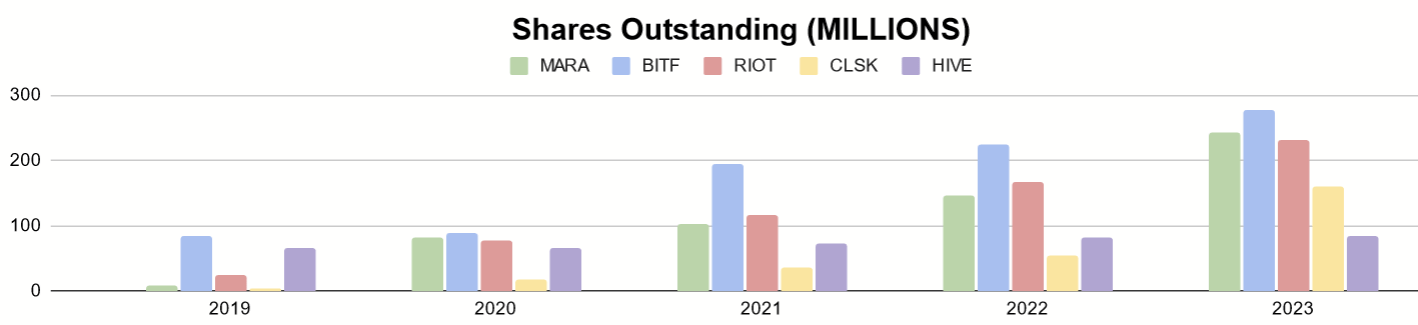

Most of these holdings are mining companies that primarily or exclusively set up their operations to mine BTC. This includes Marathon Digital Holdings, Inc. (MARA), Bitfarms Ltd. (BITF:CA), Northern Data AG, Riot Platforms, Inc. (RIOT), CleanSpark, Inc. (CLSK), and HIVE Digital Technologies Ltd. (HIVE:CA).

Example of immersion-cooling, common for miners (anandtech.com)

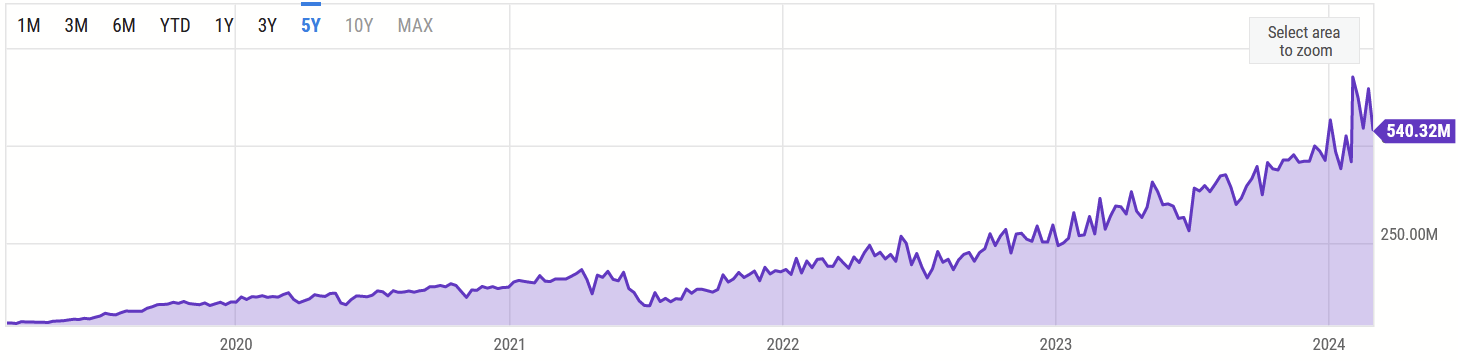

Mining entails finding cryptographic hashes in a global network. This means it is a competitive process, leading to an arms race among all mining companies to increase their own hash rate. The more miners who participate, the more the number of hashes needed to solve a block (the hash rate) increases. This chart below shows the growth of the hash rate over time.

Ycharts.com

From an operational perspective, this makes it progressively difficult for mining companies to produce BTC profitably. Riot, which I've covered before, gives significant discussion on this matter, and it explains why these companies tend to generate negative free cash flow. They have to keep spending cash on new miners. As Riot itself explains (2023 Form 10-K, pg. 20):

Therefore, our Mining operations focus exclusively on mining Bitcoin, and our Mining revenue is based on the value of Bitcoin we mine. Accordingly, if the value of Bitcoin declines and fails to recover, for example, because of the development and acceptance of competing blockchain platforms or technologies, including competing cryptocurrencies which our miners may not be able to mine, the revenue we generate from our mining operations will likewise decline. Moreover, because our miners use these highly specialized ASIC chips, we may not be able to successfully repurpose them in a timely manner, if at all, if we decide to switch to mining a different cryptocurrency (or to another purpose altogether) following a sustained decline in Bitcoin's value or if Bitcoin is replaced by another cryptocurrency not using the SHA-256 algorithm.

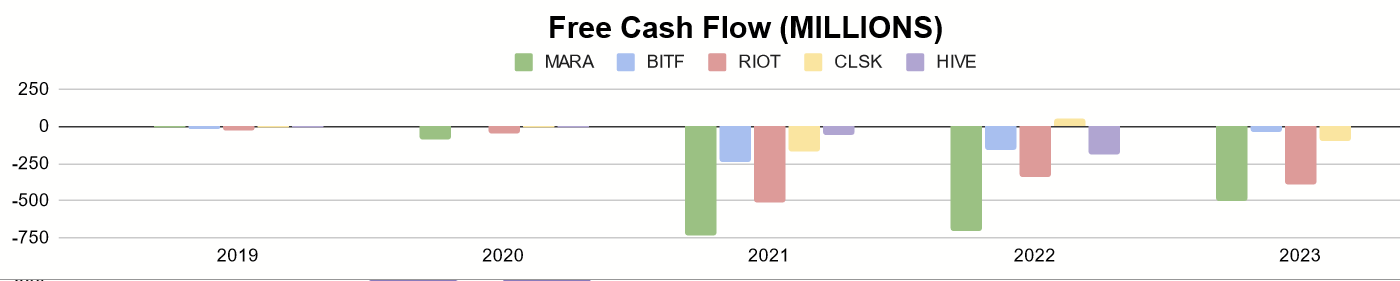

The history of the cash flows makes clear how big this risk is. Below I've aggregated the free cash flow of five of those companies, based on their reported data for 2019-2023. Keep in mind these align with their fiscal years.

Author's display of reported data

What we see here is that free cash flow is typically negative, and scaling only magnified the problem. We see this growth resulting after the COVID-19 stimulus brought a lot of retailer investors into the market, which also explains the origins of BITQ (formed in 2021).

This net cash outflow is a shared problem and risk for the mining companies in this fund. While funds usually offer some level of diversification away from certain risks, that doesn't appear to be offered here. Without a clear path to positive cash flows, I believe many of these companies will have to keeping selling new shares (and thus reducing their value) to remain operational. I'll also show how much dilution has occurred to make up this difference.

Author's display of reported data

In BITQ's lifetime, not only has the cash outflow stepped up, but so too has the dilution of the fund's equity in these companies.

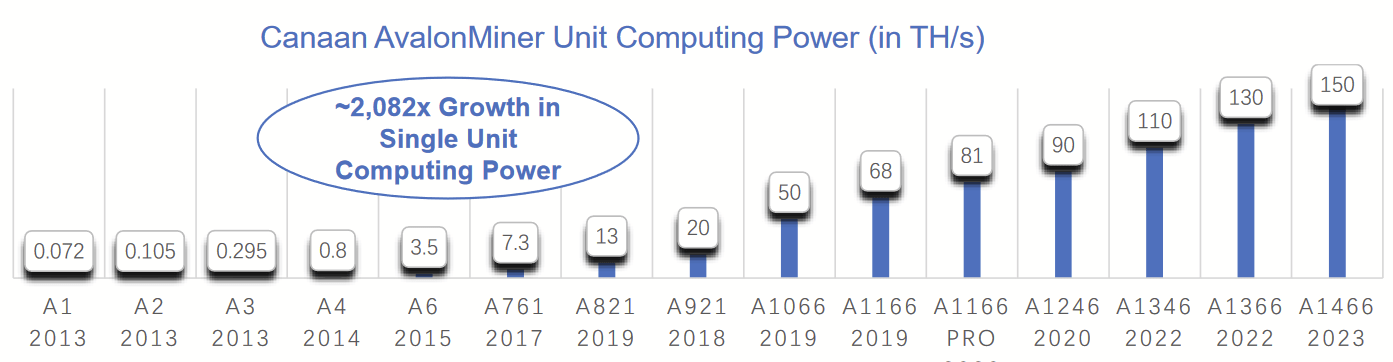

Canaan is a Chinese company that develops the hardware for miners and sells to kind of companies I just mentioned. It also has a minor mining segment of its own, but most revenue comes from the first segment.

February 2023 Company Presentation

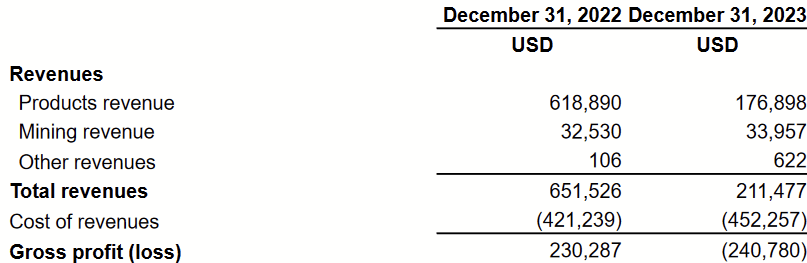

Recent financial results show that it struggles to make even a gross profit.

Company's Press Release

It also issued preferred shares that come with heavy dividends. These will compete heavily with returns to owners of the common going forward. Further dilution through preferred or common equity is a major risk with this company too.

MicroStrategy Incorporated (MSTR) is one of the better holdings purely for the reason that it generates free cash flow and has virtually no debt. Their main business? They buy and hold BTC, while also providing BTC-related software and services.

microstrategy.com

While MicroStrategy is profitable, they undertake heavy share dilution through stock-based compensation and capital raises.

2023 Form 10K

From 2021 to 2023, SBC exceed even cash flows from operating activities. While most of the capital raises can be explained by its use to acquire BTC (Purchases of digital assets), the main issue there is whether or not BTC will appreciate attractively to justify the amount of dilution. As a non-productive asset and something that was invented to function as a (stable) currency at some point, one has to wonder if that will occur.

Beyond that, shares currently trade at a P/E ratio of over 1,000, which, I think, is pricey for even a good company that we simply assume is getting good value for its BTC.

Coinbase Global, Inc. (COIN) strikes me as probably the best business of the bunch. It is a crypto exchange, and it's not exclusive to BTC transactions.

Cash Flow History (Seeking Alpha)

It enjoys high cash flow from operations most years, with outflow from capex. More shares repurchased than issued now. It currently has about $3 billion in LT debt and also trades at a high P/E of about 50!

Galaxy Digital Holdings Ltd. (GLXY:CA) does a bit of everything: trading services, asset management, mining, and own investments in crypto. Its revenues are diversified across its many segments. Seems to have positive cash flows from operations, with its diverse income sources.

Q3 2023 Company Presentation

Its financial results are somewhat mixed and hard to summarize as it is still developing its varied segments. While it's not an outright problem, I still want to see more good in this fund, considering the weaker elements of its holdings.

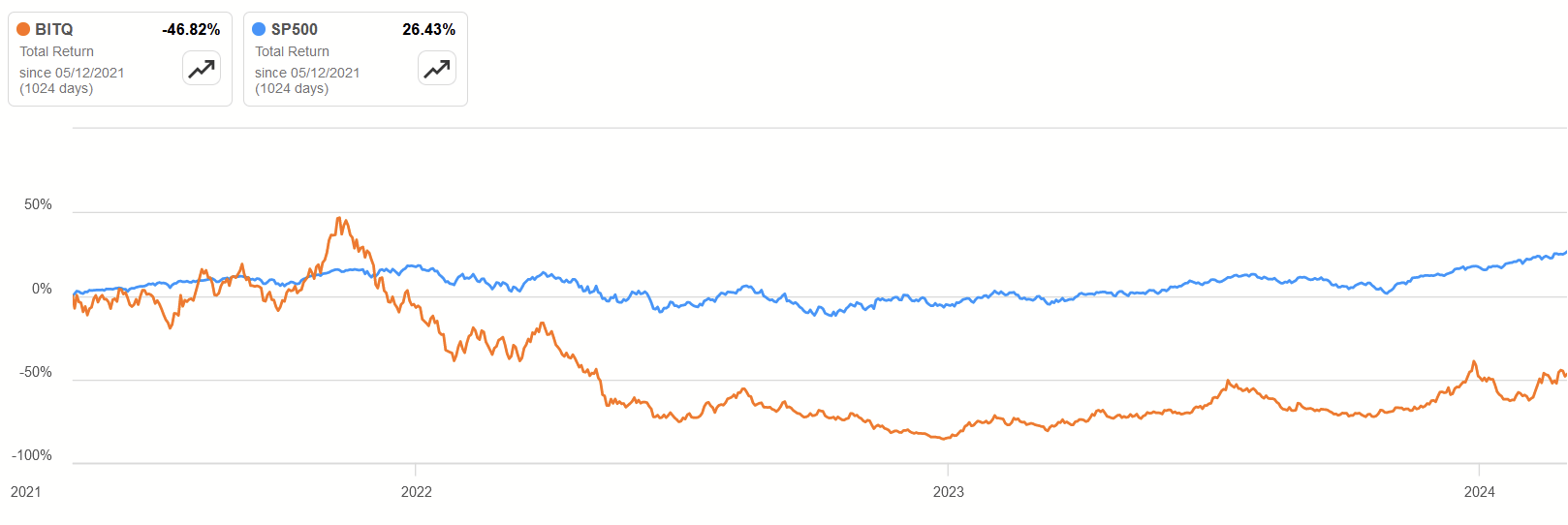

If the fund is to be a good long-term investment, there needs to be something that will contribute to positive, long-term returns. With businesses that primarily lose money and that need to dilute ownership to stay afloat, the impact so far has been negative returns.

Total Returns since Inception (Seeking Alpha)

It's not clear what exactly will be a catalyst to this. For the mining companies specifically, BTC would need to appreciate to a price that makes their miners economical to purchase and run, and it would likely have to be many times higher than the current price for some valuations of these portfolio companies to make sense.

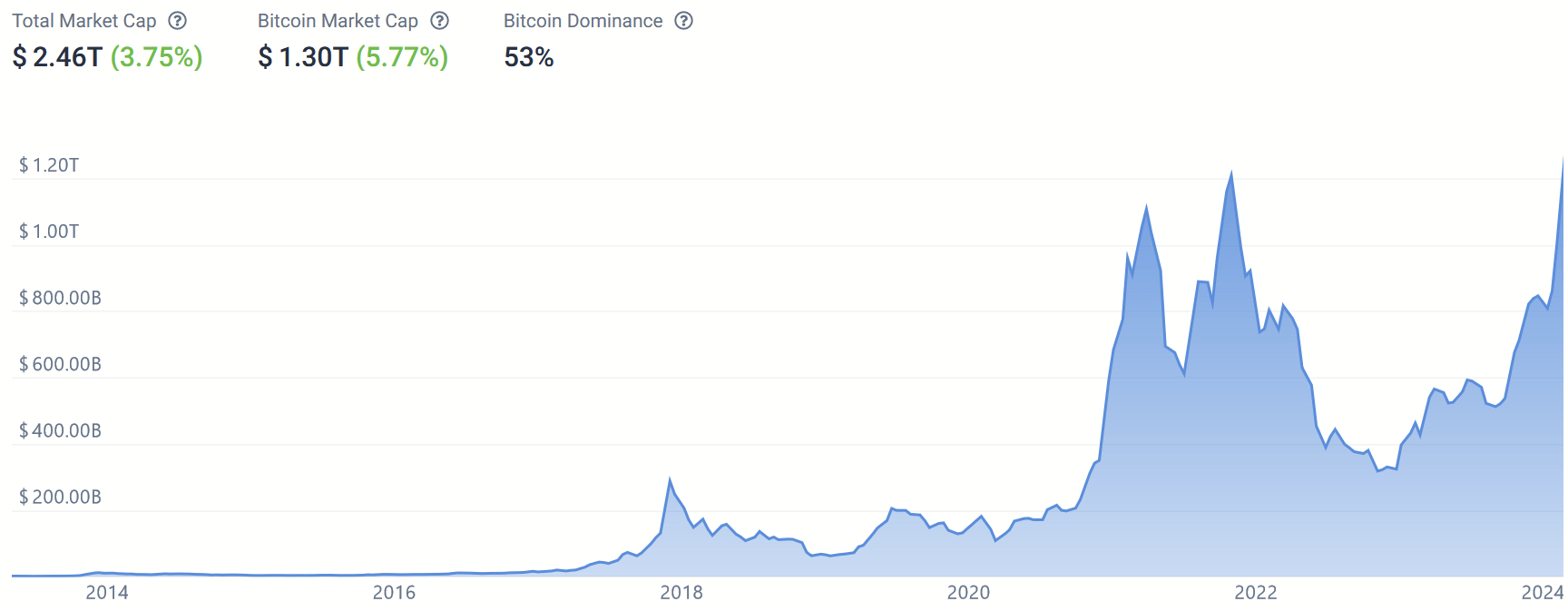

I have seen arguments that halving events have resulted in higher valuations of BTC. I would caution folks to be more skeptical of that argument going forward, considering the kind of market cap BTC has today, versus during past halvings.

BTC Market Cap History (coincodex.com)

The last halving was in May 2020. We can see the spike in activity that followed that. BTC is now valued like a mega cap over $1 trillion. It's much easier for a market cap to rise when the valuation of an asset is small. Capital entering that market will have an easier time raising that valuation. A substantial amount would have to enter BTC to raise its value sufficiently. Barring that, halving poses a major risk of hurting the mining companies' return on their miners. This isn't just true of the upcoming halving event but over time.

Coinbase seems to be the most versatile since it can make money from transactions involving other cryptocurrencies. Even then, disappointing results from the performance of BTC could lead to shrinking interest, a decline in transactions, and thus a loss of fees for the company. Other cryptocurrencies may not pick up that slack either. Is it really worth paying a high P/E ratio for such a possibility?

There are two fads in the investing world right now: crypto and ETFs. With a fund based on an Index they made themselves, Bitwise seems to be responding to consumer demand by providing a desired product. There is no filter for profitability or strong fundamentals here. Consequently, I believe the fund will continue to have the negative returns that it has had, and if that's what the people want, it's not surprising the fund was launched.

Investors should appreciate the likely dynamic at play and should understand what BITQ is. It is exposure to crypto and multiple business models, but they are ones that, by and large, don't make money and give no hint of doing so in the future. I wouldn't want to put my hard-earned money into such a fund. Consequently, BITQ is a textbook SELL for me, and it probably always will be.