E_Y_E

E_Y_E

Bath & Body Works, Inc. (NYSE:BBWI) is a leading name in home fragrance and personal care, with 1,850 locations in North America and 480 franchises internationally. Despite a decline in sales in 2022 and 2023 due to inflationary pressure, BBWI's products are considered an affordable luxury, and the firm seems to remain resilient as compared to its peers. In addition, their loyalty program has been proven effective, with a strong customer base that accounts for nearly 80% of 2023 sales and is still growing. The Men's shop has emerged as one of the fastest-growing segments, tapping into the expanding male grooming market, while its candles and sanitizer segments have normalized as consumer behavior shifted post-pandemic. My relative valuation has brought me to a target share price of ~$51.21, with an upside potential of ~16%. Therefore, I am recommending a buy.

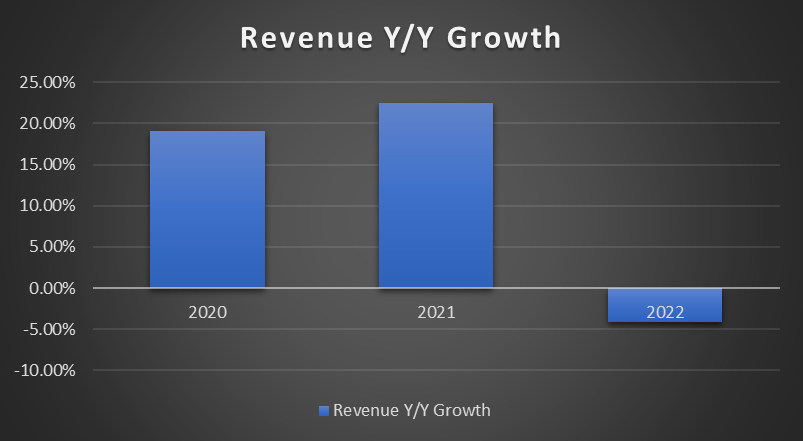

In 2020, revenue was up ~19% year-over-year. This strong growth was attributed to strong sales across all of BBWI's merchandise categories, which were driven by strong demand for soaps and sanitizers as well as home fragrances and body care. In 2021, revenue continued its strong growth momentum and increased 22.5% year-over-year. This strong growth was driven by the reopening of stores in 2021 that were closed in 2020 due to COVID-19. However, in 2022, revenue declined 4.1%, driven by a decrease in average dollar sales and a decrease in orders in the direct channel caused by a challenging macroeconomic environment, such as high inflation, which caused customers to become increasingly sensitive to prices in 2022.

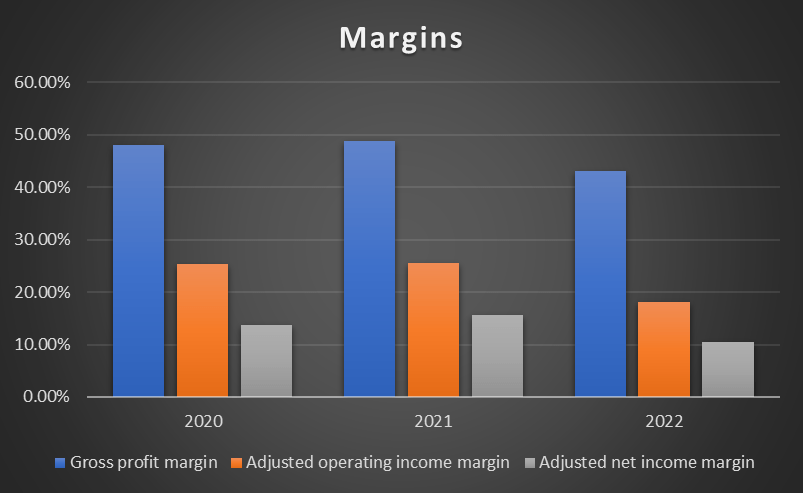

In terms of margins, it remained robust in 2020 and 2021 but contracted in 2022. Gross profit margin contracted to ~43% due to high inflation, which severely impacted its merchandise margins as product costs, labor costs, and transportation costs went up. As a result of gross profit margin contraction, it negatively impacted its adjusted operating income margin and adjusted net income margin. Its adjusted EPS from continuing operations fell from $4.51 to $3.40.

Author's Chart Author's Chart

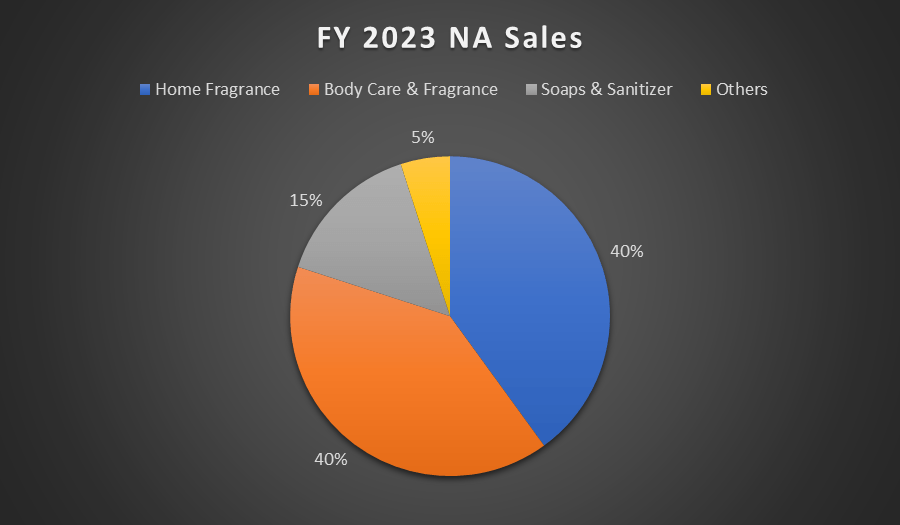

BBWI sales [North America] can be broken down into four segments, Home Fragrance, Body Care & Fragrance, Soaps & Sanitizer, and Others. Home Fragrance and Body Care & Fragrance make up 40% of sales each. 15% of it falls under Soaps & Hand Sanitizers, while Others make up the remaining 5%. Home fragrance has fallen slightly in the low-single digits. The wallflower sales remain robust, with wallflower bulbs seeing growth in the low single digits, driven by higher units and strong holiday fragrance sales. BBWI has captured unit share in home fragrance and continues to be a market leader in the field. Body care has shown a low single-digit increase in Q4, mostly driven up by its Men's sub-category. It has been rapidly growing in this category, especially in deodorants and grooming.

Author's Chart

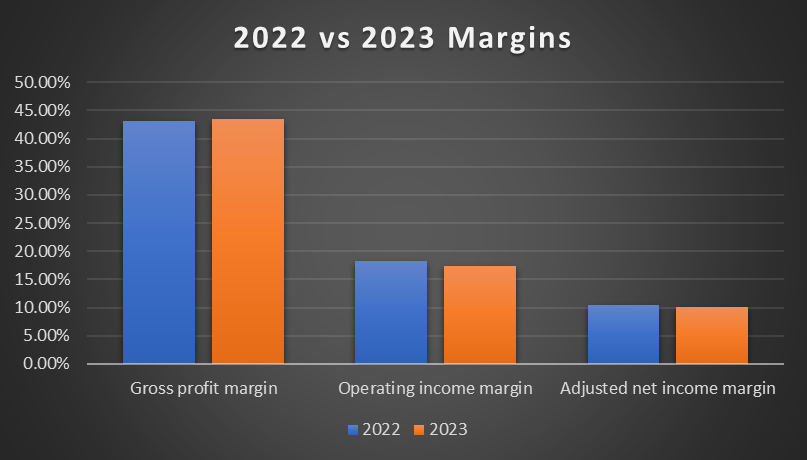

For FY2023, total revenue was down ~1.7% due to macroeconomic pressures, such as high inflation, affecting consumer spending on discretionary items. In addition, for 2023, management also stated that its candles segment, a significant product line for BBWI, is experiencing normalization. The reason for such a shift was because consumers were spending less time at home after COVID-19 had eased. Apart from candles, its sanitizer segment, which surged during the pandemic, is also experiencing a shift back towards more normalized levels. Although they are normalizing, candle and sanitizer sales are still above pre-pandemic levels. In addition, despite the normalization, BBWI is still the market leader in the candle segment, and it is also continuing to win market share in the sanitizer segment. Moving down its P&L, 2023's margins remained robust when compared to 2022, as all three margins were essentially the same year-over-year.

Author's Chart

BBWI prioritized its investment in the loyalty program, which was released in August 2022. Members are awarded points that are dependent on their purchasing activity and will expire when inactive. Points can be redeemed for awards, which the members can use on their next purchase. Those who redeem rewards have been proven to spend more with the brand. Point accelerators were introduced in the most recent quarter, and the idea of this initiative is to encourage customers to redeem more frequently.

BBWI has proven to have a strong loyalty program, with over 37 million active loyalty members of the ~45 million members as of year-end 2023, and it has grown over 30% year-over-year and 3% from its previous quarter. The large, loyal customer base accounts for nearly 80% of FY23 sales in the U.S. The holiday seasons have contributed to a higher level of enrolment in the loyalty program, especially on the bigger days. They have been emphasizing their marketing investments to boost customer acquisition and retention and will continue to do so by investing at an equivalent level in 2023. The program has been effective in its role in customer acquisition and retention, allowing BBWI to cultivate lasting relations with their customers and drive sales and long-term growth.

Statista

The Men's shop has been one of the fastest-growing segments in the past 3 years, offering customers their best-selling fragrance, body care, and hair care products. Tapping into the male market is no easy feat, especially for BBWI, which is still fundamentally targeted towards women. This growing men's line has proven that BBWI has effectively diversified its market into the men's category and reduced its reliance on a single demographic. Creating brand awareness among new consumers by drawing a younger and more diverse crowd in. There are also greater cross-selling opportunities for both men and women, driving more store visits and website traffic.

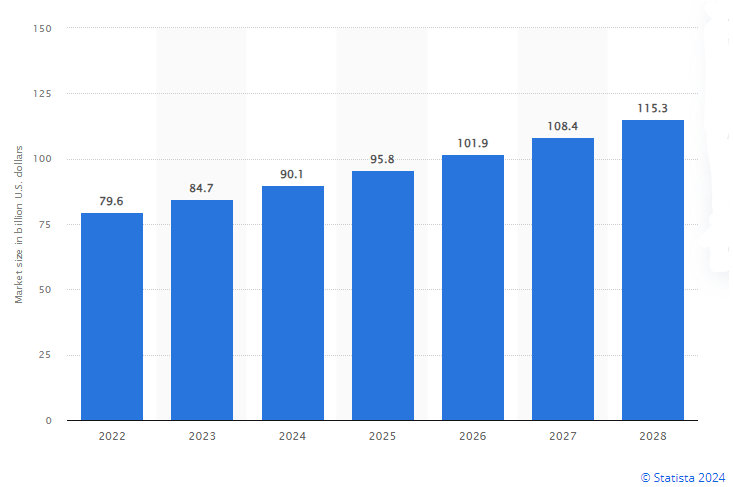

The male grooming market has been growing, with increased awareness and acceptance of men's skincare and wellness products. The global market for male grooming is projected to increase by ~44% by 2028 as compared to 2022. Men are starting to spend more on grooming products, putting more focus on their self-confidence, and putting more effort into feeling more attractive and youthful.

Although there is still some barrier for men to prioritize grooming, BBWI has made substantial investments in the male product line, which has been proven successful thus far. BBWI has initiated marketing campaigns to create greater awareness in this category by partnering with MVP athletes and influencers for promotion and pop-up stores to invite consumers to experience the wide variety of their offerings. Therefore, BBWI capitalizing on the growing male grooming trend is a strategic move that opens up an additional revenue stream and thus boosts the firm's sales and profitability.

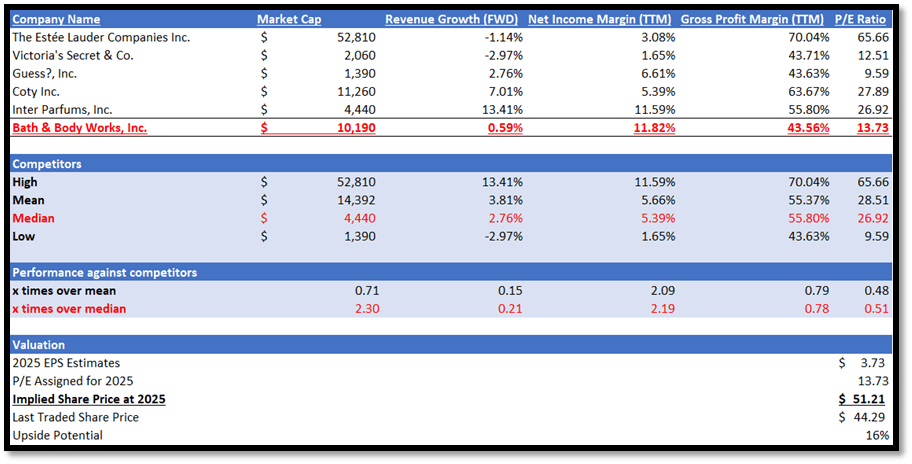

I will be comparing BBWI with its peers in terms of forward growth outlook and TTM profitability margins. In terms of growth outlook, BBWI significantly underperformed its peers. It has a forward revenue growth rate of only 0.59% vs. peers' median of 2.76%.

In terms of TTM profitability, BBWI outperformed its peers in terms of net income margin TTM. It has a net income margin TTM of 11.82% vs. peers' median of 5.39%. In addition, BBWI did so with a lower gross profit margin TTM of 43.56% vs. peers' median of 55.80%.

Currently, BBWI is trading at a forward P/E ratio of 13.73x, which is lower than its peers' median of 26.92x. Given its underperformance in forward revenue growth outlook, which is 79% lower than peers' median, I argue that it is fair for BBWI to be trading at a discounted P/E.

For 2025, the market revenue estimate for BBWI is ~$7.69 billion, while the 2025 EPS estimate is $3.73. Given the growth catalysts discussed above, the market estimates are justified as they echo the same sentiment. By applying 13.73x to its 2025 EPS estimate, my 2025 target share price is ~$51.21, which gives us an upside potential of ~16%.

Author's Relative Valuation

A downside risk would be the lingering inflationary pressure that may continue to weaken consumer demand. Policymakers have implied a rate cut this year, but not immediately. After raising the interest rate in 2022 and 2023 in an attempt to control inflation and slow growth, policymakers have indicated that they need greater affirmation that inflation is under control before they start to make the cuts in 2024.

What BBWI needs is a recovery in the macro environment to help improve consumer confidence so as to increase discretionary spending on beauty and personal care items. However, the lingering inflation at the start of 2024 is a concern and may cause policymakers to hold the interest rate or even raise it in order to conquer inflationary pressure. This scenario may further delay the recovery in consumer spending and may escalate BBWI's operational costs, thereby impacting both demand for its products and profitability.

In conclusion, BBWI's revenue has been volatile as the past two years' revenue has been falling due to a challenging macro environment. Despite these challenges, BBWI has maintained a strong customer following through its effective loyalty program and has been actively tapping into and capitalizing on the fast-growing men category. From my relative valuation, my target price is ~$51.21. When compared to its last traded price, this represents an upside potential of 16%. Therefore, with strong double-digit upside potential and the growth catalyst as discussed, I am recommending a buy rating for BBWI.