Su Arslanoglu/E+ via Getty Images

Su Arslanoglu/E+ via Getty Images

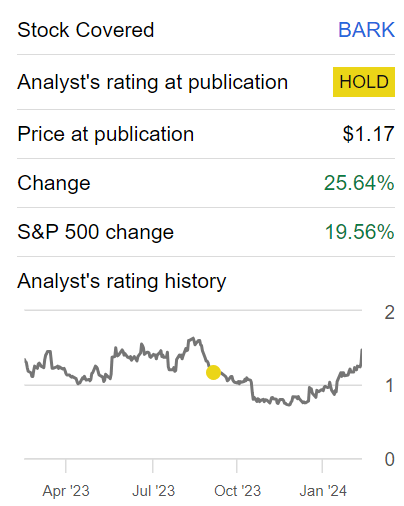

BARK, Inc. (NYSE:BARK) is starting to regain its footing, even though this investment thesis is demonstrably not blemish-free, and is led by a management team that has misfired on many occasions in the past.

Furthermore, not only is the stock trading at just over $1, meaning that it's not something an institution is likely to invest in. But also, the business just recently regained compliance with the NYSE. This means that this stock is still perceived to be a penny stock and one that's in the penalty box. And in the market, where there's belief there's truth. Consequently, if people think this is a penny stock, they'll trade it as such, with massive swings down and up.

Hence, think about that aspect, when I rate this as a tepid buy.

Back in September, I concluded by saying my neutral analysis by saying,

[...] the outlook for BARK is uncertain. With both challenges and opportunities on the horizon, I'm eager to follow this story more closely to see how it develops from this point.

Author's work on BARK

I was neutral at the time. And even though the share price is up 25% from that analysis, the market as a whole is up 20%, so this small-cap has not meaningfully outperformed the index. And my neutral recommendation avoided a lot of pain, as the stock fell significantly after that analysis was published.

BARK sells pet products, specializing in toys and consumables like treats. They've are focused on improving their business and expanding their product range. BARK operates a unified online platform, where customers can find a variety of pet products and subscribe to receive them regularly.

BARK's near-term prospects appear fair. The company's strategic focus on improving unit economics and strengthening its financial health is evident in its fiscal Q3 2024 results. With total revenue reaching $121 million and a notable 280-basis point improvement in gross margin, BARK has demonstrated its ability to navigate with some success in a competitive market.

While BARK demonstrates positive momentum, headwinds are also present. A notable challenge is the stabilization in the core toy category, affecting both the direct-to-consumer and commerce segments.

Also, the overall industry growth in this category is subdued. The company is seeking to diversify its revenue streams and mitigate reliance on specific product categories.

Given this background, let's now discuss fundamentals and risk factors.

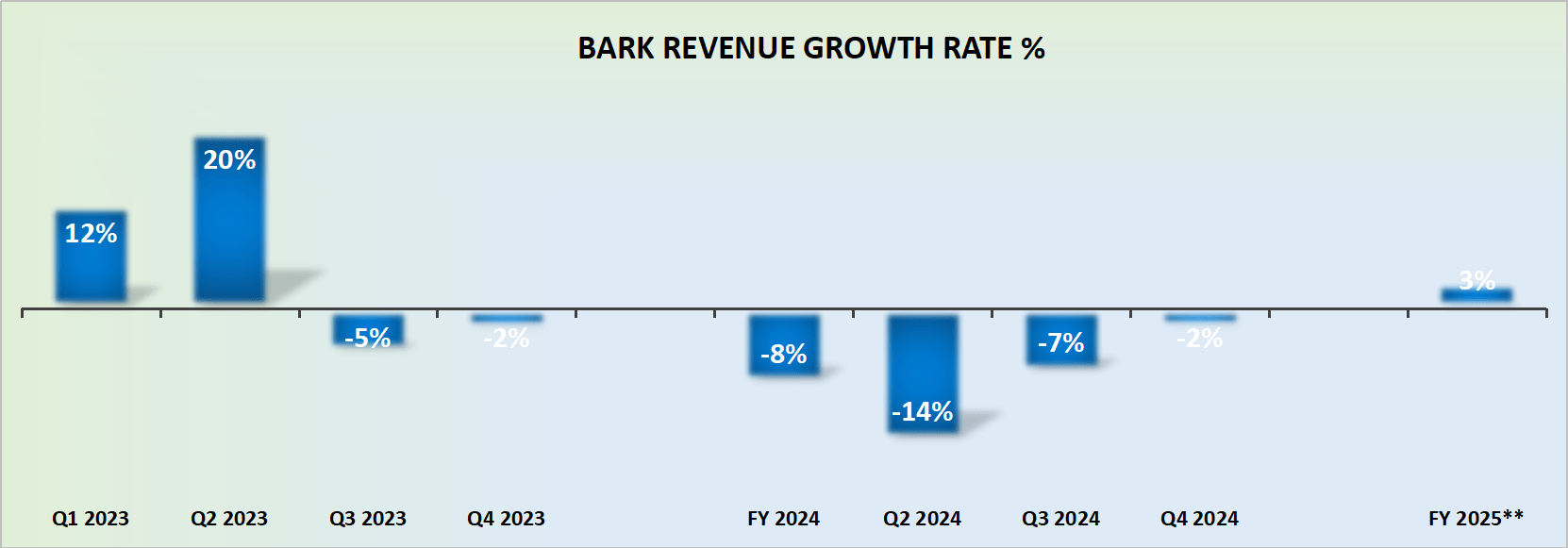

BARK revenue growth rates

During the earnings call, BARK's CEO said ''we believe we will return to top-line growth in fiscal 2025''.

How much growth can we expect? Realistically, I don't believe anyone expects much. I estimated 3% CAGR for fiscal 2025, since the comparables with the prior year are so easy, that as the company compares against this period, it should with relative ease report some topline growth.

The implications here are obvious. Management will be able to put forth a compelling story of how they've improved their prospects and turned around their operations, and convincingly describe how they've finally delivered some topline growth, for the first time in more than 7 consecutive quarters. And that's obviously nice to have.

Recall what BARK had previously said back in fiscal Q1 2024,

Beyond FY '24, we expect to deliver high single to low double-digit revenue growth in FY '25.

As we go through BARK's most recent earnings call, high single-digit growth is no longer the company's expectations

Simply put, BARK is the sort of company that has a history of overpromising and underdelivering, so keep that in mind too.

However, I don't believe this is where this bull case is found. That's what we turn to next.

BARK holds approximately 40% of its market cap as net cash. Yes, BARK holds $40 million of convertible debt, but offsetting this figure there's more than enough cash so that its net cash level stands at approximately $90 million. Hence, since BARK's market cap stands at $240 million this means there's a large amount of cash attached to its market cap.

And then, on top of that, consider this.

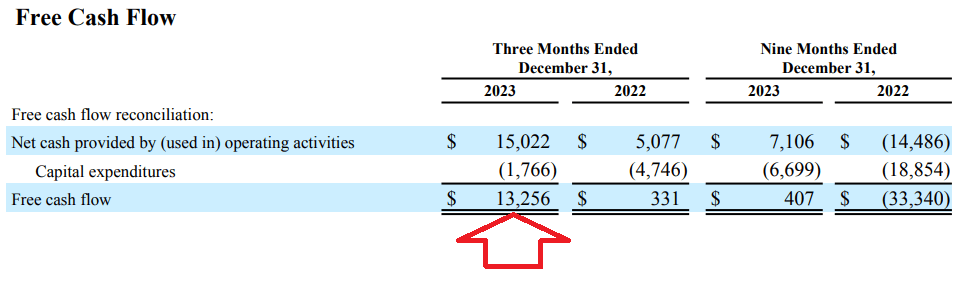

BARK Q3 2024

Now, you may contend that $11 million of that $13 million of free cash flow came from BARK liquidating inventory, so that's clearly not a recurring event. And I take that on board.

However, over the trailing twelve months, BARK generated $17 million of free cash flow, which again, has mostly been driven by liquidating excess inventory. So, that level of free cash flow will not repeat in the coming twelve months. And that would be a valid argument.

But the point to focus on here is that BARK is clearly not hemorrhaging significant free cash flow. Also, consider this:

BARK Q4 2023

In fiscal Q4 2023, the prior year's Q4, BARK delivered negative 3% EBITDA margins. Whereas its guidance for Q4 2024, its next quarter to be reported points to approximately 2% of adjusted EBITDA margins; 400 basis point expansion relative to the same period a year ago.

So, you are left with a company that has some growth next year, and is clearly on the path towards a full year of profitability.

For now, I estimate that BARK could see around $15 million of EBITDA in fiscal 2025, leaving the stock reasonably priced at 16x forward EBITDA.

In conclusion, upon closely examining its financials, the company boasts a strong position with around 40% of its market cap represented by net cash.

Despite concerns surrounding the sustainability of free cash flow derived from inventory liquidation, BARK doesn't exhibit significant cash flow challenges. Notably, its journey toward profitability is evident in the improving EBITDA margins, progressing from negative 3% in fiscal Q4 2023 to an anticipated 2% in Q4 2024. Priced at 16x forward EBITDA, with an estimated fiscal 2025 EBITDA of $15 million, BARK appears to be on a path to financial stability. Tepid buy rating.