helloabc

helloabc

Bilibili Inc. (NASDAQ:BILI) released its fourth-quarter earnings report on Thursday. It beat its top-line estimates by $4.29 million. However, Bilibili missed out on its bottom-line target by four cents per share. Although Bilibili traded down in after hours, its stock rose sharply on Friday, sending mixed signals.

Bilibili stock's consequent reaction shows that investors have mixed feelings about its bottom line. As such, we decided to examine the firm's prospects to identify whether improved profit margins are likely before Bilibili's next earnings release.

Here are our latest findings on Bilibili.

Bilibili, often referred to as China's YouTube, generated $894.3 million in Q4 revenues, a 3% year-over-year increase. The increase is moderate for its standards but consideration must be given to a slower overall economic environment in China.

Let's look at Bilibili's segmental performance and our outlook on each for additional context.

Bilibili's advertising revenue reached $271.7 million in Q4, a 27% year-over-year increase.

We think Bilibili's advertising segment will hold strong, as the trend for shorter-duration video demand has yet to reach its apex (people are moving from movies and series to short clips such as those provided by Bilibili). Furthermore, Bilibili uses its advertising for sales conversion, meaning the segment adds to synergies and doesn't merely function as a financial asset to the company.

Challenges do exist for Bilibili's advertising segment. For example, driving traffic requires a best-in-class ad algorithm, which is a fluid phenomenon. In addition, rising competition in the content creator intermediary space can pose problems.

Bilibili's mobile games segment suffered a knock in its Q4. The segment achieved $141.8 million, a 12% year-on-year decrease, driven by underwhelming results from its newly released Space Hunter 3.

Although Bilibili states that its flagship games, such as Azur Lane and FGO, remain stable, we have concerns. For example, a top-down view shows that China's mobile gaming industry has a projected CAGR of 5.8% until 2027, which is quite low for a tech-based endeavor. Moreover, mobile gaming can be very trend-like, meaning lumpy revenue can be a continuous phenomenon, adding volatility to Bilibili's stock price.

Bilibili's mobile gaming segment spans about 15.8% of its revenue mix. Some might say the segment is complementary to its business model, but we think it creates an overhang.

Value-added services added $402.4 million in Q4 revenue, a 22% year-on-year increase, driven by live broadcasting.

We think this segment is set to boom in the coming years due to the reasons mentioned in the advertising segment. Moreover, the segment is placed to up-sell its viewer base into a subscription-based model, allowing for enhanced revenue and better content (via paid programs).

Bilibili's value-added services segment has around 20.5 million premium subscribers, 80% of whom are on annual auto-renewal agreements (note that this was measured back in June 2023). This division definitely has more to offer.

Lastly, let's have a look at Bilibili's E-Commerce, aka IP Derivatives.

Bilibili's e-commerce segment generated $307.7 million in Q4 revenue, a 29% year-on-year slump. The decline was primarily due to e-sports copyright licensing and segment sales.

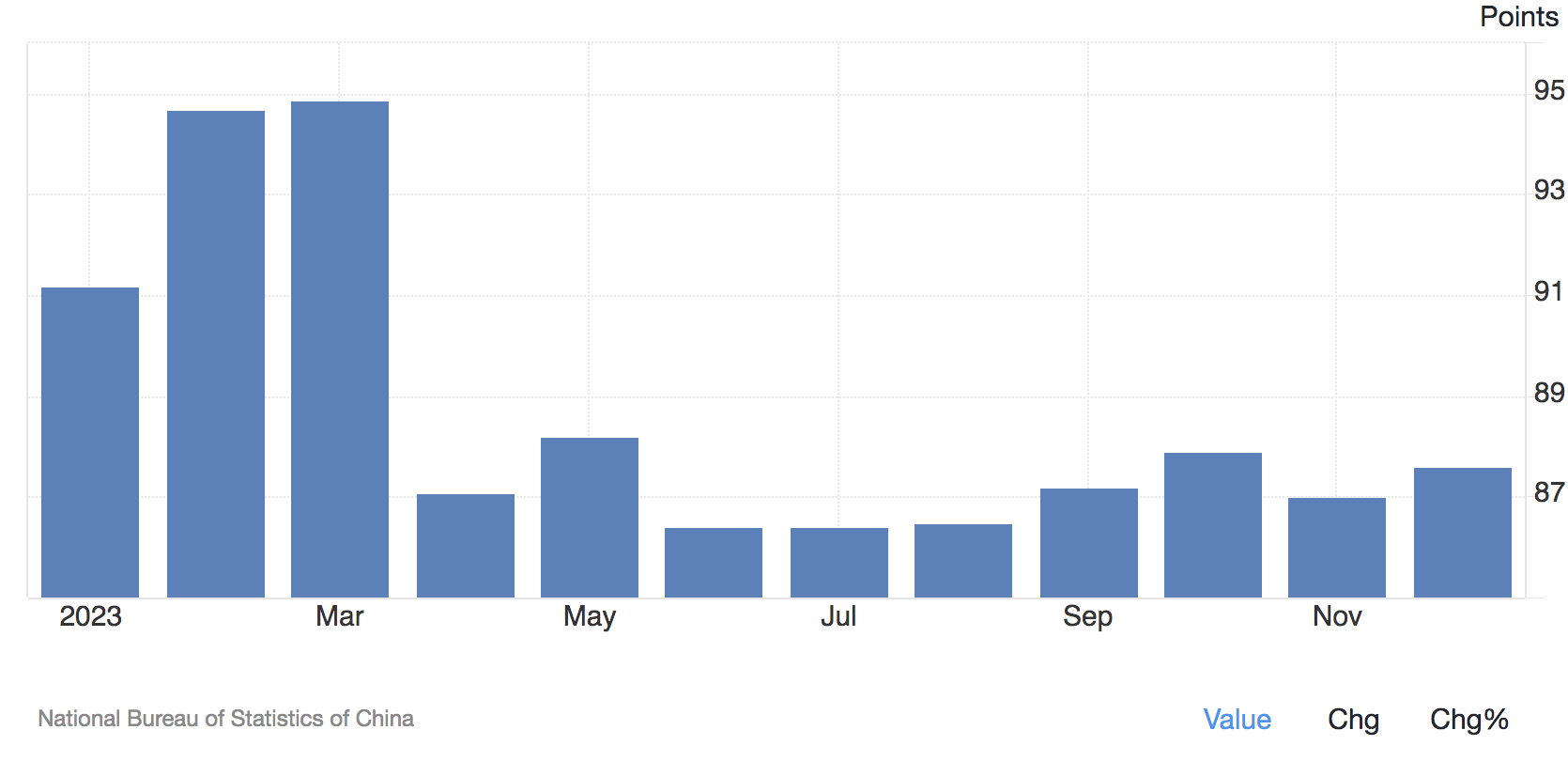

We can't speak for content licensing, as it's an esoteric concept. However, headline sales were likely driven lower by China's flimsy economic climate. China's consumer confidence remains relatively low; therefore, we think e-commerce will struggle to pick up anytime soon.

China Consumer Confidence (Trading Economics)

Why wouldn't consumer confidence affect Bilibili's other segments? Truth be told, it can, but it seems like the organic growth in advertising and value-added services is pent-up due to a significant increase in traffic due to the popularity of Bilibili's business model. Thus, economic headwinds aren't enough to drive those segments into negative growth.

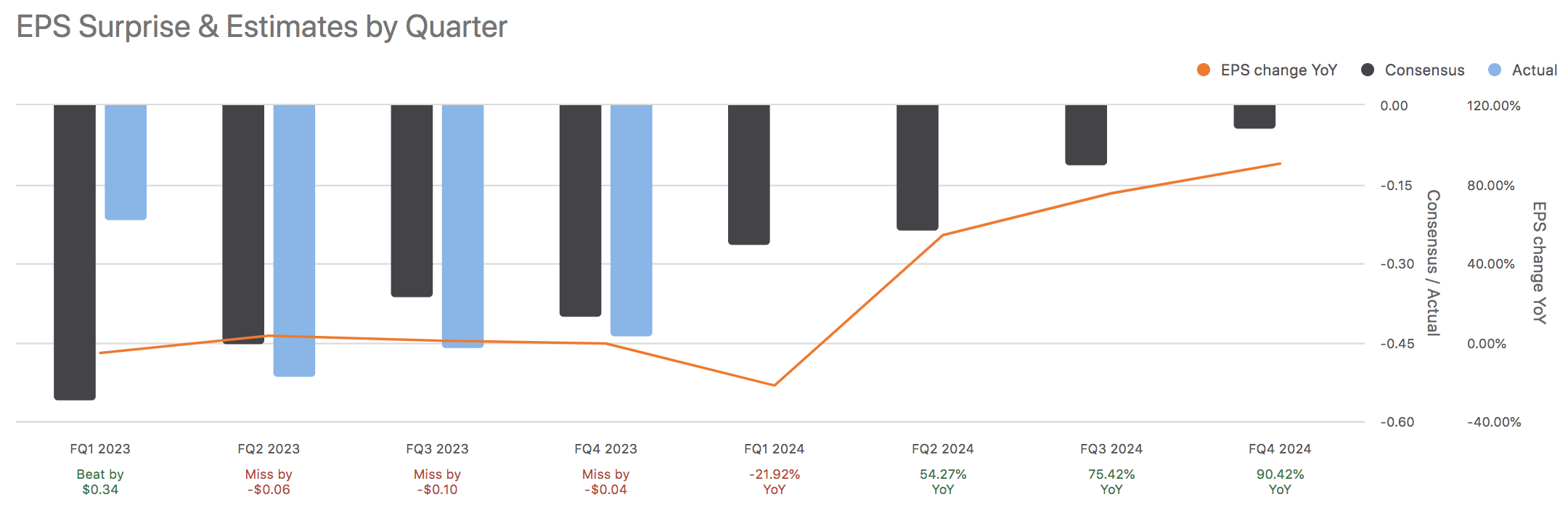

As illustrated by the diagram below, which I pulled from Seeking Alpha's database, Bilibili has a history of missing out on its bottom line. Although a superficial observation, academic research has proven that earnings momentum is critical for a stock to achieve long-term performance. As such, we highlight Bilibili's earnings history as a critical risk factor.

Seeking Alpha

I decided to point out Bilibili's price-to-sales ratio as it is an early-stage growth company, meaning a ballpark valuation is best achieved by looking at top-of-the-income statement metrics instead of something such as price-to-earnings.

Based on its latest data, Bilibili has a price-to-sales ratio of around 1.37x. The ratio isn't bad, but we think it's high given the economic and political risk embedded in China. In our view, a price-to-sales ratio below 1x is warranted at this time because we don't think the company nor China's economy have upward growth trajectories that would justify a price-to-sales ratio above 1.00. Besides, consider the sector median price-to-sales ratio of 1.28x is below Bilibili's.

| Data Point | Value |

| 2023 Sales | $3.2 billion |

| Market Capitalization | $4.37 billion |

| Price-to-Sales Ratio | 1.37x |

Sources: Seeking Alpha, Bilibili

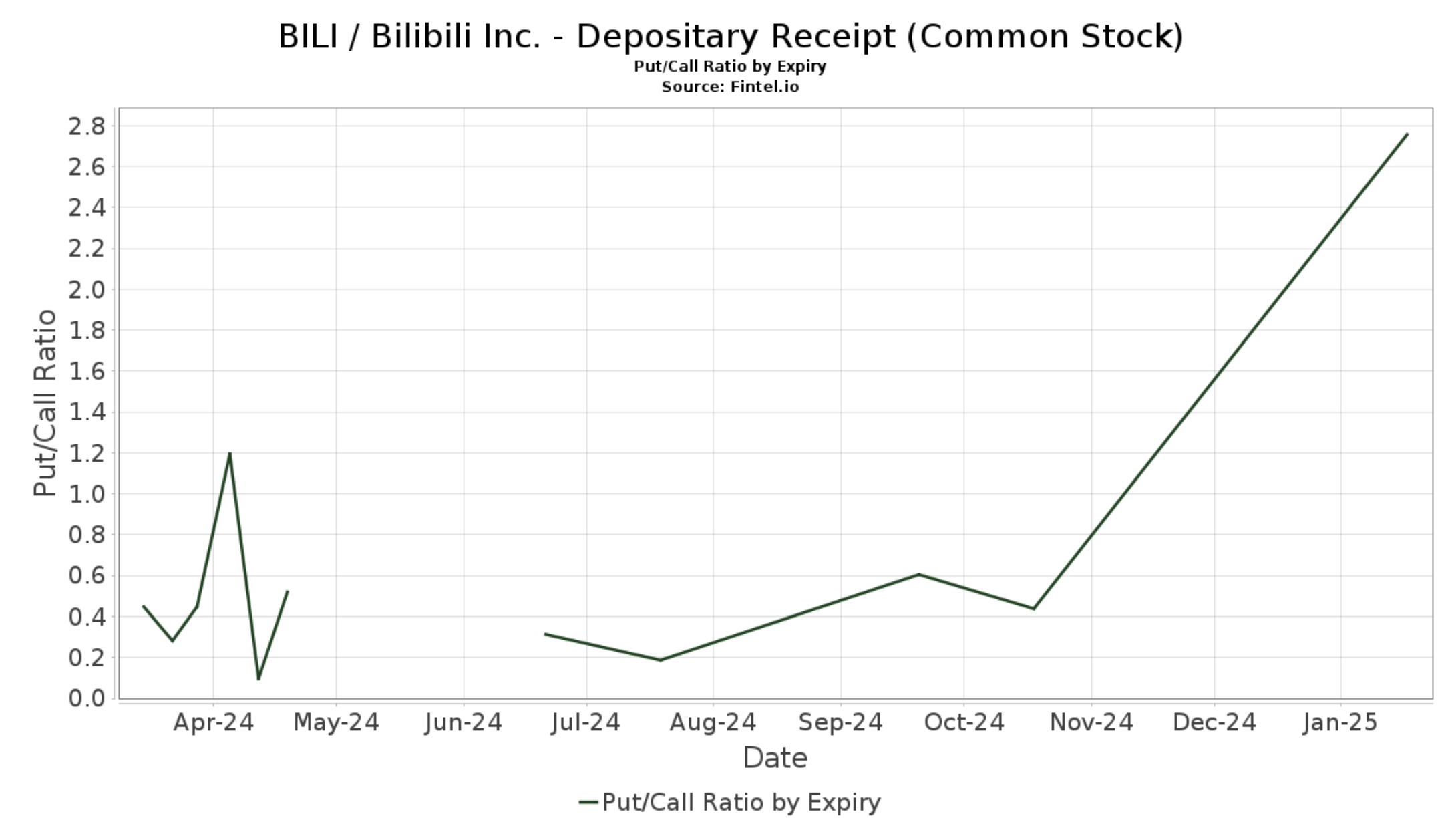

A technical analysis shows that options traders hold a bullish outlook on Bilibili as it possesses a Put/Cal ratio of 0.6x. However, the Put/Call ratio is a countercyclical metric. As such, we would not be surprised to see options activity flip in the near future.

Fintel

In essence, fundamental and technical indicators suggest Bilibili stock has price concerns. A more comprehensive analysis of Bilibili's valuation would be ideal, but a summation paints a sad picture.

Our previous analysis of Bilibili argued that its robust idiosyncratic growth, driven by its end market and novelty, would send the stock surging. However, we downgrade the stock to sell based on its latest earnings report and our outlook on systematic factors driving the firm's earnings. Moreover, we consider Bilibili overvalued as fundamental and technical indicators stack up against it.

Consensus: Sell/Market Underperform