Ethan Swope

Ethan Swope

Our analysis focuses on Birkenstock, a well-known footwear brand in the consumer discretionary sector. Birkenstock was listed on the New York Stock Exchange (NYSE) on October 11, 2023. The company reported its first earnings while being a listed company on Jan 18, 2024, with mixed results. While the company was able to increase revenue by 20% yoy, the company announced that it is facing some margin pressure as a result of "inflationary costs". Furthermore, unit growth was only 6% (our calculation shows it was more 5.5%), while the remaining 14% is attributable to ASP growth (driven by price increases and shift in channel mix towards DTC).

While we believe BIRK is a strong brand, we are mainly concerned about the current valuation levels and the implied growth expectations, as well as several concerns in the IPO prospectus, which mainly come being a Private Equity owned company. We are discussing these "concerns" in more detail below.

The main issue with Birkenstock is that 90% of the stocks are owned by LCatterton (PE Fund), the previous owner and its advisors, resulting in the free float being relatively small at 10% and subsequently the liquidity of the stock. The average daily trading volume is only 750k shares, assuming "free float" consists of around 20m shares (details below) only 3.8% of free float is traded on a daily basis. As a result, the current share price is potentially not reflecting the fair valuation, from our point of view, so while we might be right with our recommendation it might take some time until this is reflected in the current share price.

There are several factors which are supporting our bearish view and for this we need to go back a few years and dig into the IPO prospectus.

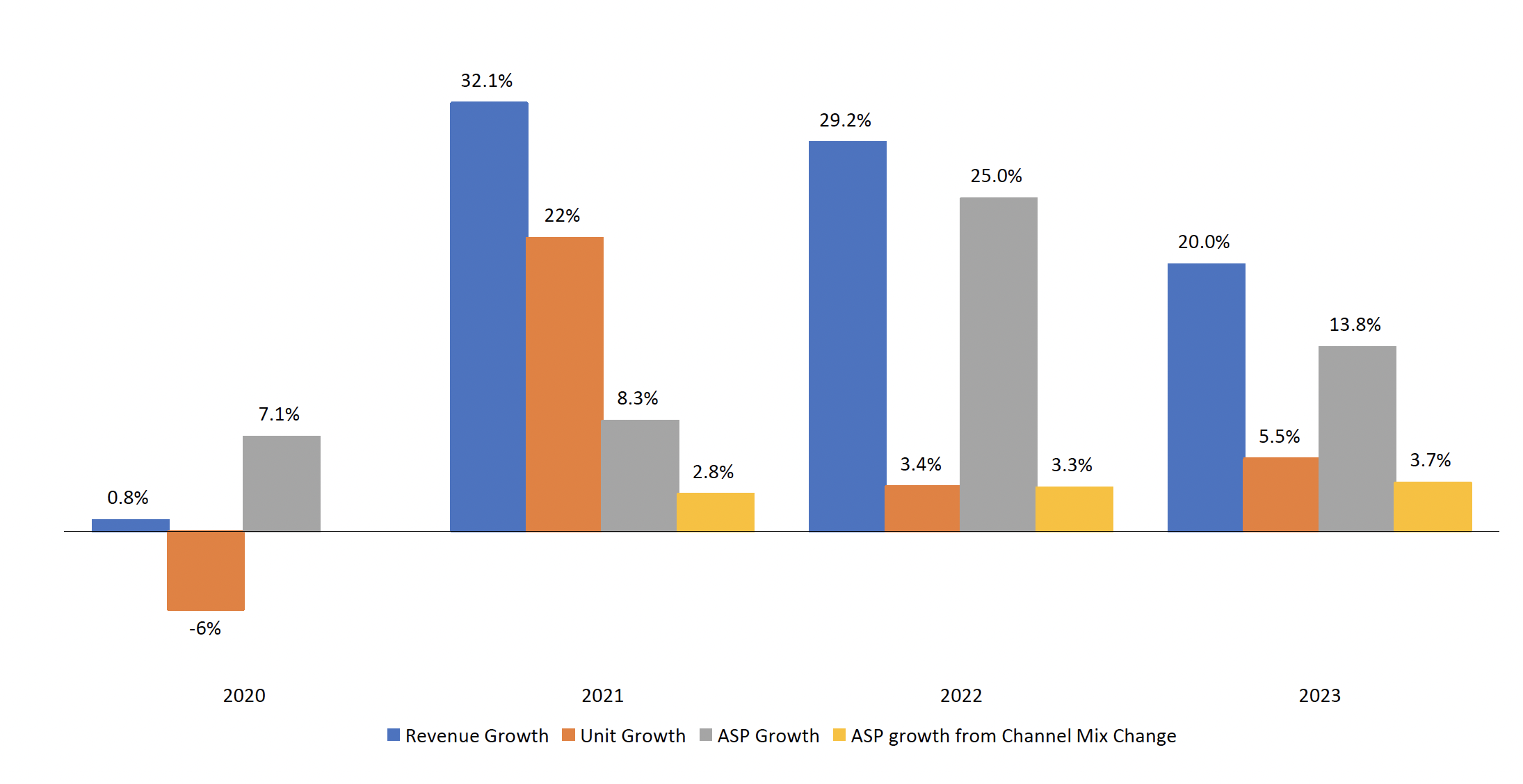

In 2021, Birkenstock experienced a significant revenue increase of 32%, driven by a 22% growth in unit sales. This indicates a strong market response in the post-lockdown period. The surge in sales post-pandemic can largely be attributed to the global shift towards remote work, leading to a change in consumer preferences for comfortable footwear like sandals. Interestingly, in 2022, the company's unit growth was only a 3%, yet revenue grew by 29%. This suggests that the growth was primarily price-driven and influenced by changes in the channel mix, rather than selling a lot more "sandals". While for FY2023 the company reported higher unit growth is still only 5.5% yoy, which raises concerns about the sustainability of Birkenstock's long-term growth potential. With product demand appearing to kind of stagnate, further price increases might not be well-received by consumers going forward. In the below chart we tried to decompose the last 3 years growth of Birkenstock. While we had to triangulate some numbers and come up with a few assumptions (for instance average RRP for wholesale and DTC), we believe these numbers are pretty much on point.

Revenue, ASP and Unit Growth decomposition (Birkenstock, own assumptions)

The key findings are:

We analysed the price development of Birkenstock's bestsellers using Wayback Machine and found out that the main price increases actually happened from 2021 to 2022, in line with what was reported in the IPO prospectus and what we also see in the chart above. Please note: Around 70% of sales in FY2022 were generated from Birkenstock's five core models, according to Fitch's report. Hence, conducting a quick price development for these 5 models is quite straight forward. The average price increase according to our analysis was staggering 15% in 2022. We haven't been able to see any major price increase in 2023. Based on this, Birkenstock's units' sales in their DTC channel is around 7 million in FY2023 or 23% of total unit sales, an indication that B2B with 23.7 million units is still very relevant. Based on the calculation above and discussions with select wholesalers, we also understand that the average markup for wholesale/ distributors partners dropped to 2.3x in 2023 vs 2.6x in 2021. This could be the result of both, cutting out distributors and/or increasing prices for wholesale partners. No matter what the reasons were, this should have given the company a major gross profit margin boost.

Based on our assumptions, the absolute unit growth in the last 2 years was mainly coming from DTC, while B2B (wholesale/distribution) was more or less flat. While we understand that this is Birkenstock's management's objective and resonates with the partial owner's strategy, LVMH, we see this as a potential risk. The advantages of wholesale, which is currently still estimated to contribute 3/4th of unit sales, are that wholesale partners typically underwrite part of the purchase orders. Which means wholesale/distribution partners commit to buy a certain amount of product upfront and hence a large part of the financial risks transfer from the manufacturer to the wholesaler, given that Birkenstock is assured of the sale before production begins. So, while DTC promises a lot higher profit margins, it comes with a much higher financial and inventory risk. Given Birkenstock didn't really grow its unit sales significantly in the last 2 years, there is a risk that the company might face some inventory issues in the near future (inventory levels are discussed below).

Product assortment expansion, as the main objective of the Birkenstock management team, seems to be a natural step for future growth. However, we see this as one other risk for the company. While the management team announced it will mainly stay within the footwear space, the reality is that the company was mainly focused on different silhouettes of sandals for the last 249 years. Most probably for a good reason. The deviation from the sandals and expansion into boots and potentially even apparel is a risky move and we are pessimistic this new categories are adding additional top-line growth, but instead resulting in higher slow-moving inventory. Many consumer companies tried to expand from their "bread and butter" business into new categories, unfortunately with limited success. Examples are: Under Armour (UAA) expanding into footwear, Allbirds (BIRD) expanding into apparel, Dr Martens (OTCPK:DOCMF) expanding into sandals and shoes (from boots).

Our overall conclusions are that unit sales in the last 2 years are rather disappointing and we don't see how Birkenstock is going deliver against the high growth expectations embedded in today's share price.

One SeekingAlpha member mentioned in a comment that "A 249 year old company doesn't need adjusted EBITDA" and we totally agree. We assume these are learnings from the majority owner, LCatterton, evidently beginning to "enhance the company's appeal" prior to the IPO.

It's a bit like navigating a jungle when going through the IPO prospectus and the annual report of Birkenstock trying to understand what was actually adjusted and why. The main objective of "adjusting" reported numbers should be to understand the real operating performance of a company, however, in Birkenstock's case it might be a bit confusing for investors. Anyhow, there are four major buckets of adjustments for Birkenstock:

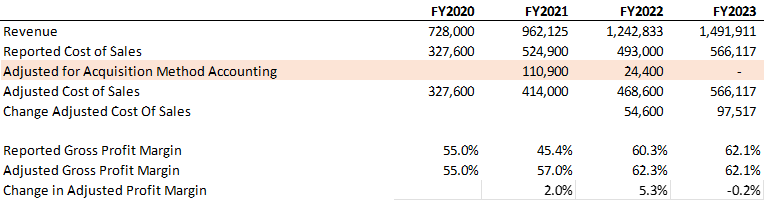

We need to go back to the IPO prospectus to understand the significant boost of Gross margins in 2022 and determine if there is a risk of this being sustainable. Birkenstock used the "acquisition method" to revalue the inventory. This happened when LCatterton acquired the company in 2021. On page 101 of the IPO prospectus the revaluation of inventory and the impact on CoS is explained in great detail. The CoS adjustments in FY2021 and FY2022 were EUR 110.9 million and EUR 24.4 million respectively. Which means, the inventory was revalued down by the same amount and retrospectively expensed in the respective fiscal years. Hence the "adjusted' Cost of Sales is showing a higher margin as compared to the reported one (see table).

Birkenstock - Cost of Sales and Gross Profit (Birkenstock)

It is mentioned in the IPO prospectus that for FY2022 "Excluding the effects of applying the acquisition method of accounting for the Transaction, cost of sales increased by €54.6 million, or 13%. The increase was primarily due to 3% growth in the number of units sold and €25.0 million of higher personnel costs. Higher personnel costs were driven by a higher overall level of full-time production workforce, replacing certain temporary workers, as well as wage and salary increases. Additionally, prices for certain core input materials increased on average by a high single-digit percentage in fiscal 2022, including EVA granulate, sole sheets, folding boxes and leather."

So why is this important? We want to understand if Birkenstock has further room to increase margins or if there is a potential risk the company is going to face some margin pressure going forward. For this we decomposed the increase of "adjusted" Gross Profit margin as shown in the table above, i.e. 2 percentage point in FY2021, 5.3 percentage points in FY2022 and -0.2 percentage points in FY2023.

We have discussed that Birkenstock's actual price increase in FY2022 was around 15%. Based on this, the Gross Profit margin should have increased to 62.6%, ceteris paribus. Given the shift to DTC from 34% in FY2021 to 38% in FY2022, we should have expected to see a Gross Profit margin uplift of additional 1.3 percentage points to 63.9%, again all else equal. We cannot adjust for the shift in product mix, so we implicitly assume the margins across all styles are the same. As a result of the above, we need to assume that Birkenstock was already facing an increase of product costs (independent of any adjustments) in FY2022 resulting in 2.4 percentage points of margin loss. Running the same logic for FY2023 we derive at a theoretical Gross Profit margin of 66.4% vs the reported "adjusted" Gross Profit margin of 62.1%, again a 4.3% percentage points eaten by cost erosion.

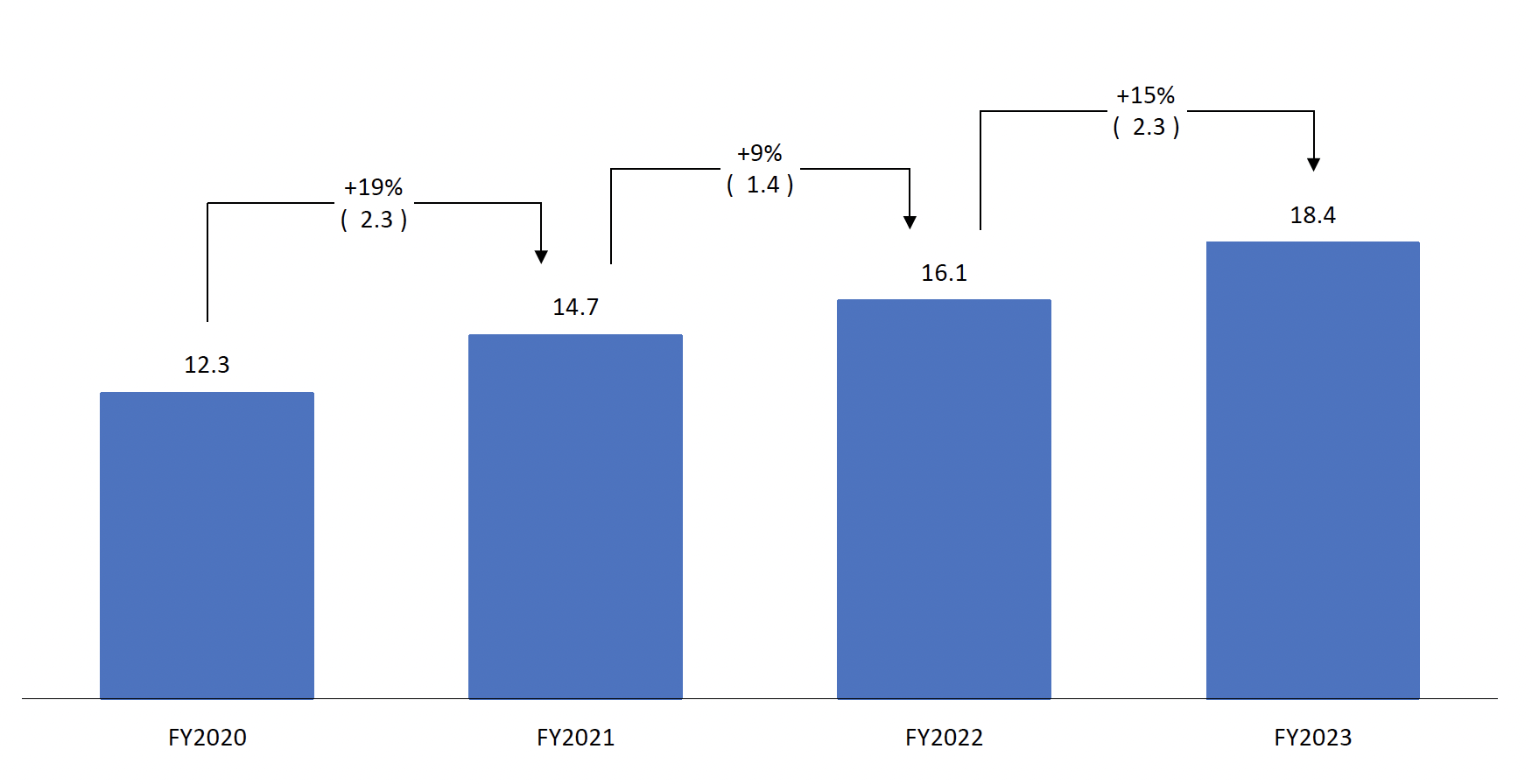

A simple calculation of the number of products sold divided by "adjusted" Cost of Sales shows a similar pattern (see graph below). We don't see any one-off items included in the Cost of Sales numbers, so there is no need for any adjustments. Another way to look at it is: Cost of sales grew by 14.8% in FY2023 vs a 5.5% unit growth, which is another indicator of a significant cost increase. Please note: Part of the increase of Cost of Sales can also come from shift to more premium higher prices items.

Birkenstock Cost of Sales per Unit (Birkenstock and own analysis)

Our conclusion is that Birkenstock is facing margin pressure and was only able to show increasing/flat Gross profit margins in the last 2 years as a result of price increases and the channel mix shift towards DTC. We don't believe Birkenstock has a lot more room for price increases in 2024 and hence there is no further room to further expand margins or even a potential risk of a margin decline.

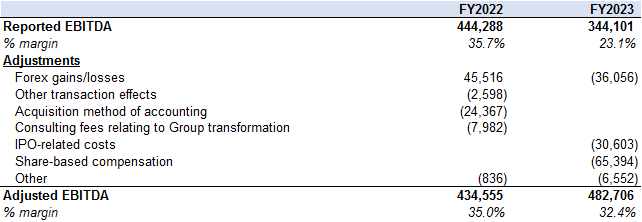

The "unadjusted EBITDA" or "reported EBITDA" for FY2023 depending on what you want to call it, actually declined. You can argue that movements of exchange rates should be adjusted to get the real operating performance and hence obtain the health of a company. However, the company also adjusted share-based compensation of EUR 65.4 million, which could be considered operating, as it's just another way of retaining talent. The interesting part of the share-based compensation is that it was entered into on March 2023 with the a 4 year vesting period.

However, the agreement also states that "If an exit event of the Company, which is defined as initial public offering or sale, takes place during the vesting period, the entire award is immediately fully vested". The IPO happened in October 2023 and it must have been pretty clear to everyone in March 2023 that this accelerated vesting clause is going to be triggered. We see this as a red-flag, where major costs to retain people in the short-term are moved to post-IPO accounts. A typical move done by a PE-owned company. Having said the above, we also consider this as a one-off item in our further analysis, even though we don't understand how Birkenstock incentivises these managers going forward.

Here are the various adjustments for FY2022 and FY2023 according to the FY2023 annual report:

Birkenstock: Reported and Adjusted EBITDA (Birkenstock)

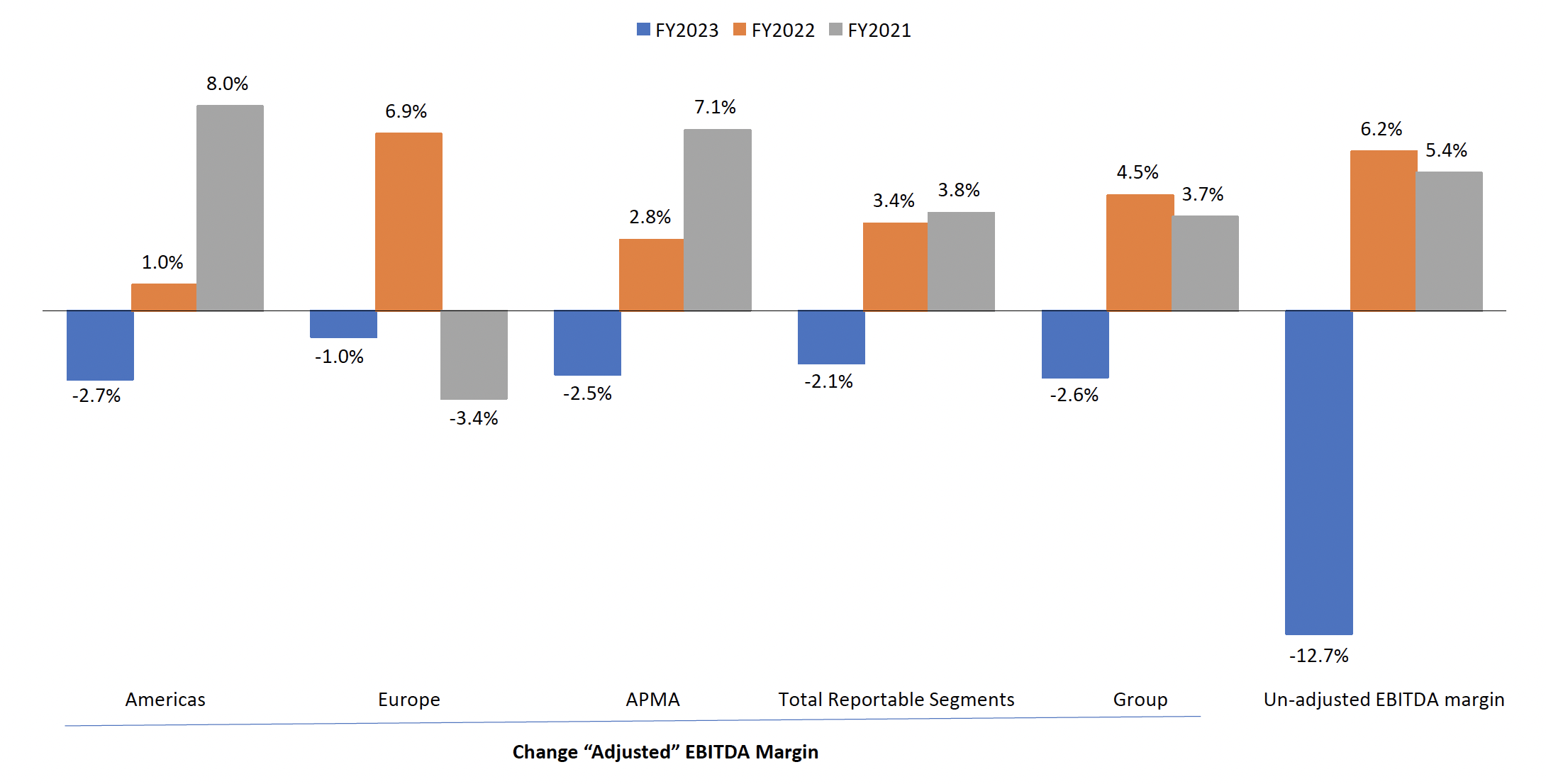

Independent of this the EBITDA margin in each reported geography dropped between 1 and 2.7 percentage points in FY 2023, which again might be a sign of an overall weakening of operating profits beyond the reported increase of "inflationary costs", in-line with our Gross Profit decline comments above.

Change of EBITDA breakdown by Geography (Birkenstock)

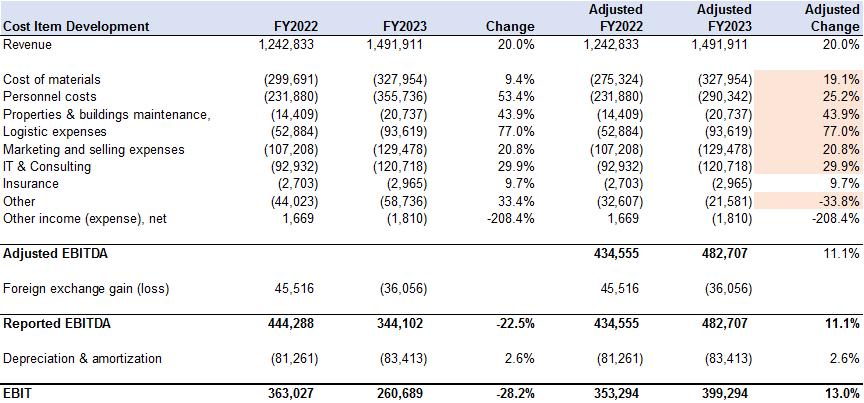

On top we looked at the cost breakdown and it's obvious that Birkenstock has seen a significant increase across the board. We adjusted the respective cost items with the reported "one-off costs" allocating it to CoS (EUR 24.3m from acquisition accounting in FY2022), personal costs (EUR 65.4m from share-based compensation in FY2023) and the remaining EUR 11.4m and EUR 37.2 million IPO and restructuring related cost to FY2022's and FY2023's Other cost line item, respectively. Please note, besides the share-based compensation, we don't know if our allocation is fully reflecting the reality, however, it won't change our conclusions, even if we are slightly wrong.

Development of (adjusted) Cost item breakdown (Birkenstock and own assumptions)

The table above shows that almost all cost items grew a lot more than the 5.5% unit growth and either the company is facing significant cost control issues or it is investing in massive future growth (also see next chapter). Both factors make us believe that the company will have a difficult time to maintain its EBITDA margin above the 30% target level going forward.

We cannot get our head around the fact that the management team stated in the last earnings call that they "continue to see strong consumer demand" and their strategy is to "balance demand and supply to create scarcity in the market" with the company's high inventory levels. The table below illustrates the development of inventories over the last 4 years.

Birkenstock: Inventories last 4 years (Birkenstock)

We used the average CoS per unit for each year to calculate the number of units, which might not be totally correct. However, even if we are not fully on point, it just makes the situation worse. The results are that Birkenstock has more than a full year of sales of stock in their warehouses, resulting in a stock-turn of 0.95x per annum; a number which is quite scary for the industry.

So why is the company, despite seeing "strong demand" holding back in selling more of the existing stock? Either the demand is actually not as high, the current stock is not the right one, or the management's strategy is to create artificial scarcity. The last one would be an odd one, given that unit sales was only 5.5% last FY. Also, the warehouse costs alone will be in the millions for holding so much stock.

These findings are another indication for us that the company is not experiencing any issues on the supply side, but the demand might not be as strong for the brand anymore. Also have in mind that Birkenstock just finished a new production facility with 36,000-square-meter in Pacewalk for EUR 120 million. Maybe the management team should focus on selling its existing inventory down to a normal level first before producing more stock.

The company has a total net debt of EUR 1.5bn resulting in Net Debt/EBITDA ratio of 3.1x, which is considered relatively high for a company in the Discretionary Consumer sector and only possible as part of the loans are linked to the previous owners and hence there are no covenants, according to the IPO prospectus. Birkenstock entered into a Vendor Loan agreement with AB-Beteiligungs GmbH for an amount of €275.0 million (see IPO Prospectus F-52). The loan is scheduled to mature on October 31, 2029 and bears interest of 4.37% per annum. AB-Beteiligungs GmbH is an entity controlled by Alexander Birkenstock.

Interest expenses in FY2023 were EUR 117.6 million which results in EBITDA interest coverage of 4.1x (using "adjusted" EBITDA) and 2.9x using the "unadjusted" EBITDA. Also note, Fitch is rating Birkenstock at BB in its latest report.

Having said this, nothing can go wrong given the company is leveraged up to the roof right now, something you would expect given the company was acquired by a Private Equity company before the IPO.

While we don't see any major risks on this front for now, it's important to keep an eye on the debt burden going forward.

Beyond the question marks regarding where future profitable growth should come from, there are a few other interesting aspect in the company's IPO prospectus that might have been overlooked by some. This is in particular interesting as it is concerning the shift of future value creation to pre-IPO shareholders, leaving new shareholders left holding the bag.

First, the IPO prospectus reveals a few complex elements related to Birkenstock's IPO, including the roles of MidCo, ManCo, the Underwriters, and a so called Tax Receivable Agreement (TLA). Let's break these down for clarity:

MidCo owns approximately 82.8% of Birkenstock's ordinary shares (or 80.2% if underwriters exercise their option to purchase additional shares). This makes Birkenstock a "controlled company" under NYSE rules and hence the company can elect not to comply with certain NYSE corporate governance requirements.

ManCo is a management ownership vehicle holding an interest in MidCo. It allowed senior management to acquire an indirect ownership interest in Birkenstock pre-IPO. Upon a qualifying event, in this case a successful IPO, partnership interests in ManCo can be converted into ordinary shares of Birkenstock. It looks like the shares are already created and hence will not dilute new shareholders.

The Underwriters, namely Goldman Sachs, Morgan Stanley, JPM and others, have been allocated a total of 32,258,064 ordinary shares for the initial offering. The underwriting discount was $1.955 per share ($63 million in total). This amount is deducted from the initial public offering price per share and represents the fee earned by the underwriters for their services. On top the underwriters have an option to purchase up to an additional 4,838,709 shares from the selling shareholder (MidCo) to cover over-allotments, which was probably 100% exercised. The proceeds from these shares will go to MidCo and not Birkenstock. On top, the underwriters issued a Directed Share Program where 8% of the shares handled by them are reserved for sale to company employees, directors, business associates, or other individuals closely associated with the company,. I guess this also includes management of the underwriters. We need to assume these 8% or 2.6 million shares have been allocated. These shares are considered "reserved shares" and hence are subject to a 180 days lock-up period. So let's have April 8th 2024 in mind. So the total "free float" or better "not reserved shares" are around 34m. A large part of these shares will be in the hands of institutional investors.

Secondly, Financière Agache (majority owned by the Arnault family) and Durable Capital Partners LP and Norges Bank Investment Management (the cornerstone investors of the IPO) have indicated to purchase around 13.5m shares of Birkenstock (see IPO Prospectus page 1 Footnote). Financière Agache was also a shareholder in MidCo before the IPO. Arnault and LVMH own a 40% stake in private equity firm LCatterton, just FYI.

Lastly and more interesting is the Tax Receivable Agreement (TRA) with pre-IPO shareholders. Birkenstock was transitioned to become a Jersey public limited company on October 4, 2023, ostensibly for leveraging Jersey's 0% corporate tax rate. While this move ostensibly positions the company for enhanced profitability and cash flow generation, the structuring of the TRA suggests a skewed benefit distribution: Under the TRA, MidCo and hence pre-IPO owners, including LCatterton, the management team, and the Birkenstock family (via MidCo), are entitled to 85% of the future tax savings. The prospectus indicates potential tax savings of up to $500 million over the next 13 years, a substantial amount that will predominantly benefit pre-IPO stakeholders and hence new public shareholders are at a distinct disadvantage. So the reported effective tax rate, doesn't really matter for valuing Birkenstock.

While the previous points do not really affect Birkenstock's fundamental health, it's important to understand the dynamics of dealing with a listed private equity-owned business. In this case, the majority owner, LCatterton, clearly prioritises the interests of its Limited Partners and of course the General Partner (which is 40% LVMH).

To make a short story even longer and the most concerning part is how LCatterton is liquidating its shares? I am confident, there will be no trade buyer at the current valuation. The PE firm has already made a around 0.7 dpi (Distributed to Paid-In Capital, a term used to measure the total capital that a PE fund has returned to its investors) on this investment (after only 2 years), as they leveraged the company to the roof (EUR 1.9bn) and got around EUR 1bn from the IPO proceeds. So even a share price of $20 and a hypothetical exit in 2024 would result in an MOIC of 1.8x, an IRR of 45% and most importantly a USD 500 million carry pool (to be distributed to the GP).

This theory might be a bit too much, but we wouldn't be surprised if Groupe Arnault at one point acquires 100% of Birkenstock - assuming the share price of Birkenstock declines to $20 levels - takes the company private in the next 3 years. Arnault already directly and indirectly owns 35% of BIRK via LCatterton anyhow. Win-win for LCatterton and Groupo Arnault, while other shareholders are left in the cold.

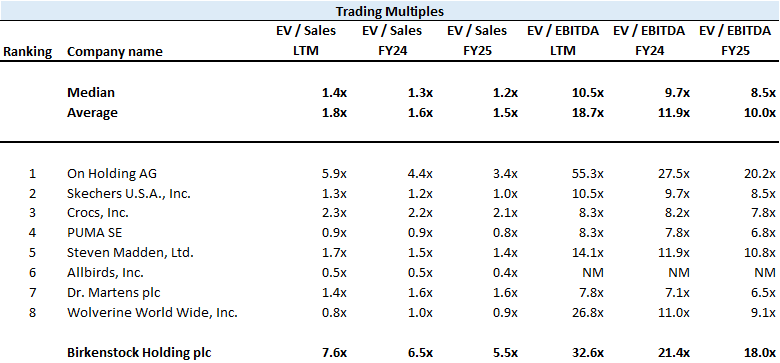

As mentioned above, Birkenstock is trading at massive premium compared to its peers. Current valuation multiples of Birkenstock are 6.5x NTM EV/Sales and 21.4x NTM EV/EBITDA respectively, compared to its peers average of 1.6x NTM EV/Sales and 11.9x NTM EV/EBITDA.

Peer Group Multiples Birkenstock (S&P Capital IQ)

To understand what these high multiples actually mean in terms of future expectation, we ran a simple 3-stage DCF model to understand the implied growth expectations. The first stage incorporates 2-3 years of consensus broker estimates, assuming brokers possess the most accurate short-term projections for the company. The next stage involves a 10-year forecasting period, maintaining consistency in major drivers such as margins and capital expenditures, and concluding with the terminal value calculated using the value driver formula (Enterprise Value = NOPAT x (1-G/ROIC)/(WACC-g). We kept EBITDA Margin constant at 30%, Capex fixed relative to sales at 5% (average last 3 years was 6.8%), WC we linearly reduced to 25% over the next years from 41% in FY2023, assuming the management team gets this part right. ROIC is an outcome and grows from 8% in 2023 to 41% in 2035.

The model suggests that to justify its current valuation, Birkenstock needs to achieve an annual top-line growth of 17.7% for the next decade plus (2024-2035), aiming for a revenue of EUR 10.8 billion by 2035. FYI, consensus broker estimates suggest a top-line CAGR of 19.7% till 2025, so the company needs to deliver similar growth for another 10 years till 2035.

The projected top-line growth suggests that the company must aim to boost its sales to approximately 200 million units by 2035, a substantial jump from the current figure of 30 million units in FY2023. The modest 5.5% increase in unit sales in FY 2023 does little to give us the confidence in the Birkenstock's ability to meet these ambitious targets.

Birkenstock stands at a critical juncture in its 249-year legacy. Known for its heritage of comfortable sandals, our analysis presents a cautious outlook on Birkenstock's future, particularly given the high implied growth expectations. The current enterprise value of EUR 11.3 billion suggests an ambitious annual growth rate of 17.7% over the next 10 years. In light of low or stagnant unit sales growth, limited pricing flexibility, and rising costs, these growth expectations seem overly optimistic. Furthermore, the substantial inventory levels, currently at 40% of revenue with a stock turnover of <1, are raising concerns about potential overstocking and/or inefficiencies in working capital management. Additionally, the pre-IPO ownership structure and arrangements, with LCatterton still retaining more than 80% ownership, indicate some conflict of interest and a potential share overhang once the lock-up period ends in April.

Given the challenges described above, the high expectations embedded in Birkenstock's current share price seem totally detached from the company's real operating performance. We hold a very bearish outlook for the stock.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.