kyoshino

kyoshino

The building blocks of modern society are dependent on basic raw materials such as oil, natural gas, steel (iron ore), copper, fertilizers, and now lithium and rare earths. However, the natural resource extraction business is capital intensive with long investing cycles and subject to volatile prices given the commodity (highly interchangeable products) nature of the product. Most commodity prices reflect a short-term, even daily, supply and demand balance. Add to this the political risk of drilling or mining in less-than-ideal rule-of-law jurisdictions and the business is downright risky. To this end, I analyzed the BlackRock Resources & Commodities Strategy Trust (NYSE:BCX) closed-end fund and came away with a neutral view.

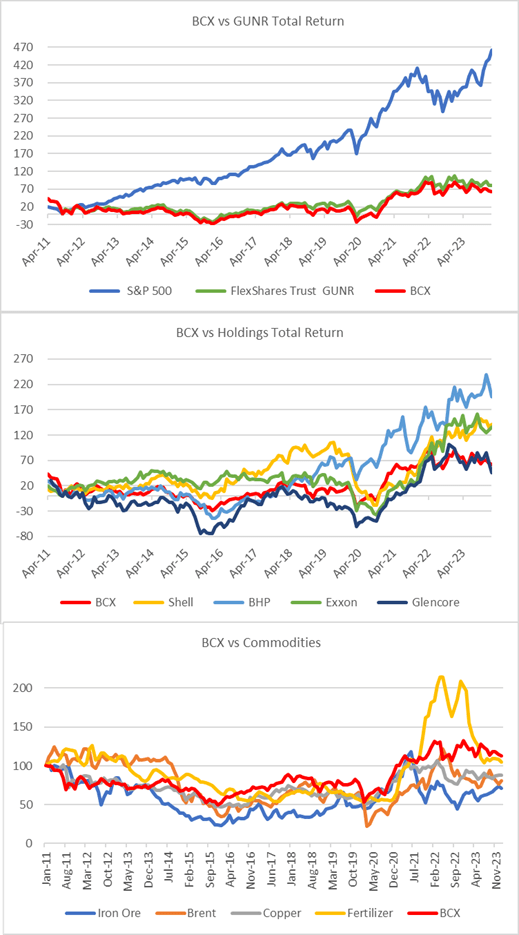

I compared the fund's total return vs. a peer, the SP500 (SPX) as well as several top oil and mining companies and the underlying commodities. One thing is evident, long-term commodity holdings are a poor choice given the volatility and lack of cash flow, earnings, and dividend compounding. Although there are funds that build options and forward contracts to extract income. The other clear conclusion is that the sector systematically underperforms the broader market, which begs the question, why bother with raw material stocks at all?

BCX Performance (Created by author with data from Capital IQ & Bloomberg)

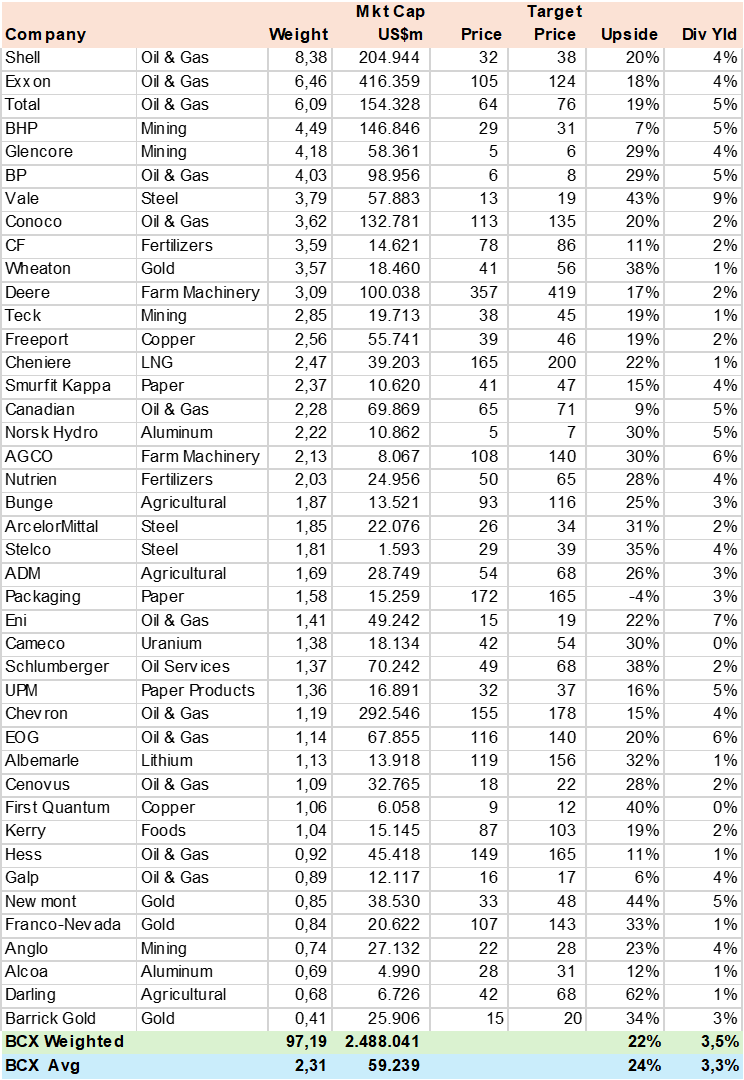

The closed-end fund is actively managed, utilizes option call writing to enhance income, and has a managed distribution plan (MDP) equal to about an 8% yield of which approximately 30% has come from ROC (return of capital) i.e., the call premium income and dividend flow from holdings does not always cover distribution. The fund has almost always traded at a 10% or more discount to NAV. I found BlackRock's disclosure regarding the call strategy and more importantly the MDP poor.

BlackRock

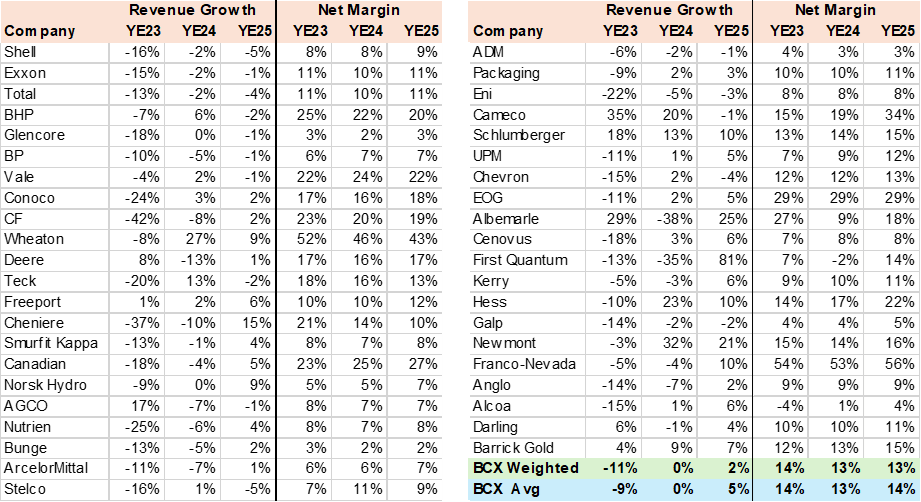

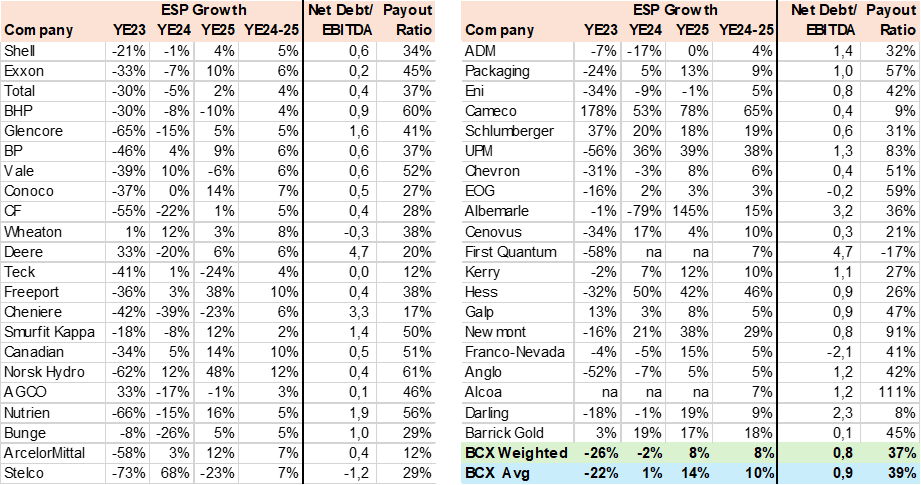

I gathered consensus estimates for 97% of the fund's AUM to measure weighted upside and dividend yield. As can be seen, the market has a very positive valuation view with a 22% upside potential based on consensus price targets. The fund has approximately 38% in Oil & Gas, 38% in Mining (iron ore and copper), and 21% in agricultural-related inputs such as fertilizers, machinery, and trading.

BCX Consensus Price Target (Created by author with data from Capital IQ)

While the consensus has very positive upside projections for the fund's holdings, the revenue forecasts are poor with zero growth in 2024 and 2% in 2025. This is likely due to the commodity price spikes post-pandemic and continued weakness into 2025. As commodity producers, they are price takers and there is not much this sector can do on the revenue side, except add volume or capacity. The main focus is on costs, to be able to weather any severe price downturn to at least break even.

BCX Consensus Revenue & Margins (Created by author with data from Capital IQ)

As can be imagined, with low revenue growth and margin gains the fund's holdings produce -2% EPS growth estimates for 2024 and a modest 8% in 2025 boosted by share buybacks most likely. While this is not a growth portfolio the sector does have ample free cashflow generation with low leverage and plenty of room to increase dividends or share buybacks given the 37% payout ratio. However, buybacks do not always translate into higher prices or more dividends for the fund. Cameco Corporation (CCJ) stands out with a very high and consistent growth rate due to the current Uranium demand cycle.

BCX Consensus EPS Growth & Leverage (Created by author with data from Capital IQ)

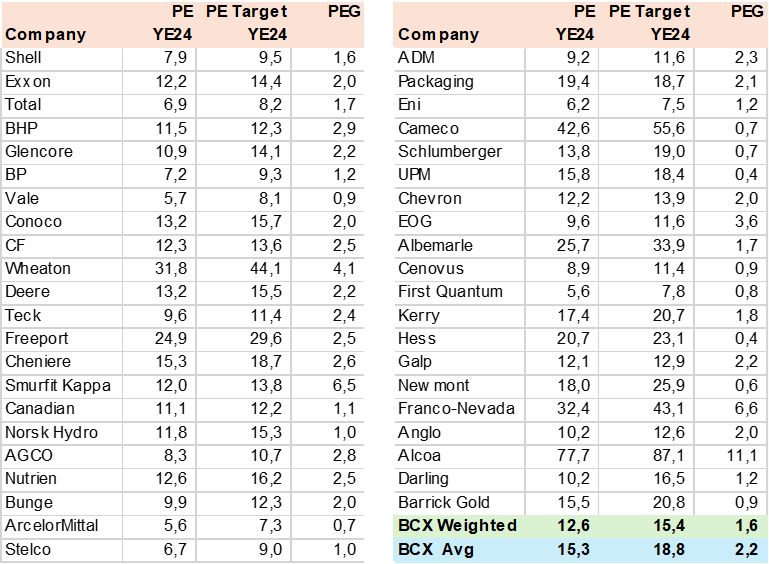

The consensus has a significant multiple expansion embedded in price targets that is not readily justifiable unless risk-free rates, i.e., Fed rates decline, in my view. Absent EPS growth, for which the stocks need commodity price gains, the valuation can come from higher free cash flow and lower discount rates. Relative to EPS growth, the fund is priced at a 1.6x PEG which in my view is reasonable given the volatile nature of the commodity business. I would most likely not be able to assign a higher PE unless the companies produced far higher dividends.

BCX Consensus Valuation (Created by author with data from Capital IQ)

I Rate BCX a Hold. The current portfolio reads like a who's who of the oil and mining sector with a strong upside under stable commodity prices and a lower-rate environment. However, as an actively managed fund with a 90% turnover, I am not assured that this portfolio will not change. The MDP requires or forces the managers to seek short-term capital gains or face deteriorating NAV. Finally, the raw material sector has not outperformed the broader market and given its cyclical and volatile nature, it is unlikely to be able to do so. There are always individual stock exceptions but as a whole predicting the price of oil, iron ore, gold, copper, potash, etc. on a long-term basis is daunting.