Marina Demeshko

Marina Demeshko

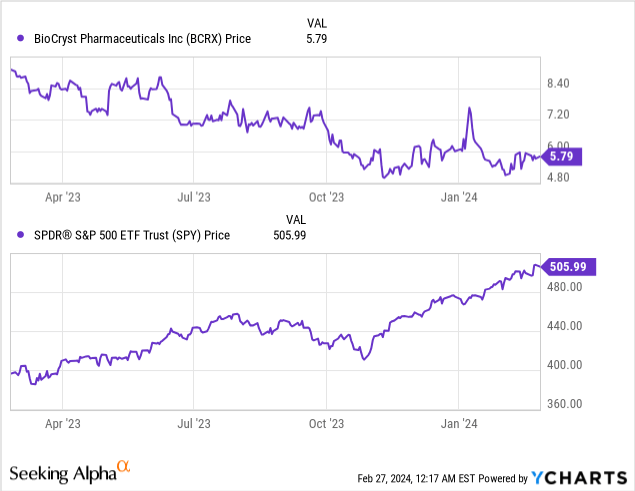

BioCryst Pharmaceuticals, Inc.'s (NASDAQ:BCRX) stock has dropped 29% since my initial "Sell" recommendation in March 2023. This is almost the opposite of the general market (SP500), which has increased 28% during the same time period.

Seeking Alpha

Orladeyo, an oral drug, for the prophylactic treatment of hereditary angioedema [HAE], doesn't have an easy path on the market. It faces stiff competition from competitors like Takeda's (TAK) Takhzyro and it is evidently costly to market (as evidenced by high SG&A expenses).

Orladeyo produced $326 million in revenue last year, but this hardly made a dent in the company's overall financial picture, which is dominated by net losses. In Q4, Orladeyo revenues totaled $90.88 million, up 30% year over year. However, these gains were offset by SG&A increasing 28.37% year over year, amounting to $64.382 million in Q4. The company attributed this rise to "increased investment to expand and enhance the U.S. commercial team and international operations." Meanwhile, R&D costs fell to $70.1 million from $73.2 million. Recall that BioCryst discontinued the BCX9930 and BCX9250 programs a while ago, so R&D costs remaining relatively high are perplexing to me.

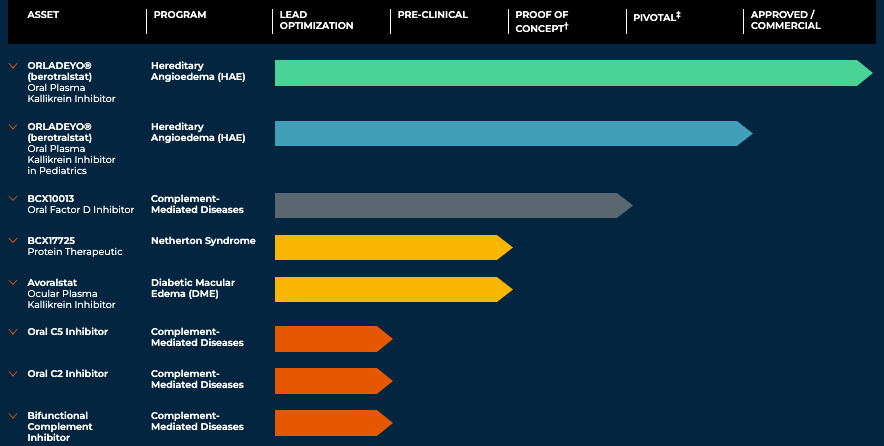

BioCryst's pipeline

Granted, they are also testing Orladeyo in pediatrics, but most of their work is preclinical.

In total, BioCryst reported another loss in Q4 of $61.7 million, compared to $71.5 million the previous year. A slight improvement, but nothing that excites anyone.

The company is still projecting $1 billion in peak annual revenue for Orladeyo before its key patents/exclusivities expire. A key exclusivity, Orladeyo's New Chemical Entity, expires next year. BioCryst then maintains a number of related patents that could extend Orladeyo's exclusivity through 2039.

Although certainly possible, I believe the $1 billion estimate is unlikely. BioCryst projects Orladeyo revenue of $380-$400 million for this year. The higher end of that estimate suggests no more than 25% growth from last year. So, its growth is slowing and drugs do not grow in linear terms for years on out. Moreover, the treatment landscape for HAE, five years from now, figures to be different than it is now.

Overall, the Q4 update is "more of the same" in my eyes. The company's progress is uninspiring and there's no reason yet to change confidence in its prospects.

Turning to the company's financial health, as apparent in the limited information provided within their 8-K, the combined liquid assets of cash, cash equivalents, and investments total $388.9 million. When juxtaposed with the company's liabilities, including a secured term loan of $303.2 million, a royalty financing obligation of $531.6 million, and an accumulated deficit of $1.68 billion, a stark contrast is evident. I am unable to calculate a current ratio in the absence of an annual report (and detailed balance sheet) at the time of writing, but the substantial liabilities point to a challenging liquidity situation.

The monthly cash burn, derived from a quarterly net loss of $61.7 million, suggests a monthly burn rate of approximately $20.6 million. This calculation indicates a cash runway of about 18.9 months, assuming no change in the burn rate or additional capital inflows. It's imperative to acknowledge that these figures are based on past performance and may not accurately predict future financial health.

The likelihood of requiring additional financing within the next twelve months is medium, considering the need to sustain operations and address substantial debt obligations.

Notably, BioCryst has the opportunity to borrow an additional $150 million from the Pharmakon loan, but has no plans to do so at this moment. Moreover, the company expects to be profitable on an EPS basis with positive cash flow in 2026.

According to Seeking Alpha data, BioCryst has a market capitalization of $1.17 billion. Analysts project a significant revenue growth trajectory, with sales expected to increase from $397.81 million in 2024 to $623.52 million by 2026, underscoring robust growth prospects. However, BCRX's stock momentum is lagging, with a -39.51% performance over the past year compared to the SPDR® S&P 500 Trust ETF's (SPY) +26.83%.

Per Fintel, the short interest is substantial at 29,043,720 shares (16.28% of float), representing a high level of market skepticism. Institutional ownership is concentrated, with a notable dynamic of 3,888,448 new positions versus 9,455,409 sold out positions, highlighting a mixed institutional sentiment. Prominent institutions, such as Avoro Capital Advisors and State Street, show increased interest, while Baker Bros. reduced their stake. Insider trades over the past three and twelve months reveal positive net activity, with more shares purchased than sold, suggesting insider confidence. Considering these factors, BCRX's market sentiment leans "fragile." Poor stock performance, high short interest, and institutional selling dominate the story.

BioCryst remains a "Sell" due to the ongoing concerns I've expressed over the past year. Its modest revenue gains are being immediately offset with increases in SG&A expenses. This tells me that the drug is not "selling itself" and is requiring significant upkeep. Moreover, given the lack of progress of their pipeline outside of Orladeyo over the past few years, the R&D expenses remain surprisingly high. Moreover, I believe analyst and management revenue projections for Orladeyo in the coming years to be overly optimistic based on the Orladeyo's performance thus far and the competitive landscape for HAE.

There are risks to my "Sell" stance. For one, BioCryst's stock is not ridiculously valued at a $1.62 billion enterprise value. Two, 20-30% revenue growth for Orladeyo, while not inspiring in my eyes, is nothing to shrug at. Three, Orladeyo is a differentiated drug in that it gives patients the only oral option for prophylactic treatment. Finally, BioCryst's R&D efforts, while costly, may end up paying off. Any positive clinical developments could lead to substantial gains in its stock and help alleviate some of its financial challenges.

To sum up, BioCryst has not yet made the breakthrough that the market has been waiting for. It feels appropriate to exercise caution and look for opportunities elsewhere in the stock market till then.