Ryan McVay/DigitalVision via Getty Images

Ryan McVay/DigitalVision via Getty Images

In December, we suggested a speculative buy that we considered a high-risk, high-reward play. At our service, we feature a secondary trading room focused on highlighting a high-risk, high-reward, speculative idea once or twice a month. A number of smaller AI-related names have been dabbled in, but we publicly discussed BigBear.ai Holdings, Inc. (NYSE:BBAI).

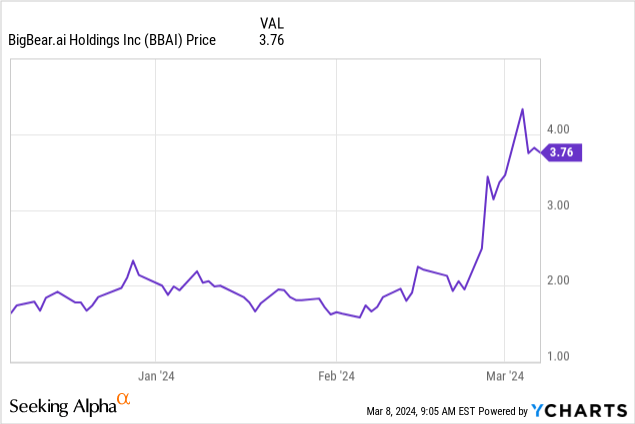

In our coverage we cited the stock being one that we thought could jump back over the $2 level with ease when it was $1.70. Well, the stock actually surged with a recent inflation of the balloon of AI-related names. In fact, the stock more than doubled.

Of course, all of these gains came in the last month, easily knocking down our trading targets in the $2.40 range, and surging over $4.00. Now, it looks like BigBear.ai may be heading into hibernation mode. We now downgrade that stock to hold on the back of its just-reported Q4 earnings. The AI momentum is strong, and wise traders who follow our teachings likely already took significant profit, but it is a good strategy to leave some profit on for a house position for the long term. Short term, it is just going to be volatile, and that can be tough to navigate. We targeted the buy at a very opportune time, but now it is wise to hold. We are not buyers at these levels. We think it retraces.

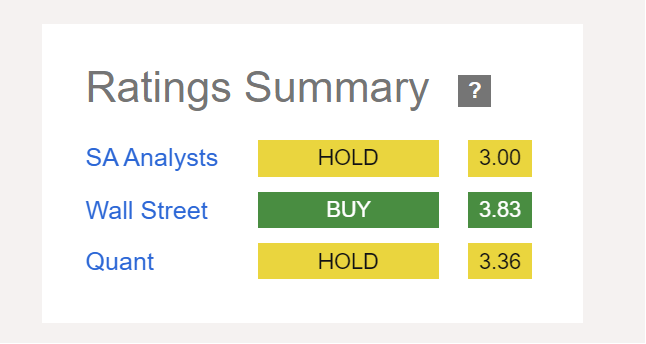

For the record, the Seeking Alpha Quant Rating and Seeking Alpha Analyst Rating are a hold for BBAI. But the Wall Street Analyst's Rating is still a buy. However, we do believe you may be seeing some analyst action on the stock perk up.

Seeking Alpha Ratings BBAI

Look, we still love the operations and what they do here. BigBear.ai products translate data into information. Information is power in today's society. And while there are many competitors in this space, the key is that their offerings help customers make complex decisions, and improve efficiency. Their algorithmic-powered decision intelligence solution has been taken up by more and more customers in the global supply chains & logistics, autonomous systems, and cyber intelligence fields. This includes the U.S. Intelligence Community and other branches of the U.S. Federal Government.

When we became speculatively bullish, we noted that it had started to work with Amazon.com, Inc. (AMZN) via its AWS, allowing AWS ProServe customers to access BigBear's ProModel AI-driven warehousing solutions. Further, there was an interesting acquisition of Pangiam Intermediate to add facial recognition and advanced biometrics to BigBear.ai's computer vision capabilities and help BigBear open up the vision AI industry.

The company continues to work to grow its customer base, but the balance sheet is a concern here. In the just-reported quarter, revenue was essentially flat from a year ago. It came in at $40.6 million, up just 0.4% from a year ago. That is not good enough to justify the recent momentum. And it missed consensus by nearly $3 million. Now, we noted in Q3 BigBear swung to its first net income positive quarter since going public. However, the company lost money in Q4, but did deliver its second straight quarter of positive EBITDA. The gross margin was a significant expansion from 24.7% in Q3, rising to 32.1%, which was also up from 29.2% in the year-ago quarter. The company saw better margins on fixed-price contracts while mixing out older lower margin contracts that have been completed.

There are other reasons to be positive, justifying a hold here. BigBear has been reducing expenses, although this quarter relative to revenue, there was elevated SG&A spending of $18.2 million versus $15.6 million. However, recurring SG&A is on the decline, down to $12.3 million from $16.1 million, which led to positive EBITDA and earnings. The overall cost of revenue was down, research and development was up, and there were very few restructuring charges, but elevated transaction expenses. All told, operating loss was $8.6 million, much improved from a loss of $26.3 million a year ago, but about on par with last year if we back out a goodwill charge of $18 million last year.

Adjusted EBITDA was positive $3.7 million, but this was a big year-over-year improvement compared to a loss of $2.5 million a year ago as there were reduced operating expenses. Net loss was $21.3 million, improved from losses of $29.9 million.

But this is a debt-heavy company. The balance sheet is quite levered. Folks, there is $194 million of long-term debt and $1.2 million of short-term debt. Considering the debt and the EBITDA, you can see the significant leverage. A few days ago we saw an investor exercise 13.9 million warrants which generated $33.2 million in proceeds for the company. Of course, that was dilutive, as new shares were issued. BigBear also issued 9.0 million new warrants with an exercise price per share equal to $4.75 following this development. Commenting on the quarter, CEO Mandy Long said in the release:

We entered the year in a different position than many other companies that are playing a role in the transformative potential of artificial intelligence. After joining in October 2022, I spoke openly about needing a foundational year to overhaul our operating structure, wind down contracts that did not meet our business objectives, reset the strategic priorities of BigBear.ai, and manage uncertainty in a volatile macroeconomic and geopolitical environment. In short, we had to do the hard work to get our house in order. We stand here in early 2024 knowing that we did what we said we would do. With the completion of the Pangiam acquisition and incremental cash proceeds of $54M from warrants exercised in Q1 2024, we are well positioned for healthy growth in the year ahead."

We do believe the acquisition will fuel growth, but the upside from here may be limited with the added dilution and the leverage on the balance sheet. Revenue was guided to between $195 million and $215 million, and that includes revenues from the acquisition. As we move forward, there remain risks. If management does not execute, BigBear might not be able to acquire new contracts. New contracts are not guaranteed. There are tons of competitors trying to get "their tech" to be used. Operationally, issues can arise which lead to failure to deliver on contracts. Free cash flow is negative, so the cash burn means ongoing dilution is expected.

All told, we flagged BigBear.ai Holdings stock as a speculative, high-risk, high-reward play. That worked out, and traders made good money here. Consider taking profit, and holding a house position to follow the story long term. Short term, we expect pressure.